- Pharmaceuticals

- PET Radioactive Tracers Market

PET Radioactive Tracers Market Size, Share, and Growth Forecast for 2025 - 2032

PET Radioactive Tracers Market by Product (F-18 [Florbetapir, Florbetaben, Flutemetamol, Fludeoxyglucose, Sodium Fluoride], by Application (Neurological Disorders [Alzheimer’s Disease, Dementia], Cancer Diagnosis & Prognosis [Solid Tumors, Hematology Tumors], Cardiac Dysfunctions [Myocardial Infarction], Infectious Disease Diagnosis), and Regional Analysis

PET Radioactive Tracers Market Size and Share Analysis

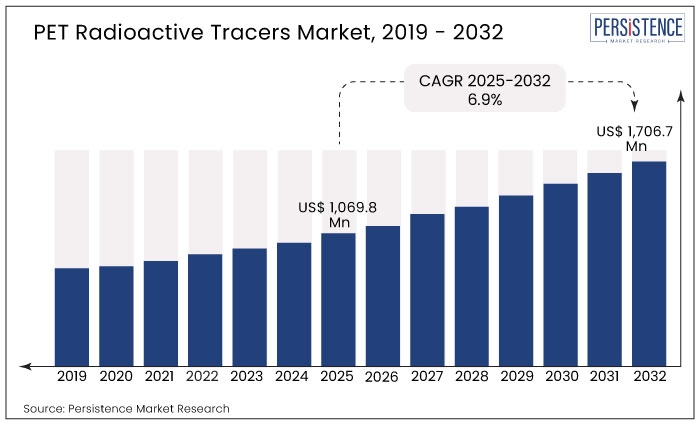

The global PET radioactive tracers market expanded at a CAGR of 4.5% from 2019 to 2024 and reached US$ 1,023.70 million in 2024. The market is forecasted to evolve at a CAGR of 6.9% to reach US$ 1,706.7 billion by the end of 2032.

Radioactive tracers, also known as radiotracers or radiopharmaceuticals, are substances used in medical imaging to help locate the diseased area before further treatment procedures. These tracers contain a small amount of a radioactive substance, which emits radiation that can be detected by specialized imaging equipment such as single-photon emission computed tomography (SPECT) and positron emission tomography (PET) scanners.

- Product-grade-based F-18 tracers accounted for a market share of 39.9% in 2024.

- Sales of PET radioactive tracers accounted for 14% share of the global radiopharmaceutical market in 2024.

In recent years, there have been several new radiopharmaceuticals approved by regulatory authorities such as the European Medicines Agency (EMA) and the United States Food and Drug Administration (FDA). These products have been developed for a range of applications, including cancer imaging and therapy, neurological disorders, and cardiology.

- For example, Lantheus obtained clearance from the FDA in May 2021 for the use of PYLARIFY® (piflufolastat F 18) Injection as a PET imaging agent for prostate cancer.

Gallium-68 has found extensive usage in nuclear medicine, especially in the diagnosis and evaluation of prostate cancer. The advancement heavily depends on the integration of various technological advancements and the introduction of a new radiotracer called 68Ga-PSMA-11, which was developed by the University of Heidelberg. The marketing authorization of the first 68Ge/68Ga generator, manufactured by the German manufacturer Eckert & Ziegler, has also positively impacted the penetration of the 68Ga-PSMA-11 tracer in the treatment of prostate cancer.

- Despite its shorter half-life, 68Ga has an ideal profile as a PET imaging agent. Several manufacturers are focusing on the introduction of cold kits for 68Ga labeling tracers (ANMI, Belgium), opening the gateways for 68Ga in PET.

Continuous development of radiopharmaceuticals and their use in nuclear medicine research for cancer diagnosis, along with the increasing prevalence of cancer, are some of the key factors driving the growth of the PET radioactive tracers market.

| Report Attribute | Details |

|---|---|

|

Global PET Radioactive Tracers Market Size (2025) |

US$ 1,069.8 Million |

|

Projected Market Value (2032) |

US$ 1,706.7 Million |

|

Market Growth Rate (2025 to 2032) |

6.9% CAGR |

|

Market Share of Top 5 Countries |

51.8% |

What are the Factors Influencing the Demand for PET Radioactive Tracers?

