- Technology

- Data Center Precision Cooling Market

Data Center Precision Cooling Market Size, Share, and Growth Forecast, 2025 - 2032

Data Center Precision Cooling Market by Technology (Air-Based Cooling, Liquid-Based Cooling), Component (Hardware, Services, Software), Data Center (Small and Medium Data Centers, Large Data Centers, Colocation Data Centers), End-use, and Regional Analysis for 2025 - 2032

Data Center Precision Cooling Market Size and Trends Analysis

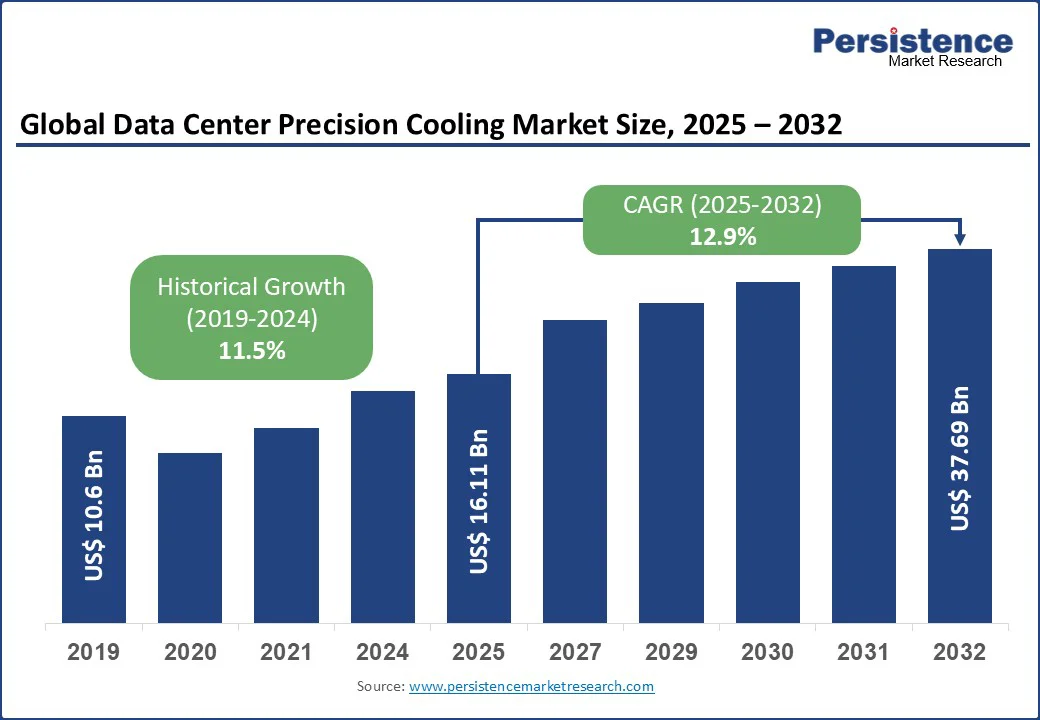

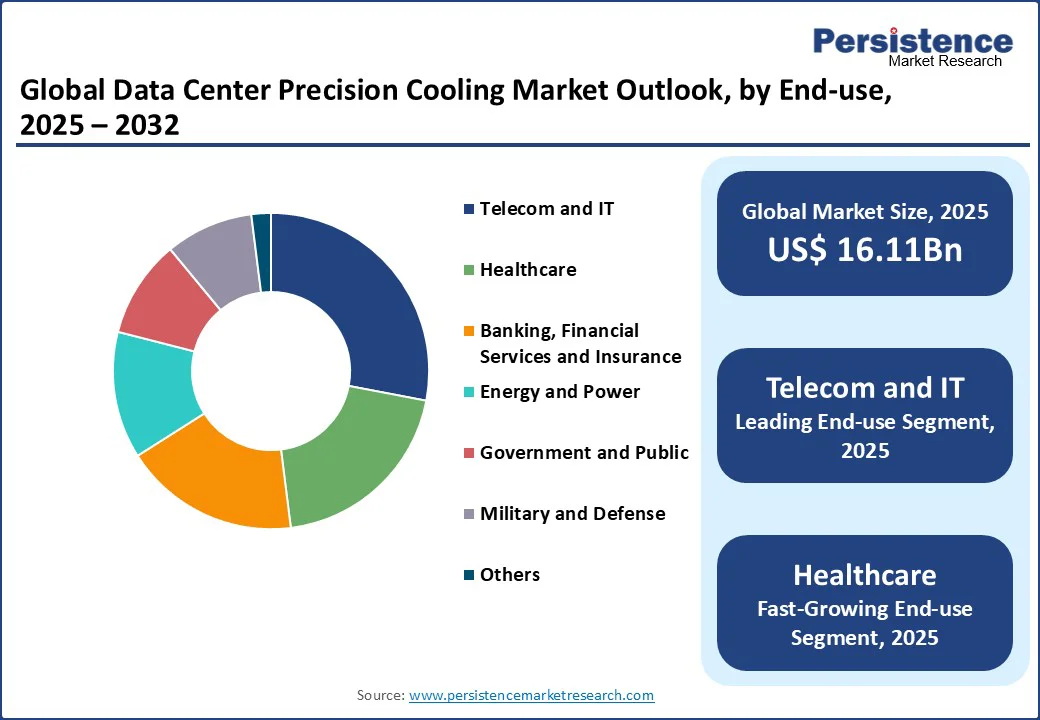

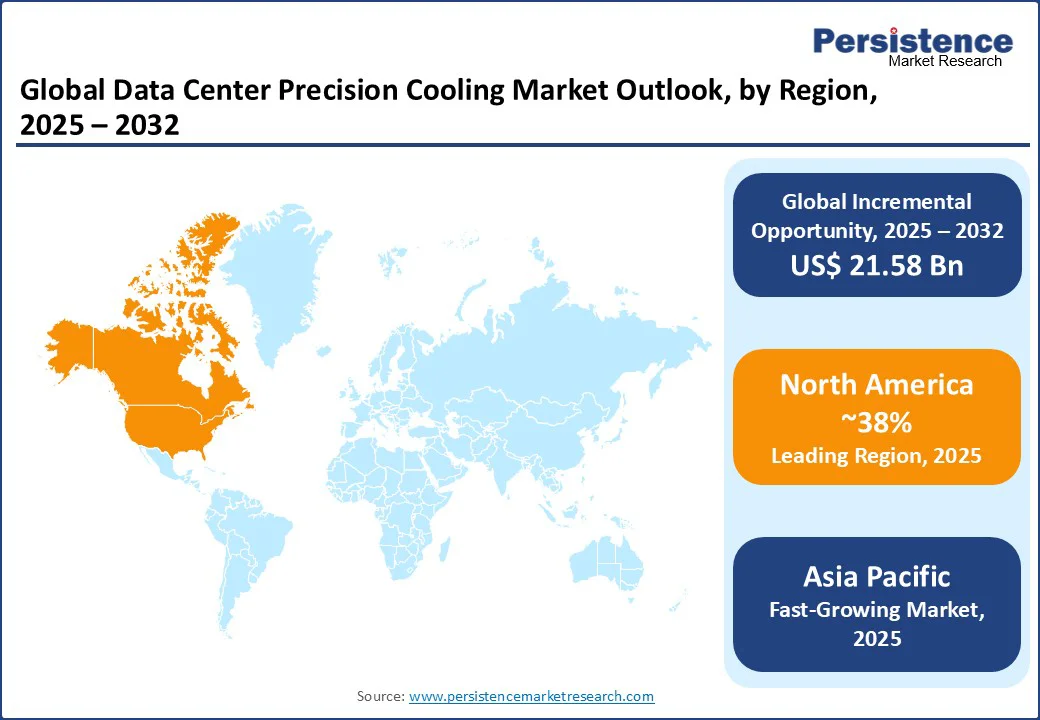

The global data center precision cooling market size is likely to value at US$16.11 Bn in 2025 and reach US$37.69 Bn by 2032, growing at a CAGR of 12.9% during the forecast period from 2025 to 2032.

