- Food Ingredients & Additives

- Commercial Seaweed Market

Commercial Seaweed Market Size, Share, and Growth Forecast 2026 - 2033

Commercial Seaweed Market by Seaweed Type (Red Seaweed, Brown Seaweed, Green Seaweed), Form (Powder, Flake, Liquid), Application (Food & Beverage, Animal Feed & Aquaculture, Agriculture, Pharmaceuticals, Cosmetics & Personal Care, Biofuels & Biomass, Others), and Regional Analysis, 2026 - 2033

Commercial Seaweed Market Share and Trends Analysis

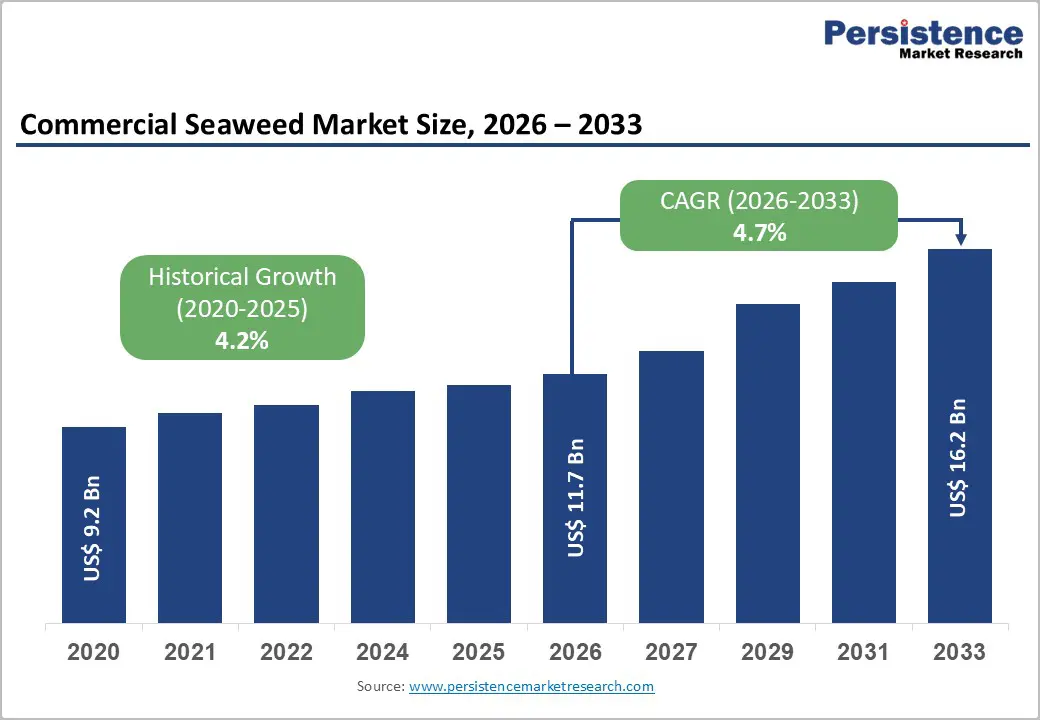

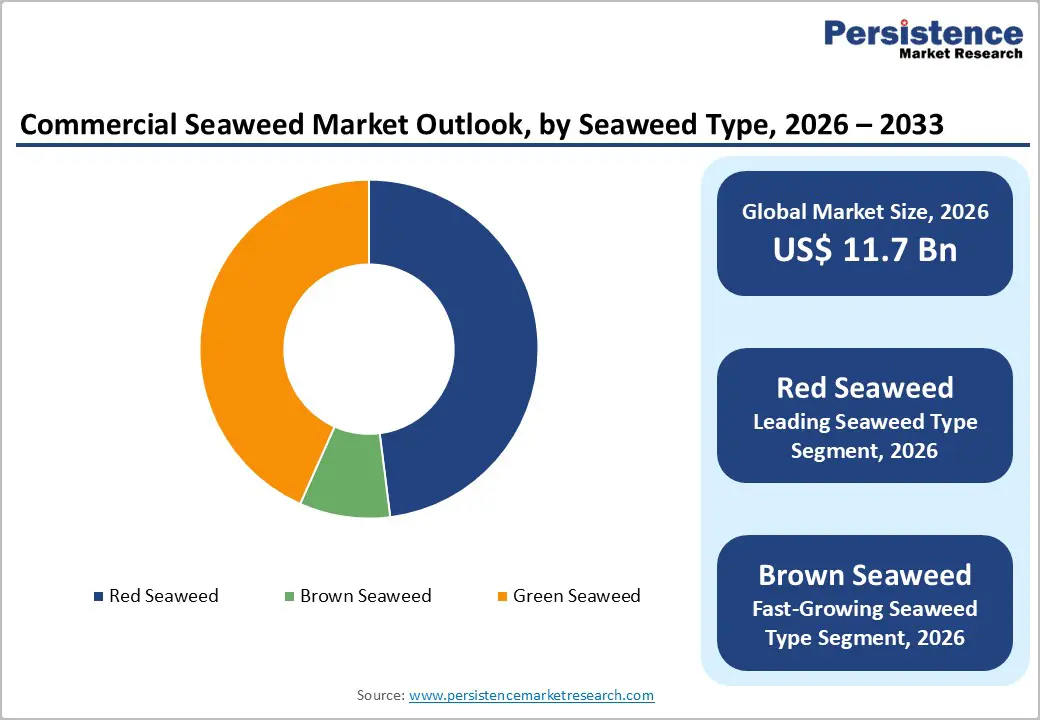

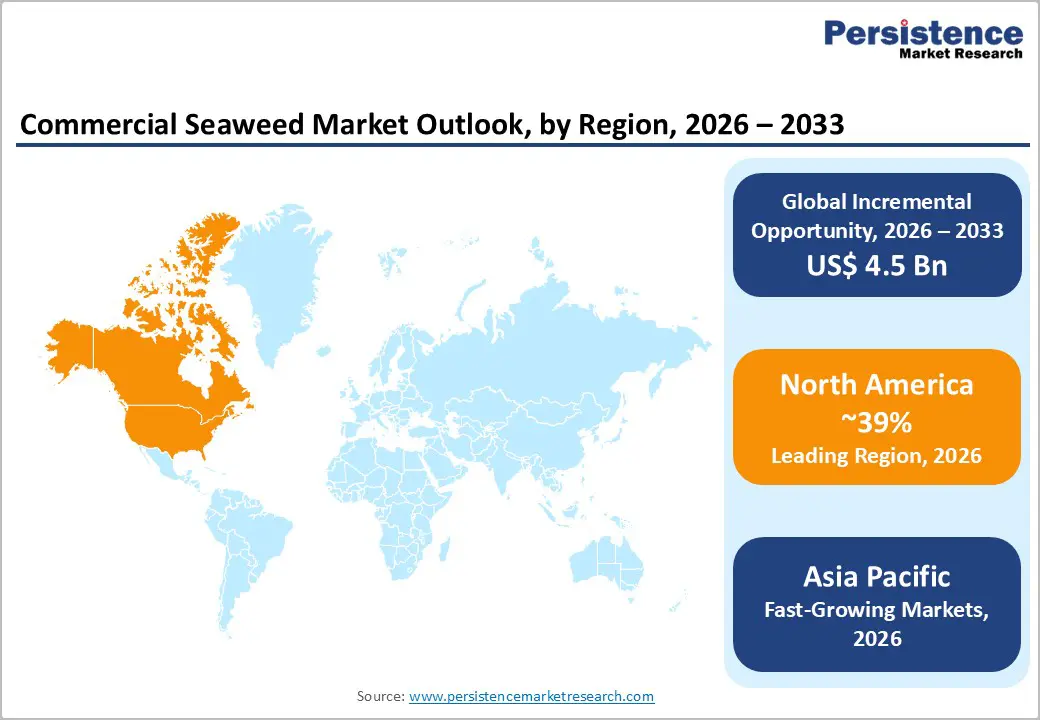

The global commercial seaweed market size is expected to be valued at US$ 11.7 billion in 2026 and projected to reach US$ 16.2 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

This growth is primarily driven by rising demand for sustainable and high-value marine ingredients across food, feed, agriculture, and cosmetics, against the backdrop of global climate-action mandates and protein diversification initiatives. Advances in marine farming technology, supportive government policies in coastal nations, and increasing consumer interest in plant-based functional foods are aligning to create a robust demand environment for cultivated seaweeds rather than relying solely on wild harvest.

