- Food Ingredients & Additives

- Fungal Protein Market

Fungal Protein Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Fungal Protein Market by Product Type (Mycoprotein, Yeast Protein, Others), End-user (Meat Alternatives, Dairy Alternatives, Nutritional Supplements, Household/Retail), Sales Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Fungal Protein Market Share and Trends Analysis

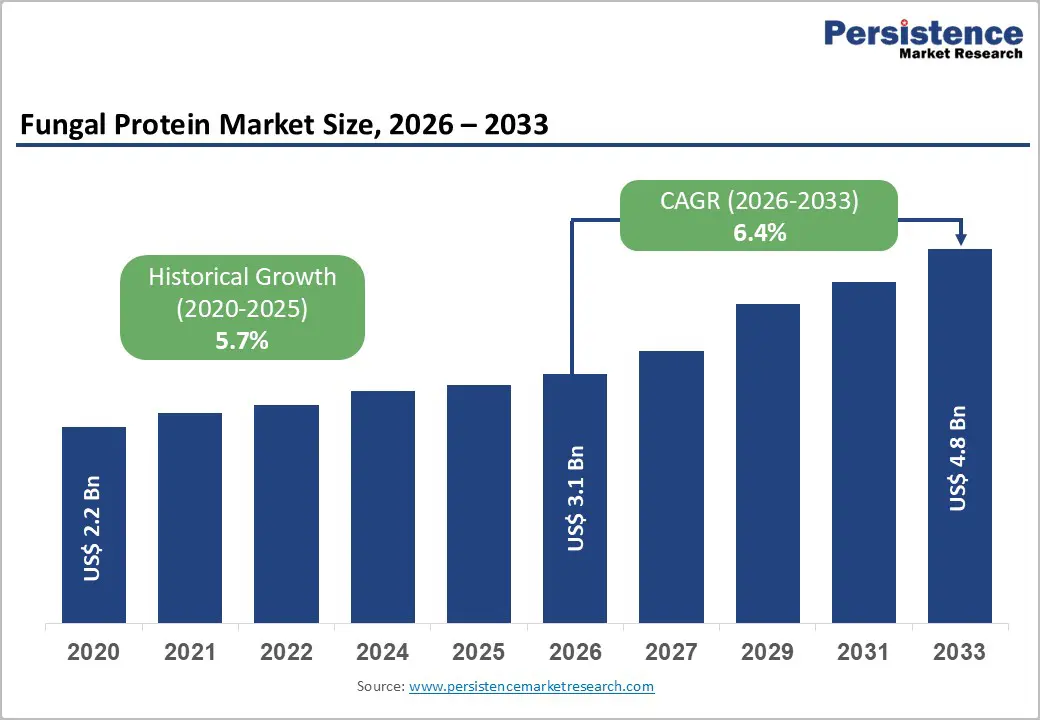

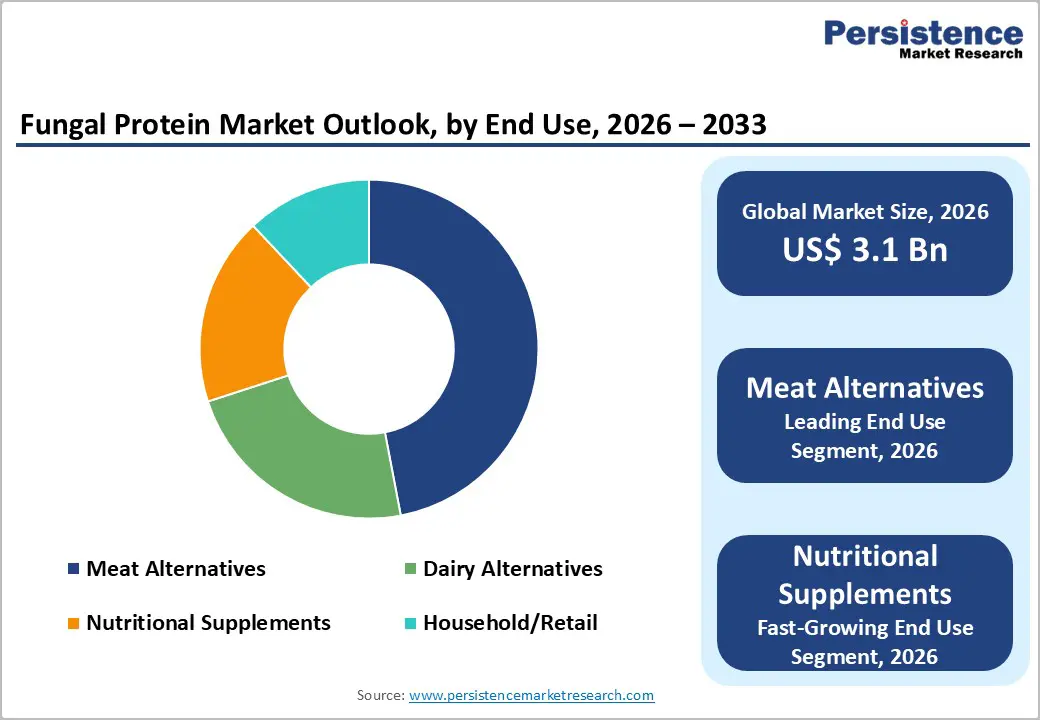

The global fungal protein market size is expected to be valued at US$ 3.1 billion in 2026 and projected to reach US$ 4.8 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

The market trajectory is primarily driven by the rise in global shift toward sustainable, resource-efficient food production systems and a surging consumer appetite for high-quality, meat-free nutritional profiles. This growth is reinforced by the superior metabolic