- Medical Devices

- Europe Precision Diagnostics Market

Europe Precision Diagnostics Market Size, Share, and Growth Forecast, 2026 – 2033

Europe Precision Diagnostics Market by Diagnostics Type (Genetic Tests, Direct to Consumer Tests, Esoteric Tests), Application (Oncology, Infectious Diseases, Others), End-user (Hospitals, Clinical Laboratories, Others), and Country Analysis 2026 – 2033

Europe Precision Diagnostics Market Size and Trends Analysis

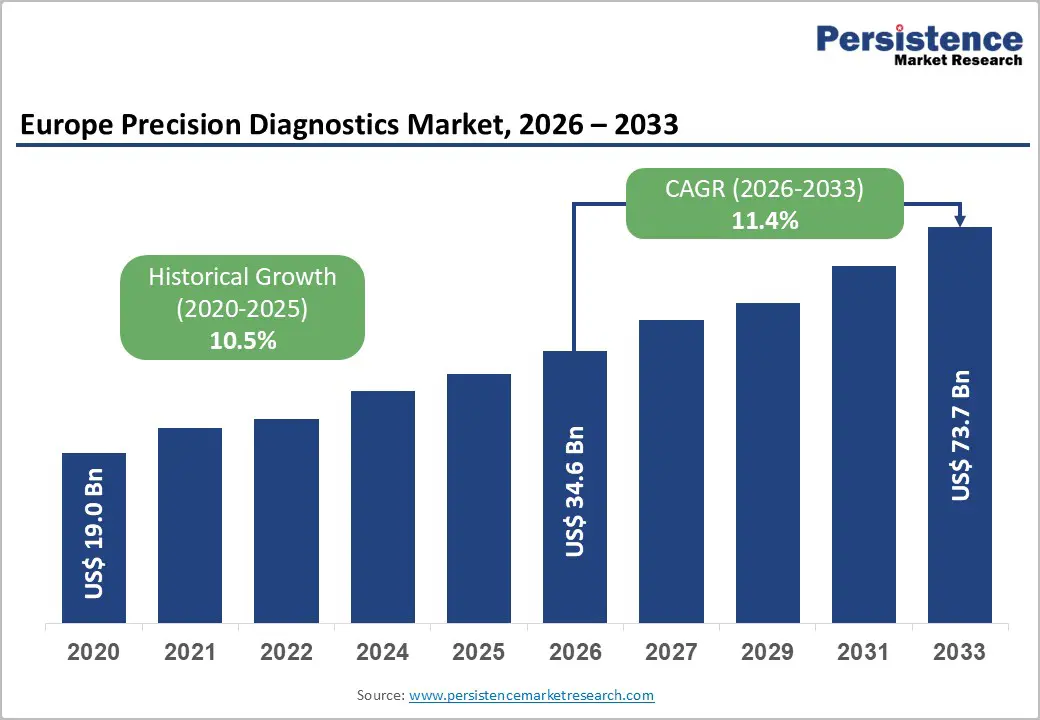

The Europe precision diagnostics market size is likely to be valued at US$34.6 billion in 2026 and is expected to reach US$73.7 billion by 2033, growing at a CAGR of 11.4% during the forecast period from 2026 to 2033, driven by the aggressive integration of multi-omics data into clinical workflows and a systemic shift toward personalized therapeutic interventions, driven by post-pandemic infrastructure upgrades and the rising prevalence of chronic conditions requiring targeted diagnostics.

Primary expansion factors include the harmonization of European regulatory frameworks (IVDR), the rapid maturation of Next-Generation Sequencing (NGS) technologies, and an escalating demand for early-stage oncology detection. Rising chronic disease prevalence drives demand for targeted testing, supported by genomic advancements like NGS. Government investments in precision medicine infrastructure further accelerate adoption across oncology and genetic applications.

