- Industrial Machinery

- North America Water Pump Market

North America Water Pump Market Size, Share, and Growth Forecast, 2026 - 2033

North America Water Pump Market by Power Source (Electric Pumps, Engine-Driven Pumps.), Pump Outlet Size (Up to 1 Inch, 1-2 Inches, 2-4 Inches, 4-6 Inches, Above 6 Inches.), Volume Flow Rate (Up to 500 GPM, 500-1000 GPM, 1000-3000 GPM, Above 3000 GPM.), Pump Type (Centrifugal Pump, Positive Displacement Water Pump), Sales Channel (OEM, Aftermarket ), End-user (Construction, Agriculture, Oil & Gas, Wastewater Treatment, Chemical, Mining, Power Generation, Food & Beverage, Misc.) and Regional Analysis for 2026 - 2033

North America Water Pump Market Size and Trends Analysis

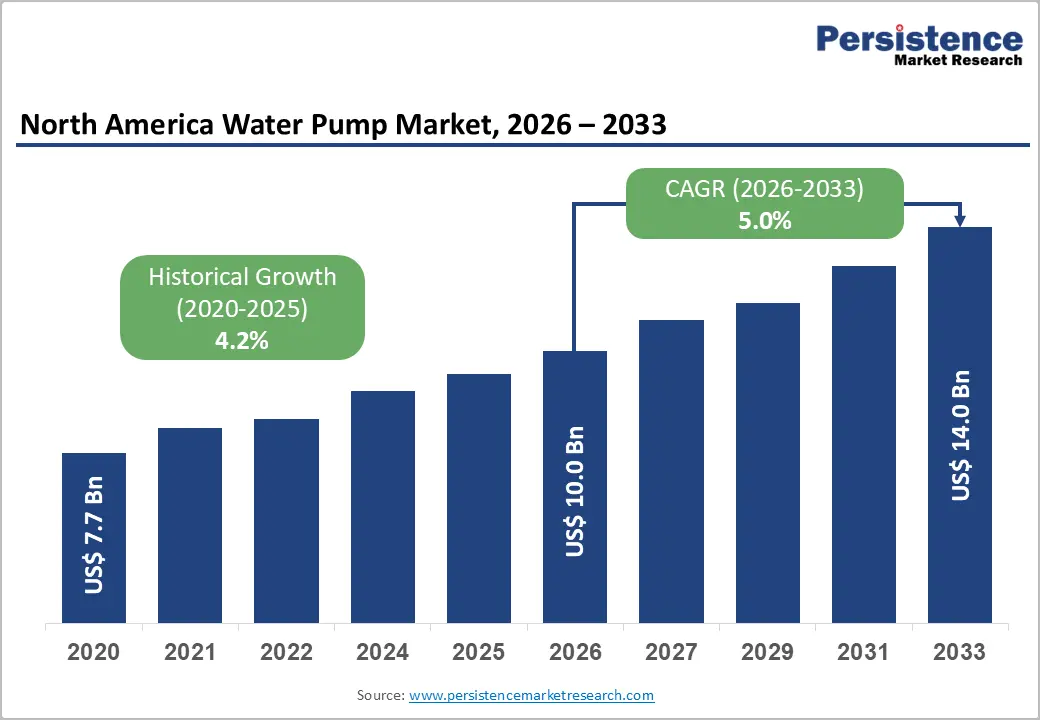

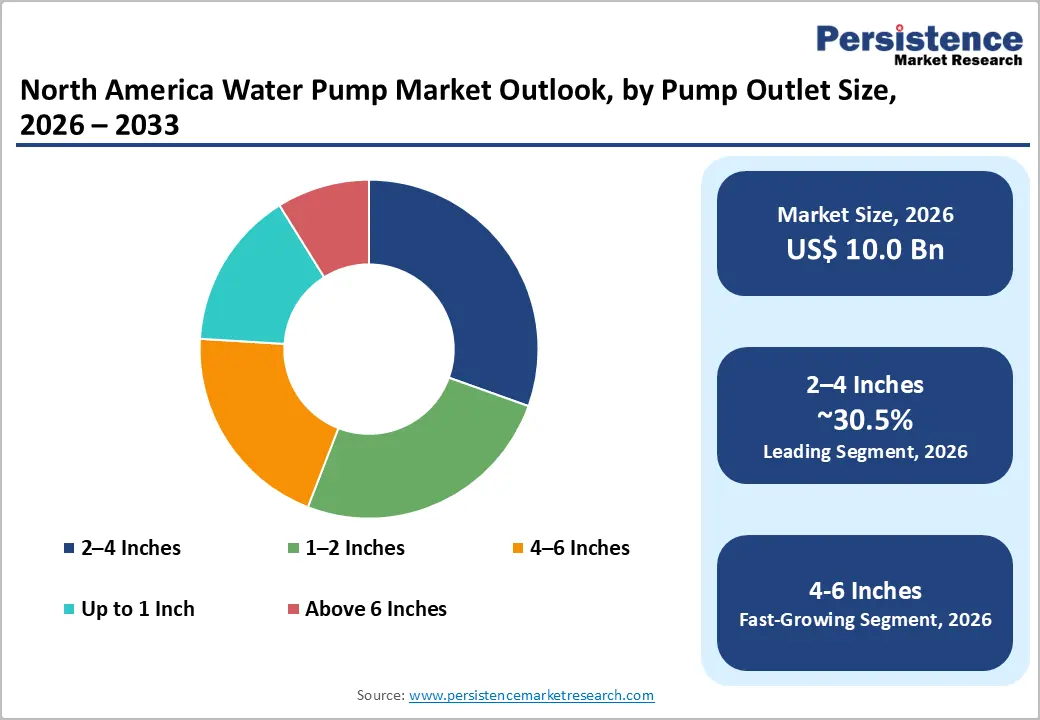

The North America water pump market size was valued at US$ 10.0 billion in 2026 and is projected to reach US$ 14.0 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033. This market expansion reflects the region's commitment to infrastructure modernisation, stringent environmental regulations, and accelerating adoption of energy-efficient pumping solutions.

Primary growth catalysts include substantial government infrastructure investments totalling over US$ 50 billion allocated through the Bipartisan Infrastructure Law for water systems modernisation, evolving regulatory frameworks such as EPA's PFAS drinking water standards affecting approximately 6,000 to 7,000 utilities, and sustained demand from oil and gas operations where North America maintains production levels exceeding 13 million barrels per day. The market benefits from diverse end-use applications ranging from municipal water treatment to agricultural irrigation, with construction and wastewater treatment segments representing critical revenue drivers in the region's economic infrastructure

Key Industry Highlights:

- Leading Regional Market: The U.S. dominates the North America Water Pump Market, driven by large municipal CAPEX cycles and southern states such as Texas and Florida accounting for nearly 44% of total water infrastructure spending.

- High-Value Leading Power Source: Electric pumps lead with 73 percent share, supported by EPA emissions standards, DOE efficiency mandates, and rapid VFD-based digitalisation across municipal and industrial assets.

- Leading Pump Type: Centrifugal pumps remain the dominant technology, with a 61% market share, supported by deep municipal installed bases and standardized compatibility across treatment, distribution, and industrial processes.

- Fastest-Growing End-user: Oil & gas applications are the fastest-growing end-use, driven by shale basin development, produced water management, and high-pressure fluid-handling requirements.

