- Beverages

- Global Keto-Friendly Sodas Market

Global Keto-Friendly Sodas Market Size, Share, and Growth Forecast 2026 - 2033

Keto-Friendly Sodas Market by Flavor (Cola, Fruit-based, Others), by Distribution Channel (Business to Business, Business to Consumer), by End-use (Food & Beverage Industry, Foodservice Industry, Others), by Regional Analysis, 2026-2033

Keto-Friendly Sodas Market and Trends Analysis

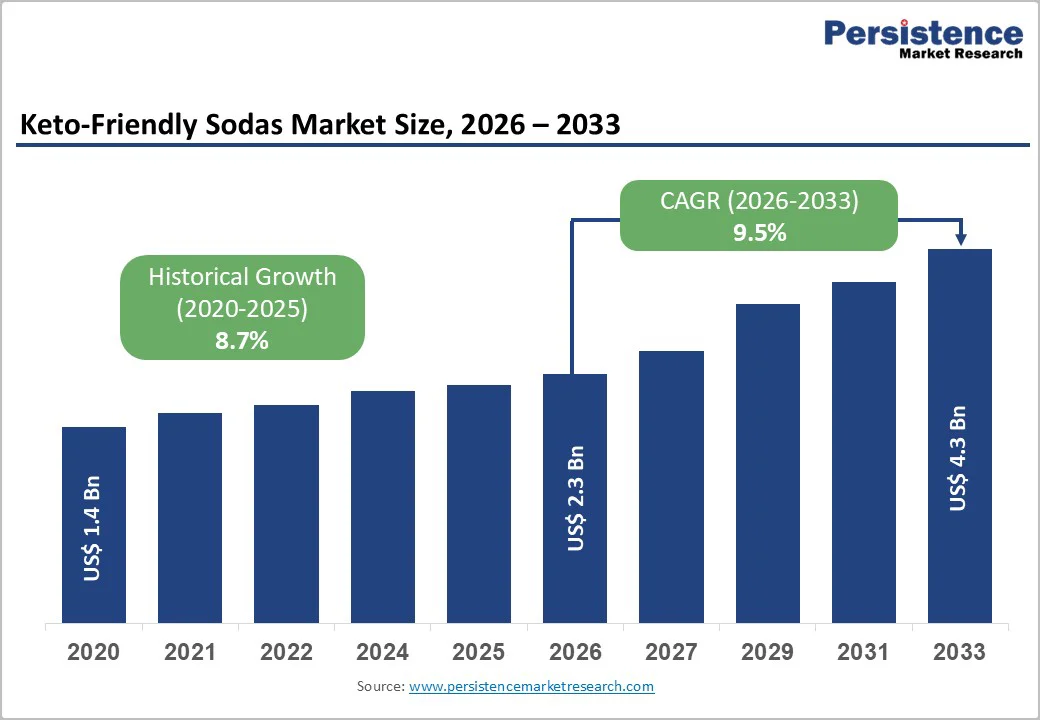

The global keto-friendly sodas market size is expected to be valued at US$ 2.3 billion in 2026 and is projected to reach US$ 4.3 billion by 2033, growing at a CAGR of 9.5% between 2026 and 2033.

Market expansion is driven by rising health consciousness, sugar-reduction policies, and growing adoption of low carb and ketogenic diets that favor zero sugar, low calorie beverages. The World Health Organization (WHO) recommends limiting free sugars to below 10% of total energy intake, with additional benefits below 5%, encouraging manufacturers and consumers to pivot toward sugar-free soft drinks, including keto-friendly sodas. Rapid innovation in sweetening systems such as stevia, erythritol, and monk fruit enables brands to deliver familiar cola and fruit flavors without raising blood glucose, aligning keto sodas with broader zero sugar and low and no calorie soda trends worldwide.

