- Food Ingredients & Additives

- Sweet Protein Market

Sweet Protein Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Sweet Protein Market by Source (Microorganisms, Plants), by Form (Liquid, Powder), by Application (Food & Beverage, Pharmaceuticals, Nutrition & Sports Nutrition, Others), by Regional Analysis, 2026 - 2033

Sweet Protein Market Share and Trends Analysis

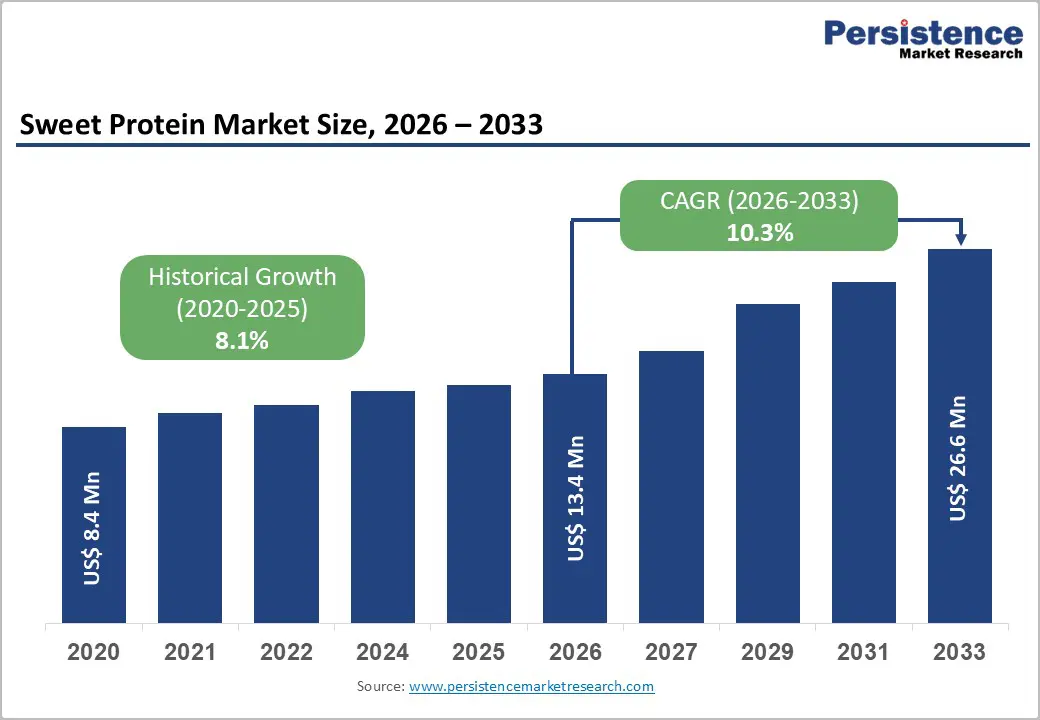

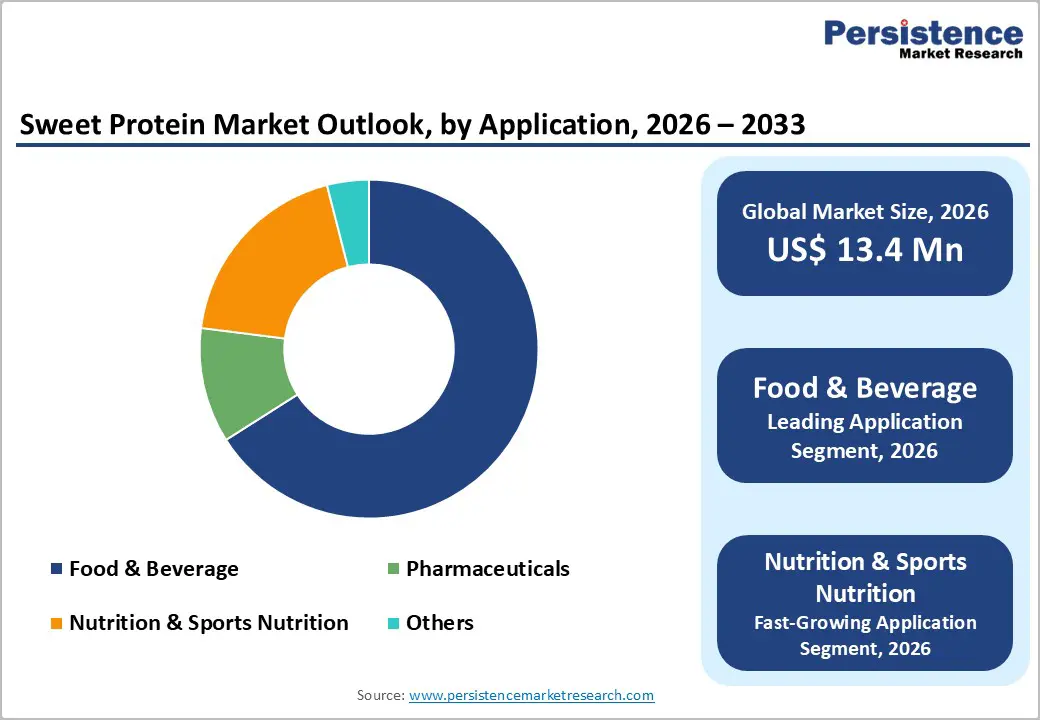

The global sweet protein market size is expected to be valued at US$ 13.4 million in 2026 and projected to reach US$ 26.6 million by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

