- LED & Lighting (Optoelectronics)

- North America Residential Lighting Fixtures Market

North America Residential Lighting Fixtures Market Size, Share, and Growth Forecast 2026 - 2033

North America Residential Lighting Fixtures Market by Product Type (Chandeliers, Pendants, Flush Mount Ceiling Lights, Semi-Flush Mount Ceiling Lights, Others), Usage (Indoor, Outdoor), by Material (Aluminum, Plastic, Metal, Others), Power Source, Sales Channel, and Regional Analysis, 2026 - 2033

North America Residential Lighting Fixtures Market Size and Trend Analysis

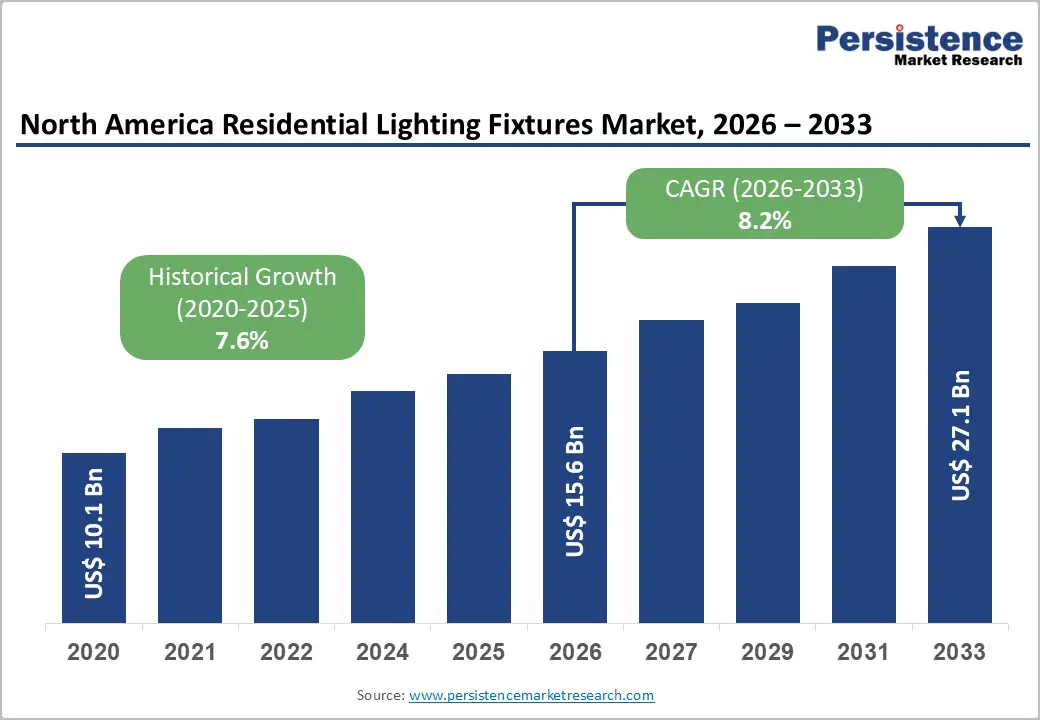

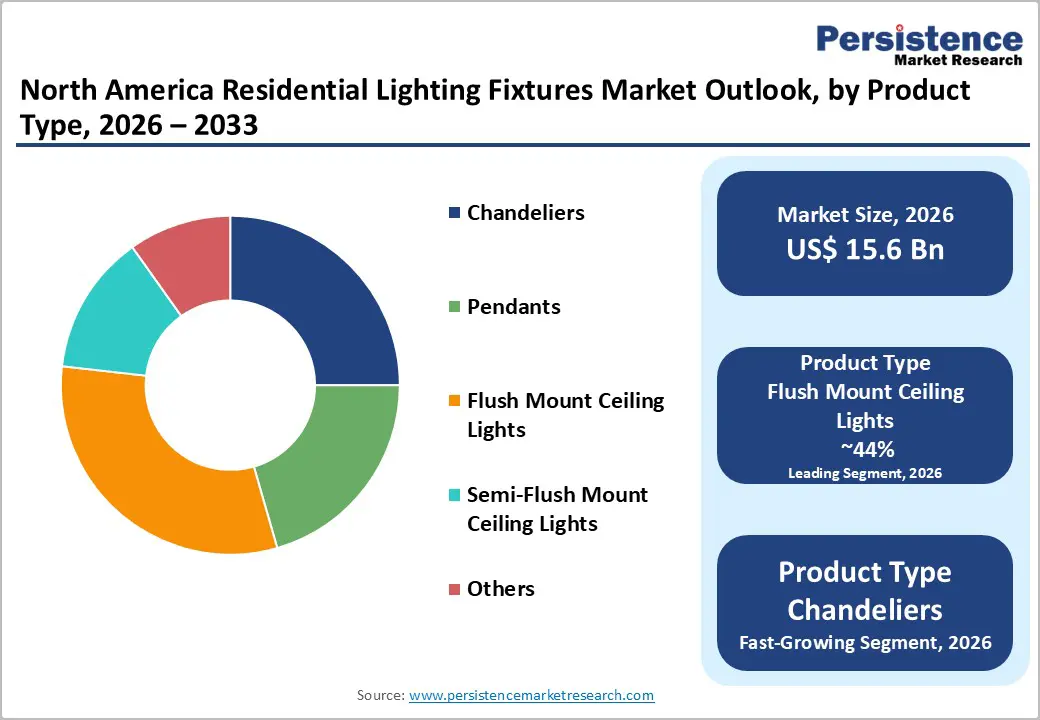

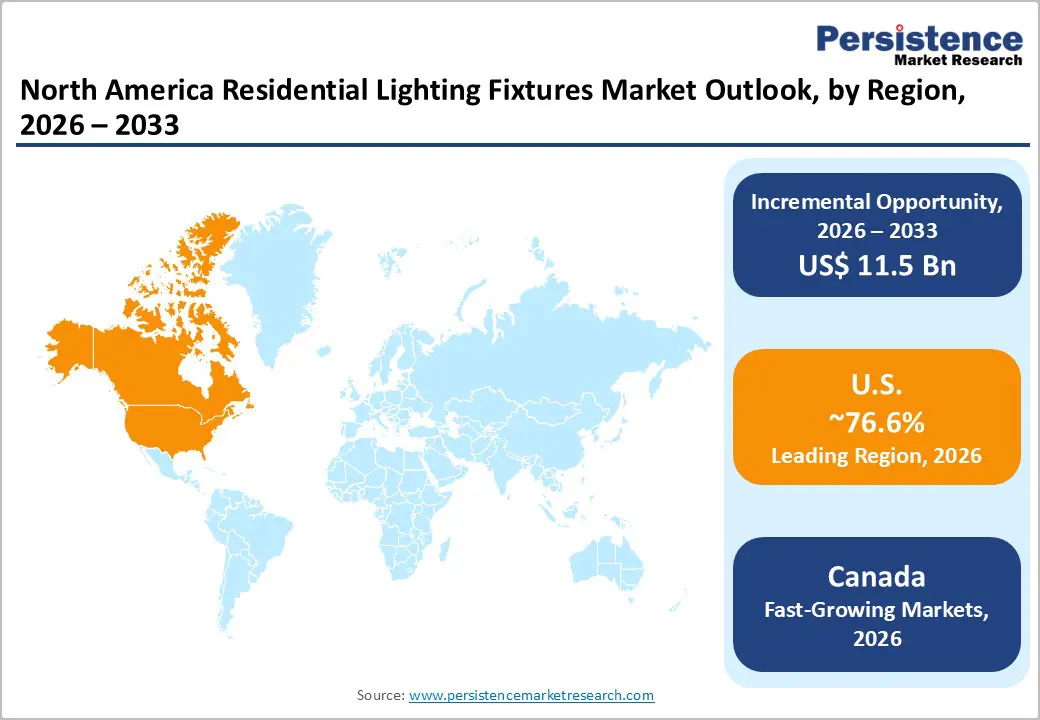

The North America residential lighting fixtures market size is valued at US$ 15.6 billion in 2026 and is projected to reach US$ 27.1 billion by 2033, growing at a CAGR of 8.2% during the forecast period from 2026 to 2033.