benefits of fungal-derived ingredients, such as their high fiber content and complete amino acid profiles, which resonate with the health-conscious demographic. Furthermore, the industrial scalability of fermentation technologies enables a lower environmental footprint than traditional livestock farming, thereby attracting significant institutional investment.

Key Industry Highlights:

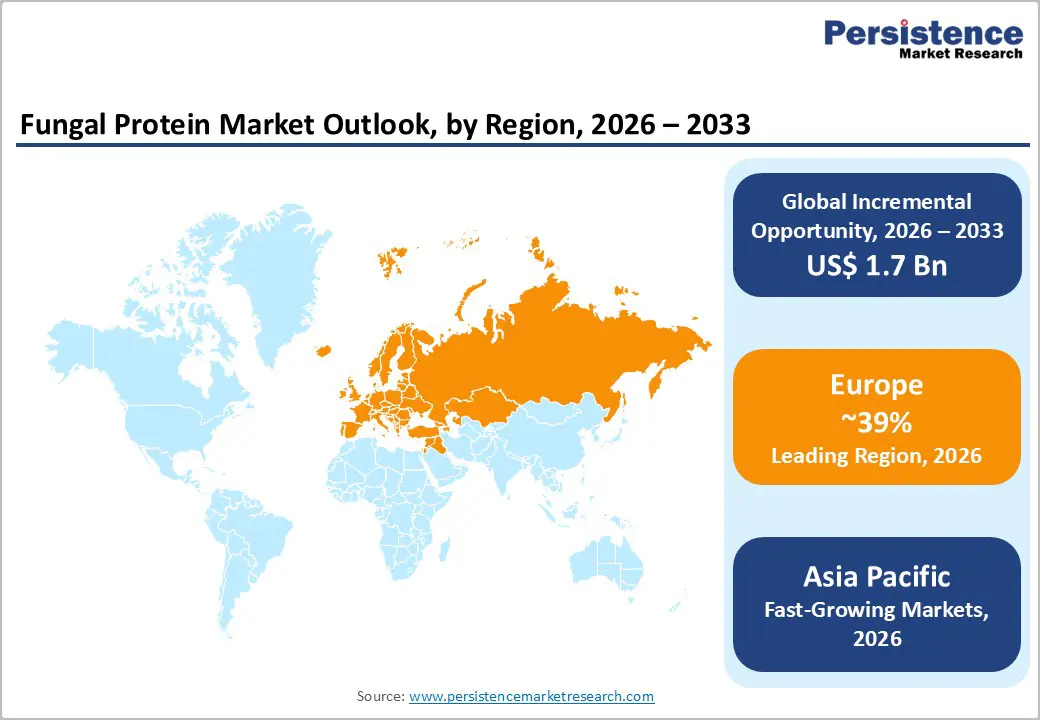

- Leading Region: North America, accounting for the largest share of the global fungal protein market, supported by strong venture capital inflows, advanced fermentation infrastructure, FDA GRAS pathways, and early adoption by foodservice and retail brands.

- Fastest-Growing Region: Asia Pacific, driven by rapid urbanization, expanding middle-class protein demand, government-backed food security initiatives, and the region’s deep-rooted cultural acceptance of fungi and fermented foods.