Key Industry Highlights:

- North America leads with a 39% share, supported by a mature food and nutraceutical industry and established supply chains.

- Asia Pacific grows fastest, driven by abundant coastal resources, government aquaculture support, and rising demand in functional foods, cosmetics, and pharmaceuticals.

- Red Seaweed leads with 48% share, largely due to high carrageenan and agar production for food stabilization, cosmetics, and pharmaceutical applications.

- Brown Seaweed is the fastest-growing segment, fueled by alginate demand, bioactive compounds, and use in nutraceuticals and animal feed.

- Animal feed expansion offers a key opportunity, as seaweed improves livestock health, supports sustainable agriculture, and meets demand for natural feed additives.

| Key Insights | Details |

|---|---|

| Commercial Seaweed Market Size (2026E) | US$ 11.7 billion |

| Market Value Forecast (2033F) | US$ 16.2 billion |

| Projected Growth CAGR (2026 - 2033) | 4.7% |

| Historical Market Growth (2020 - 2025) | 4.2% |

Market Dynamics

Drivers - Increasing Demand from Food & Beverage Applications

Food and beverage applications remain the largest pull for commercial seaweed, with seaweed-based gelling, thickening, and texturizing agents now routinely used in plant-based dairy, meat analogues, sauces, baked goods, and functional beverages. The utilization of carrageenan, alginate, and agar extracted mainly from Red and Brown seaweeds is well established in Codex Alimentarius-aligned food standards, enabling broad regulatory acceptance in both the United States and the European Union jurisdictions. According to industry-aligned production data, global seaweed biomass for food-grade hydrocolloids has grown at roughly 8-10% per year over the past five years, reflecting both population growth and a shift toward minimally processed “natural” ingredients. In regions such as Asia Pacific, where traditional seaweed cuisine is widespread, restaurants and packaged-food manufacturers are increasingly marketing seaweed as a premium, nutrient-dense ingredient, further reinforcing demand for consistent, traceable commercial supplies rather than artisanal harvests alone.

Sustainability and Climate-Action Policies Supporting Seaweed Farming

Global climate- action and blue economy strategies are increasingly positioning seaweed cultivation as a carbon-sequestering, low-impact marine activity that supports coastal livelihoods without degrading land-based agriculture. Food and Agriculture Organization of the United Nations (FAO) data indicate that seaweed aquaculture now accounts for over 50% of all marine algae produced worldwide, with China, Indonesia, and the Philippines leading farmed biomass output. Against this backdrop, national blue-economy frameworks in the European Union, United States, Canada, and Japan explicitly promote seaweed farming for carbon capture, nutrient capture from coastal eutrophication, and alternative protein feedstocks. These policy signals reduce investment risk for commercial operators, stimulate R&D in offshore farming systems, and encourage private sector partnerships that, in turn, expand the scale and reliability of commercial seaweed supply chains.

Restraints - Limited Scalability and Fragmented Farming Infrastructure

Despite the strong policy push, many coastal regions still lack the standardized infrastructure and technical know-how to scale seaweed aquaculture beyond small-holder operations. In parts of Latin America, Africa, and even some ASEAN countries, farming practices remain largely manual, with low mechanization and inconsistent grading, which complicate the supply of high-quality, uniform feedstock required by global food and pharmaceutical companies. Furthermore, permitting processes in certain jurisdictions are slow or unclear, discouraging long-term investment in large-scale marine farms. This fragmentation leads to volatile supply, price fluctuations, and quality control challenges that can deter brand-sensitive manufacturers from committing to high-volume seaweed-based formulations.

Stringent and Evolving Regulatory Scrutiny

As seaweed moves into higher-value applications such as pharmaceutical excipients and food-contact additives, regulatory scrutiny is intensifying. The European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) have periodically reviewed carrageenan and other seaweed-derived substances, raising questions about acceptable daily intake levels and purity thresholds, leading some manufacturers to temporarily de-risk formulations. In parallel, Codex Alimentarius and regional bodies are updating maximum residue limits and monitoring guidance for heavy metals and iodine, which can be elevated in wild-harvested seaweeds. These evolving standards force processors to invest heavily in cleaning, blending, and traceability systems, raising the cost of compliant seaweed products and creating a barrier to entry for smaller producers seeking to enter export markets.