The data center precision cooling market is witnessing robust growth, driven by the escalating demand for high-performance computing, the rise of artificial intelligence (AI), and the expansion of cloud and edge computing infrastructure.

Precision cooling solutions, critical for maintaining optimal temperature and humidity in data centers, are increasingly adopted to ensure equipment reliability and energy efficiency. The surge in data generation, coupled with the need for sustainable and cost-effective cooling technologies, fuels market expansion. Innovations such as liquid-based cooling and AI-driven thermal management, along with a strong infrastructure development in developed and emerging markets, further propel the market forward.

Key Industry Highlights:

- Leading Region: North America accounts for nearly 38% of the global Data Center Precision Cooling market in 2025, driven by its advanced digital infrastructure and high adoption of innovative cooling technologies.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, propelled by rapid digitalization and data center expansion in countries such as China and India.

- Investment Plans: In January 2025, Amazon Web Services (AWS) announced a USD 11 billion investment in data centers in Georgia, focusing on AI and cloud computing with advanced liquid cooling solutions.

- Dominant Technology: Air-based cooling, accounting for nearly 45% of the market share, due to its widespread adoption in traditional data centers.

- Leading Distribution Channel: Hardware, contributing over 50% of market revenue, driven by the demand for advanced cooling equipment such as CRAC and CRAH units.

|

Global Market Attribute |

Key Insights |

|

Data Center Precision Market Size (2025E) |

US$ 16.11Bn |

|

Market Value Forecast (2032F) |

US$ 37.69Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

11.5% |

Market Dynamics

Driver - Rising demand for High-performance Computing and AI-driven Workloads Fuels Market Growth

The surge in demand for high-performance computing (HPC) and AI-driven workloads, the proliferation of AI, machine learning, and big data analytics, has led to increased data center density, generating significant heat that requires advanced cooling solutions. According to the U.S. Department of Energy, data centers consumed 4.4% of total U.S. electricity in 2023, with cooling accounting for 38-40% of this consumption. Liquid cooling systems, such as direct-to-chip and immersion cooling, are gaining traction due to their ability to manage high-density server configurations efficiently. For instance, Vertiv launched the MegaMod CoolChip in September 2024, a liquid-cooled prefabricated unit designed for AI data centers, showcasing the industry’s shift toward energy-efficient solutions.

Government initiatives, such as the European Union’s Green Deal, promoting sustainable data centers, further boost adoption. In the U.S., investments by hyperscalers such as AWS and Microsoft, including Microsoft’s USD 80 billion commitment to AI-enabled data centers in January 2025, underscore the need for precision cooling to support next-generation computing, ensuring sustained market growth through 2032.

Restraint - High Initial Investment and Complexity of Liquid Cooling Systems Limit Adoption

High initial investment and complexity of deploying liquid cooling systems pose significant challenges to the data center precision cooling market, particularly for small and medium-sized enterprises (SMEs). Liquid cooling solutions, such as immersion and direct-to-chip systems, require specialized infrastructure, including coolant distribution units and leak-proof components, which increase upfront costs. Liquid cooling systems can cost more to install than traditional air-based systems.

Additionally, the lack of standardized protocols for liquid cooling in emerging markets such as Africa and parts of Latin America complicates adoption. Concerns about maintenance complexity and potential risks, such as coolant leaks, further deter smaller operators. These challenges, coupled with limited technical expertise in some regions, restrict market penetration, particularly in cost-sensitive markets.

