- Beverages

- Protein Water Market

Protein Water Market Size, Share, and Growth Forecast 2026 - 2033

Protein Water Market by Packaging Type (Bottles, Cans, Pouches, Others), by Source (Whey Protein, Pea Protein, Soy Protein, Egg Protein, Brown Rice Protein, Others), by Distribution Channel, by End User, by Regional Analysis, 2026 - 2033

Protein Water Market Share and Trends Analysis

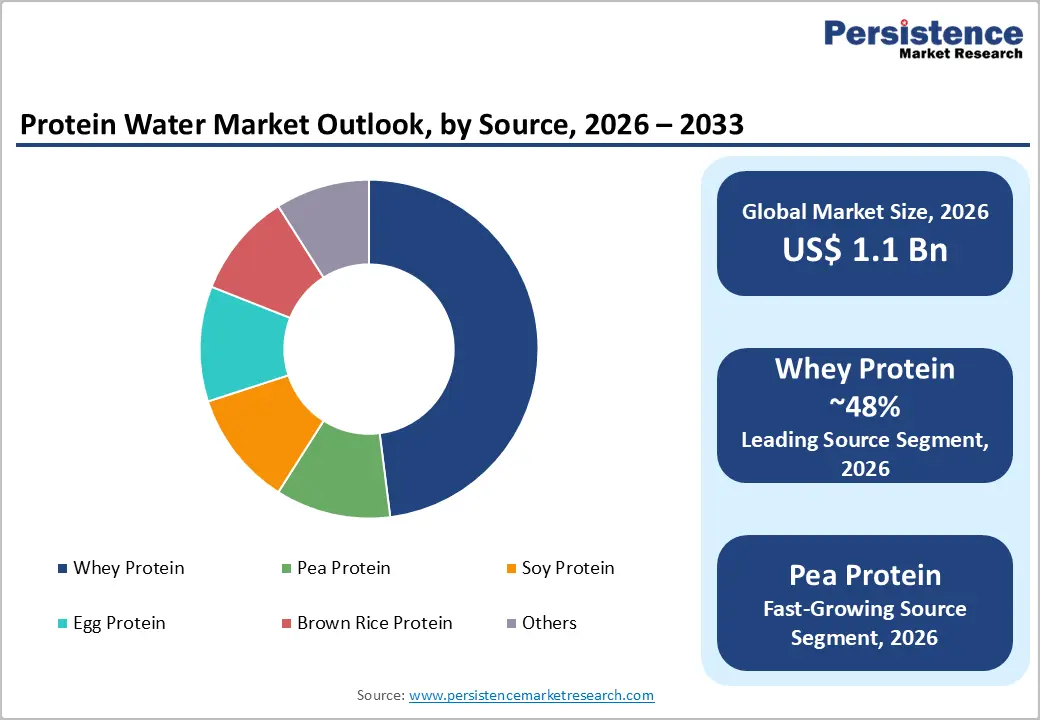

The global protein water market size is expected to be valued at US$ 1.1 billion in 2026 and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033. Protein water is a functional beverage combining purified water with proteins such as whey, collagen, or plant-based isolates, offering hydration and nutritional support.

It caters to athletes, fitness enthusiasts, and health-conscious consumers seeking convenient, low-calorie alternatives to traditional protein shakes. Popular for post-workout recovery, muscle maintenance, weight management, and overall wellness, protein water often includes added electrolytes, vitamins, or natural flavors.