Opportunities - Expansion into Animal Feed and Aquaculture Nutrition

One of the most compelling growth vectors for commercial seaweed lies in ruminant and aquaculture feed, where seaweed-based additives can reduce methane emissions, improve feed efficiency, and enhance disease resistance. Research linked to Food and Agriculture Organization (FAO)-supported projects and national agricultural programs has shown that adding small percentages of certain Red and Brown seaweeds to ruminant diets can lower enteric methane by up to 30%, aligning with Paris Agreement-linked climate targets. In aquaculture, seaweed-derived beta-glucans and other immunostimulants are being incorporated into shrimp and finfish feeds to reduce reliance on antibiotics, particularly in high-value export-oriented sectors such as Norwegian and Chilean salmon farming. These applications are driving investment in dedicated seaweed feed-grade production lines and long-term supply contracts between large agrifood companies and offshore farming operators.

Biorefinery and Bio-Material Applications

Beyond traditional food and feed, seaweed is emerging as a feedstock for bio-based materials, including bioplastics, packaging films, and bio-coatings that replace petroleum-derived polymers. European Commission-backed biorefinery pilots and national innovation funds in Germany, France, and Japan are supporting the extraction of polysaccharides and polyphenols for these applications, positioning seaweed as a circular-economy raw material. Simultaneously, academic and industrial initiatives are exploring seaweed-based biofuels and anaerobic digestion feedstocks, leveraging the high carbohydrate content of certain seaweeds to generate renewable energy while minimizing competition with food crops. These opportunities favor vertically integrated players that can control the entire chain from farm to formulated bioproduct, creating a clear differentiation pathway for market leaders in the Commercial Seaweed space.

Category-wise Analysis

Product Insights

Red seaweed is the leading segment in the Commercial Seaweed market, capturing approximately 48% of global market share in 2025. This dominance is driven by the high commercial value of carrageenan and agar, which are extracted from species such as Kappaphycus, Eucheuma, and Gracilaria and form the backbone of the global hydrocolloid industry. These ingredients are indispensable in dairy alternatives, ready-meal sauces, processed meats, and desserts, where they provide gel strength, texture control, and shelf-life extension.

FAO statistics indicate that more than half of the world’s seaweed biomass for hydrocolloid extraction is derived from Red seaweeds, underscoring their entrenched role in high-value food systems. In addition, the relative maturity of Red-seaweed farming in Indonesia, the Philippines, and China supports consistent supply volumes, enabling large food-grade processors and multinational ingredient companies to rely on long-term procurement contracts with few short-term supply disruptions.

Form Insights

Among the different forms, powder holds the largest share of the Commercial Seaweed market, driven by its versatility and ease of integration into dry-mix formulations. Powdered seaweed is widely used in food-grade blends, instant soups, seasonings, and dietary supplements, where uniform dispersion and long-term stability are critical. The rise of ready-to-eat plant-based products and functional beverages has further amplified demand for fine, standardized seaweed powders that can be metered precisely in industrial mixing lines.

Codex Alimentarius and ISO-style quality specifications now cover particle size distribution and microbial limits for powdered seaweed ingredients, encouraging manufacturers to invest in advanced drying and milling infrastructure. This has led to regional consolidation of processing around key ports and industrial hubs in Asia Pacific and Europe, where large ingredient suppliers such as Cargill, Incorporated and DuPont source bulk seaweed powders for global distribution.

Regional Insights

North America Commercial Seaweed Market Trends and Insights

North America is the leading regional segment in the Commercial Seaweed market, estimated to account for about 39% of global market share in 2025. The United States and Canada dominate this leadership, driven by strong innovation ecosystems in functional foods, nutraceuticals, and animal-feed additives. U.S. food-safety frameworks administered by the FDA and USDA enable clear pathways for the use of seaweed-derived hydrocolloids and extracts, permitting manufacturers to formulate plant-based and reduced-fat products without compromising texture or shelf life.

In parallel, NOAA-supported aquaculture programs and state-level initiatives in Maine, California, and the Pacific Northwest are expanding offshore seaweed farms that supply high-quality biomass to domestic processors and global exporters. The presence of major ingredient giants such as Cargill, Incorporated and DuPont in the region further strengthens formulation and distribution capabilities, positioning North America as a hub for commercial-scale, value-added seaweed applications rather than raw biomass trade alone.

