- Processed Food

- Precision Fermentation Market

Precision Fermentation Market Size, Share, and Growth Forecast, 2026 - 2033

Precision Fermentation Market By Ingredient Type (Dairy Proteins, Egg Proteins, Others), Application (Food & Beverages, Personal Care & Cosmetics, Others), Production Approach, Business Model, and Regional Analysis for 2026 - 2033

Precision Fermentation Market Size and Trends Analysis

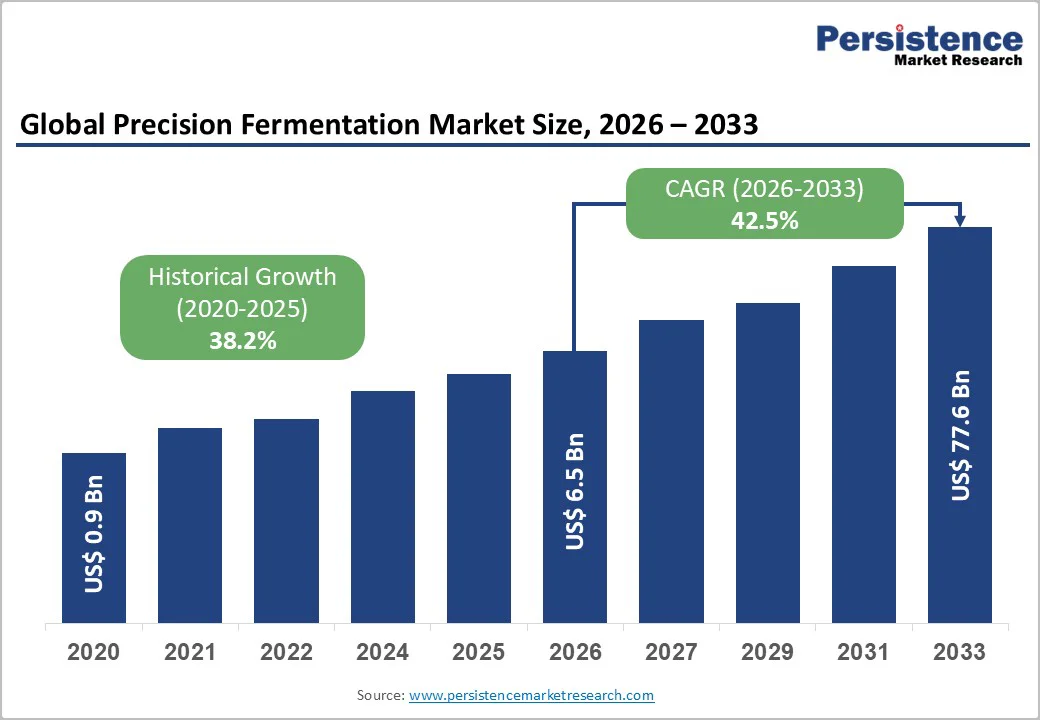

The global precision fermentation market size is likely to be valued at US$6.5 Billion in 2026. It is expected to reach US$77.6 Billion by 2033, growing at a CAGR of 42.5% during the forecast period from 2026 to 2033, driven by advances in microbial engineering, scalable bioprocessing systems, and rising demand for functional, high-purity proteins, enzymes, and specialty lipids.

Companies across food, personal care, pharmaceuticals, and animal nutrition are integrating fermentation-derived ingredients to enhance formulation performance, improve consistency, and reduce dependency on traditional raw materials. Growth is driven by a broader innovation pipeline, enhanced strain-design capabilities, and clearer regulatory frameworks in regions, including the U.S. and Europe.