- Fastest-Growing Product Type Segment: Mycoprotein, propelled by its superior meat-like texture, clean-label positioning, and long-standing safety validation, making it the preferred base for next-generation meat alternatives and hybrid protein products.

- Market Drivers: Rising demand for sustainable and ethical protein alternatives, as fungal protein offers dramatic reductions in land, water, and emissions intensity versus animal agriculture, while aligning with global climate and food security goals.

- Opportunities: Expansion into nutritional supplements and functional snacking, leveraging fungal protein’s allergen-free profile, B-vitamin richness, beta-glucans, and compatibility with sports nutrition, RTD beverages, and high-protein snack formats.

- Key Developments: In September 2025, The Protein Brewery closed a €30 million Series B round to scale fungi-based protein platforms. In May 2025, Hydrosol and Planteneers showcased mycoprotein-based hybrid foods at IFFA Frankfurt, highlighting accelerating commercial momentum.

| Key Insights | Details |

|---|---|

| Fungal Protein Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Dynamics

Driver - Rising Global Demand for Sustainable and Ethical Protein Alternatives

The primary driver of the market is intensifying consumer concern about the environmental and ethical implications of industrial animal agriculture. According to reports from the Food and Agriculture Organization (FAO), livestock farming contributes significantly to global greenhouse gas emissions. Fungal protein, particularly mycoprotein produced through fermentation, requires approximately 90% less land and water than beef production. This substantial reduction in resource intensity aligns with the Intergovernmental Panel on Climate Change (IPCC) recommendations for dietary shifts. As a result, major food corporations are increasingly incorporating fungal biomass into their portfolios to meet corporate sustainability targets. The shift is not merely ethical; it is also driven by food security needs for a global population projected to reach 9.7 billion by 2050.

Restraints - High Capital Expenditure and Technical Complexity of Industrial Fermentation

The most significant barrier to market expansion is the prohibitively high cost of establishing large-scale fermentation infrastructure. Building a state-of-the-art production facility with a capacity of 10,000 tons per year can require an upfront investment of US$80-120 million. These high entry costs limit the market to well-capitalized players and established food tech leaders. Additionally, maintaining sterile conditions and optimizing biomass doubling times requires specialized bioprocessing expertise. Small and medium-sized enterprises often struggle to achieve the economies of scale necessary to compete with the pricing of conventional proteins or mature plant-based products such as soy protein isolate, which may slow overall market penetration in price-sensitive regions.

Opportunity - Exponential Growth in the Nutritional Supplements and Functional Snacking Sector

There is a massive opportunity for fungal protein to diversify beyond traditional meat analogs into the high-growth nutritional supplements category. As fitness culture goes mainstream, there is a rising demand for allergen-free, non-GMO protein powders and ready-to-drink (RTD) shakes. Fungal proteins, particularly yeast extracts, are already used for their high B-vitamin content and immune-boosting beta-glucans. Innovations in taste-masking technologies and microencapsulation allow manufacturers to incorporate fungal protein into protein bars and snacks without compromising sensory appeal. With the World Health Organization (WHO) emphasizing the need for diverse protein sources, companies that develop specialized sports nutrition lines using fungal ingredients can tap into a segment growing faster than the broader food market, leveraging the natural and fermented health halos.

Category-wise Analysis

By Product Type Insights

The Mycoprotein segment is the dominant force in this category, accounting for a significant majority of the value share. This dominance is attributed to its exceptional ability to replicate the texture of animal meat, a feature that has made it the benchmark for the meat-alternatives industry. Developed by brands such as Quorn (owned by Monde Nissin Corporation), mycoprotein is derived from the fungus Fusarium venenatum. Its market position is supported by more than 40 years of safety data and consumer familiarity. Statistics show that the fibrous nature of mycoprotein eliminates the need for heavy processing often required for pea or soy proteins. With a protein content of roughly 11-12% in its wet form and high fiber levels, it continues to lead as manufacturers seek cleaner and more meat-like ingredients.

By End-user Insights

The Meat Alternatives segment represents the largest portion of the market, holding a 47% market share in 2025. This leadership is driven by the global flexitarian movement, where consumers seek to reduce meat consumption without sacrificing the sensory experience of eating chicken or beef. Fungal proteins are uniquely suited for this, appearing in everything from burgers and nuggets to deli slices. The segment's growth is supported by data from the Good Food Institute, which indicates that taste and texture are the primary drivers of repeat purchases in the alt-protein space. Meanwhile, the Nutritional Supplements segment is identified as the fastest-growing end-use segment, as health-conscious consumers shift toward whole-food, fermented protein sources that offer functional benefits such as gut health support and high bioavailability.

