- Food Ingredients & Additives

- Plant-Based Ice Creams Market

Plant-Based Ice Creams Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Plant-Based Ice Creams Market Size, Share, Trends by Source (Almond milk, Coconut milk, Soy milk, Oat milk, Cashew milk, and Others), by Flavor (Chocolate, Vanilla, Fruit, Nuts & caramel, Coffee & mocha, and Others), Sales Channel (HoReCa, Hypermarkets/Supermarkets, Convenience Stores, Specialty stores, Online Retail, and Others), and Regional Analysis, 2026 - 2033

Plant-based Ice Creams Market Share and Trends Analysis

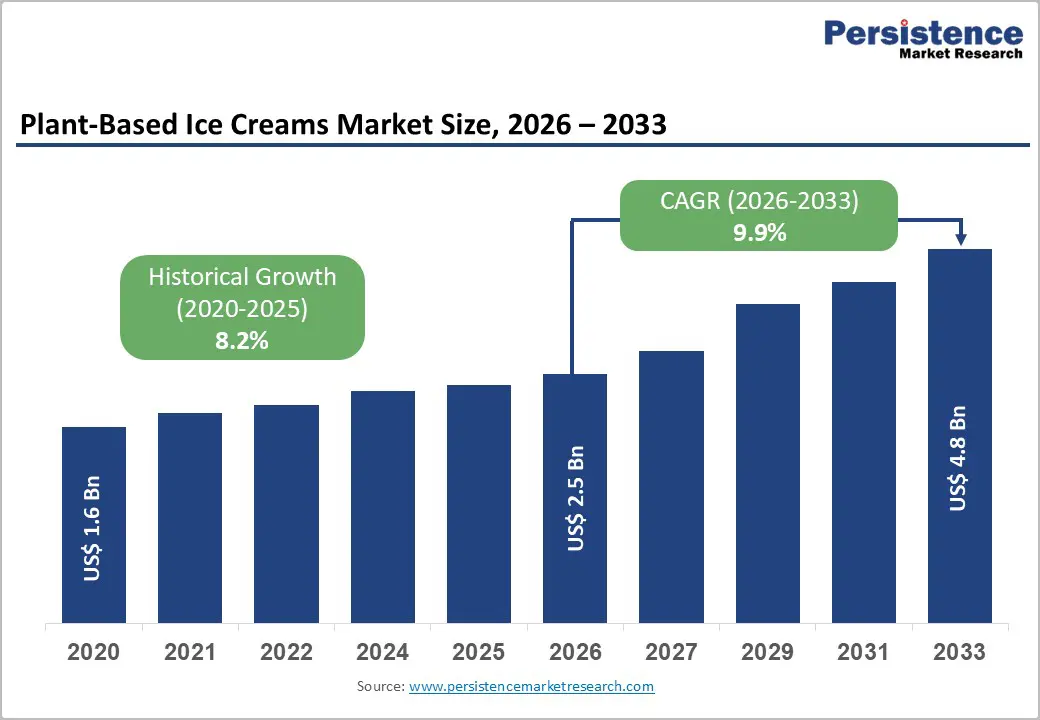

The global plant-based ice creams market size is expected to be valued at US$ 2.5 billion in 2026 and projected to reach US$ 4.8 billion by 2033, growing at a CAGR of 9.9% between 2026 and 2033.

The market is primarily propelled by the escalating global prevalence of lactose intolerance and a structural shift toward veganism among Gen Z and Millennial demographics. Rising environmental concerns about methane emissions from dairy farming have prompted consumers to seek sustainable alternatives with comparable sensory profiles. Furthermore, significant investments by multinational corporations such as Unilever PLC and Nestlé S.A. in high-moisture extrusion and precision fermentation have bridged the texture gap, making dairy-free options increasingly indistinguishable from traditional frozen desserts.

