- Processed Food

- Plant-based Butter Alternative Market

Plant-based Butter Alternative Market Size, Share, and Growth Forecast, 2026 - 2033

Plant-based Butter Alternative Market by Product Form (Flavored, Salted, Unsalted), Source (Almond, Cashew, Coconut, Olive, Soy), Distribution Channel (Convenience Store, Food Service, Online Retail, Others), and Regional Analysis for 2026 - 2033

Plant-based Butter Alternative Market Size and Trends Analysis

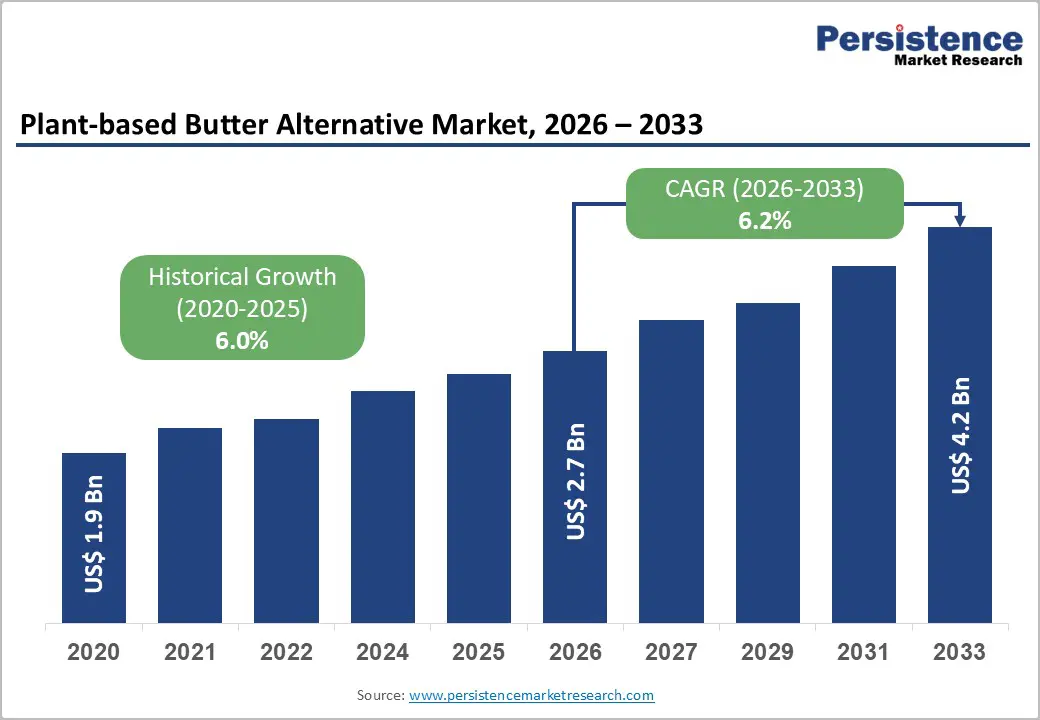

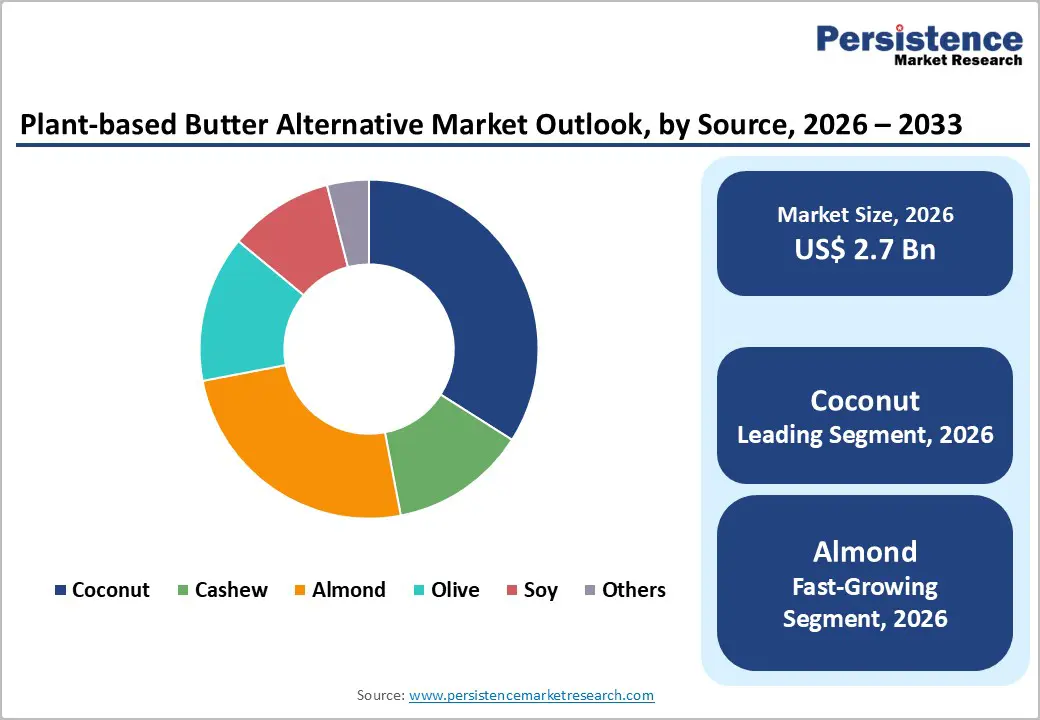

The global plant-based butter alternative market size is likely to be valued at US$2.7 billion in 2026 and is expected to reach US$4.2 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by a fundamental shift in consumer preferences toward plant-based and dairy-free food options. Increasing awareness of lactose intolerance, coupled with the rising adoption of vegan and flexitarian lifestyles, is significantly influencing purchasing behavior.

Consumers are actively seeking healthier alternatives to traditional dairy butter, favoring products with lower saturated fat content and clean-label ingredients. Sustainability concerns related to animal agriculture, including environmental impact and resource consumption, are encouraging a transition toward plant-derived formulations. Manufacturers are responding with continuous product innovation, focusing on improving taste, texture, and functionality to closely replicate conventional butter, which is enhancing consumer acceptance across both household and commercial applications.

Key Industry Highlights:

