- Medical Devices

- PET/CT Systems Market

PET/CT Systems Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

PET/CT Systems Market by Product Type (Low-Range Slice Scanners, Middle-Range Slice Scanners, High-Range Slice Scanners), Isotope (Fluorodeoxyglucose, Gallium, Thallium, Others), by Modality (Fixed Scanners, Mobile Scanners), Application, End-user, Regional Analysis, from 2026 to 2033

PET/CT Systems Market Share and Trends Analysis

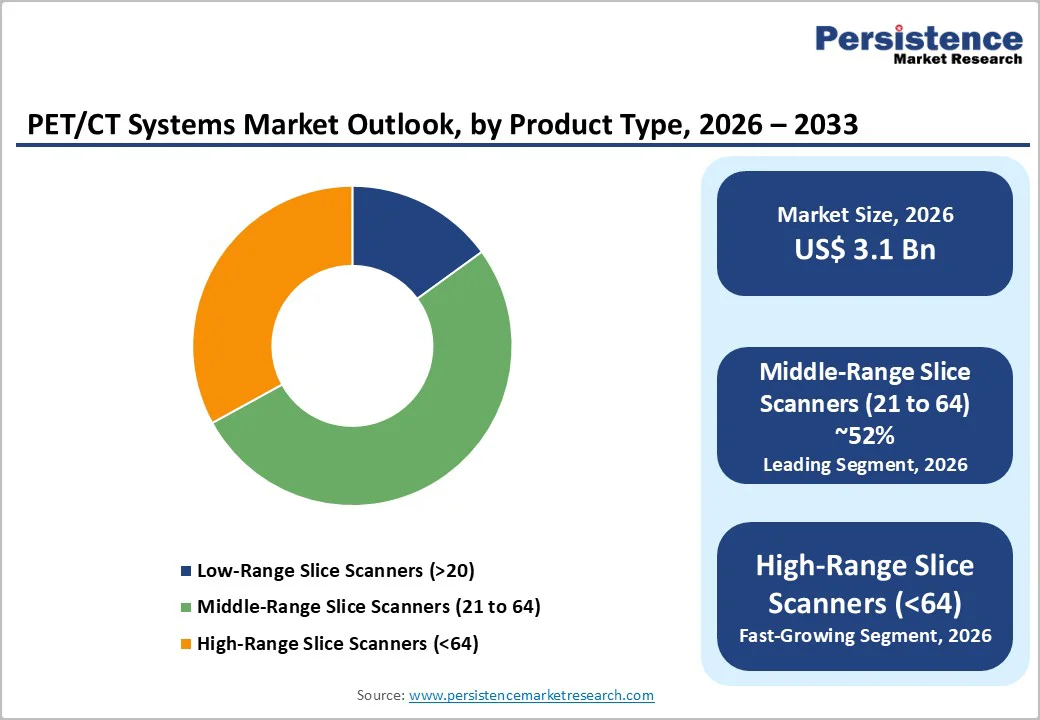

The global PET/CT systems market size is estimated to grow from US$ 3.1 billion in 2026 and reach US$ 4.6 billion, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033. PET/CT systems introduced corrected images exposure. PET/CT systems are also faster which helps reduce motion artifacts.

This unique mix of functional information being gathered with the help of Positron Emission Tomography (PET), with anatomic information collected with the help of Computed Tomography (CT), has led to an increase in the adoption of PET/CT systems. PET/CT systems have several major advantages for various applications over PET systems.

For instance, PET/CT increases sensitivity for the further detection of small brain metastases when performed with contrast agents and in a full-dose manner. They have helped reduce the time required for patients to lie motionless from approximately 40 minutes to 20 minutes.