Key Industry Highlights:

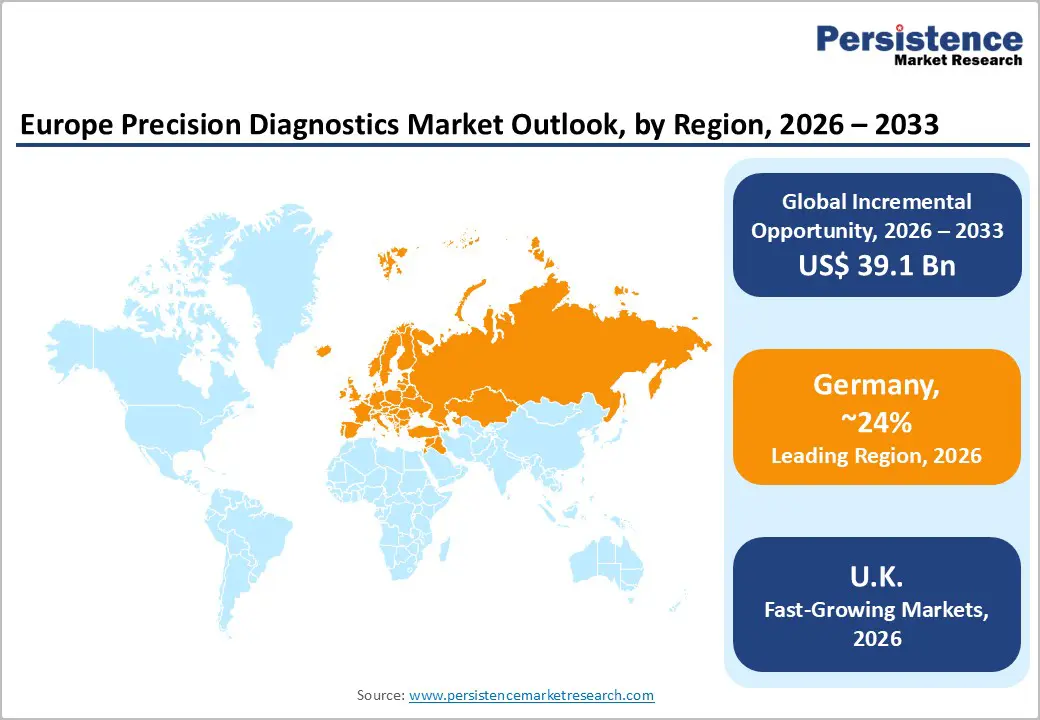

- Leading Country: Germany is projected to lead due to deep institutional adoption, robust healthcare infrastructure, and high-tech biotech integration, accounting for approximately 24% share in 2026, supported by advanced NGS platforms, liquid biopsy adoption, and AI-enabled diagnostic workflows.

- Fastest-Growing Country: The U.K. is anticipated to grow fastest due to expansive national genomics initiatives, post-Brexit regulatory agility, and AI-driven clinical diagnostics adoption across oncology, rare diseases, and population-scale screening.