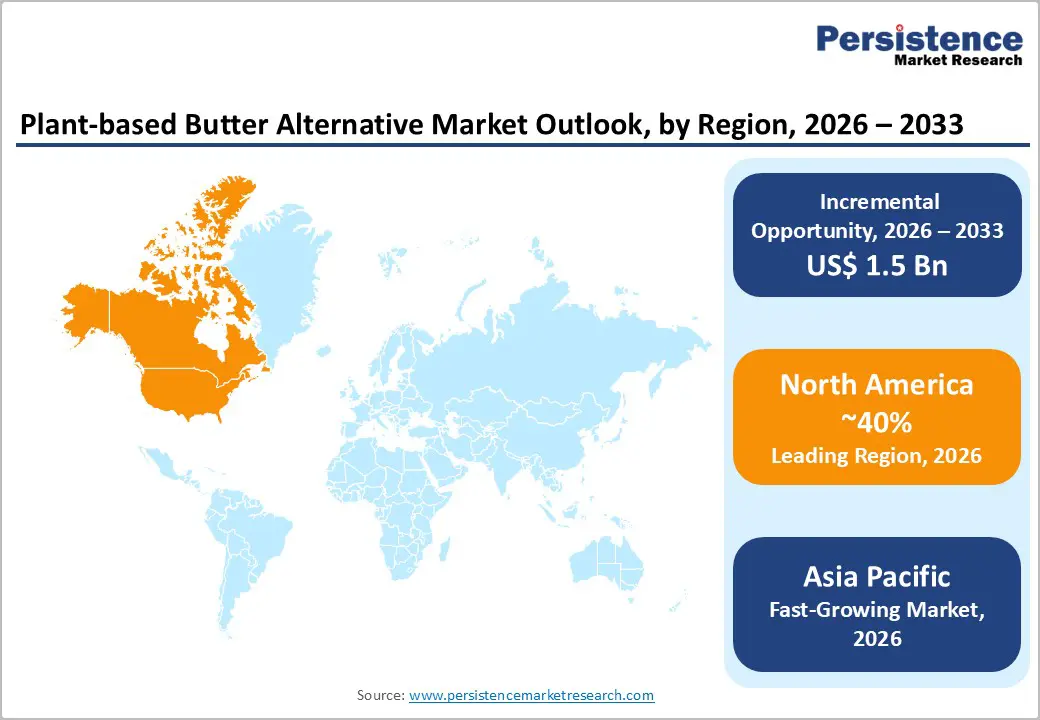

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong consumer adoption, innovation, and a well-established retail and foodservice ecosystem.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by strong demand growth and regional manufacturing advantages.

- Leading Product Form: Unsalted is projected to represent the leading product form in 2026, accounting for 45% of the revenue share, driven by its versatility in cooking, baking, and ability to serve as a neutral base without altering flavor profiles.

- Leading Source Type: Coconut is anticipated to be the leading source type, accounting for over 40% of the revenue share in 2026, supported by its natural creaminess and functional similarity to traditional butter in cooking and baking applications.

| Key Insights | Details |

|---|---|

|

Plant-based Butter Alternative Market Size (2026E) |

US$2.7 Bn |

|

Market Value Forecast (2033F) |

US$4.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.0% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Rising Health Consciousness and Prevalence of Lactose Intolerance and Dairy Allergies

Consumers are increasingly aware of the health implications associated with high saturated fat intake, cholesterol, and lactose consumption, prompting a shift toward plant-based alternatives. Lactose intolerance and dairy allergies affect a growing proportion of the population, creating strong demand for products that offer similar taste and functionality without adverse health effects. Plant-based butter alternatives provide a suitable solution, delivering creamy textures and versatile applications while catering to sensitive digestive systems.

Rising health consciousness also encourages the adoption of clean-label products, emphasizing natural ingredients and minimal processing. Manufacturers are responding by fortifying plant-based butter with vitamins, omega fatty acids, and functional ingredients to appeal to health-oriented consumers. The market benefits from increased awareness campaigns highlighting the benefits of dairy-free options, targeting allergy-prone demographics, fitness enthusiasts, and families seeking healthier spreads for daily use. Retailers are expanding plant-based offerings across mainstream and premium shelves, ensuring visibility and accessibility.

Growing Adoption of Vegan, Vegetarian, and Flexitarian Diets

Dietary shifts toward vegan, vegetarian, and flexitarian lifestyles are reshaping food consumption patterns. Consumers are increasingly reducing animal product intake for ethical, environmental, and health reasons, creating opportunities for plant-based butter alternatives. These products align with values such as animal welfare, lower carbon footprint, and sustainable food systems while fulfilling culinary needs for spreads, cooking, and baking. Retailers and foodservice providers are actively responding by integrating plant-based butter into meal solutions, bakery applications, and ready-to-eat products, broadening adoption across multiple channels.

The rise of flexitarian diets, in particular, expands the target demographic beyond strict vegans. Consumers are exploring plant-based options as partial replacements without compromising taste, convenience, or nutritional needs. Influencers, social media trends, and recipe innovation are promoting plant-based spreads as versatile, everyday staples. Product positioning emphasizes ethical sourcing, sustainability claims, and clean-label benefits, fostering brand differentiation. This growing dietary consciousness fuels continuous market expansion, drives premiumization of offerings, and motivates manufacturers to innovate flavors, textures, and functional formulations to satisfy increasingly diverse consumer demands.

Restraint Analysis - Perception and Sensory Gaps Relative to Traditional Butter

Despite technological advancements, plant-based butter alternatives still face challenges replicating the full sensory experience of traditional dairy butter. Taste, aroma, and mouthfeel differences can create consumer hesitation, especially among individuals accustomed to conventional butter. Variations in melting behavior and texture during cooking or baking can impact culinary results, leading to perceived inferiority. Even with marketing highlighting health or sustainability benefits, some consumers may prioritize flavor authenticity, limiting adoption in certain demographics or high-end culinary applications.