Key Industry Highlights:

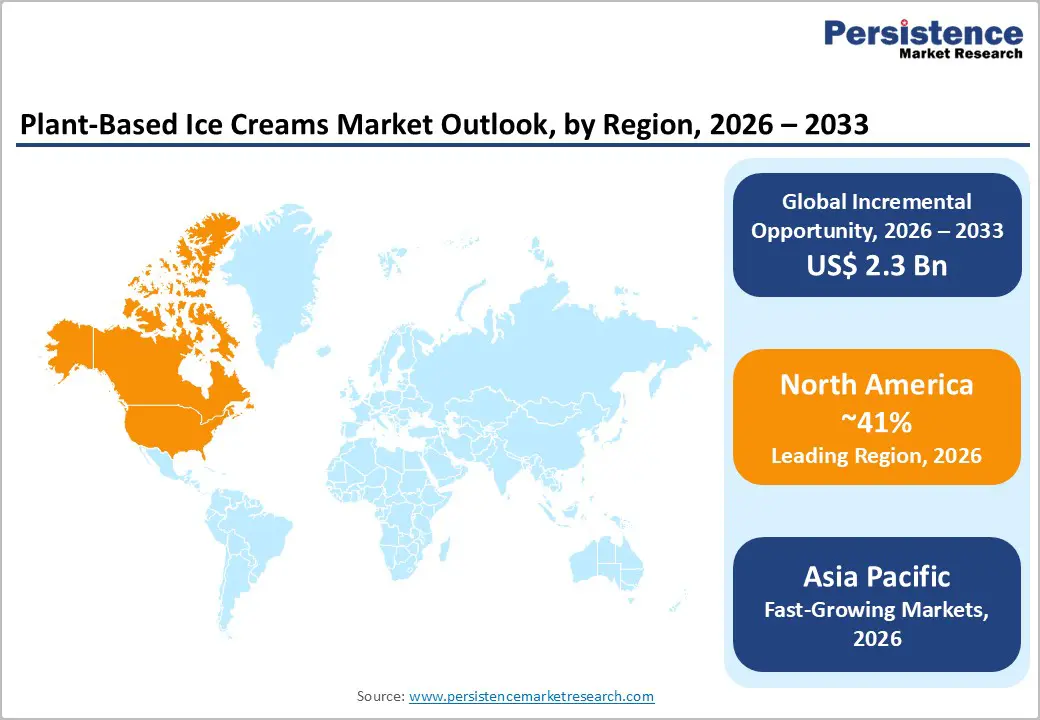

- Leading Region: North America dominated the market in 2025 with a 41% share, driven by high consumer awareness, a robust retail infrastructure, and the early adoption of vegan lifestyles in the U.S.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, fueled by rising disposable incomes, a high prevalence of lactose intolerance, and the rapid expansion of Online Retail in China and India.

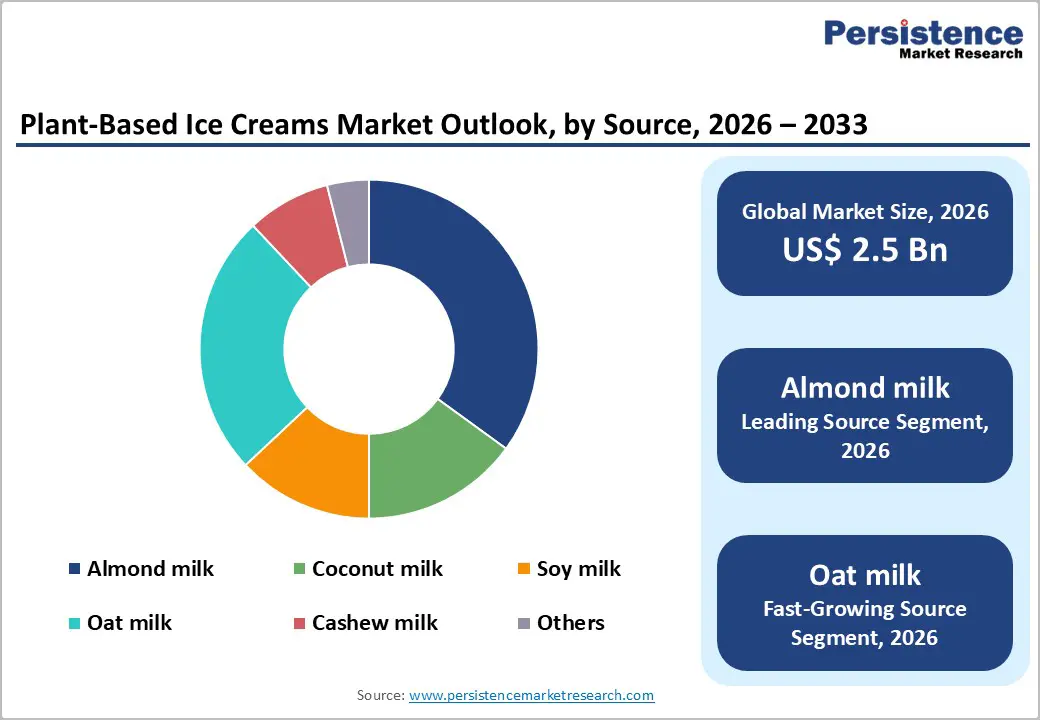

- Dominant Segment: Almond milk remains the leading source segment, valued for its familiarity and light texture, though it faces increasing competition from creamier alternatives like Oat and Cashew.

