- Animal Feed & Additives

- Pet Food Market

Pet Food Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Pet Food Market by Product (Wet Pet Food, Dry Pet Food, Treats & Snacks, and Toppers & Mixers), by Pet Type (Dogs, Cats, and Others), by Ingredient (Animal Derived Ingredients, Plant Derived Ingredients, and Synthetic Additives) by Distribution Channel (Hypermarkets, Specialty Pet Stores, Veterinary Clinics, Convenience Stores, Online Retail, and Others), and Regional Analysis from 2026 - 2033

Pet Food Market Share and Trend Analysis

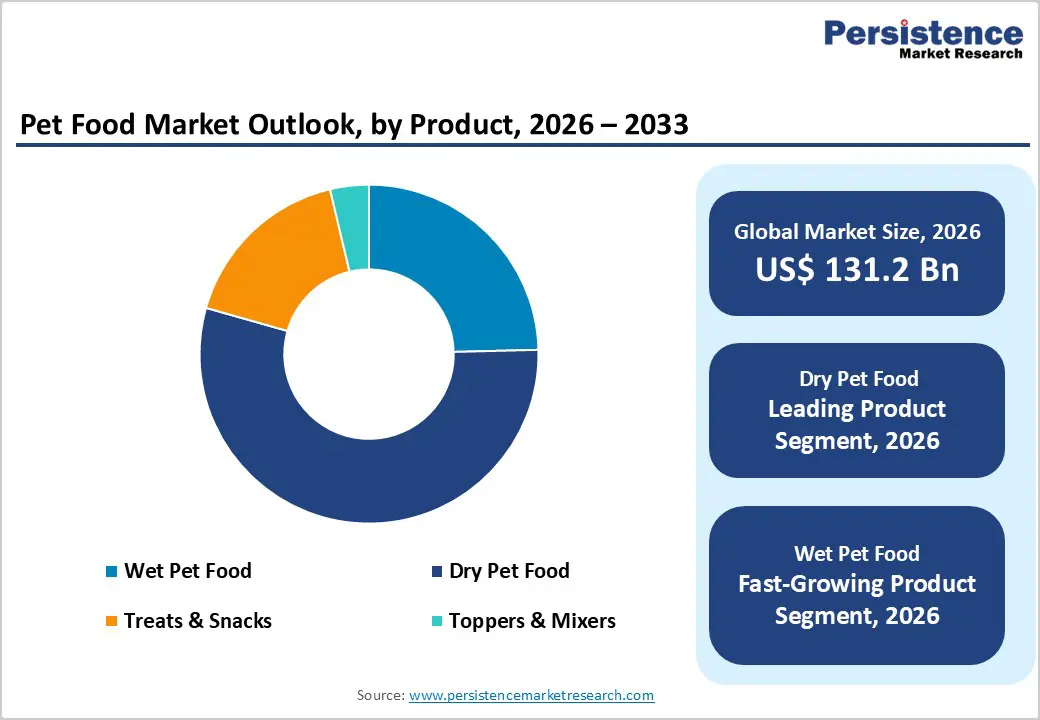

The global pet food market size is estimated to grow from US$ 131.2 billion in 2026 to US$ 215.5 billion by 2033. The market is projected to grow at a CAGR of 5.6% from 2026 to 2033. Growing global interest in companion animal care is steadily strengthening demand for nutritionally balanced pet food, supported by rising pet ownership and a clear shift toward health-focused feeding practices. Pet owners increasingly prioritize scientifically formulated diets that support digestion, immunity, mobility, and overall vitality rather than relying on traditional home feeding. Greater awareness of preventive pet healthcare, combined with veterinary guidance and digital access to nutrition information, is encouraging consistent use of commercial pet food products.