Key Industry Highlights

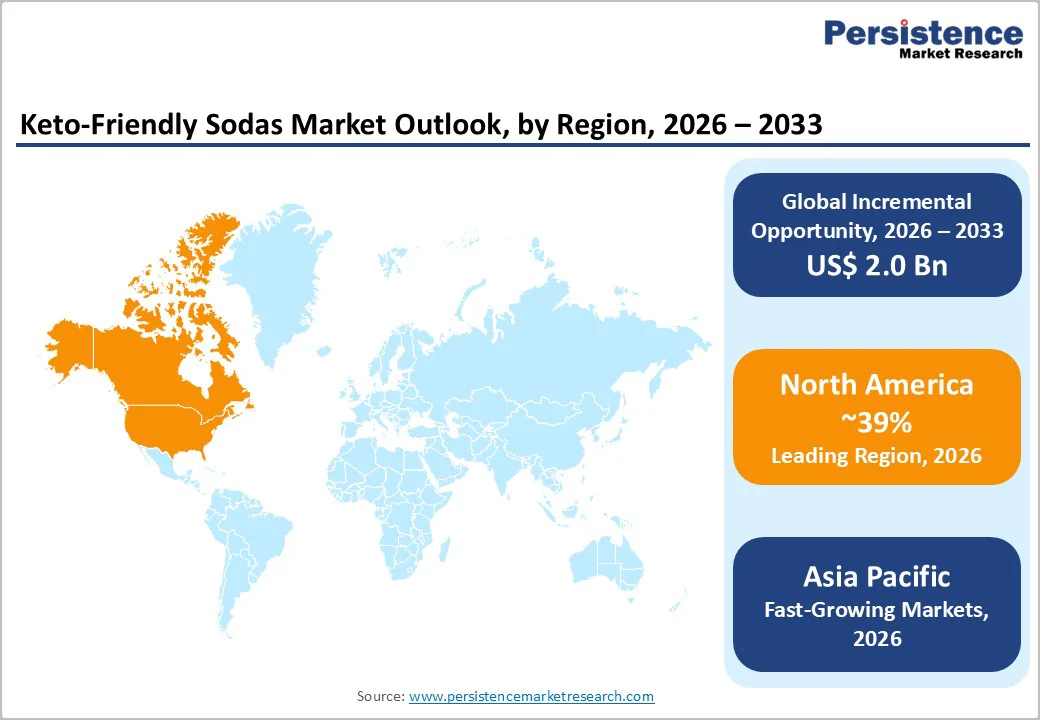

- Leading Region: North America leads the global keto-friendly sodas market, supported by high diet soda penetration, sugar reduction policies, and strong ketogenic and low carb diet adoption.

- Fastest Growing Region: Asia Pacific is the fastest growing region for keto-friendly sodas, as rising obesity concerns, growing middle class incomes, and rapid expansion of modern retail and e commerce accelerate the shift toward zero sugar and low carb beverage choices.