Key Industry Highlights:

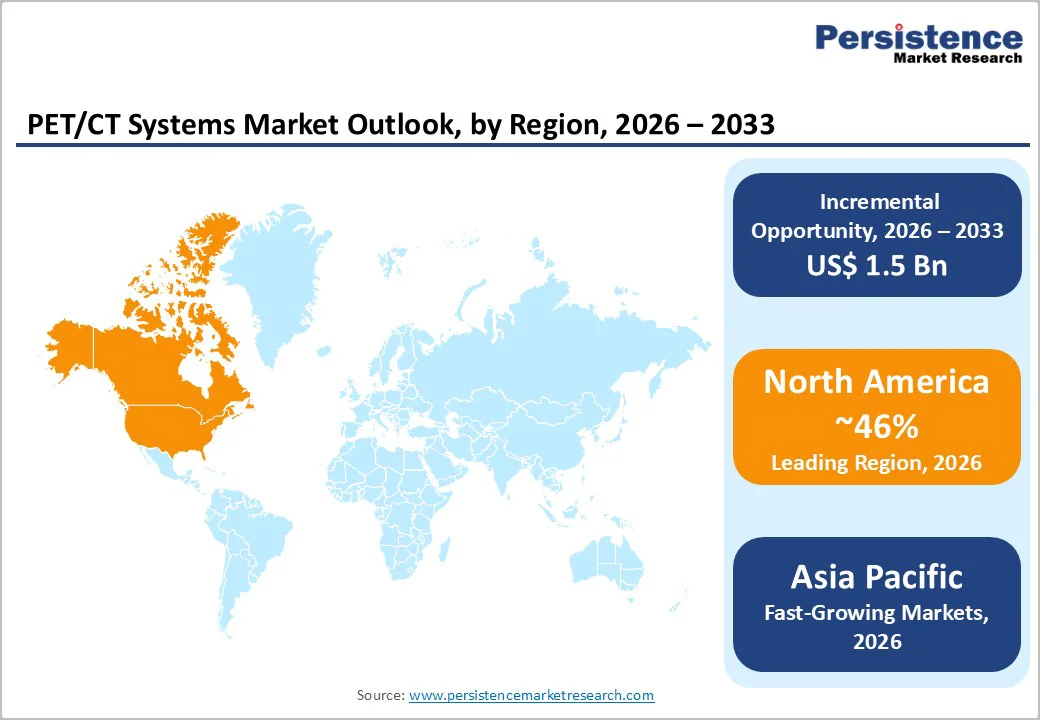

- Leading Region: North America remains the largest market, supported by high diagnostic imaging demand, strong oncology infrastructure, and widespread availability of advanced PET tracers and hybrid imaging facilities.

- Fastest Growing Region: Asia Pacific is expected to expand at the fastest pace, driven by rising cancer incidence, improved healthcare access, and rapid installation of modern PET/CT systems across China, India, and Southeast Asia.

- Dominant Segment: High-range slice PET/CT scanners (<64 slices) hold the largest share due to superior image resolution, faster scan times, and strong adoption in comprehensive cancer centers and academic hospitals.

- Fastest Growing Segment: Middle-Range Slice Scanners (21 to 64) represent the fastest-growing segment, fueled by rising demand for versatile imaging performance, wider affordability, and increasing adoption in expanding oncology and cardiac diagnostic programs.

| Key Insights | Details |

|---|---|

| PET/CT Systems Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.2% |

Market Dynamics

Driver - Increase in Demand for Cancer Monitoring Using PET/CT Systems Market

The management of cancer has evolved to include different modalities of treatment methods, such as chemotherapy, surgery, and radiation therapy. Efficient management requires the accurate evaluation and diagnosis of tumour growth, and PET/CT systems are being extensively used for providing sophisticated images for further assessing the origin of the tumour and the metastatic disease.

PET/CT systems are being increasingly adopted for cancer monitoring around the globe. In a study conducted at a major hospital in the Asian region, which consisted of 98 patients affected with various forms of cancer, it was found that PET-CT systems were successful in diagnosing the presence of cancer in 77% of the cases.

In comparison, a whole-body Magnetic Resonance Imaging (MRI) was able to do so in only 55% of them. Furthermore, the demand for PET/CT systems is being triggered by the growing demand from radiology departments. PET/CT systems can be easily used to perform standalone CT scans. This has further justified the usage of CT as a part of PET/CT systems for justifying the high investments in this technology.

Restraints - High Capital and Operating Costs of PET/CT Infrastructure

A key restraint limiting broader PET/CT adoption is the high financial burden associated with establishing and maintaining hybrid imaging facilities. PET/CT scanners require multimillion-dollar capital investment, and the costs extend beyond equipment to include specialized room construction, radiation shielding, and quality-assurance systems.