Region-wise Insights

North America Fungal Protein Market Trends and Insights

North America remains a critical hub for innovation and venture capital investment in the fungal protein sector. The United States market leadership is characterized by a mature ecosystem of food tech startups, such as Nature's Fynd, which leverages unique fungal strains sourced from Yellowstone National Park. The U.S. regulatory framework is relatively conducive to growth, with the FDA providing clear GRAS notification pathways, enabling faster commercialization than in other regions.

Furthermore, the Silicon Valley of Food mindset has driven significant breakthroughs in precision fermentation. Strategic partnerships between traditional agricultural giants like Cargill and innovative startups are accelerating the scale-up of production facilities. Consumers in this region are increasingly looking for bioavailable and non-soy protein options, driving demand for fungal-based dairy and meat substitutes in both the retail and food service sectors, including major fast-food chains adopting mycoprotein-based menu items.

Asia Pacific Fungal Protein Market Trends and Insights

Asia-Pacific is the fastest-growing market for fungal protein, driven by rapid urbanization, a burgeoning middle class, and a significant shift in dietary habits in countries such as China, India, and Japan. The region's dietary westernization has created dual demand for protein: basic nutritional security and a growing appetite for premium, healthy alternatives. China is a major manufacturing hub, with companies such as Angel Yeast Co., Ltd. leveraging its substantial existing fermentation capacity to pivot toward high-quality protein production.

The manufacturing advantages in the Asia-Pacific region, including lower labor costs and extensive supply chains for fermentation feedstocks, make it an attractive destination for global companies to establish production bases. Additionally, the tradition of consuming fungi (mushrooms and fermented soy) in Asian cuisines provides a natural cultural bridge for the acceptance of mycoprotein. Governments across the ASEAN region are increasingly supportive of alternative proteins to enhance national food security, creating fertile ground for the 6.4% projected growth.

Competitive Landscape

The global fungal protein market is currently characterized by a consolidated structure at the top tier, where a few long-standing players like Monde Nissin Corporation (through Quorn Foods) and Cargill dominate the supply chain. However, the landscape is becoming increasingly fragmented as a wave of food tech startups enters the space with proprietary fermentation technologies. Key strategies employed by market leaders include vertical integration and strategic partnerships to secure feedstock supplies and R&D capabilities.

Companies are focusing on Product Differentiation by developing whole-food fungal ingredients that require minimal processing. There is also a significant trend toward Collaborative Innovation, where ingredient specialists like DSM-Firmenich and Givaudan work with startups to improve the sensory profiles of fungal proteins. Emerging business models are shifting toward Protein-as-a-Service, where companies provide fermentation platforms for third-party food manufacturers to create their own branded alt-protein lines.

Key Developments:

- In September 2025, The Protein Brewery secured €30 million in a Series B funding round to scale its fungi-based ingredient platform and accelerate commercialization across alternative protein applications.

- In May 2025, Hydrosol and Planteneers highlighted mycoprotein-based hybrid foods and meat alternatives at IFFA Frankfurt, underscoring growing industry momentum toward fungi-driven protein innovation.

Companies Covered in Fungal Protein Market

- Monde Nissin Corporation

- Cargill, Incorporated

- DSM-Firmenich

- Lallemand

- Angel Yeast Co., Ltd.

- Novozymes

- Givaudan

- VW-Ingredients

- Nature's Fynd

- Others

Frequently Asked Questions

The global fungal protein market is expected to reach a valuation of US$ 3.1 billion in 2026, growing steadily as fermentation technologies scale globally.

The primary drivers include the rising consumer preference for Sustainable and Ethical food sources, along with the superior Nutritional Profile of fungal biomass, which offers a complete amino acid profile and high fiber content.

Europe is the leading region, holding a 39% market share in 2025, supported by established brands like Quorn and a strong regulatory focus on sustainability.

A significant opportunity lies in the Nutritional Supplements sector and the adoption of Precision Fermentation, which allows for more cost-effective and functionally diverse protein production.

Key market participants include Monde Nissin Corporation, Cargill, Incorporated, DSM-Firmenich, Angel Yeast Co., Ltd., and innovative startups like Nature's Fynd and ENOUGH.