- Fastest Growing Segment: Oat milk is the fastest-growing source category, preferred for its neutral taste, superior creaminess, and lower environmental impact compared to other nut-based or dairy alternatives.

- Key Market Opportunity: The integration of precision fermentation and animal-free dairy proteins presents a significant opportunity to attract flexitarian consumers by offering a molecularly identical vegan ice cream experience.

| Global Market Attributes | Key Insights |

|---|---|

| Plant-Based Ice Creams Market Size (2026E) | US$ 2.5 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.2% |

Market Dynamics

Driver - Rising Health Consciousness and Lactose Intolerance Awareness

The global surge in digestive health awareness acts as a primary catalyst for market expansion. According to the National Institutes of Health (NIH), approximately 65% to 70% of the global population has some degree of lactose malabsorption. This physiological necessity, combined with a broader clean-label movement, has shifted consumer interest toward plant-derived lipids. Unlike traditional dairy, plant-based alternatives often feature lower saturated fat and zero cholesterol. In 2025, health-conscious consumers increasingly viewed Almond milk and Oat milk bases as functional foods, often enriched with Vitamin D and B12 to mirror the nutritional density of cow’s milk. This shift is particularly evident in the United States and Western Europe, where the demand for allergen-friendly desserts has become a mainstream retail requirement rather than a niche preference.

Restraints - High Price Points and Production Costs

The premium pricing of plant-based frozen desserts remains a significant barrier to universal adoption. Ingredients such as organic Almond milk, high-grade Cashews, and specialized stabilizers such as guar gum or locust bean gum incur higher procurement costs than subsidized dairy milk. Furthermore, the complexity of maintaining the overrun (the air incorporated during freezing) in plant-based proteins requires more intensive processing. Data from 2025 indicates that vegan ice cream pints can be 20% to 40% more expensive than their dairy counterparts. This price disparity limits market penetration in price-sensitive emerging economies across Latin America and parts of the Asia-Pacific, where dairy-based impulse products still dominate lower-tier consumer segments.

Opportunity - Advancements in Precision Fermentation and Lab-Grown Dairy

The emergence of precision fermentation represents a transformative opportunity for market participants. Companies such as Perfect Day, Inc. are producing bio-identical whey proteins using microflora, enabling the creation of ice cream that is molecularly identical to dairy but remains entirely vegan. This animal-free dairy segment is expected to capture significant market share by addressing long-standing issues of texture and flavor consistency. In 2025, several global brands began integrating these lab-grown proteins into their premium lines. This technology enables manufacturers to target flexitarian consumers who do not follow a strict vegan diet but are motivated by animal welfare and sustainability, providing a future-proof growth avenue that could redefine the plant-based ice cream market landscape.

Category-wise Analysis

Source Insights

In 2025, Almond milk remains the leading segment, commanding a 35% market share. This dominance is attributed to its early entry into the market and widespread consumer familiarity with its light texture and subtle nutty profile. Almond milk is perceived as a healthy base due to its low calorie count and high Vitamin E content. However, Oat milk is the fastest-growing segment for the 2026 - 2033 period. The rapid rise of Oatly Group AB and the inherent creaminess of oats, which naturally contain starches that mimic the viscosity of dairy, have made it the preferred base for premium artisanal brands. Unlike Almond milk, Oat milk production is also touted for having a lower water footprint, appealing to the growing segment of environmentally conscious consumers.

Sales Channel Insights

Hypermarkets/supermarkets represent the leading sales channel in 2025, accounting for over 46% of total revenue. These large-scale retailers provide the necessary cold-chain infrastructure and bulk-purchasing options (pints and multi-packs) that drive the take-home consumption model. Conversely, Online Retail is the fastest-growing channel. The shift toward D2C (Direct-to-Consumer) models by premium brands like Van Leeuwen Ice Cream and the integration of rapid delivery services have revolutionized accessibility. The ability to offer a wider variety of SKUs online than is typically available on physical shelves has proven to be a key differentiator, especially for niche artisanal brands targeting specific dietary needs such as keto-vegan or sugar-free plant-based options.