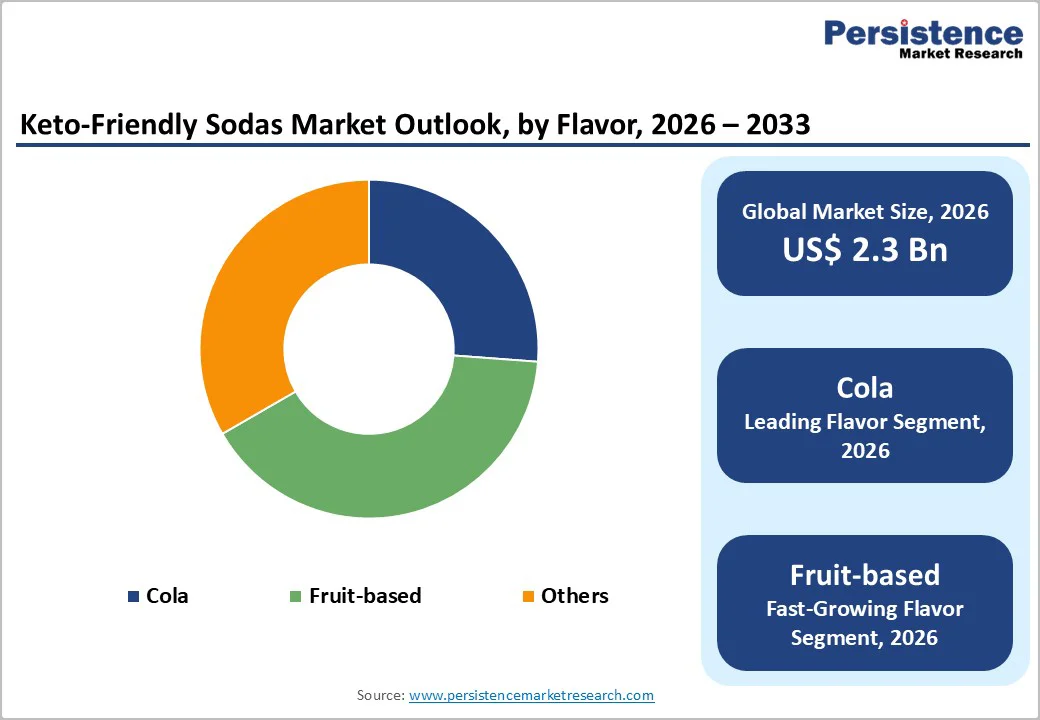

- Dominant Segment: Cola flavor remains the dominant segment benefiting from brand familiarity, extensive marketing by global soft-drink leaders, and successful reformulation into zero sugar, keto compatible variants.

- Fastest Growing Segment: Online Retail within the B2C distribution structure is anticipated to be the fastest growing channel, leveraging subscriptions, community marketing, and targeted keto-diet campaigns to reach digitally savvy, health conscious consumers.

| Global Market Attributes | Key Insights |

|---|---|

| Keto-Friendly Sodas Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 4.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.5% |

| Historical Market Growth (CAGR 2020 to 2024) | 8.7% |

Market Dynamics

Driver – Health-driven sugar reduction and ketogenic lifestyles

Escalating concerns about obesity, type 2 diabetes, and metabolic syndrome are prompting consumers and policymakers to reduce intake of sugar-sweetened beverages. The WHO guidelines that advocate keeping free sugars below 10% of daily energy intake, and ideally 5%, have catalyzed fiscal measures and reformulation efforts in many countries, leading consumers to seek sugar-free alternatives. Keto-friendly sodas, formulated with zero calorie sweeteners and minimal net carbohydrates, appeal not only to strict ketogenic diet followers but also to broader low sugar, low carb audiences, echoing trends seen in the wider zero sugar beverages and diet soft drinks markets. Manufacturers highlight “keto,” “zero sugar,” and “zero net carbs” claims on packaging, reinforcing health credentials and supporting premium pricing compared with conventional sodas.

Innovation in sweetening technology and functional formulations

Advances in sweetening technology are significantly improving the taste profile and acceptance of keto-friendly sodas. Companies increasingly employ combinations of high intensity sweeteners such as stevia, sucralose, and monk fruit, often blended with sugar alcohols like erythritol, to deliver sweetness curves similar to sucrose without the associated glycemic load. Simultaneously, some brands are adding functional ingredients electrolytes, vitamins, caffeine, green tea extracts, or probiotics to position keto sodas as both refreshing and performance- or wellness-oriented, echoing developments in the broader zero sugar beverages market where functional “gut healthy” or energy sodas are gaining traction. These innovations enhance consumer perception, expand usage occasions, and support category growth beyond simple “diet” alternatives.

Restraints – Consumer skepticism about artificial sweeteners and long-term safety

Despite strong health positioning, keto-friendly sodas face skepticism from consumers wary of artificial sweeteners and ultra processed beverages. Public debates over the safety and metabolic impacts of sweeteners such as aspartame or sucralose, and evolving evaluations by regulatory bodies, can dampen demand among health-conscious shoppers who might otherwise choose keto products. Some consumers prefer naturally flavored sparkling water or unsweetened beverages instead, which can slow conversion from traditional sodas to keto-specific offerings.

Regulatory scrutiny and sugar tax spillover effects

Sugar tax regimes and front of pack nutrition labelling rules are mainly targeted at high sugar beverages but can indirectly impact keto-friendly sodas. In markets where thresholds are based on total energy or sweetener content, brands must closely manage formulations and claims to avoid confusion and comply with evolving labelling, advertising, and health claim regulations. Additionally, some advocacy groups call for broader restrictions on marketing of all sweetened beverages, including zero sugar variants, particularly to children, which can constrain promotional strategies and shelf placement.