Expanding availability through supermarkets, specialty pet stores, veterinary clinics, and rapidly growing online platforms is improving accessibility across both developed and emerging economies. Urban lifestyles and higher disposable incomes are also supporting premium product adoption, including natural, grain-free, and functional formulations. Continuous advancements in ingredient quality, palatability enhancement, safety standards, and life-stage nutrition are improving consumer confidence and repeat purchasing behavior. Increasing spending on companion animals, coupled with innovation in personalized nutrition and subscription-based delivery models, continues to reinforce long-term industry expansion worldwide.

Key Industry Highlights:

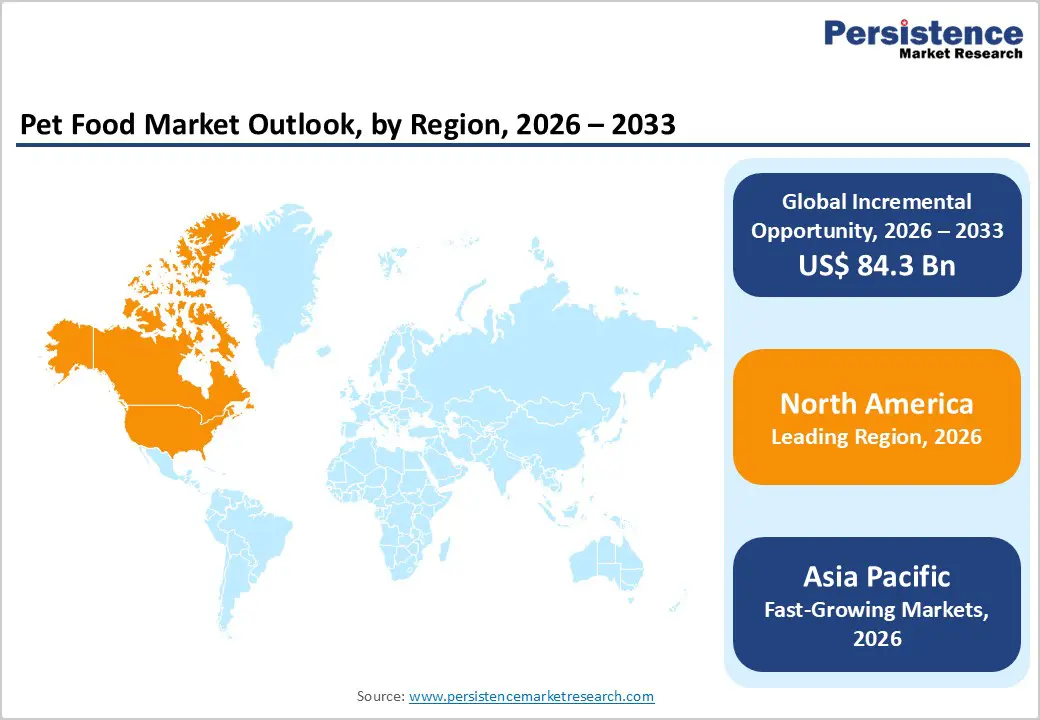

- Leading Region: North America accounts for 46.7% of global revenue, supported by high pet ownership, strong premiumization trends, advanced veterinary awareness, mature retail infrastructure, and well-established e-commerce penetration.

- Fastest-Growing Region: Asia Pacific is expanding most rapidly due to urbanization, rising middle-class income, increasing pet adoption, and improving access to organized retail and digital purchasing platforms.

- Leading Product Segment: Dry pet food leads the market owing to feeding convenience, longer shelf life, affordability, and suitability for daily nutrition routines.

- Fastest-Growing Product Segment: Wet pet food is witnessing accelerated growth as owners increasingly seek higher palatability, hydration benefits, and premium feeding experiences.

- Leading Ingredient Segment: Animal derived ingredients hold the largest share due to superior protein quality, digestibility, and alignment with natural dietary requirements of pets.