Key Industry Highlights

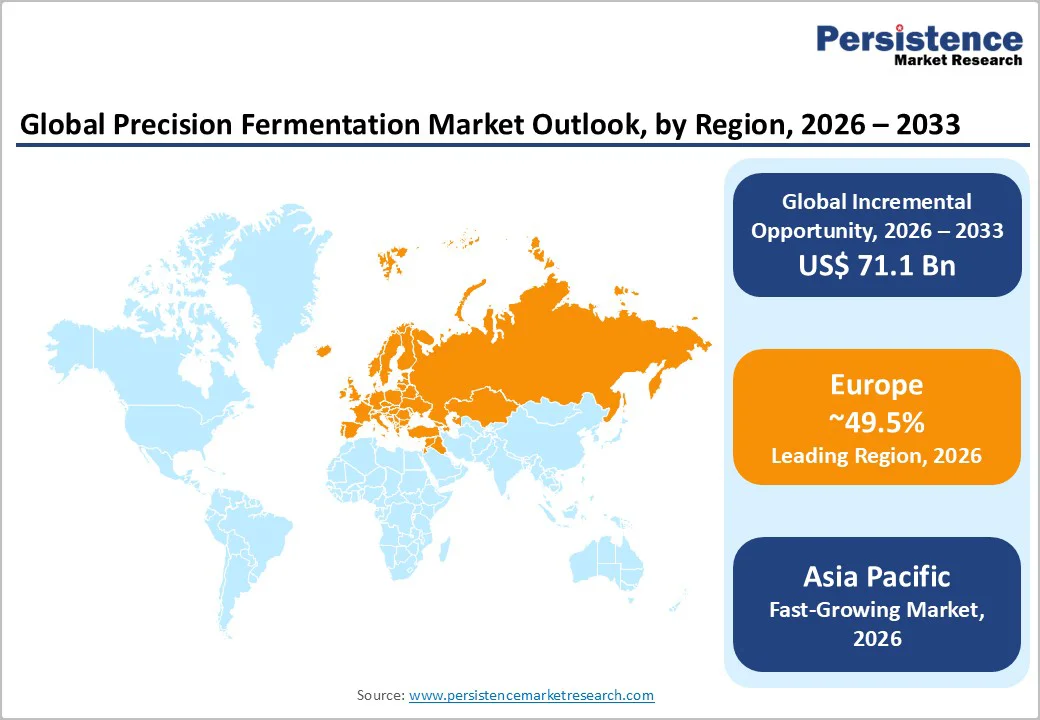

- Leading Region: Europe is anticipated to account for approximately 49.5% of the global precision-fermentation market value in 2026, driven by its structured regulatory framework, strong public research base, and mature food-manufacturing ecosystem.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, supported by expanding fermentation infrastructure in China and India, cost-efficient manufacturing capabilities, and increasing product trials across Japan and ASEAN markets.

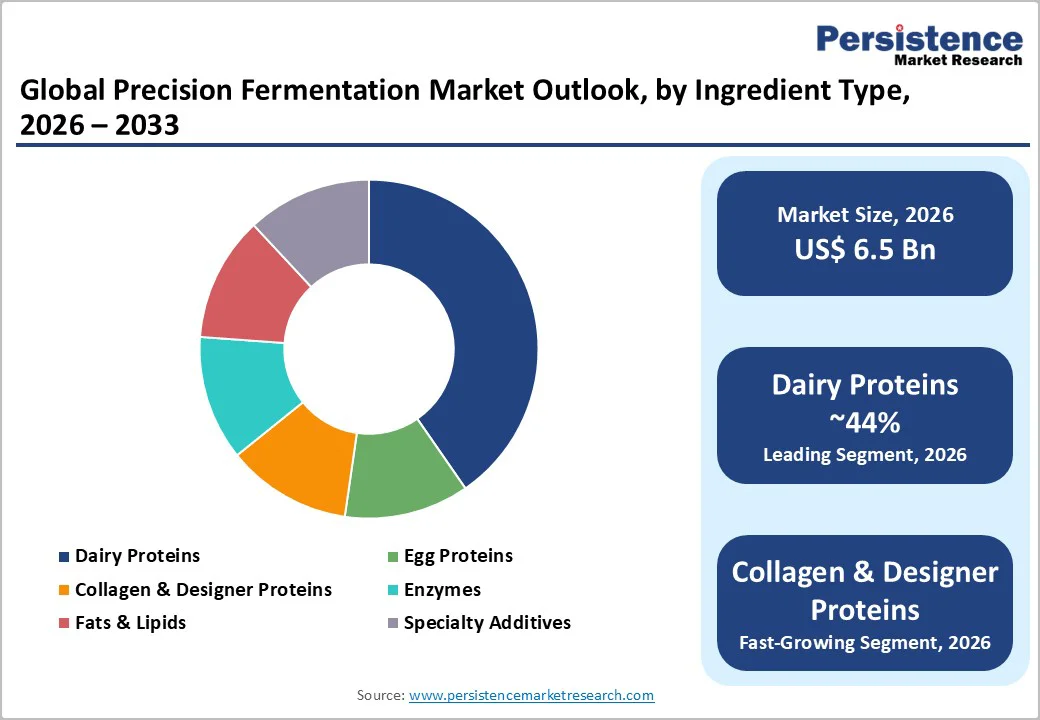

- Dominant Ingredient Type: Dairy proteins are expected to remain the largest ingredient category in 2026, accounting for around 44% of total precision-fermentation ingredient value, driven by strong commercial interest, early regulatory activity, and clear application pathways in beverages, specialty nutrition, and dairy alternatives.