“Increasing Prevalence of Cancer Worldwide Driving Need for PET Radioactive Tracers”

Cancer is a complex disease, and accurate diagnosis and effective treatment often require the use of advanced imaging techniques, such as SPECT and PET. These imaging techniques use radiopharmaceuticals, or radioactive tracers, to detect and visualize cancerous tissues.

As the incidence of cancer continues to rise, the demand for these imaging techniques is also increasing.

- According to the World Health Organization (WHO), cancer is the second leading cause of death worldwide, and it is estimated that there will be 27.5 million new cases of cancer each year by 2040.

This growing prevalence of cancer is creating a significant demand for radiopharmaceuticals, including radioactive tracers, which are essential for accurate diagnosis and effective treatment.

Radiopharmaceuticals are essential for nuclear medicine imaging procedures such as SPECT and PET. Many countries rely on imported radiopharmaceuticals for these procedures, which can lead to supply chain problems, delays, and higher costs. Radiopharmaceutical manufacturers are currently focusing on increasing their domestic radioisotope production to generate higher revenues.

- A manufacturing facility operated by the Oak Ridge National Laboratory (ORNL) in the United States produces, purifies, and supplies more than 300 stable and radioactive isotopes that are used in medical, research, industrial, and space exploration applications.

Governments and private companies are investing in building domestic radiopharmaceutical production facilities. These facilities can produce a wide range of radiopharmaceuticals, ensuring a reliable and stable supply of products.

Increasing domestic radiopharmaceutical production will not only ensure a reliable and stable supply of radiopharmaceuticals for nuclear medicine imaging, but will also create jobs, facilitate access to healthcare, and improve healthcare outcomes.

What’s Hindering the Adoption of PET Radioactive Tracers?

“Limited Imaging Time Offered by PET Radioactive Tracers Due to Their Shorter Half-life”

Radiopharmaceuticals are radioisotopes with shorter half-lives due to their limited shelf life. Radiopharmaceuticals with shorter half-lives provide limited imaging time, which may be insufficient for some imaging protocols. This can be a challenge for imaging procedures that require longer imaging times, such as some dynamic PET studies.

The shorter half-life of radiopharmaceuticals can lead to decreased image quality, as the radiotracer may not have sufficient time to accumulate in the target tissue. This may result in images that are less clear and more difficult to interpret.

Radiopharmaceuticals with shorter half-lives may not be available in all imaging centers or hospitals, limiting their use in some clinical settings.

Country-wise Insights

What Makes the United States a Lucrative Market for Producers of PET Radioactive Tracers?

“Increasing Utilization of PET Scanning Boosting Demand for Radiopharmaceuticals”

The United States dominated the North American PET radioactive tracers market in 2024 with a revenue of US$ 310.57 million.

Use of PET scanning has grown significantly in the United States over the past decade. PET scans are commonly used in oncology to detect, stage, and monitor cancer, as well as in neurology to diagnose and track the progression of Alzheimer's and other neurological disorders.

- According to a report by the National Institutes of Health (NIH), the number of PET scans performed in the country increased from 200,000 in 1996 to 2 million in 2017.

How is Demand for PET Radioactive Tracers Shaping Up in China?

“Increasing Investments in Development of Advanced Cyclotron Facilities to Enhance Radioactive Isotope Production”

China held 48.8% share of the East Asia market in 2024. The country has made significant investments in the development of cyclotron facilities and in enhancing its radioactive tracer production capabilities in recent years, with several facilities located in cities such as Beijing, Shanghai, and Guangzhou. These facilities produce a range of radioactive isotopes for medical imaging applications, including fluorine-18, carbon-11, and oxygen-15.