The market is primarily driven by the escalating global demand for high-potency, zero-calorie sugar alternatives that do not compromise the sensory profile of food products. As clinical evidence links excessive sugar consumption to metabolic syndromes, both consumers and manufacturers are pivoting toward sweet proteins like Brazzein and Thaumatin. These proteins are preferred because they are metabolized as proteins rather than carbohydrates, ensuring a zero-glycemic response.

Key Industry Highlights:

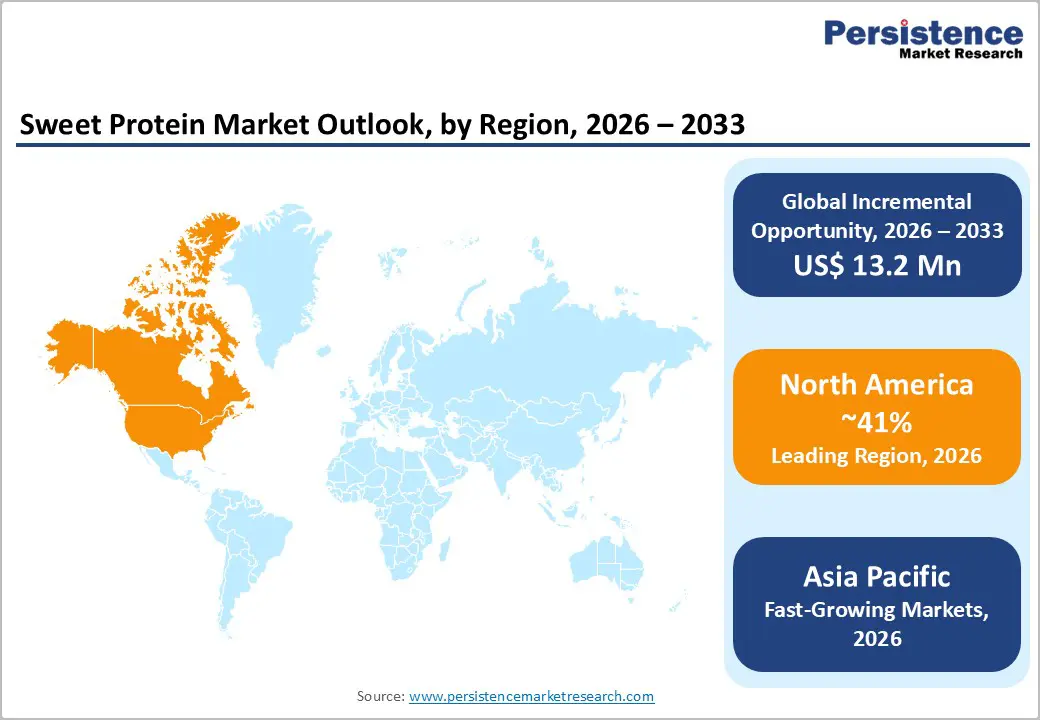

- Leading Region: North America dominated the market with a 41% share in 2025, driven by a mature biotech sector, favorable FDA regulatory pathways, and high consumer demand for sugar-free clean label products.