- Fastest-Growing Ingredient Segment: Plant derived ingredients are gaining traction as sustainability concerns and demand for alternative protein sources continue to rise among health-conscious pet owners.

| Key Insights | Details |

|---|---|

|

Pet Food Market Size (2026E) |

US$ 131.2 Bn |

|

Market Value Forecast (2033F) |

US$ 215.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6 % |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4 % |

Market Dynamics

Driver - Rising Pet Humanization and Nutrition-Focused Feeding Behavior

A fundamental transformation in pet ownership attitudes is reshaping purchasing behavior worldwide, with companion animals increasingly regarded as integral family members rather than household animals. This emotional shift is directly influencing feeding decisions, encouraging owners to prioritize nutritional quality, ingredient transparency, and long-term health benefits. Growing awareness around preventive pet healthcare has accelerated demand for balanced diets formulated to support digestion, immunity, joint mobility, and coat health. Veterinary recommendations and expanding access to pet health information through digital platforms are further reinforcing informed purchasing patterns.

Urban lifestyles and smaller family structures are also contributing to higher emotional attachment to pets, translating into increased spending on premium and specialized nutrition. Consumers are moving away from table scraps and unstructured feeding toward scientifically formulated commercial products designed for specific breeds, life stages, and health conditions. Additionally, rising adoption among millennials and younger households who tend to favor premium, natural, and ethically sourced products is strengthening value growth. Continuous product innovation, improved availability through organized retail, and subscription-based online purchasing models are collectively accelerating consistent consumption and supporting sustained expansion across developed and emerging markets.

Restraints - Cost Sensitivity, Ingredient Volatility, and Trust Barriers

The major constraint relates to fluctuating raw material prices, particularly animal protein sources such as poultry, fish, and meat derivatives, which significantly impact production costs and profit margins. Supply chain disruptions, regulatory compliance requirements, and quality certification standards further increase operational complexity for manufacturers. Premium pet food products often carry higher price points, limiting adoption among price-sensitive consumers, especially in developing economies where homemade feeding practices remain common.

Another limiting factor involves consumer skepticism surrounding ingredient claims and marketing terminology. Confusion around labels such as “natural,” “grain-free,” or “holistic” can create uncertainty regarding actual nutritional benefits. Product recalls or safety concerns within the broader industry occasionally weaken consumer confidence, emphasizing the importance of transparency and traceability. Additionally, balancing nutritional performance with palatability remains technically challenging, as pets may reject formulations optimized solely for health benefits. Retail competition and shelf congestion also make differentiation difficult for newer brands. These combined pressures require companies to invest heavily in quality assurance, education initiatives, and pricing strategies to sustain long-term consumer trust.

Opportunity - Premiumization, Functional Nutrition, and Emerging Market Expansion

Shifting consumer priorities are creating substantial opportunities for innovation and category diversification within pet nutrition. Demand is increasingly moving toward functional formulations that address specific health outcomes, including digestive wellness, weight control, cognitive support, and age-related conditions. Advances in ingredient science are enabling incorporation of probiotics, omega fatty acids, and novel proteins while maintaining product stability and taste acceptance. Fresh, freeze-dried, and minimally processed formats are gaining traction as owners seek diets perceived as closer to natural feeding patterns.

Rapid urbanization and rising disposable incomes across emerging economies are expanding the addressable consumer base, particularly as awareness regarding pet health continues to improve. Manufacturers are leveraging localized production, regionally adapted flavors, and smaller pack sizes to improve affordability and accessibility. Digital commerce presents another strong growth avenue, allowing brands to engage directly with consumers through personalized recommendations, subscription delivery, and data-driven marketing. Sustainability initiatives, including responsibly sourced ingredients and recyclable packaging, are also becoming important purchase drivers among younger consumers. Together, these developments position the industry for long-term value creation through differentiated nutrition solutions and evolving lifestyle alignment.