Opportunity – Premium fruit-based keto sodas and flavor diversification

The Fruit-based flavor segment offers substantial growth potential as consumers look for variety beyond classic colas while remaining within keto and low carb parameters. Innovations in natural flavor extraction and non nutritive sweeteners allow the development of citrus, berry, tropical, and botanical profiles that mimic traditional fruit sodas without sugar, a direction already evident in broader zero sugar carbonated drink portfolios. Brands that highlight real fruit flavors, natural colors, and clean label claims can differentiate from generic “diet” sodas and capture flavor seeking consumers who might otherwise exit the category. Limited edition seasonal flavors and collaborations with mixologists or functional beverage brands can further elevate the fruit-based keto soda proposition.

Category-wise Analysis

Flavor Analysis

In the Flavor category, Cola is estimated to hold around 38% share of the keto-friendly sodas market in 2025, making it the leading segment. Consumers transitioning from regular soft drinks often seek familiar cola taste profiles, and major beverage companies have invested heavily in perfecting zero sugar cola formulations that closely mimic their flagship products. Diet and zero sugar colas already account for a substantial portion of low and no calorie soda sales, benefiting from brand equity, extensive distribution, and strong marketing support. This momentum carries into the explicitly “keto-friendly” cola segment, where formulations emphasize zero sugar, low net carbs, and sometimes added caffeine or functional ingredients, anchoring the category against which fruit-based and “Others” flavors compete for incremental occasions.

Distribution Channel Analysis

Within Distribution Channel, Business to Consumer Hypermarkets/Supermarkets can be viewed as the leading segment, capturing an estimated 45% share of keto-friendly soda sales in 2025. Large retailers remain primary shopping destinations for soft drinks, dedicating significant shelf space to diet and zero sugar ranges from leading brands such as Pepsi and Coca Cola, alongside emerging keto-centric labels. Their strong promotional capabilities multi buy offers, end cap displays, and loyalty programs help drive trial and repeat purchases. However, Online Retail within the B2C structure is the fastest growing sub channel, as health-conscious shoppers increasingly purchase beverages via e commerce, enabling discovery of niche keto brands, bulk ordering, and subscription services that are less feasible in-store.

Region-wise Insights

North America Keto-Friendly Sodas Market Trends

North America is the leading regional market, representing around 39% of global keto-friendly soda sales in 2025, underpinned by high soft-drink consumption, widespread diet soda acceptance, and strong ketogenic and low carb diet communities. The U.S. has implemented or experimented with sugar-sweetened beverage taxes in several jurisdictions, while public health bodies emphasize reducing added sugars, reinforcing consumer migration toward low and no calorie alternatives. Data indicate that North America accounts for nearly two fifths (about 38.7%) of global turnover in sugar-free carbonated soft drinks, reflecting the region’s readiness to adopt zero sugar formulations.

Major brands such as Pepsi, Coca Cola, Red Bull, and emerging functional soda labels increasingly highlight “zero sugar,” “keto,” and “no net carbs” on packaging and marketing campaigns, while sparkling water brands like La Croix and Perrier further normalize unsweetened or naturally flavored options. Robust convenience-store networks and vending channels extend reach to on the go consumers, while e commerce and club stores support bulk purchases for home consumption. Innovation hubs in the U.S. beverage sector also foster start ups producing niche keto sodas with added nootropics, adaptogens, or electrolytes, enriching the competitive landscape.

Europe Keto-Friendly Sodas Market Trends

Europe presents a dynamic environment for keto-friendly sodas, shaped by stringent sugar reduction policies, front of pack labelling schemes, and strong consumer interest in healthier beverages. The U.K. Soft Drinks Industry Levy (SDIL) led to substantial reformulation, with studies showing significant reductions in sugar content across carbonated soft drinks and related categories, demonstrating manufacturers’ responsiveness to policy signals. Similar initiatives and voluntary reformulation programs in countries such as Germany, France, and Spain encourage the proliferation of zero sugar and low calorie beverages, including options tailored to low carb and keto lifestyles.