Another key feature of the North American market is the convergence of climate-action policy and corporate sustainability goals. The U.S. Department of Agriculture and various state environmental agencies increasingly promote seaweed aquaculture as a low-impact method to sequester carbon and reduce coastal nutrient loading. Large food and beverage multinationals headquartered in United States are also adopting seaweed-based ingredients as part of their “clean-label” and carbon-footprint-reduction strategies, driving demand for certified, traceable seaweed supplies.

At the same time, venture-capital-backed startups in the plant-based and alternative-protein space are integrating seaweed into meat and dairy analogues, leveraging its umami richness and functional binding properties. These interlinked trends support a robust innovation pipeline, ensuring that North America remains the most mature and commercially advanced regional segment in the Commercial Seaweed market.

Asia Pacific Commercial Seaweed Market Trends and Insights

Asia Pacific is emerging as the fastest-growing region in the commercial seaweed market, driven by abundant coastal resources, supportive aquaculture policies, and increasing demand across food, pharmaceutical, and cosmetic industries. Countries such as China, Indonesia, South Korea, and Japan dominate production, particularly of red and brown seaweed, supplying global carrageenan, agar, and alginate markets. Rising health consciousness and the growing popularity of functional foods, plant-based products, and nutraceuticals are fueling demand for seaweed-derived ingredients.

Urbanization, expanding e-commerce channels, and modern retail networks are enhancing market access, especially for processed and value-added seaweed products. Government initiatives promoting sustainable aquaculture, environmental protection, and organic certification further support market expansion. Additionally, innovations in bioactive compounds, food additives, and natural preservatives are attracting investment and driving adoption.

Competitive Landscape

The commercial seaweed market is moderately consolidated, with competition driven by product innovation, sustainability, and value-added derivatives. Key players focus on expanding cultivation of red, brown, and green seaweed to meet rising global demand for carrageenan, agar, alginate, and bioactive compounds. Companies invest in advanced aquaculture technologies, sustainable harvesting practices, and certified organic production to differentiate offerings in food, pharmaceuticals, cosmetics, and nutraceuticals. E-commerce, modern retail, and industrial partnerships strengthen market reach, while regulatory compliance and traceability are critical for international trade.

Key Market Developments

- In February 2025, Ocean Rainforest acquired a 60% stake in Alamarsa, a Mexico-based company known for its Algamar brand, which specializes in biostimulants and food products made from giant kelp and other seaweed species, strengthening its presence in the North American seaweed market.

- In January 2025, The U.S. Department of Energy's ARPA-E announced a $25 million investment to develop large-scale deep-water cultivation of seaweed biomass for energy and industrial applications, positioning the U.S. as a leader in marine hydrocarbon supply chains.

- In September 2024, The Seaweed Company, with support from EU funding, has launched Ireland’s first commercial seaweed farm and processing facility in Donegal. This full-scale operation represents a significant advancement in the country’s marine biotechnology landscape and highlights a growing commitment to sustainable seaweed cultivation and processing.

Companies Covered in Commercial Seaweed Market

- Cargill, Incorporated

- DuPont

- Arctic Seaweed AS

- ASL (Acadian Seaplants)

- Tate & Lyle

- Irish Seaweeds

- W Hydrocolloids, Inc

- Ocean Rainforest

- The Seaweed Company

- Gelymar S.A

- Thorverk hf.

- Ocean's Balance

- Seakura

- Seaweed & Co.

Frequently Asked Questions

The global commercial seaweed market is projected to reach US$ 11.7 billion in 2026, reflecting growing adoption across food, nutraceutical, cosmetic, and pharmaceutical industries.

The primary growth driver is the food and beverage sector, which is expanding at a 12% CAGR, fueled by functional foods, plant-based ingredients, and natural additives derived from seaweed.

North America leads with a 39% market share, supported by advanced processing infrastructure, strong consumer demand for healthy foods, and well-established supply chains.

Animal feed applications offer a major opportunity, particularly seaweed’s role in reducing livestock methane emissions, supporting sustainability, and meeting regulatory and environmental goals.

Leading companies include Cargill, DuPont, and Gelymar S.A., focusing on innovative seaweed derivatives, sustainable sourcing, and value-added products for multiple end-use industries.