- Fastest Growing Region: Asia Pacific is projected to witness the highest CAGR due to rising diabetic populations in China and India and expanding manufacturing capabilities in precision fermentation technology.

- Dominant Segment: The Food & Beverage application held a 66% market share in 2025, as global brands aggressively reformulate sodas and snacks to avoid sugar taxes and meet health trends.

- Fastest Growing Segment: Nutrition & Sports Nutrition is the fastest-growing application, as athletes transition away from artificial sweeteners in favor of natural, protein-based ingredients that align with holistic wellness goals.

- Key Market Opportunity: Strategic partnerships between biotech startups and Fortune 500 food giants offer a massive pathway for scaling Precision Fermentation technologies and achieving mass-market penetration across global supply chains.

| Key Insights | Details |

|---|---|

|

Global Sweet Protein Market Size (2026E) |

US$ 13.4Mn |

|

Market Value Forecast (2033F) |

US$ 26.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

10.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.1% |

Market Dynamics

Driver - Rising Global Health Advocacy and Sugar Tax Implementation

The surge in lifestyle-related disorders, particularly Type 2 diabetes and obesity, has prompted international health bodies like the World Health Organization (WHO) to advocate for reduced free sugar intake. In response, over 50 jurisdictions globally, including the United Kingdom, Mexico, and several U.S. cities, have implemented sugar-sweetened beverage (SSB) taxes. This regulatory pressure is a significant catalyst for the Sweet Protein Market, as manufacturers seek clean label ingredients that can achieve the requisite sweetness without the tax burden. Sweet proteins offer a unique advantage over synthetic sweeteners like Aspartame, as they are naturally occurring and align with the clean label movement. According to the International Diabetes Federation (IDF), the global diabetic population is expected to reach 643 million by 2030, further solidifying the long-term demand for zero-glycemic sweeteners.

Restraints - High Production Costs and Scale-Up Complexity

Despite the promise of fermentation, the initial capital expenditure for bioreactor infrastructure and the complexity of downstream processing remain significant barriers. Sweet proteins are required in minute quantities due to their extreme potency (often 1,000 to 3,000 times sweeter than sucrose), yet achieving the necessary purity levels to ensure a clean taste profile is technically demanding. As of 2025, the cost-per-unit of sweetness for many sweet proteins remains higher than that of high-intensity sweeteners like Sucralose or even refined sugar in some regions. This price disparity can deter budget-conscious manufacturers in emerging markets from switching, particularly when traditional sweeteners are highly subsidized.

Opportunity - Integration in the Nutrition & Sports Nutrition Sector

The Nutrition & Sports Nutrition segment presents a massive opportunity for sweet protein adoption, fueled by the growing active lifestyle consumer base. Athletes and fitness enthusiasts are increasingly avoiding artificial sweeteners due to concerns over gut health and the microbiome. Sweet proteins, being natural amino acid chains, are perceived as a functional sweetening solution that fits perfectly within protein powders, amino acid supplements, and energy bars. Innovations in this space are expected to drive a CAGR exceeding the market average between 2026 and 2033. As the Global Wellness Institute highlights the shift toward proactive health, sweet proteins are positioned as the gold standard for high-performance nutrition products that require a premium, natural ingredient profile.

Category-wise Analysis

Source Insights

The plants segment held the leading position in the sweet protein market in 2025, accounting for a market share of approximately 58%. This dominance is attributed to the long-standing use of Thaumatin, which is extracted from the Katemfe fruit indigenous to West Africa. Thaumatin has benefited from early regulatory approvals and a well-established supply chain compared to lab-grown alternatives. However, the Microorganisms segment is rapidly gaining ground. The reliance on plant-based extraction is often limited by climate variability and low protein yields in the fruit. Consequently, the industry is shifting toward fermentation-based sources to ensure sustainability. While plant-derived proteins currently lead in volume, the consistency and purity offered by microbial synthesis are becoming the preferred choice for high-end Food & Beverage applications.

Application Insights

The food & beverage application stands as the dominant segment, capturing a 66% market share in 2025. The demand within this segment is primarily concentrated in the soft drinks, dairy, and confectionery sub-sectors. Beverage manufacturers, in particular, are the most aggressive adopters of sweet proteins as they seek to navigate the war on sugar without resorting to synthetic chemicals that might alienate health-conscious consumers. The ability of sweet proteins to provide a clean sweetness without the bitter aftertaste associated with some Stevia extracts makes them a premium choice for high-end diet and zero drink lines. This segment's lead is reinforced by the sheer volume of production in the global soft drink industry.