European consumers increasingly scrutinize ingredient lists and are receptive to naturally sweetened sodas that use stevia or plant-based sweeteners rather than artificial alternatives. Large multinational brands offer zero sugar colas and flavored drinks alongside emerging craft and functional sodas positioned as organic, botanical, or gut friendly. The expansion of discounters and private-label ranges, combined with strong online grocery growth particularly in the U.K. and parts of Western Europe creates opportunities and price pressure simultaneously, pushing keto-friendly soda brands to differentiate via taste, functionality, and sustainability credentials.

Asia and Pacific Keto-Friendly Sodas Market Trends

Asia Pacific is projected to be the fastest growing region for keto-friendly sodas between 2025 and 2032, reflecting rising incomes, urbanization, and heightened awareness of diet-related diseases. Countries such as China, Japan, South Korea, India, and Australia are seeing rapid growth in zero sugar and low calorie beverages as governments and medical associations highlight links between sugary drink consumption, obesity, and diabetes. The spread of Western-style QSR chains, cafés, and convenience stores fuels demand for ready-to-drink sodas and energy beverages, with diet or sugar-free variants gaining share among younger, health conscious consumers.

Regional and global players are launching fruit-based and tea inspired keto-friendly formulations that resonate with local taste profiles for example green-tea or citrus forward sparkling drinks that use natural sweeteners. Online marketplaces and super apps play an outsized role in beverage distribution, enabling direct engagement with keto communities and fitness enthusiasts. Meanwhile, manufacturing investments and partnerships in countries such as India and members of ASEAN help reduce production costs and support export of keto sodas to neighboring markets, reinforcing Asia Pacific’s status as the fastest growing hub.

Market Competitive Landscape

The keto-friendly sodas market is moderately consolidated at the top, with global beverage giants complemented by agile niche brands and functional drink startups. Major companies such as Pepsi and Coca Cola leverage extensive bottling infrastructure, marketing budgets, and distribution networks to scale zero sugar cola and flavored lines that naturally appeal to keto consumers. At the same time, brands like Celsius Naturals, MatchaBar Hustle Sparkling Matcha Energy Drink, RUNA Energy Drinks, Solimo Silver Energy Drink, EBOOST Super Fuel, Perrier, and La Croix position themselves at the intersection of energy, hydration, and wellness, often emphasizing natural ingredients, botanicals, or functional benefits. Emerging business models include D2C subscriptions, influencer driven launches, and collaborations with gyms and wellness programs, while R&D focuses on flavor masking, sweetener blends, and functional ingredient stability.

Key Industry Developments:

- In August 2025, OLIPOP launched a SpongeBob-inspired soda, sparking strong fan excitement and high consumer demand.

- In April 2022, Coca Cola launched Coca Cola Zero Sugar Byte, a limited edition zero sugar beverage aimed at younger digital consumers, illustrating the brand’s commitment to expanding its zero sugar innovation pipeline.

Companies Covered in Global Keto-Friendly Sodas Market

- Pepsi

- Coca-Cola

- Red bull

- Celsius Naturals

- MatchaBar Hustle Sparkling Matcha Energy Drink

- RUNA Energy Drinks

- Solimo Silver Energy Drink

- EBOOST Super Fuel

- Perrier

- La Croix

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 2.3 Bn in 2026.

Demand is driven by sugar‑reduction policies, growing prevalence of obesity and diabetes, rising popularity of low‑carb and ketogenic diets, and advances in sweeteners that enable great‑tasting zero‑sugar colas and fruit sodas.

The global market is expected to witness a CAGR of 9.5 between 2026 and 2033.

A major opportunity lies in fruit-based and functional keto sodas featuring natural flavors, clean-label sweeteners, and added benefits such as probiotics, energy ingredients, or electrolytes, distributed through fast-growing online and D2C channels.

Key companies include Pepsi, Coca-Cola, Red Bull, Celsius Naturals, MatchaBar Hustle Sparkling Matcha Energy Drink, RUNA Energy Drinks.