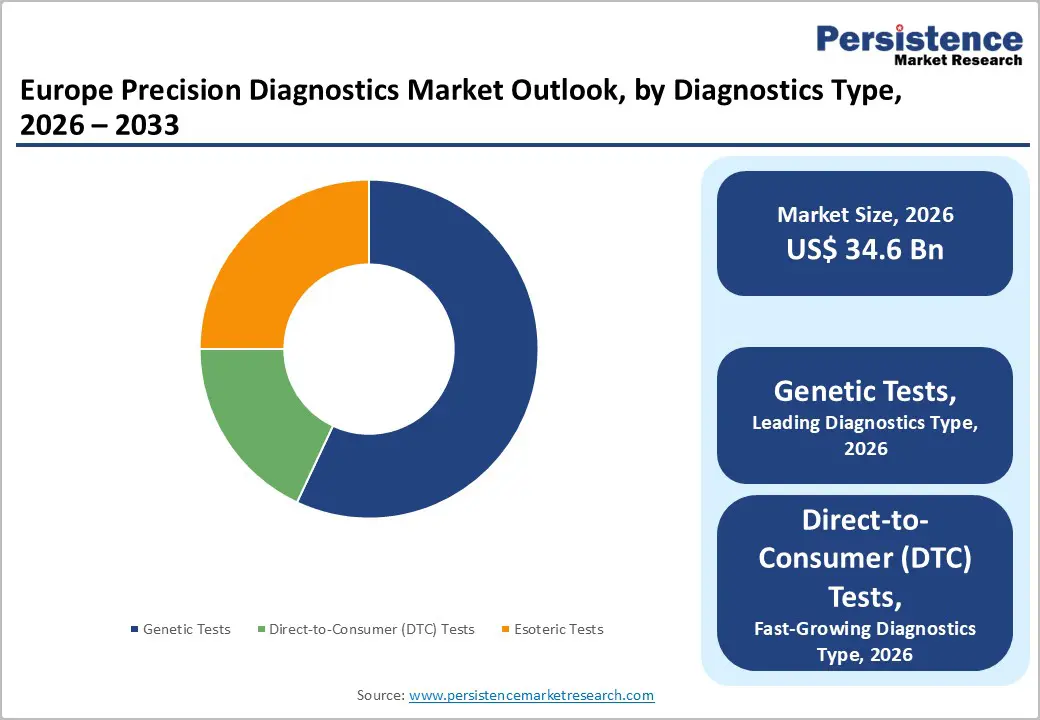

- Leading Diagnostics Type: Genetic tests are expected to lead, accounting for approximately 57% share in 2026 through high-throughput clinical adoption, integration into oncology and rare-disease workflows, precision, and multi-omics platform evolution.

- Leading Application: Oncology is projected to dominate for high precision, multi-omics integration, and adoption across hospitals and laboratories, holding approximately 44% share in 2026.

| Key Insights | Details |

|---|---|

|

Europe Precision Diagnostics Market Size (2026E) |

US$34.6 Bn |

|

Market Value Forecast (2033F) |

US$73.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Advancements in Genomic Sequencing and Bioinformatics Integration

The evolution of next-generation sequencing platforms has structurally transformed precision diagnostics across European healthcare systems. Reduced costs per genome have enabled broader adoption within routine clinical workflows, particularly for rare genetic disorders and complex oncology profiling. Integration of artificial intelligence and machine learning facilitates rapid processing of large genomic datasets, converting raw sequences into actionable clinical insights.

Advanced bioinformatics pipelines allow clinicians to stratify patient populations efficiently, reducing ineffective therapeutic interventions. European regulatory frameworks increasingly recognize AI-assisted genomic interpretation, accelerating clinical acceptance. The improved throughput and analytical depth of genomic platforms are reshaping clinical trial design and therapeutic decision-making.

The combination of sequencing evolution and computational integration creates a self-reinforcing cycle of innovation and adoption. Hospitals and clinical laboratories optimize workflows through automated data interpretation, enhancing turnaround times and laboratory efficiency. The technological synergy aligns with value-based care objectives, emphasizing measurable clinical outcomes over procedural volume. Bioinformatics tools reduce dependency on specialist interpretation, mitigating human error and supporting broader clinical deployment. Cross-border collaborations leverage shared genomic databases, enhancing European-wide research capabilities.

Supportive Government Initiatives and Healthcare Digitalization

Strategic European policy frameworks are significantly strengthening the precision diagnostics landscape across member states. Initiatives such as "1+ Million Genomes" promote cross-border collaboration and secure data sharing, enabling robust clinical research and validation of novel diagnostic markers.

The establishment of interoperable infrastructures facilitates access to genomic and clinical datasets, supporting advanced analytics and algorithm refinement. Implementation of the European Health Data Space enhances the secondary use of health data, allowing diagnostic providers to optimize assay development and testing accuracy. These digital health investments reinforce trust among healthcare stakeholders, underpinning regulatory compliance and data security. By fostering localized diagnostic hubs, governments structurally expand market readiness and support scalable adoption of advanced testing technologies.

The convergence of policy and digital infrastructure is creating a favorable ecosystem for innovation in diagnostics. High-quality data repositories empower laboratories and research institutions to improve algorithmic performance and clinical validity. Enhanced digital interoperability reduces delays in diagnostic workflows while supporting real-time analytics across healthcare networks. Regulatory alignment ensures ethical and secure data utilization, mitigating legal and operational risks for market participants.

Private-sector investment is incentivized through clear policy signaling and infrastructure support, fostering technology diffusion. These initiatives collectively strengthen clinical precision, enable efficient diagnostic delivery, and structurally enhance market growth prospects within Europe’s evolving healthcare environment.

Barrier Analysis – High Implementation Costs

The deployment of advanced genomic and precision diagnostic tools is constrained by substantial capital expenditure requirements. Next-generation sequencing platforms and associated reagents demand significant upfront investment, restricting access primarily to well-funded hospitals and specialized laboratories. High implementation costs also extend to maintenance, software licensing, and staff training, adding complexity to operational budgets.

Compliance with European regulatory frameworks, including IVDR mandates, introduces additional expenditure burdens that further inhibit smaller providers from adopting cutting-edge technologies. These financial constraints slow the diffusion of innovative diagnostic solutions and limit equitable access across diverse healthcare infrastructures.

