- Food Ingredients & Additives

- Sea Salt Market

Sea Salt Market Size, Share, and Growth Forecast, 2026-2033

Sea Salt Market by Salt Type (Refined, Unrefined), Packaging (Bags, Drums & Sacks, Shakers, Glass Jars), Application (Regenerating Water Agent, De-Icing Agent, Detoxifying Agent, Antioxidant Agent), End-Use (Food Industry, Agriculture, Cosmetics, Animal Feed), and Regional Analysis for 2026-2033

Sea Salt Market Share and Trends Analysis

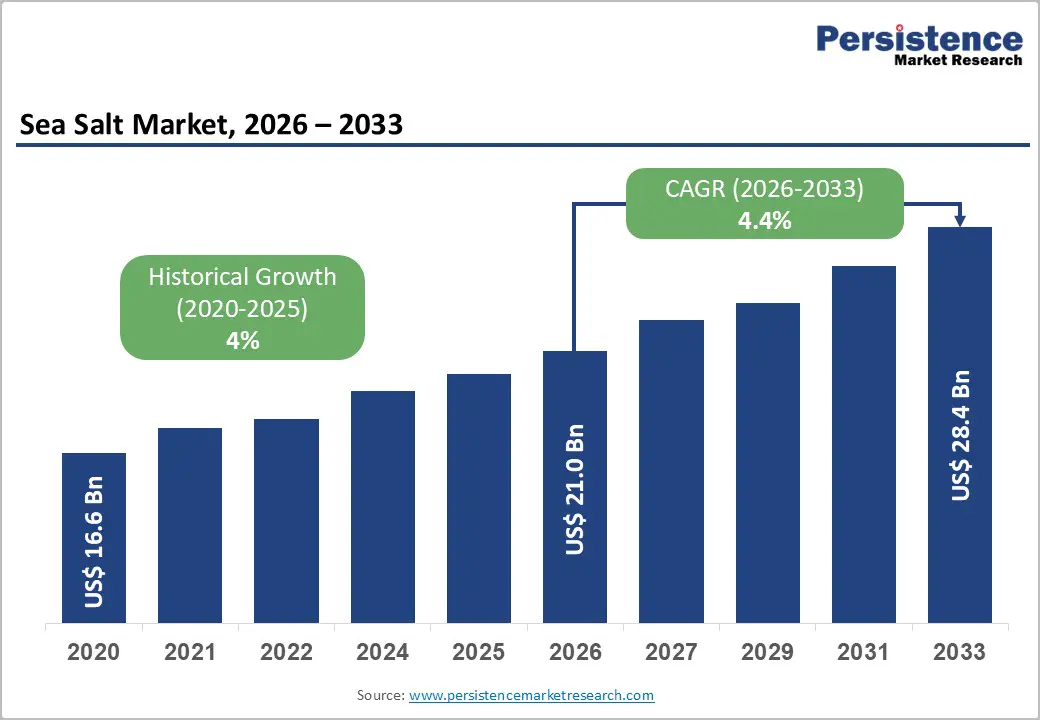

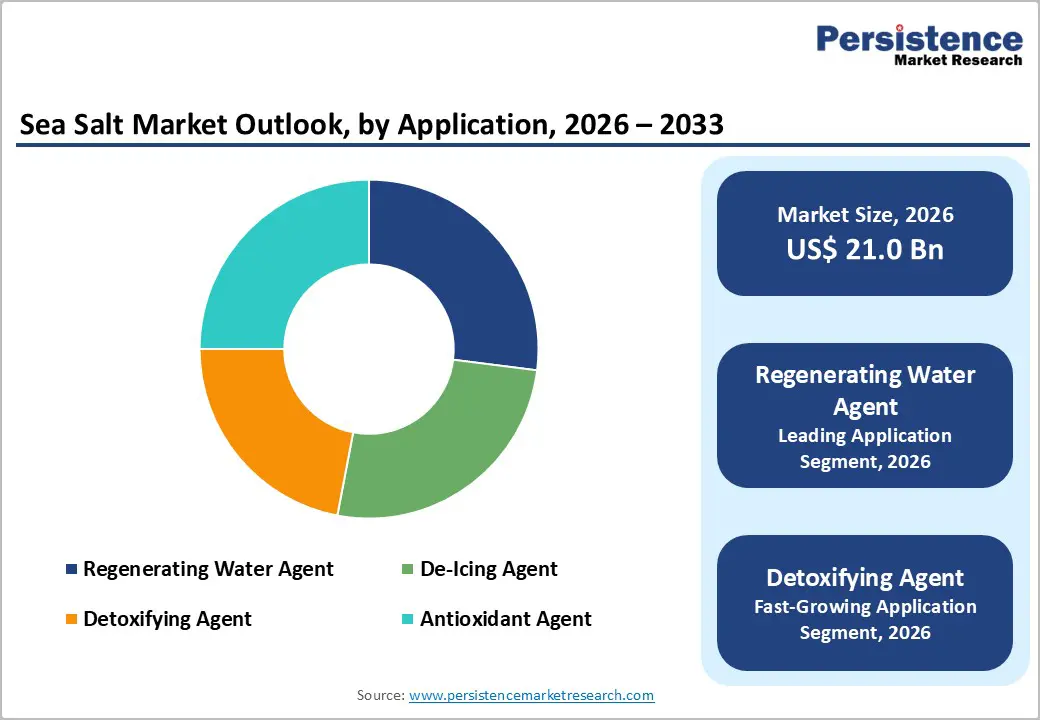

The global sea salt market size is likely to be valued at US$ 21.0 billion in 2026, and is projected to reach US$ 28.4 billion by 2033, growing at a CAGR of 4.4% during the forecast period 2026-2033. The market is undergoing steady expansion due to the indispensability of sea salt in food, industrial, and personal care sectors. Health-conscious consumers have increasingly chosen natural ingredients with rich minerals, bolstering clean-label preferences that shield the market from economic ups and downs.

Industrial uses, such as water-softening agents and de-icing solutions, have expanded applications, while global distribution networks continue to strengthen access. End-use areas such as cosmetics and animal feed can diversify revenue sources. Producers that can capitalize on these trends by emphasizing sustainable sourcing and versatile product forms, with future growth hinging on innovation in premium blends and targeted marketing to urban demographics.

Key Industry Highlights

- Application Outlook: De-icing is projected to lead with 27% share in 2026, fueled by municipal and infrastructure demand, while detoxifying applications are forecast to grow fastest at 5.9% CAGR through 2033, led by cosmetics and wellness adoption.

- Salt Type Dominance: Unrefined sea salt is expected to dominate with 63% revenue share in 2026, driven by natural and minimally processed food demand

- Fastest-growing Salt Type: Refined sea salt is projected to grow fastest, at a 4.8% CAGR through 2033, due to its use in industrial and water treatment applications.

- End-Use Leadership: The food industry is projected to account for 60% of market revenue in 2026, supported by large-scale food processing, whereas cosmetics is forecast to expand at a 5.6% CAGR through 2033, driven by rising demand for natural detoxifying and antioxidant ingredients.