- Leading Application: Food and beverages are likely to account for over 49% of total application demand, driven by the adoption of dairy-identical proteins, functional enzymes, and flavor compounds in reformulation projects, private-label trials, and specialty product development.

| Key Insights | Details |

|---|---|

| Precision Fermentation Market Size (2026E) | US$6.5 Bn |

| Market Value Forecast (2033F) | US$77.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 42.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 38.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Improving Unit Economics through Scale and Process Optimization

Advances in strain engineering, substrate conversion efficiency, feedstock flexibility, and bioreactor capacity continue to reduce the cost of goods sold for precision-fermented ingredients. Larger fermentation vessels, optimized downstream purification, and iterative process improvements allow companies to target higher-value functional proteins and enzymes. Industry analyses report consistent declines in production costs over pilot-to-commercial transitions.

Ingredient producers can now supply dairy proteins, collagen, egg proteins, and specialized enzymes at cost points appropriate for premium food, beverage, and personal-care categories. These economics strengthen the commercial case for precision fermentation as an alternative to animal-derived proteins.

Demand for Sustainable, Animal-Free Functional Ingredients

Consumer interest in environmentally efficient and animal-free ingredients is driving procurement shifts across food, beverage, and personal-care companies. Sustainability commitments and Scope 3 emissions targets create structured demand for low-impact proteins, enzymes, and lipids. Industry association work documents rising buyer intent from global consumer-goods companies that seek consistent quality and supply security.

Precision fermentation enables ingredient uniformity independent of agricultural variability, improving performance and labeling flexibility. This alignment of sustainability, quality, and consistency forms a reliable pull factor that accelerates adoption, especially in North America and Europe.

Barrier Analysis - Regulatory Burden and Labeling Complexity

Regulatory reviews for novel ingredients require significant documentation, safety testing, and process transparency. In the EU, Novel Foods approval demands comprehensive dossiers, extending timelines, and increasing costs.

In the U.S., self-affirmed GRAS places legal responsibility on companies to ensure safety, while FDA-reviewed GRAS can take longer but offers stronger validation. These requirements influence time-to-market and add compliance costs for smaller firms. Labeling norms also differ across jurisdictions, slowing uniform multinational launches.

Capital-Intensive Scale-Up and Manufacturing Risks

Building commercial-scale fermentation plants requires substantial capital expenditure, advanced process engineering capabilities, and stringent quality controls. Scaling from pilot to commercial capacity often reveals yield variability, production bottlenecks, or purification challenges that directly influence unit economics.

Uncertain performance at commercial scale can delay revenue and increase financing needs. These risks limit the number of companies that can independently build manufacturing assets, pushing many toward contract manufacturing or asset-light business models.

Opportunity Analysis - High-Margin Specialty Ingredients

Precision fermentation enables the production of functional dairy proteins, egg proteins, collagen alternatives, and specialized enzymes with performance comparable to traditional sources. These ingredients command premium pricing in food, beverage, cosmetics, and nutraceutical applications.

Multiple industry forecasts highlight significant addressable markets in dairy-identical proteins and designer enzymes, reflecting strong interest from multinational consumer brands. Co-branded product launches, ingredient licensing, and B2B supply agreements create rapid pathways to commercialization and reduce go-to-market risk.

Contract manufacturing & toll-fermentation capacity

A growing number of design-focused companies rely on third-party fermentation facilities to produce at scale, creating a strong opportunity for contract manufacturers with food-grade fermentation expertise. As more companies adopt an asset-light model, demand rises for large fermenters, GMP-capable plants, and downstream-processing capacity.

Several scale-up announcements across Israel, Asia, and Europe reflect a shift toward specialized fermentation hubs. These facilities support a consistent supply, allow ingredient companies to avoid capex-heavy plant builds, and accelerate time-to-market.

Category-wise Analysis

Ingredient Type Insights

Dairy proteins are expected to remain the largest ingredient type segment in 2026, holding an estimated market share of around 44%. Their dominance is linked to the established global infrastructure for whey and casein production, consistent quality, and wide applicability across sports nutrition, medical nutrition, infant formula, and functional foods.