Opportunity - Growing Adoption of Sustainable and Energy-efficient Cooling Solutions

The increasing focus on sustainability and energy efficiency presents significant opportunities for the data center precision cooling market. With global emphasis on reducing carbon footprints, data center operators are adopting eco-friendly cooling technologies such as free cooling and liquid-based systems to lower power usage effectiveness (PUE). Government regulations, such as the EU’s push for carbon neutrality by 2050, encourage the adoption of green cooling solutions.

Companies such as Schneider Electric and Vertiv are innovating with waterless and hybrid cooling systems to meet these demands. The rise of edge computing and the expansion of hyperscale data centers further amplify the need for scalable, energy-efficient cooling, creating lucrative opportunities for market players through 2032.

Category-wise Analysis

Technology Insights

- Air-based cooling holds the largest market share, approximately 45% in 2025 of the data precision cooling market, due to its widespread use in traditional data centers. Technologies such as computer room air conditioning (CRAC) and air handler (CRAH) units are favored for their reliability and ease of implementation, particularly in small and medium-sized data centers across North America and Europe. Companies such as Daikin Industries and STULZ GmbH lead with advanced air-cooling solutions tailored for cost-effective thermal management.

- Liquid-based cooling is experiencing rapid growth, driven by its superior efficiency in handling high-density server environments. Direct-to-chip and immersion cooling solutions are increasingly adopted in hyperscale and AI-driven data centers, with companies such as LiquidStack and Green Revolution Cooling (GRC) innovating to meet the rising demand for sustainable cooling in regions such as Asia Pacific and North America.

Component Insights

- Hardware dominates, accounting for over 50% of market revenue in 2025, driven by the demand for advanced cooling equipment such as CRAC units, chillers, and liquid cooling systems. Major players such as Vertiv Group Corp. and Schneider Electric offer robust hardware solutions, widely adopted in large data centers and colocation facilities for their reliability and scalability.

- Services are the fastest-growing segment, fueled by the increasing need for maintenance, installation, and consulting services for complex cooling systems. As data centers adopt liquid cooling, companies such as Johnson Controls and Asetek provide specialized services to ensure optimal performance, particularly in high-performance computing environments in North America and Asia Pacific.

Data Center Insights

- Large data centers hold the largest share, approximately 42% in 2025, due to their extensive server setups and high cooling requirements. Hyperscale facilities, operated by companies such as AWS and Google, rely on precision cooling to manage high-density workloads, driving demand for both air and liquid cooling solutions in regions such as North America.

- Colocation data centers are experiencing rapid growth, driven by the rising demand for scalable and cost-effective infrastructure. These facilities cater to enterprises seeking flexible solutions, with providers such as LiquidStack and Rittal offering tailored cooling systems to support diverse workloads, particularly in Asia Pacific and Europe.

End-use Insights

- Telecom and IT dominate, contributing over 28% of market revenue in 2025, due to the rapid expansion of 5G, cloud computing, and AI applications. Companies such as Schneider Electric and Mitsubishi Electric provide precision cooling solutions to ensure reliable operations in telecom and IT data centers, especially in North America and Europe.

- Healthcare is the fastest-growing segment, driven by the increasing adoption of digital health records and AI-driven diagnostics. Data centers supporting healthcare applications require precise cooling to ensure uptime, with companies such as Vertiv and Daikin Industries offering specialized solutions in regions such as the Asia Pacific and North America.

Regional Insights

North America Data Center Precision Cooling Market Trends

In 2025, North America continues to dominate the global data center precision cooling market, commanding approximately 38% of total market share. This leadership is largely attributed to the region’s highly advanced digital infrastructure and rapid adoption of next-generation cooling technologies, especially to support AI-driven workloads. The United States is at the forefront, fueled by massive capital investments from hyperscale cloud providers such as AWS, Microsoft, and Google. A standout example is AWS’s USD 11 billion data center expansion in Georgia, announced in January 2025, which underscores the scale and strategic focus of these deployments.