- Leading End-user: Construction is the largest end-use segment, with a 24 Percent share, driven by infrastructure modernisation, residential housing starts, and federally supported civil engineering expansion.

| North America Market Attributes | Key Insights |

|---|---|

| Water Pump Market Size (2026E) | US$ 10.0 Bn |

| Market Value Forecast (2033F) | US$ 14.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Drivers - Infrastructure Modernisation and Federal Investment Mandate

The U.S. water and wastewater infrastructure sector faces an unprecedented modernisation imperative driven by ageing assets and regulatory compliance requirements. The American Society of Civil Engineers assigned a D+ grade to drinking water infrastructure, requiring US$114 billion in investments by 2030 to replace deteriorating pipelines and enhance pumping capacity across American cities.

The Bipartisan Infrastructure Law catalyzes this transformation by allocating US$ 50 billion exclusively for water infrastructure projects, while the U.S. municipal capital expenditure for water and wastewater treatment infrastructure is projected to total around US$ 515 billion through 2035, growing at a CAGR of 4 to 5 percent from US$ 37 billion to US$ 58-60 billion annually. Wastewater treatment represents 58 percent of this investment of US$ 310.4 billion, while drinking water investment totals US$ 214 billion, with approximately 80 percent dedicated to upgrades and rehabilitation of existing treatment systems. This massive capital allocation directly expands demand within the North America Water Pump Market, as municipalities and utilities require advanced pumping solutions capable of meeting enhanced efficiency standards, handling increased throughput, and integrating with modernised treatment technologies.

Mid-sized utilities serving populations of 25,000 to 100,000 are the optimal market segment, as they have sufficient capital and require scalable, cost-effective solutions. Geographic concentration in the southern U.S. Texas and Florida account for 44% of total spend, and accelerated investment in smaller states where ageing infrastructure converges with regulatory pressures creates localised pump demand spikes that favour regional manufacturers and specialised solution providers.

PFAS Regulatory Compliance and Drinking Water Quality Standards

The Environmental Protection Agency's finalisation of the National Primary Drinking Water Regulation for per- and polyfluoroalkyl substances (PFAS) on April 10, 2024, establishes the first legally enforceable drinking water standards for six PFAS chemicals, including PFOA and PFOS at 4 parts per trillion, and PFNA, PFHxS, HFPO-DA, and PFBS at 10 parts per trillion. This regulatory action directly stimulates demand in the North American Water Pump Market by compelling 6 to 10 percent of the 66,000 covered public drinking water systems to implement advanced treatment solutions, thereby protecting approximately 100 million Americans from PFAS exposure.

Public water utilities face a three-year compliance timeline for initial monitoring and a five-year implementation deadline for treatment systems, creating an urgent capital expenditure cycle. Advanced treatment technologies such as granular activated carbon filtration, ion exchange resins, and reverse osmosis systems require specialised high-performance pumps capable of handling elevated pressures and complex fluid dynamics. Xylem's introduction of the MitiGATOR Mobile System in collaboration with Evoqua in April 2024 exemplifies the technological response to this regulatory mandate, offering utilities flexible treatment solutions without requiring extensive permanent infrastructure modifications.

The combined effect of PFAS compliance costs, revised Lead and Copper Rule thresholds, and emerging contaminant regulations creates a multi-year revenue stream for pump manufacturers specialising in municipal water treatment applications within the North America Water Pump Market, with utilities prioritising equipment that exceeds baseline compliance to ensure long-term resilience.

Restraint - Regulatory Complexity and Compliance Cost Burden

Manufacturers and distributors within the North America Water Pump Market face escalating regulatory complexity stemming from federal EPA standards, state-level environmental regulations, and municipal-specific requirements. The U.S. Department of Energy pump efficiency standards, taking effect in 2020 and subsequent enhancements, mandate that all commercial pump designs exceed baseline efficiency thresholds, necessitating substantial R&D investments in hydraulic optimization and advanced materials.