Capital intensity and regulatory cost pressures collectively shape the strategic landscape for market expansion. Institutions must allocate resources to both technological acquisition and long-term operational sustainability, which can defer investments in emerging diagnostics. The combination of high equipment costs, consumable pricing, and specialized personnel requirements reinforces market concentration in major hospitals. Smaller facilities encounter barriers to establishing fully compliant workflows, creating structural gaps in nationwide diagnostic coverage. These cost-driven dynamics impede the uniform rollout of genomic testing, delaying clinical integration.

Stringent Regulatory Hurdles and IVDR Compliance

The European transition to In Vitro Diagnostic Regulation (IVDR 2017/746) imposes substantial structural challenges across the diagnostics sector. Rigorous requirements for clinical evidence, technical documentation, and conformity assessments create bottlenecks in product certification. Smaller enterprises encounter disproportionate compliance costs, which absorb significant portions of research and development budgets. These financial and procedural burdens constrain the development of high-innovation, niche diagnostic tools.

Laboratories and manufacturers must invest in quality management systems and extensive validation protocols to meet regulatory expectations. Collectively, these requirements slow adoption cycles and reduce the pace at which cutting-edge technologies reach clinical settings.

Compliance demands reshape resource allocation and operational planning across the industry. Organizations must navigate intricate documentation, audit, and reporting obligations while maintaining core development pipelines. Extended certification timelines introduce uncertainty in strategic planning and can defer commercialization decisions. Smaller diagnostic firms face elevated risk of delayed returns on innovation, impacting competitive positioning. Large hospitals and reference laboratories bear lower proportional burdens, but still encounter integration delays and procedural overhead. These dynamics structurally moderate market growth, particularly in segments reliant on novel genomic and esoteric testing solutions.

Opportunity Analysis – Expansion of Direct-to-Consumer Genetic Testing

The Direct-to-Consumer (DTC) genetic testing segment is structurally positioned for accelerated adoption across Europe. Rising consumer health consciousness and proactive wellness management are driving demand for tests focused on ancestry, nutrition, and predisposition to lifestyle-related conditions. Integration with digital health platforms enables hybrid models, allowing consumers to transition from home-based sample collection to professional clinical consultation.

The convergence of telemedicine and DTC diagnostics also facilitates longitudinal health monitoring and early risk detection. Enhanced consumer education and awareness campaigns further reinforce adoption, supporting structural expansion of DTC offerings in Western Europe.

Market expansion in DTC genetics is reinforced by technology-enabled platforms and consumer empowerment trends. Data-driven insights from large-scale DTC testing enable refinement of algorithms, improving diagnostic accuracy and clinical relevance. Strategic partnerships with healthcare providers can create integrated pathways linking consumer testing to professional interpretation. This integration strengthens trust, mitigates regulatory risk, and encourages repeat engagement.

Overall, DTC genetic testing represents a structurally underpenetrated segment, offering significant incremental market potential. Its growth aligns with broader digital health adoption, precision medicine frameworks, and population-level wellness initiatives, supporting long-term structural expansion of the European diagnostics market.

AI and Big Data Integration

The integration of artificial intelligence and big data analytics is structurally transforming precision diagnostics across Europe. AI-driven analytics facilitate rapid interpretation of multi-dimensional datasets, enhancing the accuracy of infectious disease diagnostics and reducing diagnostic uncertainty. Collaborative initiatives between diagnostics and pharmaceutical companies accelerate algorithm development and validation, embedding advanced computational tools into clinical workflows.

The structural combination of AI and big data strengthens the precision and scalability of diagnostic services, enabling more efficient healthcare delivery while supporting regulatory compliance and clinical evidence generation.

The deployment of AI platforms reshapes diagnostic processes at the market level. Integration of pathology and genomics data improves the sensitivity and specificity of disease detection, reducing reliance on conventional labor-intensive methods.

Large-scale predictive models enable the identification of population-level trends, informing clinical decision-making and public health strategies. Cloud-based analytics and machine learning pipelines optimize laboratory throughput while minimizing human error. These technological advancements facilitate dynamic monitoring of emerging infectious diseases and rare conditions. Collaborative partnerships drive the standardization of AI algorithms and enhance market adoption, creating structural efficiencies.