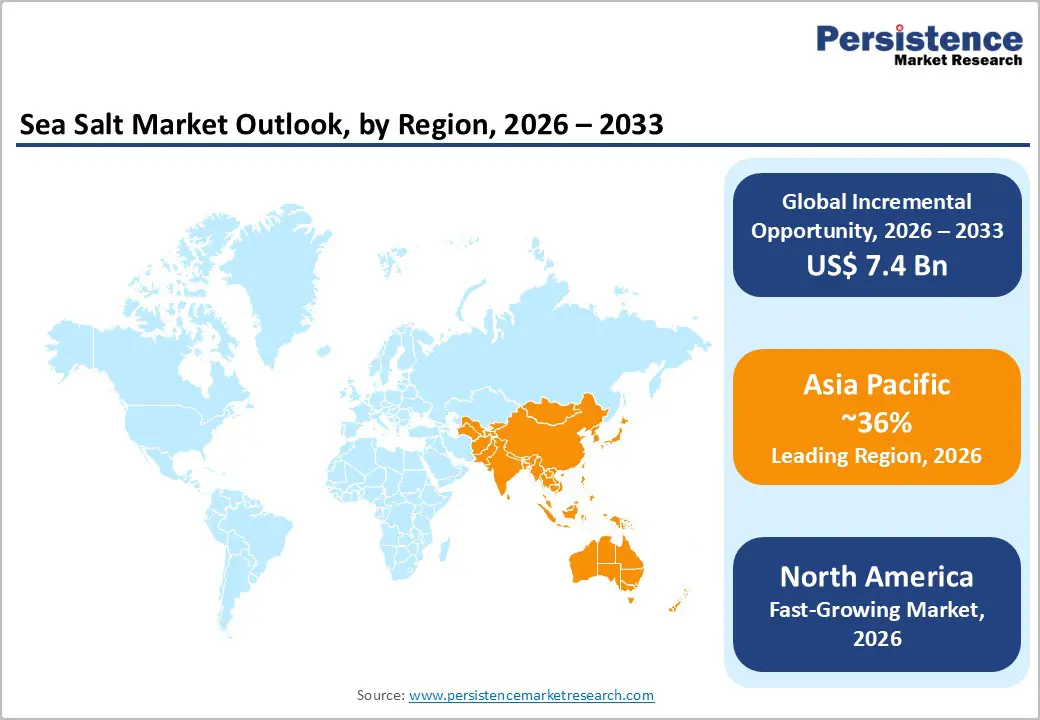

- Regional Performance: Asia Pacific is expected to lead with 36% share in 2026, while North America will grow fastest at 5% CAGR through 2033, driven by premium food, natural personal care, and municipal applications.

- Strategic Direction: Market competition is being increasingly shaped by premiumization, digital distribution, and product innovation, improving margins and brand differentiation.

| Key Insights | Details |

|---|---|

| Sea Salt Market Size (2026E) | US$ 21.0 Bn |

| Market Value Forecast (2033F) | US$ 28.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Natural, Health-Oriented, and Multi-Purpose Sea Salt

The global shift toward natural and minimally processed food ingredients is materially strengthening demand for sea salt. A growing share of consumers now favor sea salt over refined alternatives due to perceived mineral retention and clean-label appeal, prompting food manufacturers to adapt formulations. For example, companies such as SaltWorks have expanded portfolios of gourmet and artisanal sea salts to meet health-oriented consumer demand, while major food brands increasingly highlight sea salt in ingredient lists to appeal to wellness-focused buyers. Sea salt’s functional role in seasoning, preservation, and flavor enhancement across packaged foods and foodservice continues to reinforce its dominant market position.

Beyond food, the multi-purpose utility of sea salt across industrial and wellness applications is broadening its demand base. Municipal authorities increasingly rely on sea salt for water softening regeneration systems, while transportation departments across colder regions continue large-scale procurement for winter road de-icing programs. Salt facilitates water softening by creating a brine solution that regenerates ion-exchange resin beads in softeners. Hard water's calcium and magnesium ions attach to the resin during treatment, while salt displaces them during regeneration, flushing minerals away.This process ensures continuous soft water supply for residential and industrial use. At the same time, cosmetic and personal care brands are incorporating sea salt into detoxifying, exfoliating, and antioxidant formulations, reflecting rising preference for mineral-based ingredients. These non-food applications contribute a growing share of market value and reduce reliance on food sector cycles.

Price Volatility, Supply Constraints, and Competitive Alternatives

Sea salt prices are highly sensitive to raw material volatility and climatic disruptions, as production relies on solar evaporation in coastal areas. Weather events such as droughts, tropical storms, and cyclones can significantly reduce output, creating unpredictable supply and price fluctuations. Smaller producers are disproportionately affected due to limited storage and lack of integrated operations. For example, coastal salt harvesting cooperatives in Gujarat and Tamil Nadu, India, reported lower yields after unseasonal monsoon surges, leading to temporary price spikes. Price volatility directly impacts gross margins across the value chain, especially for industrial buyers such as municipal water treatment plants and large-scale agricultural users, who rely on predictable, high-volume procurement.

The sea salt market growth also faces strong competition from lower-cost alternatives, including refined table salt and rock salt, which are widely available at commodity prices. Large producers and bulk distributors often promote these substitutes through price leadership strategies, making them attractive to cost-conscious consumers and industrial buyers in developing markets. Retail chains frequently market rock salt or low-cost refined blends, constraining the adoption of premium sea salt in volume-driven applications. Combined with supply unpredictability, these alternatives limit market penetration and revenue growth, particularly for industrial and high-volume food processing segments.