The proliferation of emerging regulations, including PFAS drinking water standards, revised Lead and Copper Rule compliance thresholds, stormwater management mandates, and state-specific contaminant monitoring requirements, fragments the market into specialised application niches requiring customised pump solutions. Utilities and industrial operators must navigate multi-layered compliance frameworks that vary by jurisdiction, delaying capital procurement timelines and creating uncertainty in demand forecasting. These regulatory burdens particularly affect smaller manufacturers, which lack the resources for extensive product certification and testing, thereby concentrating market share among multinational corporations capable of absorbing compliance costs.

Opportunity - Renewable Energy Integration and Decarbonization Infrastructure

Accelerating global energy transition initiatives creates specialized pump market opportunities within solar-powered agricultural systems, geothermal HVAC applications, biogas production facilities, hydrogen hub infrastructure, and district heating networks. The U.S. Department of Energy's US$7 billion hydrogen hub grant program establishes development corridors across North America, requiring cryogenic pumps, high-pressure fluid transfer systems, and specialised equipment for hydrogen production, compression, and liquefaction. Flowserve's June 2022 contract award to supply pumps for TMGcore's liquid immersion cooling systems demonstrates emerging demand within data centre cooling applications, where energy-efficient pump solutions address the cooling requirements of advanced artificial intelligence, machine learning, and high-performance computing infrastructure

The North American water pump market captures a portion of renewable energy infrastructure investment through agricultural applications, where solar-powered submersible pumps support irrigation in water-scarce regions, reducing reliance on grid electricity and aligning with sustainability objectives.

Green building certifications and net-zero energy mandates drive the adoption of high-efficiency circulating pumps in HVAC systems, creating replacement demand for legacy equipment. Manufacturers investing in specialised cryogenic pump technology, magnetic bearing systems, and materials capable of withstanding novel operating conditions position themselves advantageously within this emerging opportunity segment.

Wastewater Reuse and Circular Water Economy Development

Water scarcity across North America, intensified by regional droughts, particularly in western states, catalyses investment in wastewater recycling, reclamation, and reuse infrastructure. Industrial facilities increasingly implement on-site wastewater treatment and recycling systems to reduce freshwater consumption, lower municipal sewer fees, and demonstrate environmental stewardship, creating demand for specialised pumps capable of handling treated effluent and managing variable water quality within recycled water systems. Municipalities develop advanced water recycling programs to augment supply during drought periods, which require pumps designed for non-potable applications, including landscape irrigation, industrial cooling, toilet flushing, and aquifer recharge injection.

The North American Water Pump Market benefits from this transition to circular water economy models, as utilities and facility managers require a diverse range of pump types optimised for distinct recycled water applications. Expanding desalination infrastructure, driven by increasing coastal drought severity in California and the Southwest, creates demand for high-pressure reverse osmosis feed pumps and brine disposal systems. Mid-sized water utilities represent the "sweet spot" for this opportunity, as they have sufficient scale to justify advanced treatment and recycling investments while remaining flexible enough to adopt innovative solutions without legacy-system constraints.

Category-wise Analysis

Power Source Insights

Electric Pumps, holding share of 72.9% dominate the North America water pump market, reflecting regulatory preferences for zero-emission municipal equipment, operational simplicity, and declining electricity costs relative to diesel fuel. The prevalence of electric pumps across municipal water supply systems, with over 150,000 public water systems in the United States relying predominantly on centrifugal pumps for distribution, establishes electric drive technology as the infrastructure standard.

Regulatory mandates from the U.S. Environmental Protection Agency requiring reductions in emissions from municipal equipment and state-level air quality standards reinforce the adoption of electric pumps. Industrial applications in chemical processing, food and beverage production, and wastewater treatment similarly favor electric motors for their precise speed control, compatibility with variable frequency drives, and integration with modern process automation systems. The installed base of electric pumps across North America creates substantial aftermarket opportunities for replacement equipment, spare parts, and retrofit solutions as legacy pumps reach end-of-life.