Operational expenses further elevate lifetime ownership costs, as providers must manage ongoing service contracts, periodic upgrades, consumables, and radiotracer procurement often sourced from nearby cyclotrons or commercial radiopharmacies.

Staffing requirements add another layer of expense since PET/CT imaging demands training in nuclear medicine physicians, technologists, physicists, and radiation safety personnel. In low- and middle-income countries, constrained healthcare budgets and competing priorities significantly slow technology adoption, with many centers operating aging equipment well past recommended replacement cycles.

Even in developed markets, tight reimbursement frameworks, cost-containment initiatives, and limited capital approvals make it challenging for community hospitals and small imaging centers to justify new installations. These financial pressures collectively hinder market expansion and restrict access to advanced hybrid imaging, particularly outside major urban healthcare hubs.

Opportunity - Rising Adoption of Mobile and Distributed Imaging Models

The increasing push to improve access to advanced diagnostic imaging offers a strong opportunity for mobile PET/CT units and distributed imaging networks. Many secondary hospitals and rural regions continue to face limited availability of hybrid imaging systems, resulting in long travel distances and delayed diagnostic pathways for patients.

Mobile PET/CT units deployed on scheduled routes or through long-term service agreements enable providers to extend high-quality imaging to underserved areas without the burden of building a full on-site facility. Similarly, hub-and-spoke models, where cyclotrons and radiopharmacy services are centralized and scanners are distributed across multiple satellite sites, help optimize asset usage and reduce overall operating costs.

Improvements in system design, including compact high-slice scanners, ruggedized components, and faster setup times, have made mobile deployment more practical and scalable.

Cloud-enabled reporting platforms and remote reading capabilities further support these models by allowing specialists based in tertiary centers to interpret scans performed at distant locations. As healthcare systems prioritize decentralization and equitable access, vendors offering flexible, mobile, and shared-service imaging solutions are well-positioned to capture emerging demand across expanding regional networks.?

Category-wise Analysis

By Product Type Insights

High-range slice scanners (<64 slices) are projected to hold the largest share of the PET/CT systems market in 2025, contributing roughly 57%. These systems deliver faster acquisition speeds, broader anatomical coverage, and improved temporal resolution, which are essential for oncology staging, complex treatment planning, and high-throughput diagnostic workflows.

Their ability to visualize small lesions with greater clarity supports more accurate disease assessment, particularly in cancers requiring whole-body imaging. Many high-range models also incorporate advanced features such as ultra-low-dose imaging, iterative reconstruction techniques, and metal artifact reduction, enabling clinicians to achieve high-quality scans while minimizing radiation exposure.

Because leading cancer institutes and academic hospitals often manage large patient volumes and diverse clinical indications, they prefer systems capable of supporting multi-organ protocols in a single session. As hybrid applications like PET/CT angiography, cardiac perfusion imaging, and therapy response monitoring continue to expand, the demand for high-performance, high-range scanners remains strong, reinforcing their dominant market position.

By Isotope Insights

Fluorodeoxyglucose (FDG) continues to dominate PET/CT utilization worldwide, accounting for more than 70% of annual PET scan volumes. Its capability to map glucose metabolism makes it indispensable for evaluating a wide range of tumors, inflammatory conditions, and certain neurologic disorders.

Because FDG is included in numerous global clinical guidelines for diagnosis, staging, and treatment response assessment, it remains the primary tracer used in routine oncologic imaging. National audits, including those from Canada and Europe, consistently show that FDG-based oncology scans form the bulk of PET/CT procedures, underscoring its deep integration into standard care pathways.

Although new isotopes such as Gallium-68 PSMA, Gallium-68 DOTA derivatives, and emerging fluorinated tracers are gaining momentum particularly in prostate cancer, neuroendocrine tumors, and targeted Theranostics they currently serve specialized applications rather than replacing FDG.

As a result, PET/CT system configurations, dose management protocols, and workflow designs continue to be optimized around FDG, preserving its central role in clinical and operational decision-making.