Region-wise Insights

North America Sweet Protein Market Trends and Insights

North America is the leading regional market, holding a 41% share in 2025. The region’s dominance is anchored by the United States, which serves as the global hub for food biotechnology and venture capital investment. The presence of pioneering companies like Sweegen, Inc. and Oobli has accelerated the commercialization of sweet proteins. The U.S. FDA’s flexible GRAS notification framework provides a more streamlined path for innovative sweeteners compared to other regions, fostering a vibrant ecosystem of startups and pilot-scale production facilities.

Furthermore, American consumers are increasingly scrutinizing labels for added sugars, a trend amplified by the U.S. Department of Agriculture (USDA) dietary guidelines. This has led to a surge in demand for sugar-reduced snacks and functional beverages in retail channels like Whole Foods and Amazon. The tech-forward approach to food in North America, combined with high disposable income and a robust fitness culture, ensures that the region remains the primary revenue generator for the Sweet Protein Market through 2033.

Asia Pacific Sweet Protein Market Trends and Insights

Asia Pacific is the fastest-growing region for the Sweet Protein Market. The rapid urbanization in China, India, and ASEAN countries has brought about a significant shift in dietary habits, leading to a diabetes epidemic that governments are desperate to curb. China, already a global leader in the production of high-intensity sweeteners, is now investing heavily in precision fermentation to diversify its ingredient exports. The region's manufacturing advantages, including lower labor costs and massive fermentation capacity, make it an ideal base for the mass production of sweet proteins.

In Japan, the concept of Functional Foods is deeply ingrained in the culture, leading to early adoption of sweet proteins in teas and health drinks. India is also emerging as a critical market, with a growing middle class that is becoming increasingly wary of sugar. As local manufacturers in the Asia Pacific region begin to incorporate sweet proteins into traditional sweets and beverages to meet new labeling laws, the region's CAGR is expected to outpace all other geographical segments during the forecast period.

Competitive Landscape

The sweet protein market is currently fragmented, characterized by a mix of specialized biotech startups and established global ingredient players. Companies like Tate & Lyle PLC and Sweegen, Inc. are leveraging their extensive distribution networks and formulation expertise to integrate sweet proteins into broader sweetness systems. Meanwhile, startups like Amai Proteins and Oobli are the primary drivers of innovation, focusing on computational protein design and precision fermentation.

The key differentiator in this market is the ability to achieve a sugar-like sweetness curve without a lingering aftertaste. Leading players are increasingly adopting platform-based business models, offering multiple types of sweet proteins to provide tailored solutions for different food matrices (e.g., acidic beverages vs. pH-neutral dairy). Strategic R&D and securing patent portfolios for specific fermentation strains are the dominant growth strategies.

Key Developments:

- In October 2025, Oobli achieved a key regulatory milestone by securing its third FDA no questions letter, confirming brazzein-54 as GRAS for use as a sweetener in foods and beverages and strengthening its position in the next-generation protein sweetener space.

- In February 2025, Oobli partnered with Ingredion to accelerate market access for affordable, great-tasting sweetener systems, combining Oobli’s protein-based sweeteners with Ingredion’s stevia solutions to advance next-generation, healthier sugar reduction across foods and beverages.

Companies Covered in Sweet Protein Market

- Tate & Lyle PLC

- Sweegen, Inc.

- Oobli

- Amai Protein

- Lifeasible

- Miraburst

- Sunesta Life Science

- Amyris, Inc.

- Talin

- Brain Biotech AG

- Others

Frequently Asked Questions

The global sweet protein market is projected to be valued at US$ 13.4 Mn in 2026.

Rising Global Health Advocacy and Sugar Tax Implementation is driving demand for Sweet Protein market.

The Global Sweet Protein market is poised to witness a CAGR of 10.3% between 2026 and 2033.

Integration in the Nutrition & Sports Nutrition Sector is key opportunity for key players in the market.

The market is led by global giants such as Tate & Lyle PLC, Sweegen, Inc., Oobli, Amai Protein, Sunesta Life Science, Amyris, Inc., and others.