Whey protein concentrates and isolates benefit from strong clinical validation, high amino-acid bioavailability, and robust supply chains built over decades by major dairy processors.

Demand from performance nutrition brands supports stable volume growth, while formulators favor dairy proteins for their emulsification, foaming, and solubility advantages. For example, ready-to-drink high-protein beverages launched in 2024 by several global beverage groups continue to rely on whey isolates as they deliver shelf-stable clarity and minimal off-flavors.

Designer proteins and collagen-based proteins are likely to be the fastest-growing ingredient category, driven by surging interest in functional wellness, beauty-from-within products, personalized nutrition, and the rapid emergence of precision-fermentation-derived designer proteins that mimic or exceed natural functionality.

Collagen maintains momentum due to its strong association with joint health and skin elasticity, while designer proteins attract investment as they offer tunable amino-acid sequences, improved digestibility, and sustainability advantages.

The segment’s rise is reinforced by partnerships between food-technology companies and beauty-nutrition brands. A notable example is a 2025 collaboration between a precision-fermentation protein developer and a global skincare company to integrate bio-identical collagen peptides into nutritional gummies.

Application Insights

Food and beverages are expected to constitute the largest application segment, contributing roughly 49% of total market demand in 2026. This leadership stems from the extensive use of dairy proteins, enzymes, fats, and specialty additives in bakery, dairy alternatives, sports nutrition, fortified beverages, confectionery, and high-protein snacks.

Rising consumer preference for clean-label, protein-rich, and functional foods reinforces consistent demand. Manufacturers prioritize these ingredients as they offer performance, flavor stability, and nutritional improvements, making them indispensable across mainstream and premium product lines.

A relevant example is the expansion of high-protein yogurts and functional RTD smoothies across the U.S. and Europe, which heavily rely on whey protein isolates, enzymatic texturizers, and specialty lipids.

Pharmaceuticals and bioprocessing enzymes are anticipated to be the fastest-growing application segment. Growth accelerates due to increasing use of highly purified proteins, enzymes, and specialty excipients in biologics production, cell-culture media, vaccine manufacturing, and advanced drug-delivery systems.

As biopharmaceutical pipelines widen, demand rises for ingredients that ensure high stability, controlled release, and efficient bioprocessing performance. This segment benefits from stringent regulatory standards that prioritize traceability and high functionality, leading to premium pricing and rapid adoption.

For example, in 2025, several bioprocessing firms increased procurement of specialty enzymes engineered for high-yield fermentation, enabling more efficient production of monoclonal antibodies and next-generation therapies.

Regional Insights

North America Precision Fermentation Market Trends - Innovation-Driven Scale-Up and Regulatory Flexibility

North America is expected to grow steadily, supported by a strong innovation network, active venture funding, and clear regulatory rules. Companies can use GRAS notifications, either on their own or through FDA review, to confirm ingredient safety, helping them get ready for early commercial use.

Several U.S.-based firms have advanced from pilot-scale production to strategic B2B partnerships in specialty proteins, enzymes, and functional lipids. Innovation clusters in California, Colorado, and Massachusetts continue to drive progress in strain engineering, metabolic pathway optimization, and downstream process intensification. Capital availability remains selective but resilient, with investors favoring companies capable of demonstrating quantifiable production-cost reductions and clear regulatory roadmaps.

Recent developments include the commissioning of new demonstration-scale fermentation facilities in the Midwest focused on dairy-identical proteins, as well as a series of co-development agreements between ingredient technology startups and major beverage and snack manufacturers for high-purity flavor molecules.

Several companies also reported successful techno-economic assessments, indicating improved yield efficiencies at 30,000-L and 50,000-L runs. These milestones highlight North America’s growing capacity to transition from R&D to repeatable, scalable production, reinforcing the region’s influence on global commercial strategies.

Europe Precision Fermentation Market Trends - Structured Regulation and Collaborative R&D Ecosystem

Europe is expected to lead in 2026, accounting for approximately 49.5% of the market share, driven by its structured regulatory framework, strong public research base, and mature food-manufacturing ecosystem. The region continues to strengthen its position in precision fermentation through structured public research funding, a mature food-manufacturing base, and coordinated regulatory oversight.

The EU Novel Foods framework, although more conservative than the U.S. system, provides unified market access once authorization is achieved, making it strategically attractive for companies targeting continent-wide distribution.