Key Industry Highlights

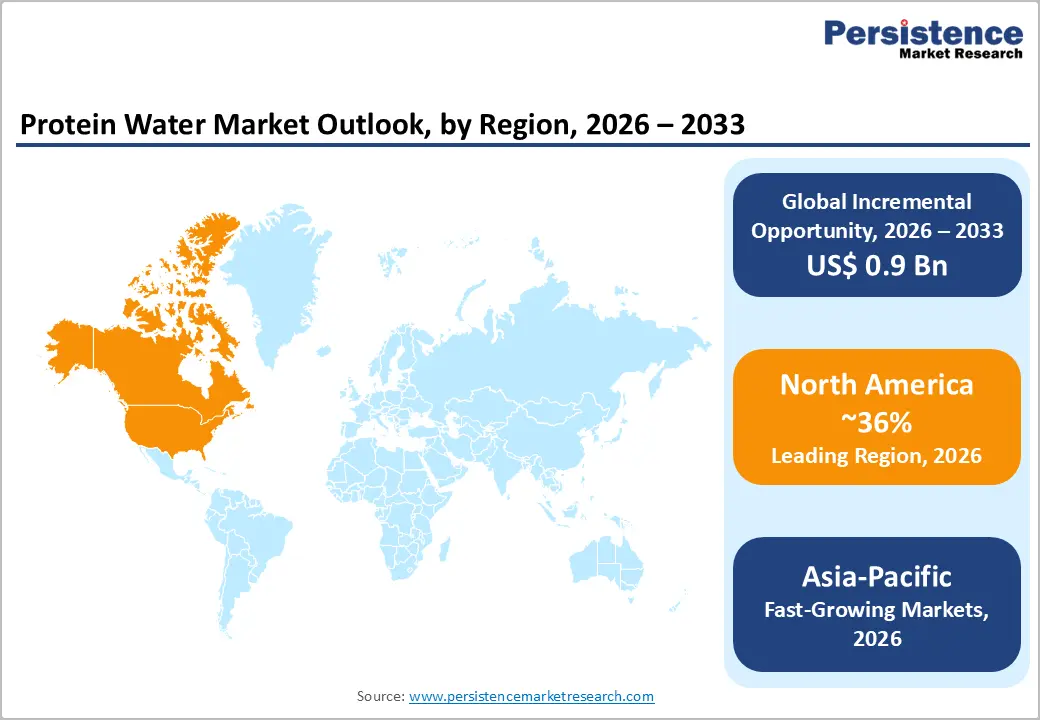

- Leading Region: North America leads the global protein water market, supported by strong fitness culture, high functional beverage consumption, advanced retail infrastructure, and continuous product innovation in sports nutrition.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising health awareness, expanding middle-class population, increasing gym participation, and growing demand for convenient ready-to-drink functional beverages.

- Dominant Segment: Bottled packaging dominates the market, accounting for the largest revenue share due to portability, resealability, shelf stability, and widespread availability across supermarkets and convenience stores.

- Fastest Growing Segment: Plant-based protein water is the fastest-growing segment, fueled by increasing vegan preferences, clean-label demand, lactose intolerance concerns, and rising interest in sustainable, non-dairy nutrition options.

| Key Insights | Details |

|---|---|

| Protein Water Market Size (2026E) | US$ 1.1 billion |

| Market Value Forecast (2033F) | US$ 2.0 billion |

| Projected Growth CAGR (2026 - 2033) | 9.3% |

| Historical Market Growth (2020 - 2025) | 7.9% |

Market Dynamics

Driver - Rising Health and Wellness Trends & Expansion of Fitness and Sports Nutrition

Rising health and wellness trends are a primary driver for the protein water market. Consumers increasingly prioritize clean-label, functional beverages that combine hydration with nutritional benefits. The FDA’s updated “healthy” labeling framework in February 2025 allows low-calorie, water-based drinks to carry health claims, increasing the appeal of protein-infused waters. This aligns with global fitness participation growth; data from the International Health, Racquet & Sportsclub Association shows a 40% rise in gym memberships, highlighting a growing population focused on active lifestyles. Protein water addresses needs for satiety, muscle recovery, and daily nutrition, positioning itself as a convenient, low-calorie alternative to traditional protein shakes. Its multifunctional benefits make it an essential component in the routines of health-conscious consumers, supporting category growth through 2033.

The expansion of fitness and sports nutrition also fuels adoption. With over 1.9 billion adults classified as overweight globally (WHO), there is increasing demand for low-calorie, high-protein alternatives to sugary beverages. Ready-to-drink protein waters eliminate preparation challenges associated with powders, making them convenient for post-workout recovery. Additionally, e-commerce growth, with e-grocery sales rising 25% annually, enhances accessibility and convenience, allowing brands to reach digital-first consumers. This combination of lifestyle awareness, functional benefits, and distribution innovation strengthens sustained market demand worldwide.

Restraint - High Production Costs & Taste and Texture Challenges

High production costs present a significant restraint to protein water market growth. Premium protein sources, such as whey and pea protein isolates, require complex extraction and purification processes, which elevate production expenses. In 2025, USDA data reported a 15% increase in dairy prices, contributing to cost volatility in whey-based products. These high input costs are often passed to consumers, raising retail prices and limiting adoption in price-sensitive emerging markets. Despite growing awareness of protein benefits, manufacturers face challenges in maintaining competitive pricing, which constrains volume growth even as overall demand remains strong.