Engine-driven pumps, which use internal combustion engines for power generation, constitute the fastest-growing segment within the power source category, driven by applications requiring portability, rapid deployment, and independence from electrical grid infrastructure. Construction site dewatering operations, emergency flood-response scenarios, temporary water-supply systems for remote agricultural operations, and mining activities are primary demand drivers for engine-driven pump solutions.

Pump Type Insights

Centrifugal pumps maintain market dominance, accounting for 61.1% of the North America Water Pump Market in 2026, driven by their high volumetric flow capacity, operational simplicity, cost-effectiveness, and suitability for low-to-moderate pressure applications characteristic of municipal water supply and wastewater treatment infrastructure.

The prevalence of centrifugal technology across public water systems reflects decades of proven reliability, extensive spare parts availability, and the presence of skilled technicians capable of servicing and maintaining this established equipment category. End-suction and split-case centrifugal pump designs are the architectural standards for municipal applications, with manufacturers maintaining extensive product portfolios that address diverse flow-rate and pressure requirements.

Xylem's joint venture manufacturing facility, established in Cairo, Egypt, and inaugurated in May 2023 in collaboration with Tiba Manzalawi Group, represents strategic capacity expansion for centrifugal pump production serving irrigation, HVAC, commercial building services, and industrial applications across the broader regions, demonstrating continued investment in centrifugal technology platforms despite industry-wide digitalization trends.

Agricultural irrigation applications, particularly for flood irrigation and surface water source development, rely extensively on centrifugal pump designs because of their capacity to handle large water volumes at variable discharge heads. Industrial applications in chemical processing, power generation, and mineral processing utilise centrifugal pumps for process fluid circulation, cooling system operation, and product transfer. The market maturity of centrifugal pump technology, combined with the established supplier ecosystem and component availability, creates barriers to displacement by alternative technologies, preserving market dominance for this segment within the North America Water Pump Market.

Positive displacement pumps represent the fastest-growing technology category within the North American Water Pump Market, expanding at approximately a 6.5 percent CAGR, driven by the expansion of precision agriculture, growth in pharmaceutical manufacturing, chemical processing automation, and specialised high-pressure applications requiring metering accuracy and viscous-fluid handling. Positive displacement pump designs, including gear pumps, screw pumps, peristaltic pumps, and progressive-cavity configurations, deliver constant volumetric flow rates independent of pressure variations, making them ideal for applications requiring precise flow control, accurate chemical dosing, and reliable performance with high-viscosity fluids.

End-user Insights

Construction applications represent the largest end-use category within the North America water pump market, commanding 24.0% market share in 2026, driven by dewatering requirements, concrete pumping operations, temporary water supply systems, and material transfer functions essential to civil engineering and building development projects. The U.S. construction sector's economic contribution of US$ 2.2 trillion annually, representing 4.5 percent of gross domestic product, combined with employment of over 8.2 million workers across 3.7 million construction businesses, establishes construction as a substantial demand driver for portable and high-capacity pumping equipment.

Residential construction, buoyed by 1.6 million new housing starts in 2024 and ongoing suburban development, creates recurring demand for site dewatering pumps managing groundwater infiltration at excavation sites. Commercial real estate development, including data centres, office buildings, and retail infrastructure, requires temporary pumping systems for foundation work and site preparation. Infrastructure projects funded through the Bipartisan Infrastructure Law, encompassing roadway, bridge, rail, and utility expansion, generate sustained demand for specialised construction pumps capable of managing high-flow dewatering requirements over extended project timelines. Mining and tunnelling operations utilise construction pump systems for groundwater control and material slurry transfer.

Oil and gas operations constitute the fastest-growing end-use segment in the North American Water Pump Market, driven by sustained crude oil production, produced water management requirements, and enhanced recovery operations. The U.S. oil and gas industry's capital investment, exceeding US$ 50 billion allocated to new projects annually, particularly concentrated in shale formations including the Permian Basin, Eagle Ford Shale, and Marcellus Shale, creates ongoing demand for specialised pumping equipment capable of managing extreme pressure conditions, corrosive fluid streams, and remote operational environments.