Overcoming these perception challenges requires significant investment in R&D and formulation expertise. Manufacturers are experimenting with ingredient blends, fermentation techniques, and fat structuring technologies to closely mimic dairy characteristics. Education through sampling campaigns, chef endorsements, and recipe integration can also mitigate hesitancy. Retail and foodservice sectors play a role by positioning plant-based spreads as functional alternatives rather than exact substitutes, gradually shaping taste acceptance.

Inconsistent Labeling Standards

Variability in labeling regulations across countries complicates product marketing and consumer understanding. Terms such as butter, spread, or margarine face restrictions in some regions, leading to confusion about nutritional content, ingredients, and functional use. Consumers seeking clarity on fat composition, allergens, or source ingredients may hesitate to adopt plant-based alternatives if labeling is inconsistent or unclear. This lack of standardized guidance affects trust, purchase confidence, and cross-border market expansion, particularly in regions where regulatory frameworks are evolving or fragmented.

Brands must invest in compliance and transparency to navigate diverse labeling environments. Clear ingredient declarations, allergen warnings, and nutritional transparency help mitigate consumer uncertainty. Certification programs, such as vegan, organic, or non-GMO labeling, can enhance credibility but require adherence to strict standards. Inconsistent labeling affects how consumers perceive products and also creates challenges for manufacturers operating in different regional markets. Ensuring harmonized, informative, and reliable labeling is essential to foster acceptance, maintain brand trust, and enable broader distribution across both domestic and international retail channels.

Opportunity Analysis - Technological Convergence with Functional Ingredients and Clean-Label Formulations

The integration of functional ingredients and clean-label approaches presents a significant opportunity for the plant-based butter market. Consumers increasingly demand products that combine taste with health benefits, such as fortified vitamins, omega-3s, probiotics, or plant proteins. Clean-label formulations using minimally processed, natural ingredients resonate with health-conscious buyers seeking transparency and authenticity. This convergence allows manufacturers to differentiate products, justify premium pricing, and appeal to diverse demographics seeking both nutrition and indulgence.

Innovation extends to flavor, texture, and stability enhancements achieved through plant protein blends, emulsification technologies, and fat structuring methods. Marketing emphasis on functional benefits and natural sourcing strengthens brand positioning and encourages trial among skeptical consumers. Retailers and foodservice providers benefit from versatile, value-added products suitable for various culinary applications. Leveraging technology to align sensory quality with functional claims enables plant-based butter alternatives to compete with conventional butter while meeting evolving consumer expectations in taste, health, and sustainability.

Fermentation and Sustainable Tech Convergence

Emerging fermentation-based technologies offer the potential to replicate butter’s sensory and functional characteristics sustainably. Microbial fermentation can produce fats and flavors that closely mimic dairy butter while reducing environmental impact and resource usage. Coupling these techniques with sustainable sourcing of plant ingredients enhances eco-friendly appeal, meeting the growing consumer demand for ethical and low-carbon products. Fermentation also enables precise control over texture, melting point, and flavor profiles, providing differentiated offerings in a competitive market.

Investment in sustainable technology convergence supports cost-efficient scale-up, localized production, and reduced dependence on commodity volatility. Partnerships between biotech firms and food manufacturers accelerate product innovation, bringing premium and functional plant-based butter alternatives to market faster. Regulatory acceptance and consumer education regarding fermentation-derived ingredients enhance market potential. This convergence positions companies to capitalize on environmental trends, address taste and texture gaps, and meet both B2B and B2C demand for high-quality, sustainable, and innovative butter alternatives.

Category-wise Analysis

Product Form Insights

Unsalted is expected to lead the plant-based butter alternative market, accounting for approximately 45% of revenue in 2026, driven by its versatility and wide-ranging applications in cooking, baking, and general use. Their neutral flavor allows consumers to incorporate them seamlessly into recipes without affecting taste, making them suitable for both household and commercial culinary needs. Unsalted butter alternatives serve as direct substitutes for dairy butter, allowing flexibility in seasoning, baking, and food preparation. For example, Upfield’s Flora Plant Butter Unsalted has gained notable traction due to its smooth texture, clean label, and compatibility with various recipes, reflecting the strong consumer preference for neutral, multipurpose options.