Category-wise Analysis

By Product, Dry Pet Food Leads Due to Feeding Convenience and Cost Efficiency

The dry pet food segment is projected to dominate the global pet food market in 2026, capturing a revenue share of 54.8%. This leadership is primarily driven by its convenience, longer shelf life, and cost effectiveness compared to wet alternatives. Dry formulations support easy storage, bulk purchasing, and portion control, making them highly preferred among multi-pet households. Kibble products also contribute to dental health benefits and consistent daily feeding routines. Manufacturers favor dry formats due to efficient large-scale production and easier incorporation of functional nutrients such as vitamins, minerals, and probiotics. Continuous innovation in high-protein, grain-free, and life-stage-specific formulations further strengthens segment dominance globally.

By Ingredient, Animal-Derived Ingredients Lead Due to Nutritional Value and Palatability

The animal-derived ingredients segment is expected to lead the global pet food market in 2026, accounting for a 74.3% revenue share. Meat-based proteins remain essential due to their superior amino acid profile, digestibility, and strong palatability preferred by pets. Ingredients such as poultry, beef, fish, and lamb provide balanced nutrition aligned with natural dietary requirements. Pet owners increasingly associate animal protein with higher quality and improved health outcomes, supporting premium product adoption. From a manufacturing perspective, animal ingredients enable formulation of specialized diets targeting muscle development, skin and coat health, and overall vitality. Growing demand for high-protein and biologically appropriate diets continues to reinforce segment leadership worldwide.

By Distribution Channel, Hypermarkets Lead Due to High Product Visibility and Consumer Accessibility

Hypermarkets are projected to dominate the global pet food market in 2026, capturing a 41.6% revenue share. The channel benefits from extensive shelf availability, strong brand visibility, and high consumer footfall, enabling comparison across multiple brands and price tiers. Bulk purchasing options and promotional discounts encourage repeat purchases among pet owners. Hypermarkets also support both premium and economy product placement, ensuring broad consumer reach. For manufacturers, these retail formats provide consistent sales volumes and strong geographic penetration across urban and suburban markets. Although online retail is expanding rapidly, hypermarkets remain the primary purchase point for routine pet food buying globally.

Regional Insights

North America Pet Food Market Trends

North America is expected to dominate the global pet food market in 2026, accounting for a 46.7% value share, led primarily by the United States. The region benefits from one of the highest pet ownership rates globally, supported by strong pet humanization trends where pets are increasingly viewed as family members. This behavioral shift drives sustained demand for premium, natural, and functional pet nutrition products, including grain-free, high-protein, and veterinary therapeutic diets. Consumers demonstrate strong willingness to spend on specialized nutrition addressing weight management, digestive health, and age-specific dietary needs. Advanced veterinary infrastructure and widespread availability of specialty pet retailers further strengthen adoption.

Additionally, well-developed e-commerce ecosystems and subscription-based purchasing models support recurring sales and brand loyalty. Major manufacturers maintain strong innovation pipelines focused on fresh food, personalized nutrition, and clean-label formulations, supported by robust R&D investments. High disposable income levels and regulatory clarity around ingredient standards continue to reinforce North America’s long-term leadership in both value and innovation.

Europe Pet Food Market Trends

Europe represents a mature yet steadily expanding pet food market driven by strict regulatory standards, sustainability priorities, and rising consumer awareness regarding pet health and nutrition. Key markets such as Germany, United Kingdom, France, and Italy demonstrate strong adoption of premium and organic pet food products. European consumers prioritize ingredient transparency, ethical sourcing, and environmentally responsible packaging, encouraging manufacturers to invest in clean-label and sustainable formulations. Regulatory oversight ensures high product quality and safety, strengthening consumer trust in branded offerings.

Growth is further supported by increasing demand for functional nutrition addressing allergies, digestive sensitivity, and mobility health among aging pets. Private-label premium offerings by supermarket chains are expanding accessibility while maintaining affordability. Online pet specialty platforms and subscription delivery services are gaining traction, complementing traditional retail channels. Continued innovation in natural ingredients and eco-friendly packaging positions Europe as a stable, innovation-driven regional market.