Stringent energy efficiency regulations and robust government incentives for sustainable infrastructure further drive the shift toward more efficient and environmentally conscious cooling systems. Technologies such as liquid cooling and hybrid precision systems are gaining momentum, particularly as AI and HPC workloads demand denser compute environments. Additionally, the U.S. Department of Energy’s push for high-efficiency cooling adds further regulatory support.

Asia Pacific Data Center Precision Cooling Market Trends

The Asia Pacific region is emerging as the fastest-growing data center precision cooling market in 2025, driven by aggressive digitalization, cloud adoption, and data center expansion across major economies such as China, India, and Japan. In China, the government’s Made in China 2025 initiative is a key driver, incentivizing the development of high-performance computing and AI-focused data centers. This has significantly increased the demand for liquid cooling and other high-efficiency thermal management solutions to support dense workloads.

Japan is focusing heavily on AI, IoT, and robotics, which is creating demand for next-generation cooling technologies. Established companies such as Mitsubishi Electric and Daikin Industries are leveraging their expertise in HVAC and energy-efficient technologies to develop tailored solutions for modern data centers, positioning themselves as key players in the region’s precision cooling ecosystem.

Europe Data Center Precision Cooling Market Trends

Europe is projected to be the second fastest-growing region in the Data Center Precision Cooling market from 2025 to 2032, fueled by stringent environmental regulations, a strong push for energy efficiency, and the EU’s broader commitment to carbon neutrality under the European Green Deal. These regulatory frameworks are compelling data center operators to adopt sustainable and low-emission cooling technologies, accelerating the shift toward liquid cooling, free cooling, and hybrid precision systems.

The U.K. and Germany are at the forefront of this transformation. In the U.K., rapid growth in fintech, e-commerce, and edge computing is creating demand for compact, high-performance cooling systems capable of supporting decentralized infrastructure in urban environments. Meanwhile, Germany's robust IT and industrial base, combined with its reputation for engineering excellence, is driving the adoption of advanced liquid cooling solutions in both hyperscale and colocation data centers.

Competitive Landscape

The global data center precision cooling market is highly competitive, with key players such as Vertiv Group Corp., Schneider Electric S.E., STULZ GmbH, Daikin Industries Ltd., and Mitsubishi Electric Corporation dominating through extensive product portfolios and global distribution networks. Regional players such as Green Revolution Cooling (GRC) and LiquidStack focus on niche liquid cooling solutions. Companies are investing in sustainable technologies and partnerships to enhance market share, driven by the demand for energy-efficient cooling.

Key Industry Developments

- February 2025: Carrier Global Corporation announced that its venture arm, Carrier Ventures, is leading both an investment and a technology partnership with ZutaCore, a company specializing in two?phase, direct?to?chip liquid cooling solutions for data centers.

- November 2024: CoolIT Systems announced the launch of the CHx1000, the world’s highest-density liquid-to-liquid coolant distribution unit (CDU). This unit is specifically engineered to support the cooling demands of high-performance AI workloads, including the NVIDIA Blackwell platform.

Companies Covered in Data Center Precision Cooling Market

- Vertiv Group Corp.

- Schneider Electric S.E.

- STULZ GmbH

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- Johnson Controls International plc

- Asetek, Inc.

- Rittal GmbH & Co. KG

- Green Revolution Cooling (GRC)

- LiquidStack

- Others

Frequently Asked Questions

The data center precision cooling market is projected to reach US$16.11 Bn in 2025.

Rising demand for high-performance computing and AI-driven workloads, along with expanding cloud and edge computing infrastructure, are the key market drivers.

The Data Center Precision Cooling market is poised to witness a CAGR of 12.9% from 2025 to 2032.

The growing adoption of sustainable and energy-efficient cooling solutions is the key market opportunity.

Vertiv Group Corp., Schneider Electric S.E., STULZ GmbH, Daikin Industries Ltd., and Mitsubishi Electric Corporation are key market players.