Flavored is likely to represent the fastest-growing segment, supported by increasing consumer interest in innovative taste experiences and premium offerings. Products infused with flavors such as garlic, herbs, or cinnamon appeal to consumers seeking convenient, ready-to-use spreads for snacking, specialty recipes, or culinary experimentation. The segment benefits from trends toward experiential eating, where flavor differentiation and creativity influence purchase decisions. For example, Miyoko’s Garlic Herb Cultured Butter has successfully captured consumer attention with its rich taste and artisanal positioning, highlighting the growing demand for unique, flavorful plant-based spreads.

Source Type Insights

Coconut is projected to lead the market, capturing around 40% of the revenue share in 2026, supported by its natural creaminess, functional similarity to dairy butter, and widespread consumer familiarity. Coconut fats provide a desirable texture and melting behavior that closely mimics traditional butter, making them ideal for spreads, baking, and cooking applications. Cost-effectiveness and ease of sourcing from regions such as Southeast Asia strengthen their market dominance. For example, Butters & More Vegan Natural Coconut Butter represents a real coconut-based plant butter alternative commonly used as a dairy-free spread and in baking, illustrating consumer preference for coconut variants due to their texture and usability.

Almond is likely to be the fastest-growing source type, driven by their premium positioning, mild flavor, and association with health-conscious lifestyles. Almond spreads are favored for their perceived nutritional benefits, including protein content, vitamin E, and healthy fats, appealing to consumers seeking functional, indulgent, and clean-label options. For example, The Butternut Co. Almond Butter Creamy is a real almond-based plant butter alternative that exemplifies the growing interest in almond-derived spreads for their mild flavor and perceived nutritional benefits, supporting the accelerated growth of this segment. Almond variants also benefit from enhanced processing techniques that reduce bitterness, improve stability, and ensure consistent quality, encouraging broader acceptance in retail, online, and foodservice channels.

Regional Insights

North America Plant-based Butter Alternative Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by high health awareness and widespread adoption of vegan and flexitarian diets in the U.S. and Canada. Manufacturers are introducing a broader range of textures, formulations, and functional profiles to meet diverse tastes and dietary needs. Clean-label positioning and nutritional enhancements such as lower saturated fat content and added plant-based nutrients are appealing to health-oriented consumers who seek both everyday utility and perceived wellness benefits in their spreads.

Leading brands are actively shaping these trends with strategic product launches and expanded market presence. For example, Upfield has broadened its retail footprint across North American grocery chains with its plant-based butter offerings, leveraging flavor variety and improved sensory profiles to attract mainstream consumers. These companies emphasize research-driven innovation, functional ingredient integration, and sustainability messaging to differentiate their products in a competitive landscape. Foodservice adoption is also rising as cafés, bakeries, and restaurants incorporate plant-based butters to cater to expanding vegan and allergy-friendly menus.

Europe Plant-based Butter Alternative Market Trends

Europe is likely to be a significant market for plant-based butter alternatives, due to well-established consumer demand for plant-based and clean-label foods, particularly in Western European countries with high vegan and sustainability awareness. The region’s mature organic food sector and increasing lactose intolerance awareness are driving consistent product launches that emphasize natural ingredients, improved nutritional profiles, and diverse culinary applications. Retailers across the UK, Germany, France, and the Netherlands are expanding their plant-based dairy aisles to include a wider variety of butter alternatives, reflecting broader dietary shifts.

European brands and manufacturers are leveraging this trend to introduce products tailored to local tastes and culinary traditions, contributing to a vibrant, competitive landscape. For example, Naturli’ Foods A/S has expanded its European presence with plant-based butter alternatives made from rapeseed, coconut, and other plant oils, catering to demand for dairy-free spreads that perform well in baking and cooking applications. Naturli’ emphasizes sustainability, clean-label formulations, and functional performance, aligning with consumer expectations for healthy, environmentally conscious food choices.