- One of the advanced cyclotron facilities in China is the Beijing Cyclotron Center, which is operated by the Chinese Academy of Engineering Physics. This facility has multiple cyclotrons capable of producing a range of isotopes for medical imaging, including fluorine-18 and carbon-11.

What is the Demand Outlook for PET Radioactive Tracers in Germany?

“Growing Burden of Neurological Disorders in the Country”

Germany held 27.8% of the Western Europe market share in 2024. Neurological disorders, such as Alzheimer's disease, Parkinson's disease, and stroke, are a significant health burden in Germany, affecting millions of people each year.

Use of PET-CT imaging in the diagnosis and management of neurological disorders in Germany reflects a growing recognition of the importance of advanced medical imaging technologies in the field of neurology and a commitment to improving the care and outcomes for patients with these conditions.

Category-wise Insights

Which PET Radioactive Tracer Accounts for High Demand?

“High Demand for F-18 Tracers Due to Their Short Half-life Reducing Patients’ Radiation Exposure Time”

Fluorine-18 (F18) radioactive tracers held 39.9% share of the global market in 2024.

Fluorine-18 (F18) is a commonly used radioactive tracer in nuclear medicine. F18 is an isotope of fluorine that is routinely used in radiolabeling of biomolecules in PET. The fluorine-18 (F18) radioactive tracer is widely used in PET scans due to its short half-life of approximately 110 minutes, making it well-suited for imaging studies without prolonged exposure to patients. The fluorine-18 (F18) radioactive tracer currently holds a significant share of the global market.

Which Application Occupies a Dominant Share of the Market?

“Rising Awareness about Early Cancer Detection Driving Sales of Radioactive Tracers from Cancer Diagnosis & Prognosis Segment”

The cancer diagnosis & prognosis segment held 45.4% share of the market in 2024.

Radioactive tracers are extensively used for cancer diagnosis because they allow for the detection of cancerous tissues at an early stage, which can improve patient outcomes. They help differentiate between malignant and benign tumors, which is important for determining the appropriate treatment plan. Accurate detection and localization of cancerous tissues, even at early stages when they may not be visible on other imaging modalities, is a key factor for the cancer diagnosis & prognosis segment holding a dominant share of the market.

Competition Landscape

The PET radioactive tracers market is highly consolidated with few market players active within this space. Companies are investing significant efforts in expanding their foothold in emerging markets while also maintaining their relationships with existing distributors. They are also exploring options such as acquisitions, mergers, and partnerships with key players in the market to achieve their growth objectives.

Some key instances of this development include:

- In Sep 2022, the FDA accepted Blue Earth Diagnostics’ new drug application for a PET imaging agent, called 18F-rhPSMA-7.3. This drug is a radiohybrid PSMA (prostate-specific membrane antigen) for diagnostic imaging of prostate cancer.

- In March 2022, Cardinal Health announced its plans to construct a medical distribution center in Ohio in the United States to enhance its offerings.

The team at Persistence Market Research has tracked recent developments related to companies manufacturing PET radioactive tracers, which are available in the full report.

Companies Covered in PET Radioactive Tracers Market

- Eli Lilly and Company

- Blue Earth Diagnostics

- Lantheus

- Siemens Healthcare Private Limited

- GE Healthcare

- Advanced Accelerator Applications (Novartis)

- University of Lowa HealthCare

- Telix Pharmaceuticals Limited

- Jubilant Radiopharma

- TRASIS

- RadioMedix Inc.

- IBA Radiopharma Solutions

- Piramal Imaging (Life Molecular Imaging)

- Cardinal Health

- DuchemBio, Co., Ltd

Frequently Asked Questions

The market reached US$ 1,023.7 million in 2024.

The market is forecasted to reach US$ 1,706.7 million by 2032.

The market is projected to grow at a 6.9% CAGR during this period.

They are used in medical imaging to detect diseases, especially in cancer, neurology, and cardiology.

PET tracers accounted for 14% of the global radiopharmaceutical market in 2024.

F-18 tracers held the highest share, accounting for 39.9% of the market.