Category–wise Analysis

Diagnostics Type Insights

Genetic tests are expected to lead, accounting for approximately 57% share in 2026, underpinned by their entrenched role in clinical workflows for oncology, rare diseases, and prenatal screening across the U.K., Germany, and France. Adoption remains anchored by high diagnostic reliability, throughput efficiency, and integration readiness, with providers prioritizing workflow standardization and scale economics in high-volume hospital and laboratory environments.

Ongoing platform evolution, including AI-enabled variant interpretation, multi-omics integration, and ultra-rapid sequencing, continues to reinforce replacement cycles and utilization intensity. Roche, Illumina, and Eurofins Genomics, with their comprehensive genomic and diagnostic ecosystems, further consolidate clinical adoption and embed enterprise-level workflows. This combination of mature infrastructure, technological leadership, and predictable demand sustains the segment’s dominance within structured European deployment models.

Direct-to-consumer tests are expected to be the fastest-growing segment, driven by emerging consumer demand for proactive health insights and lifestyle-focused genetic screening. Growth is being catalyzed by reduced sequencing costs, digital health platforms, and hybrid models that integrate home sampling with professional consultation, which materially improve accessibility, personalization, and user engagement. Accelerating adoption is supported by AI-driven interpretation, e-commerce distribution, and multi-lingual localization, lowering operational friction for first-time consumers.

23andMe, MyHeritage, and Dante Labs are expanding health-risk reporting platforms to capture early-cycle demand and embed brand familiarity. As digital literacy, platform trust, and institutional support improve, the segment is expected to outpace overall market growth, establishing a structurally underpenetrated pathway for consumer-driven precision diagnostics.

Application Insights

Oncology is expected to lead, accounting for approximately 44% share in 2026, underpinned by its entrenched role in biomarker-driven patient stratification and therapy selection across hospitals and clinical laboratories in the UK, Germany, and France. Adoption remains anchored by high diagnostic precision, integration into clinical trials, and capacity for high-throughput genomic and PCR workflows, with providers prioritizing operational standardization and multi-omics profiling in complex oncology care pathways.

Ongoing platform evolution, including AI-enabled variant interpretation, liquid biopsy monitoring, and single-cell multi-omics, continues to reinforce utilization intensity and replacement cycles. Roche, Illumina, and Thermo Fisher Scientific, with their integrated sequencing, automation, and assay platforms, consolidate enterprise adoption and workflow embedding. This combination of technological sophistication, clinical reliability, and scalable infrastructure sustains the segment’s dominance within European oncology diagnostics.

Infectious diseases are expected to be the fastest-growing, driven by the urgent need for rapid pathogen identification and antimicrobial resistance management across hospitals, GP clinics, and decentralized testing sites. Growth is being catalyzed by NGS-based pathogen genomics, multiplexed respiratory panels, and point-of-care molecular platforms, which materially improve detection speed, accuracy, and outbreak responsiveness.

Accelerating adoption is supported by AI-enabled early warning systems, decentralized laboratory networks, and hybrid at-home testing models, lowering operational friction for healthcare providers and consumers. bioMérieux, Danaher, and QIAGEN are expanding clinical and POC platforms to capture early-cycle demand and embed brand familiarity. As cross-border data integration and post-pandemic molecular infrastructure mature, this segment is expected to outpace overall market growth, structurally transforming infectious disease diagnostics in Europe.

Country Insights

Germany Precision Diagnostics Market Trends

Germany is expected to remain the leading regional market for precision diagnostics, approximating 24% share in 2026, supported by deep institutional adoption, robust healthcare infrastructure, and high-tech biotech integration. Core demand is projected to be anchored in oncology and rare-disease testing, with advanced NGS and liquid biopsy platforms driving clinical trial stratification and routine diagnostics. Industrial ecosystems are anticipated to reinforce leadership through concentrated vendor presence, AI-enabled diagnostic workflows, and integrated bioinformatics networks.

Regulatory frameworks such as IVDR and the Digital Healthcare Act (DVG) are likely to streamline compliance while maintaining high quality and safety standards, fostering premium solution deployment across hospitals and specialized labs. Germany, France, and the Nordics are expected to sustain structural dominance through coordinated reimbursement policies and public-private collaborations supporting innovative diagnostics. Diagnostic-therapeutic bundling and AI integration are projected to optimize lab operations and patient stratification, while point-of-care adoption across pharmacies and GP clinics is likely to expand service coverage.