Asia Pacific Plant-based Butter Alternative Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by shifting dietary preferences and increasing health awareness, which propel demand for dairy-free options across the region. Rapid urbanization, rising disposable incomes, and expanding middle-class populations in countries such as China and India are major contributors to this trend, with consumers increasingly seeking healthier, lactose-free, and sustainable food alternatives. Plant-based butter resonates with prevailing dietary transitions toward plant-based-centric eating, supported by growing vegetarian and flexitarian lifestyles.

Regional and multinational companies are capitalizing on these opportunities with tailored products that appeal to local tastes and preferences. In the Asia Pacific plant-based butter alternative market, Bunge Loders Croklaan has introduced Beleaf™ PlantBetter, a plant-based butter alternative designed to meet growing demand for dairy-free options with sensory and functional qualities similar to traditional butter. Beleaf™ PlantBetter combines plant oils such as coconut and rapeseed to deliver desirable texture and performance for bakery and food production applications, highlighting innovation in the region’s plant-based ingredient landscape.

Competitive Landscape

The global plant-based butter alternative market exhibits a moderately fragmented structure, driven by the presence of several well-established multinational companies alongside a growing number of innovative niche brands focused on new formulations and sensory performance. Smaller brands and startups also contribute to fragmentation by targeting specific segments such as organic, artisanal, or functional ingredient fortified products, creating a landscape where innovation and differentiation are essential competitive levers.

With key leaders including Upfield Holdings B.V., Conagra Brands, Inc., and Naturli’ Foods A/S setting competitive benchmarks, the landscape continues to evolve rapidly. These players compete through continuous product innovation, expanded distribution strategies, and sustainability initiatives that align with consumer preferences for healthier and environmentally friendly food choices.

Key Industry Developments:

- In January 2026, Japanese plant-based food brand Brown Sugar 1st officially launched its Better Than Butter vegan plant-based butter alternative in the U.S., marking a significant international expansion for the product. Better Than Butter is crafted predominantly from coconut-derived ingredients and is designed to deliver rich taste and versatile performance in both home kitchens and professional culinary settings, while also being certified organic, halal, and kosher.

- In May 2025, French luxury pastry brand Maison Linotte launched “Purely,” a new organic plant-based butter designed specifically for professional chefs and pastry makers. The product, free from palm oil, additives, and major allergens, is formulated to act as a direct 1:1 replacement for conventional butter without altering the flavor or appearance of baked goods. Maison Linotte developed Purely to fill a gap in clean, high-quality plant-based butter options, appealing to both chefs and home bakers seeking reliable performance and natural ingredients.

- In July 2025, agribusiness leader Bunge introduced its Beleaf® PlantBetter plant-based butter alternative to the North American market, expanding on its earlier European launch and addressing growing industry demand for dairy-free spreads that match traditional butter’s sensory and functional qualities. Beleaf® PlantBetter is formulated from recognizable plant ingredients such as coconut, rapeseed, and cocoa butter, and delivers comparable aroma, texture, melt profile, and versatility for bakery, sauce, and prepared food applications.

Companies Covered in Plant-based Butter Alternative Market

- Upfield B.V.

- Unilever PLC

- Conagra Brands, Inc.

- The Kraft Heinz Company

- Oatly AB

- Miyoko's Creamery, Inc.

- Follow Your Heart, Inc.

- Daiya Foods Inc.

- Valsoia S.p.A.

- Naturli Foods A/S

Frequently Asked Questions

The global plant-based butter alternative market is projected to reach US$2.7 billion in 2026.

The plant-based butter alternative market is driven by rising health consciousness, increasing vegan and flexitarian diets, and growing demand for sustainable, dairy-free products.

The plant-based butter alternative market is expected to grow at a CAGR of 6.2% from 2026 to 2033.

Key market opportunities lie in product innovation with functional ingredients, clean-label formulations, premium flavored variants, and expansion into foodservice and emerging regional markets.

Upfield B.V., Unilever PLC, Conagra Brands, Inc., The Kraft Heinz Company, and Oatly AB are the leading players in the plant-based butter alternative market.