Asia Pacific Pet Food Market Trends

The Asia Pacific pet food market is projected to register the fastest growth, expanding at a CAGR of approximately 7.6% between 2026 and 2033. Rapid urbanization, increasing disposable income, and changing lifestyles across China, India, Japan, and South Korea are significantly accelerating companion animal adoption. Younger urban populations increasingly prefer commercially prepared pet food over traditional homemade feeding practices, supporting market formalization. Expansion of organized retail, pet specialty chains, and fast-growing e-commerce platforms is improving accessibility to premium and international brands.

Manufacturers are investing in localized production facilities and region-specific product formulations to match taste preferences and price sensitivity. Social media influence, rising veterinary awareness, and education around balanced pet nutrition are encouraging premiumization trends. Government support for food processing and growing investments in supply chain infrastructure further enhance market scalability, positioning the Asia Pacific as the primary future growth engine for the global pet food industry.

Competitive Landscape

The global pet food market is highly competitive, with strong participation from SCHELL & KAMPETER, INC., Mars, Incorporated, Nestlé, Allanasons Pvt Ltd, Champion Petfoods USA, Inc, and United Petfood. These players leverage extensive retail and e-commerce distribution networks, strong brand equity, and continuous innovation in ingredient sourcing, nutritional formulation, palatability enhancement, and product safety to meet evolving pet nutrition demands.

Rising pet humanization, increasing awareness of balanced diets, and premium feeding trends are accelerating market growth. Manufacturers are focusing on high-protein recipes, functional nutrition, natural ingredients, and specialized diets while expanding online channels, entering emerging markets, and strengthening R&D to deliver health-focused and premium pet food solutions.

Key Industry Developments:

- In February 2026, Colgate-Palmolive announced its agreement to acquire the Prime100 pet food brand to strengthen its presence in the premium pet nutrition segment. The acquisition is expected to expand the company’s portfolio of specialized and veterinarian-recommended pet food products while supporting growth in high-value fresh and functional pet diets.

- In February 2026, Freshpet, Inc., announced that its complete product portfolio across the United States and Canada received the Clean Label Project™ Purity Award, recognizing high standards in ingredient quality and safety. The certification, granted by the nonprofit Clean Label Project™, evaluates products for hidden contaminants such as heavy metals, pesticides, and environmental toxins not typically disclosed on labels.

- In May 2024, Nestlé Purina announced an investment of CHF 200 million to expand its pet food manufacturing facility in Silao, Mexico. The project includes installing an additional production line for wet pet food and another for dry pet food, which will position the site as the largest pet food manufacturing plant in Latin America.

Companies Covered in Pet Food Market

- SCHELL & KAMPETER, INC.

- Mars, Incorporated

- Nestlé

- Allanasons Pvt Ltd

- Champion Petfoods USA, Inc

- United Petfood

- Nestlé Purina

- General Mills Inc.

- Wellness Pet, LLC

- Orange Pet Nutrition Pvt Ltd

- Hill's Pet Nutrition, Inc.

- Midwestern Pet Foods.

- BARRETT PETFOODS

- freshpet

- NGP Good Petfood

- Others

Frequently Asked Questions

The global pet food market is projected to be valued at US$ 131.2 Bn in 2026.

Rising pet ownership and pet humanization, increasing awareness of pet nutrition, premiumization trends, and rapid expansion of e-commerce and modern retail channels are the primary drivers accelerating global pet food demand.

The global pet food market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Growth opportunities lie in premium and functional nutrition, natural/organic formulations, sustainable ingredient innovations, capacity expansion by manufacturers, and subscription-based and online distribution models targeting evolving pet care spending.

SCHELL & KAMPETER, INC., Mars, Incorporated, Nestlé, Allanasons Pvt Ltd, Champion Petfoods USA, Inc, and United Petfood are some of the key players in the pet food market.