The U.K. is expected to register the fastest growth trajectory, driven by expansive national genomics initiatives and AI-enabled clinical diagnostics integration. Core growth is anticipated across oncology, rare diseases, and population-scale screening, supported by public health system modernization and large-scale sequencing networks. Industrial scaling is projected to accelerate through genomics hubs, direct-to-consumer testing localization, and advanced digital health integration. Policy agility under MHRA post-Brexit is expected to facilitate faster pilot adoption, cross-sector collaborations, and regulatory alignment for innovative diagnostic platforms.

The UK ecosystem is projected to strengthen through AI-driven biomarker discovery, pharmacogenomics deployment, and integrated clinical data infrastructures, reinforcing catch-up growth relative to Germany and other leading European markets. Genomics England is projected to serve as the primary anchor for the UK’s market acceleration, driving national adoption through large-scale sequencing, newborn genome programs, and cancer vaccine precision matching initiatives. Public-private partnerships, data liquidity via the U.K. Biobank, and localized DTC infrastructure are likely to enhance market efficiency and innovation, positioning the U.K. as the structural growth engine for Europe’s precision diagnostics ecosystem.

Competitive Landscape

The Europe precision diagnostics market is moderately consolidated, with leadership concentrated among global suppliers such as Roche, Thermo Fisher Scientific, Illumina, Siemens Healthineers, and Abbott. These players exert influence through extensive patent portfolios, integrated NGS platforms, and wide-reaching distribution networks, establishing functional and technological benchmarks across clinical laboratories and hospital systems. Competitive positioning is defined by horizontal and vertical differentiation, where incumbents integrate end-to-end sequencing, bioinformatics, and companion diagnostic solutions, while specialized European startups focus on AI-driven analytics and niche liquid biopsy applications. The industry behavior reflects ongoing platform evolution and consolidation, with M&A activity facilitating technology aggregation and service-led business models emerging to support clinical workflow integration. This dynamic balance between large-scale dominance and agile niche innovation is expected to sustain a moderately consolidated yet technologically progressive market structure across Europe.

Key Industry Developments:

- In January 2026, Agilent Technologies launched the Agilent S540MD Slide Scanner System in Europe. It enhances digital pathology capabilities, offering improved throughput and imaging accuracy

- In September 2024: Sanofi partnered with RadioMedix to develop next-generation radioligand medicines like AlphaMedix, which use precise lead-212 targeting for rare neuroendocrine tumors.

Companies Covered in Europe Precision Diagnostics Market

- Roche Diagnostics

- Siemens Healthineers

- Thermo Fisher Scientific

- Illumina

- QIAGEN N.V.

- Agilent Technologies

- Bio-Rad Laboratories

- Myriad Genetics

- Oxford Nanopore Technologies

- Eurofins Scientific

- Sysmex Corporation

- Koninklijke Philips N.V.

- SGS SA

- SOPHiA GENETICS

- Danaher Corporation

- BioMérieux

Frequently Asked Questions

The Europe precision diagnostics market is projected to be valued at US$34.6 billion in 2026 and is expected to reach US$73.7 billion by 2033, driven by multi-omics integration, NGS adoption, and rising demand for early-stage oncology detection.

Advancements in next-generation sequencing and AI-enabled bioinformatics enable rapid interpretation of complex genomic data, improving diagnostic accuracy, workflow efficiency, and clinical decision-making, particularly for oncology and rare disease applications across hospitals and laboratories.

The Europe precision diagnostics market is forecast to grow at a CAGR of 11.4% from 2026 to 2033, reflecting the combined effects of regulatory harmonization, digital infrastructure upgrades, and expansion of direct-to-consumer genetic testing.

The U.K. is the fastest-growing market, driven by national genomics initiatives, AI-enabled clinical diagnostics, direct-to-consumer testing adoption, and post-Brexit regulatory agility that accelerates pilot programs and technology deployment.

The Europe precision diagnostics market is moderately consolidated, with leading players including Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, Illumina, QIAGEN N.V., Agilent Technologies, Bio-Rad Laboratories, Myriad Genetics, Oxford Nanopore Technologies, Eurofins Scientific, Sysmex Corporation, Koninklijke Philips N.V., SGS SA, SOPHiA GENETICS, Danaher Corporation, and BioMérieux.