Taste and texture challenges further hinder market penetration. Protein fortification can result in chalky mouthfeel or off-flavors, discouraging repeat purchases. Surveys from Nutraceuticals World show that 30% of consumers reject fortified waters due to sensory concerns. While reformulation efforts are underway, solutions lag behind consumer expectations, slowing mainstream acceptance. This sensory barrier limits the beverage’s appeal beyond niche fitness and health segments, reducing overall velocity in global markets and creating an ongoing challenge for producers to balance functionality with taste.

Opportunity - Innovation in Plant-Based Formulations & E-Commerce and Subscription Models

Innovation in plant-based protein formulations represents a significant growth opportunity. Pea protein is gaining traction due to its clean taste, sustainability, and alignment with vegan and environmentally conscious consumer preferences. Pew Research indicates that 6% of U.S. adults identify as vegan, reflecting rising demand for plant-based alternatives. EU clean-label policies promoting non-GMO ingredients further encourage manufacturers to invest in R&D for plant-based protein waters. Recent product launches incorporating pea protein have reported up to 20% sales growth, demonstrating strong revenue potential for companies that adapt formulations to clean-label and sustainable standards. This trend allows brands to differentiate products while appealing to health-conscious, environmentally aware consumers globally.

E-commerce and subscription-based models offer another avenue for growth, particularly in high-growth regions like Asia-Pacific. Online food and beverage sales are projected to reach $1 trillion by 2030, and protein water can leverage auto-replenishment and fitness app integrations to build loyal consumer bases. Digital platforms allow brands to directly target active consumers with personalized recommendations. Partnerships with major e-commerce players such as Amazon enable scalable distribution and recurring revenue streams, enhancing accessibility while building engagement with tech-savvy fitness enthusiasts. This combination of digital reach and convenience positions protein water for sustained market expansion.

Category-wise Analysis

By Packaging Insights

Bottles are projected to lead the protein water market with approximately 45% share in 2026, primarily due to their portability and resealability. Consumers prefer bottled formats for on-the-go consumption, especially in gym settings, workplaces, and outdoor activities. Their lightweight structure, durability, and compatibility with single-serve and multi-serve options make them highly practical. According to Nielsen data, bottled beverages account for nearly 60% of total hydration sales, reflecting strong consumer familiarity and established purchasing behavior. The convenience factor continues to strengthen bottle dominance across both developed and emerging markets.

Additionally, established manufacturing and distribution supply chains support cost efficiency and wide retail availability. Sustainability initiatives, including recycling programs promoted by FEMA and industry bodies, are improving consumer perception of plastic packaging. Companies are increasingly introducing recyclable PET bottles and lightweight materials to align with environmental goals. These innovations help maintain bottle leadership while addressing sustainability concerns, ensuring continued segment dominance amid evolving regulatory and consumer expectations.

By Distribution Channel Insights

Supermarkets and hypermarkets are expected to hold highest market share in 2026, driven by strong product visibility and impulse purchasing behavior. Large retail chains provide dedicated shelf space, in-store promotions, and end-cap displays that significantly influence beverage buying decisions. Consumers often prefer physical stores for first-time trials, as they can compare brands, flavors, and nutritional claims directly.

Trust in brick-and-mortar retail further strengthens this channel’s position. Promotional pricing strategies, bundled offers, and sampling campaigns enhance consumer engagement and repeat purchases. Additionally, supermarkets maintain strong relationships with beverage distributors, ensuring consistent stock availability. While e-commerce continues to grow, supermarkets and hypermarkets remain the primary revenue generators due to high footfall, immediate product access, and established consumer shopping habits, securing their leadership in protein water distribution.

Regional Insights

North America Protein Water Market Trends

North America remains a mature yet innovation-driven protein water market, supported by strong fitness culture and high functional beverage penetration. The U.S. leads regional demand due to widespread gym participation, sports nutrition awareness, and increasing preference for low-calorie, high-protein hydration. Consumers actively seek clean-label, sugar-free, and keto-friendly beverages, encouraging brands to introduce collagen-infused and whey-isolate formulations. Regulatory clarity from agencies such as the U.S. Food and Drug Administration regarding protein claims further strengthens product positioning and consumer trust.