Regional Insights

North America Plant-Based Ice Creams Market Trends and Insights

North America remains the dominant regional market, holding 41% share in 2025. This leadership is sustained by a mature vegan ecosystem in the United States and Canada, where plant-based diets have moved from the periphery to the mainstream. The U.S. Food and Drug Administration (FDA) recently released draft guidance in January 2025 regarding the labeling of plant-based alternatives, emphasizing clarity in nutrient disclosure. This regulatory framework, while stringent, has actually boosted consumer trust by ensuring that dairy-free claims are backed by standardized nutritional profiles.

Innovation in the U.S. is largely driven by the premiumization trend. Brands such as NadaMoo! and Coconut Bliss are focusing on high-quality ingredients and sustainable sourcing, often leveraging fair-trade certifications to appeal to ethical shoppers. The presence of a robust venture capital environment has also allowed startups like Cado Ice Cream (using avocado as a base) to scale rapidly, ensuring that the North American market remains the global hub for product diversity and technological advancement in the frozen dessert sector.

Europe Plant-Based Ice Creams Market Trends and Insights

The European market is characterized by a strong emphasis on sustainability and a highly fragmented regulatory landscape. Germany, the U.K., and France are the primary growth engines, driven by a high percentage of flexitarian consumers. In 2024, the European Parliament continued to debate the dairy naming ban, which restricts the use of terms like milk or butter for non-dairy products. Despite these hurdles, brands have successfully adapted by focusing on brand identity and the vegan symbol (the V-Label), which is widely recognized across the continent.

Regulatory harmonization through the European Green Deal is also pushing manufacturers toward eco-friendly packaging. By 2025, a majority of European plant-based ice cream brands have transitioned to compostable or FSC-certified paper tubs. The U.K. specifically has witnessed a surge in artisanal plant-based parlors in cities like London and Manchester, indicating a strong demand for high-quality, non-industrialized vegan treats that cater to local taste preferences while maintaining strict animal welfare standards.

Competitive Landscape

The global plant-based ice creams market is currently in a state of moderate consolidation, where large multinational conglomerates coexist with a vibrant ecosystem of specialized startups. Leaders like Unilever PLC and Danone S.A. maintain their dominance through extensive distribution networks and the acquisition of successful niche brands (e.g., Danone’s acquisition of WhiteWave Foods). However, the market remains fragmented at the premium and artisanal levels, where brand loyalty is driven by unique flavor profiles and ethical storytelling. Key differentiators have shifted from simple dairy-free status to total sustainability, including carbon-neutral manufacturing and plastic-free packaging. Emerging business models are increasingly focusing on the HoReCa (Hotel, Restaurant, and Café) sector, where custom-branded vegan soft-serve and artisanal scoops are becoming standard offerings. Research and development are currently focused on next-generation bases such as Faba bean and potato protein to find the ultimate balance between sustainability and creaminess.

Key Developments:

- In August 2025, Japanese food tech startup Kinish entered the plant-based dessert space with the launch of The Rice Creamery, a vegan ice cream brand leveraging rice as a dairy alternative to target allergen-free and sustainability-driven consumers.

- In July 2025, Latvia’s Food Union marked a strategic shift as its iconic Pols brand introduced a 100% vegan coconut milk-based ice cream, signaling legacy dairy players’ adaptation to modern, plant-forward snacking trends.

- In April 2025, Oppo Brothers expanded its better-for-you portfolio with Oppo Refreshed, a low-calorie vegan ice cream stick range that blends sorbet-style fruit refreshment with ice cream-like creaminess.

Companies Covered in Plant-Based Ice Creams Market

- Unilever PLC

- Nestlé S.A.

- General Mills Inc.

- Danone S.A.

- Perfect Day, Inc.

- Oatly Group AB

- NadaMoo!

- Coconut Bliss

- Cado Ice Cream

- Mammoth Creameries

- Van Leeuwen Ice Cream

- Others

Frequently Asked Questions

The global plant-based ice creams market is projected to be valued at US$ 2.5 Bn in 2026.

Rising Health Consciousness and Lactose Intolerance Awareness is driving demand for Plant-Based Ice Creams market.

The Global Plant-Based Ice Creams market is poised to witness a CAGR of 9.9% between 2026 and 2033.

Advancements in Precision Fermentation and Lab-Grown Dairy is key opportunity for key players in the market.

Leading companies include Unilever PLC, Nestlé S.A., General Mills Inc., Danone S.A., Perfect Day, Inc., Oatly Group AB, and Others.