Innovation-Driven Growth Opportunities in Developing Economies

Emerging economies across Asia Pacific and Latin America present significant growth opportunities for sea salt market players due to rising disposable incomes, expanding food industries, and developing industrial sectors. China and India are high-growth markets, with strong adoption across food processing, industrial, and consumer seasoning applications. The government in these regions is taking initiatives to enhance coastal salt production infrastructure, increasing efficiency and reducing logistics costs for domestic producers. Strategic investments in local manufacturing and distribution networks can capture unmet demand while minimizing import dependence. Urbanization, expanding retail chains, and growing industrial applications further support broader market penetration and revenue expansion in these emerging economies.

The product innovation and digital commerce are driving premium growth globally. There is a marked shift toward value-added sea salt variants, including low-sodium salts, mineral-fortified blends, and flavored gourmet salts that cater to culinary and health-conscious consumers. For example, Maldon Sea Salt Company introduced flavored products such as Garlic Sea Salt, Smoked Sea Salt, and Pepper Sea Salt in late 2025, targeting gourmet chefs and premium consumers. Online retail channels complement this trend, enabling brands to showcase origin, traceability, and artisanal qualities to global consumers. This combination of emerging market expansion, innovation, and e-commerce reach underpins substantial long-term growth potential for sea salt producers worldwide.

Category-wise Analysis

Salt Type Insights

The unrefined segment is likely to lead, capturing an estimated 63% of the sea salt market revenue share in 2026, supported by a robust consumer demand for natural, non-processed ingredients. Unrefined variants retain trace minerals that appeal to health-focused and culinary users, reinforcing demand in both retail and premium foodservice channels. Cargill Inc. sources unrefined sea salt for its high-end seasoning lines, while Kraft Heinz has reformulated several snack and sauce products to include sea salt labeling to meet clean-label consumer expectations. The Consumer Affairs Agency in Japan and Ministry of Food and Drug Safety of South Korea emphasized ingredient transparency, bolstering confidence in unrefined salt products. These regulatory environments further enhance unrefined sea salt’s market position.

The refined sea salt segment is projected to be the fastest-growing, with an estimated 4.8% CAGR through 2033, driven by broader acceptance across industrial applications and large-scale food processing. The refined sea salt’s uniform granule size and predictable purity make it attractive for consistent integration into mass-market food products and technical applications such as water treatment. Tata Salt uses refined sea salt extensively in processed food categories in India, while Diamond Crystal® Salt is widely used in industrial water softening systems. Ongoing investments in automated milling and quality control technologies are enabling lower production costs, which support wider adoption in high-volume use cases.

Packaging Insights

Bags are expected to hold the largest packaging share, representing 45% of packaging revenue in 2026, due to broad adoption in both retail and bulk channels. This format balances cost efficiency with ease of handling for supermarkets, foodservice distributors, and industrial buyers. Sysco Corporation, a major global foodservice supplier, distributes sea salt primarily in bagged formats to restaurant and institutional clients. Salt Institute of Thailand encouraged the use of standardized bag packaging to ensure quality and reduce contamination risks. Regional producers across Southeast Asia and Latin America leverage bagged packaging to broaden availability and affordability.

Glass jars are poised to be the fastest-growing packaging format, with an estimated 6.1% CAGR through 2033, fueled by demand for premium and specialty sea salts. Glass packaging is favored by specialty retailers and culinary professionals because of its aesthetic appeal and recyclable nature. La Baleine expanded its sea salt offerings in glass jars in late 2025 to appeal to gourmet markets in Europe and North America. Independent retailers and boutique food stores also favor glass jar presentations for artisanal blends, enhancing product visibility and perceived value. This trend supports higher unit prices and elevates the overall market value.

Application Insights

De-icing applications are expected to represent the largest non-food use, holding an estimated 27% of the generated revenue in 2026, driven by recurring municipal demand in colder climates. Government transportation agencies allocate substantial winter maintenance budgets for rock and sea salt procurement. For example, the U.S. Department of Transportation continues to contract large sea salt supplies for state-level highway de-icing programs. Similarly, Canadian provincial transportation ministries secure consistent salt volumes to ensure road safety. These institutional purchasing structures provide predictable annual demand, reinforcing de-icing as a foundational application segment.