Competitive Landscape

The North America water pump market exhibits a moderately consolidated competitive landscape, characterized by a mix of large North America OEMs with significant market share and numerous regional and niche specialists competing in specific end-use segments. Leading multinational players such as Xylem Inc., Flowserve Corporation, Grundfos, Ingersoll Rand Inc., Sulzer AG, and Wilo SE dominate the market through extensive distribution networks, broad product portfolios, and strong brand recognition across industrial, municipal, commercial, and residential water pumping applications. These established incumbents leverage strategic acquisitions, partnerships, and region-specific manufacturing investments to strengthen their market positions and respond to rising demand for energy-efficient, digitally enabled pumping solutions.

Smaller regional manufacturers and speciality technology providers retain meaningful presence in targeted niches such as dewatering, booster systems, wastewater handling, and submersible pumps, where local service responsiveness and customisation are valued. Competitive dynamics are also shaped by increasing regulatory emphasis on sustainability, water infrastructure modernisation, and energy usage standards, prompting players to innovate with smart, IoT-enabled, and high-efficiency products. As a result, while a handful of large firms influence overall market direction, fragmentation persists at sub-segment levels, and competition remains robust on price, performance, and service quality.

Key Industry Developments:

- In October 2024, Franklin Electric Co., Inc. has announced the realignment of Headwater Companies' Engineered Systems facility in Abernathy, Texas, into its North America Water Systems segment. This strategic move aims to bolster Franklin Electric’s investment in water systems product innovation, leveraging 84,000 sq. ft. state-of-the-art manufacturing and testing facility. The realignment consolidates Headwater Engineered Systems' operations with selected functions from its Olive Branch, MS plant to optimize manufacturing, engineering, and sales resources. This will support Franklin Electric's offerings in commercial, industrial, municipal, agricultural, and irrigation markets. This development represents a strategic business realignment, emphasizing resource optimization and innovative product delivery in the water systems market.

- In March 2024, ITT Inc. announced an $11 million investment to enhance testing capabilities at three Industrial Process (IP) sites in Obernkirchen, Germany, Vadodara, India, and Dammam, Saudi Arabia. The investment aims to increase capacity for testing complex and large pump packages, bolstering ITT's local market strength in line with its ‘in region, for region’ strategy. This initiative will further the company’s ability to replicate real-world conditions for decarbonization applications and complex projects in North America. Expected to be completed by Q3 2024, the move highlights ITT’s commitment to superior innovation and customer service, supporting growth across its chemical, energy, mining, and industrial markets.

Companies Covered in North America Water Pump Market

- Waste Management Inc.

- SUEZ Group

- Veolia Environment S.A.

- Biffa PLC

- Clean Harbors Inc.

- Covanta Holdings Corporation

- Hitachi Zosen Corporation

- Remondis AG & Co. Kg

- Republic Services Inc.

- Stericycle Inc.

- ALBA Group

Frequently Asked Questions

The North America Water Pump Market is projected to be valued at US$ 10.0 Bn in 2026.

The Electric Pump segment is expected to account for approximately 72.9% of the North America Water Pump Market by Processing Treatment in 2026.

The market is expected to witness a CAGR of 5.0% from 2026 to 2033.

Infrastructure modernisation mandates and PFAS-driven regulatory compliance are accelerating municipal investments in advanced water treatment and pumping systems, driving growth in the North America Water Pump Market.

Key market opportunities in the Water Pump Market include renewable energy-linked pumping systems such as solar, geothermal, hydrogen, data center cooling and wastewater reuse-driven circular water infrastructure, both creating demand for high-efficiency, specialised, and next-generation pumping solutions.

Key players in the Water Pump Market include Xylem Inc., Flowserve Corporation, Grundfos, Ingersoll Rand Inc., Sulzer AG, and Wilo SE.