Region-wise Insights

North America PET/CT Systems Market Trends

The North American PET/CT systems market continues to advance on the back of strong adoption of hybrid imaging for oncology, cardiology, and neurology applications. Hospitals and diagnostic centers across the U.S. and Canada are steadily upgrading older scanners to high-slice, low-dose platforms that support faster throughput and improved lesion detectability.

This shift is reinforced by an increasing clinical emphasis on early cancer detection, precision therapy planning, and quantitative imaging for treatment response assessment. Health systems are also integrating digital detector technologies, motion-correction tools, and AI-enabled reconstruction software to enhance workflow efficiency and reduce scan times.

The presence of well-established radiopharmacies and expanding access to tracers beyond FDG further strengthens utilization. Transition toward outpatient imaging centers, value-based care models, and reimbursement support for advanced PET procedures continue to sustain demand.

Academic institutions and research networks in the region actively drive clinical innovation, contributing to early adoption of new PET tracers and hybrid modalities. Overall, North America remains a mature but steadily progressing market focused on technology replacement, performance optimization, and expanding the clinical scope of PET/CT imaging.

Asia and Pacific PET/CT Systems Market Trends

Asia Pacific PET/CT systems market is experiencing strong growth as healthcare systems expand diagnostic imaging capacity and invest in advanced cancer management pathways. Rising cancer incidence across India, China, South Korea, and Southeast Asian countries has increased demand for accurate staging and early detection, pushing hospitals to adopt modern hybrid imaging systems.

Governments and private providers are upgrading radiology infrastructure, particularly in metropolitan and tier-2 cities, to meet the growing volume of oncology and cardiology cases. The region is also seeing a broader rollout of cyclotrons and radiopharmacies, improving access to PET tracers and reducing dependency on imported isotopes.

Adoption of high-slice scanners is increasing as clinicians prioritize better resolution, shorter scan times, and improved sensitivity for small-volume disease. Training programs in nuclear medicine and partnerships with global imaging companies are helping enhance clinical expertise and service standards.

Meanwhile, mobile PET/CT units and shared-service models are gaining traction in countries aiming to extend hybrid imaging to underserved regions. Overall, Asia Pacific remains one of the fastest-growing markets, driven by rising healthcare investment, expanding patient pools, and increasing focus on advanced diagnostic technologies.

Competitive Landscape

The PET/CT systems market features strong competition among global imaging leaders, regional manufacturers, and specialized technology developers. Established companies such as GE HealthCare, Siemens Healthineers, and Philips dominate through broad portfolios, digital detector platforms, and continuous software innovation.

These firms compete with image quality, workflow efficiency, low-dose capabilities, and wide service networks. Emerging players from Asia are gradually strengthening their presence by offering cost-effective systems and localized support.

Collaborations with radiopharmacies, hospitals, and research centers help vendors expand tracer access, strengthen clinical validation, and support training programs. Product differentiation increasingly centers on high-slice scanners, AI-enabled reconstruction, and compact designs suited for outpatient centers, creating a dynamic and innovative-driven competitive environment.

Key Industry Developments:

- In February 2024, United Imaging Healthcare Europe, a major producer of advanced imaging and radiation systems, introduced its first mobile digital PET/CT unit in Italy.

- In December 2023, Ascension St. John in Tulsa introduced the first fully digital, transportable PET/CT system.

Companies Covered in PET/CT Systems Market

- Siemens AG

- General Electric Company

- Koninklijke Philips N.V.

- Hitachi, Ltd.

- Canon Inc.

- Neusoft Corporation

- MinFound Medical Systems Co., Ltd

- Mediso Ltd.

- Bruker Corporation

- MR Solutions

- Others

Frequently Asked Questions

The global PET/CT systems market is projected to be valued at US$ 3.1 Bn in 2026.

The rise in prevalence of cancer, growing demand for early diagnosis, technological advances, and expanding applications in cardiology and neurology drive PET/CT adoption.

The global PET/CT systems market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Growing preference for hybrid imaging, rising investment in precision medicine, and expanding access in emerging regions create strong growth opportunities.

North America is the leading region in the global PET/CT systems market.