The detoxifying application segment is projected to be the fastest-growing with an estimated 5.9% CAGR between 2026 and 2033, as a result of the rising use of sea salt in cosmetics, personal care, and wellness products. The mineral-rich composition and natural exfoliating properties of sea salt have prompted brands such as The Body Shop and Lush to include sea salt across scrub and bath collections. A mid-sized skincare manufacturer, Jurlique, recently expanded its sea salt-based exfoliant range into broader Asia Pacific distribution. These developments reflect strong consumer preference for functional, naturally derived ingredients in beauty and wellness formulations.

End-Use Insights

The food industry is likely to be the largest end-user, accounting for nearly 60% of sea salt market revenue in 2026, due to its extensive use in seasoning, preservation, and taste enhancement. Sea salt is integral to sauces, snacks, packaged meals, and culinary applications spanning global cuisines. Unilever incorporates sea salt into multiple food product lines as part of its flavor strategy, while Nestlé sources it for ready-to-eat meals and seasoning blends. Nutrition and food composition guideline- from the European Food Safety Authority (EFSA) continue to encourage the use of natural mineral salts, supporting sea salt’s strong positioning in food applications.

The cosmetics and personal care sector is forecast to be the fastest-growing end-user, with an estimated 5.6% CAGR during the 2026-2033 forecast period, as brands increasingly use natural exfoliants and mineral-rich formulations. Sea salt’s functional benefits in skincare have led brands such as Neutrogena and Kiehl’s to feature sea salt in exfoliating scrubs, masks, and body treatments. Independent beauty companies in Australia and South Korea are also scaling sea salt-based offerings to meet premium skincare demand. As transparency and ingredient authenticity become priorities for consumers, sea salt’s positioning as a natural, multifunctional ingredient continues to expand in beauty categories.

Regional Insights

North America Sea Salt Market Trends

North America is projected to be the fastest-growing sea salt market, anticipated to register a CAGR of about 5% through 2033, owing to the widespread demand for premium food ingredients, natural personal care products, and expanded municipal use in water treatment and de-icing applications across the region. The United States leads regional adoption due to health-conscious consumers and a mature food processing sector that integrates sea salt into sauces, snacks, and prepared meals. Retailers such as Whole Foods Market and Trader Joe’s continue to expand curated sea salt assortments to meet premium and wellness-oriented demand. Industrial applications, including municipal winter de-icing and water softening, provide stable volume consumption and predictable revenue streams.

Regulatory oversight from the U.S. Food and Drug Administration (FDA) ensures strict food safety, labeling, and quality compliance, which reinforces consumer trust in natural and trace mineral-rich sea salts. Major producers such as Morton Salt, Inc. are investing in automation, traceability, and sustainable production technologies to maintain product consistency and meet consumer expectations. Additionally, artisanal brands such as Celtic Sea Salt / Selina Naturally emphasize regional harvesting practices and sustainable operations to appeal to niche premium markets. These developments collectively support North America’s rapid growth and expanding adoption across food, industrial, and personal care segments.

Europe Sea Salt Market Trends

Europe is slated to maintain a stable share of global sea salt consumption, supported by strong culinary traditions and high interest in artisanal and specialty salts. Germany, the U.K., France, and Spain reflect diversified demand patterns, illustrated through the pairing of gourmet table salts and regional varieties in Western Europe with industrial salt use in utilities and manufacturing. Retailers such as Marks & Spencer and Waitrose have expanded premium sea salt assortments, including regional French fleur de sel and smoked sea salts, catering to food enthusiasts and upscale buyers.

Other key drivers of regional market growth include high consumption of specialty and regional salt varieties, harmonized European Union (EU) food safety regulations emphasizing transparent origin labeling and mineral content standards, and the rising influence of spa, wellness, and therapeutic products incorporating sea salt. The government initiatives such as France’s National Saltwork Centre promote sustainable harvesting and heritage salt production, highlighting artisanal methods that enhance export value. European salt producers are investing in eco-friendly extraction technologies and renewable energy-driven drying systems, enabling cost-efficient and sustainable salt production while reinforcing premium positioning in global markets.