Convenience retail and club stores play a major role in bulk purchasing, while private-label expansion by major retailers intensifies competition. Sustainability is another defining trend, with companies adopting recyclable PET packaging and transparent sourcing disclosures. Influencer marketing and athlete endorsements significantly shape purchasing behavior, especially among millennials and Gen Z. Additionally, functional crossover products combining hydration, electrolytes, and immunity support are gaining traction, reflecting consumer preference for multifunctional beverages. Continuous product innovation and premiumization strategies are expected to sustain steady regional growth.

Europe Protein Water Market Trends

Europe’s protein water market is characterized by strong regulatory standards, clean-label demand, and sustainability-focused innovation. Consumers prioritize natural ingredients, non-GMO proteins, and transparent nutritional labeling, aligning with guidelines from the European Food Safety Authority. Western European countries, including Germany, the UK, and the Nordics, are early adopters of plant-based protein water, reflecting high vegan and flexitarian populations.

Environmental consciousness significantly shapes product development, with brands emphasizing recyclable packaging, reduced carbon footprints, and ethically sourced proteins. Functional hydration targeting aging populations is also emerging, with collagen-based formulations positioned for joint and skin health. Specialty health stores and pharmacy chains contribute notably to premium product sales. Additionally, cross-border trade within the European Union enhances distribution efficiency, allowing multinational beverage brands to scale rapidly. As consumers increasingly replace sugary soft drinks with functional alternatives, protein water continues to gain traction as a healthier hydration choice across the region.

Asia Pacific Protein Water Market Trends

Asia Pacific represents a high-growth market fueled by rising urbanization, expanding middle-class populations, and increasing health awareness. Countries such as China, Japan, South Korea, and Australia are witnessing rapid adoption of ready-to-drink functional beverages. Growing gym memberships, marathon participation, and interest in weight management programs are accelerating demand for convenient protein hydration solutions. Government-led health initiatives promoting active lifestyles across markets like India and Singapore further support product uptake.

Flavor localization is a key regional strategy, with brands introducing tropical fruit, matcha, and lychee variants to match regional taste preferences. E-commerce and mobile-first purchasing behavior significantly influence sales, as consumers increasingly order beverages through digital marketplaces and quick-commerce platforms. Additionally, plant-based protein water is gaining popularity due to lactose intolerance prevalence in several Asian populations. Regional manufacturers are focusing on affordable pack sizes to enhance accessibility, while partnerships with fitness chains and wellness influencers are strengthening brand visibility across metropolitan cities.

Competitive Landscape

The protein water market is moderately fragmented, with global beverage companies and emerging functional drink brands competing on innovation, formulation, and branding. Players differentiate through plant-based proteins, collagen infusions, sugar-free claims, and clean-label positioning. Continuous flavor innovation and improved texture technologies are central to gaining repeat purchases. Strategic partnerships with fitness centers, sports influencers, and e-commerce platforms strengthen brand visibility. Companies also focus on sustainable packaging and recyclable materials to align with environmental expectations. Expansion through online subscription models and international distribution agreements further intensifies competition, driving product diversification and premiumization across regional markets.

Key Industry Developments:

- In November 2025, Aquatein introduced India’s first vegan protein water on World Vegan Day, blending nutrition, sustainability, and refreshing taste in a single beverage. Each 500 mL bottle delivers 15 grams of plant-based protein along with natural electrolytes.

- In October 2025, beverage manufacturer iPRO announced the upcoming launch of its protein water product.

- In October 2025, FORALL® Nutrition announced the launch of WATER+PROTEIN, the first clear, flavorless, ready-to-drink protein water, a breakthrough innovation combining hydration and nutrition in their simplest, purest form.

Companies Covered in Protein Water Market

- Soulfuel India LLP

- Aquatein

- Applied Nutrition Ltd

- VPA Australia

- The Vita Coco Company

- Drink Tatu

- Protein Water Co

- NZ Muscle

- Nexus Sports Nutrition

- Muscle Nation

- Musashi Nutrition

- Protein2o

- Others

Frequently Asked Questions

The protein water market is estimated to be valued at US$ 1.1 Bn in 2026.

Rising fitness trends, health-conscious consumers, demand for low-calorie protein drinks, and sports nutrition awareness drive growth.

The global protein water market is expected to witness a CAGR of 9.3% between 2026 and 2033.

A few of the prominent players operating in the market are Soulfuel India LLP, Aquatein, Applied Nutrition Ltd, VPA Australia, and The Vita Coco Company.

North America is the leading region in the global protein water market.