Research clusters in Germany, the U.K., France, Denmark, and Spain are driving advancements in dairy-identical proteins, specialty enzymes, and flavor-modulating compounds, supported by high-quality universities and national innovation programs. European stakeholders emphasize labeling transparency, traceability, and consumer communication, shaping how precision-fermented ingredients are positioned within the broader food ecosystem.

Recent developments include new pilot-scale fermentation hubs opened in the Netherlands and Denmark, designed to support collaborative R&D between startups and established food processors. Multiple European retailers began limited-scope trials of fermentation-derived cheese ingredients and functional flavor enhancers in private-label products.

Several regional food manufacturers also announced procurement partnerships for fermentation-derived enzymes aimed at improving bakery performance and reducing formulation costs. Ongoing regulatory-harmonization discussions within the EU signal a commitment to streamlining application reviews while maintaining high safety standards. These actions reinforce Europe’s role as both a demand center and a regulatory trend-setter in precision fermentation.

Asia Pacific Precision Fermentation Market Trends - Rapid Capacity Expansion and Emerging Market Adoption

Asia Pacific is projected to be the fastest-growing region for both precision-fermentation manufacturing and long-term consumption. China and India are scaling fermentation capacity through national biotechnology missions, industrial-park incentives, and private investments targeted at high-volume production of proteins, enzymes, and specialty metabolites. Competitive operating costs, established engineering capabilities, and proximity to equipment suppliers provide structural advantages for scaling commercial fermentation.

Japan contributes specialized strengths in enzyme fermentation, amino-acid engineering, and flavor-compound development, while South Korea and Singapore continue to expand pilot-scale capabilities in functional proteins and bioactive ingredients. ASEAN markets, particularly Thailand and Indonesia, are beginning to trial fermentation-derived components in plant-based product lines and fortified functional beverages.

Recent developments include the commissioning of large-scale fermentation systems in Eastern China dedicated to food-grade protein isolates, and a newly announced collaboration between an Indian biotech manufacturer and regional food producers to integrate fermentation-derived lipids into dairy-alternative formulations.

Japan expanded its regulatory guidance for certain enzyme categories, offering clearer pathways for manufacturers. Several Southeast Asian food companies initiated pilot projects evaluating fermentation-derived flavor compounds in sauces and snacks. These initiatives underline Asia Pacific’s growing manufacturing importance and its increasing potential as a demand center for precision-fermented ingredients.

Competitive Landscape

The global precision fermentation market is moderately concentrated, comprising specialized start-ups developing specific proteins or enzymes, platform engineering firms offering strain design and process optimization, and established ingredient suppliers entering via partnerships and investments.

Europe holds significant market value due to its structured regulations, strong research institutions, and mature food-manufacturing ecosystem. Competitive advantage depends on proprietary strain technology, high-yield processes, regulatory progress, and scalable manufacturing.

Leading companies differentiate through unique strains, efficient fermentation, and early regulatory engagement, while partnerships with consumer-goods firms and asset-light, contract-based models support rapid market entry and flexible production.

Key Industry Developments

- In January 2025, New Culture announced the rollout of its animal-free mozzarella to additional U.S. foodservice partners following successful 2024 pilots, marking a broader market introduction of precision-fermented casein-based cheese.

- In March 2025, Vivici introduced expanded commercial availability of its precision-fermented beta-lactoglobulin ingredient for ready-to-drink nutrition beverages, following regulatory progress and customer-scale trials initiated the previous year.

Companies Covered in Precision Fermentation Market

- Perfect Day

- The EVERY Company

- Geltor

- Clara Foods

- Change Foods

- Motif FoodWorks

- Imagindairy

- New Culture

- Remilk

- Formo

- Those Vegan Cowboys

- Superbrewed Food

- Helaina

- Planetary

- Cauldron

- Eden Brew

- All G Foods

- Onego Bio

- BioBrew

- Fermbox Bio

Frequently Asked Questions

The precision fermentation market size in 2026 is US$6.5 Billion.

By 2033, the precision fermentation market is projected to reach US$77.6 Billion.

Major trends include rapid scale-up of dairy-identical proteins, rising food and beverage reformulation using high-purity enzymes and lipids, stronger regulatory clarity in the U.S. and Europe, and increased partnerships between biotechnology firms and global CPG companies.

The food and beverages segment leads the market, accounting for over 50% of total application demand due to strong adoption of dairy proteins, enzymes, and functional ingredients.

The precision fermentation market is expected to grow at a CAGR of 42.5% from 2026 to 2033.

Key players include Perfect Day, The EVERY Company, Geltor, Imagindairy, and Remilk.