Asia Pacific Sea Salt Market Trends

Asia Pacific is poised to dominate in 2026, accounting for approximately 36% of the sea salt market, fueled by rapid industrialization and expanding food processing sectors in countries such as China and India. Rising disposable incomes have spurred consumer interest in culinary variety and premium salt varieties, while coastal producers continue to scale operations for domestic use and exports. Retailers and foodservice providers have increasingly adopted sea salt in processed foods, seasoning mixes, and gourmet dishes.

Government initiatives have further reinforced this position through targeted investments. For instance, India’s Blue Economy program upgraded coastal salt production sites, and the China National Salt Industry Corporation has introduced mechanized harvesting along with quality assurance systems. Regulatory frameworks, including the China Food Safety Law and India’s Food Safety and Standards Regulations (FSSR), have built trust in local products. Sustainable methods and advanced processing in areas such as Gujarat and Shandong will ensure enduring regional strength.

Competitive Landscape

The global sea salt market exhibits a moderately consolidated structure, with leading players such as Morton Salt, Cargill, Tata Salt, La Baleine, and Unilever collectively accounting for over 50% of total market revenue. These companies benefit from vertically integrated supply chains, extensive retail and foodservice distribution networks, and strong brand equity across both food-grade and industrial sea salt segments. Continuous investments in automation, quality traceability, sustainable harvesting, and regulatory compliance strengthen their competitive positioning, particularly in premium and value-added salt categories.

Niche and regional players, including Selina Naturally, Celtic Sea Salt, and China National Salt Industry Corporation focus on artisanal, mineral-rich, and wellness-oriented sea salt offerings. While entry barriers remain high due to environmental regulations, quality standards, and scale requirements, the growth of digital and e-commerce channels enables smaller brands to access global consumers. The market is expected to witness gradual consolidation, supported by acquisitions, strategic partnerships, and innovation-led expansion in specialty and premium sea salt products.

Key Industry Developments

- In June 2025, Indonesia initiated the development of a 10,000+ hectare salt project in East Nusa Tenggara to modernize production, achieve national salt self-sufficiency by 2027, and reduce import dependence. Phase 1 began mid-2025 with solar evaporation and processing facilities, managed by PT Garam, attracting both domestic and foreign investment. The project is expected to produce up to 5 million tons annually and create thousands of jobs, enhancing food security.

- In June 2025, Arizona State University (ASU) researchers partnered with Nestlé to transform industrial brine from reverse osmosis processes into reusable freshwater and solid salt. This mobile, closed-loop facility recovers additional water from salty byproducts, easing disposal challenges for sectors such as semiconductors, batteries, and food production in Arizona's arid environment.

- In May 2025, Slick Gorilla introduced a Sea Salt Scalp Scrub, formulated with natural sea salt that deeply cleanses and exfoliates using natural sea salt to remove buildup, excess oil, and impurities.

The vegan formula includes sweet almond oil for softness and hydrated silica for oil absorption, suiting all hair types with weekly use followed by shampoo. It rebalances the scalp, soothes irritation, and prepares hair for styling.

Companies Covered in Sea Salt Market

- Cargill, Inc.

- Morton Salt, Inc.

- Tata Salt

- China National Salt Industry Corporation

- K+S Aktiengesellschaft

- Salins Group

- Maldon Crystal Salt Company Ltd.

- Cheetham Salt Limited

- Murray River Salt

- Dominion Salt Limited

- SaltWorks, Inc.

- Compass Minerals International, Inc.

Frequently Asked Questions

The global sea salt market is projected to reach US$ 21.0 billion in 2026.

The enormous demand for natural, health-oriented, and multi-purpose sea salts across food, personal care, and industrial applications is driving market growth.

The market is poised to witness a CAGR of 4.4% from 2026 to 2033.

Product innovation with flavored and low-sodium salts and the proliferation of e-commerce and digital distribution channels, especially in developing economies, are opening new and highly lucrative opportunities.

Morton Salt, Inc., Cargill, Tata Salt, China National Salt Industry Corporation, and SaltWorks, Inc. are some of the key players in the market.