Market growth is driven by the rapid adoption of LED lighting, rising demand for smart and connected lighting solutions, and increasing home renovation and remodeling activities. Consumers are prioritizing energy-efficient, visually appealing fixtures, supported by favorable government policies and rebate programs promoting LED upgrades. Additionally, strong retrofit demand from the region’s large existing housing stock and growing integration with home automation and voice-controlled platforms continue to reshape residential lighting preferences.

Key Market Highlights:

- Leading Region: The U.S. dominates North America with 76.6% smart-lighting market share, driven by high disposable incomes, smart home adoption, and strong home improvement activity.

- Fastest-Growing Region: Canada shows the highest growth momentum at a 7.8% CAGR, driven by energy-efficiency regulations, progressive building codes, and the increasing adoption of connected-home technologies.

- Dominant Product Segment: Ceiling fixtures, including recessed downlights and flush mounts, account for 44% of the market, supported by standardized installation and widespread adoption in new homes.

- Fastest-Growing Product Segment: Smart decorative lighting, including AI-enabled pendants and connected chandeliers, is growing at 9.1% CAGR, driven by aesthetic customization and smart home integration.

- Key Market Opportunity: Circadian rhythm lighting systems present significant growth potential, offering advanced lighting that mimics natural daylight cycles to enhance sleep quality, wellness, and overall residential comfort.

| Key Insights | Details |

|---|---|

|

North America Residential Lighting Fixtures Market Size (2026E) |

US$ 15.6 Billion |

|

Market Value Forecast (2033F) |

US$ 27.1 Billion |

|

Projected Growth CAGR (2026-2033) |

8.2% |

|

Historical Market Growth (2020-2025) |

7.6% |

Market Dynamics

Drivers - Accelerating LED Adoption Supported by Energy Efficiency Regulations

The accelerating adoption of LED lighting continues to act as a major growth engine for the North American residential lighting fixtures market. LEDs deliver substantial energy savings, longer operating life, and lower maintenance costs compared to traditional incandescent and halogen lighting, making them increasingly attractive to cost- and sustainability-focused homeowners.

This transition is further supported by government-led efficiency mandates and incentive programs such as ENERGY STAR rebates, utility subsidies, and updated General Service Lamp regulations in the U.S. and Canada. Stricter minimum efficacy standards are compelling manufacturers and consumers to replace legacy fixtures, accelerating LED penetration across both new residential construction and retrofit applications.

Rising Smart Home Integration and Voice-Enabled Lighting Demand

The rapid expansion of smart home ecosystems is transforming consumer expectations for residential lighting fixtures across North America. Growing ownership of IoT-enabled devices has increased demand for connected lighting solutions that offer automation, remote control, and personalized lighting experiences.

Voice-enabled platforms such as Amazon Alexa, Google Assistant, and Apple HomeKit have significantly reduced adoption barriers by enabling seamless control and integration with broader home automation systems. Continuous innovation in smart lighting features, coupled with rising consumer spending on connected home technologies, is driving faster growth in smart residential lighting than in conventional fixture segments.

Restraints - Supply Chain Disruptions and Raw Material Cost Volatility

The North America residential lighting fixtures market continues to face supply chain challenges that constrain operational efficiency and place sustained pressure on manufacturer margins. Trade regulations, tariff policies, and cross-border logistics complexities have increased procurement costs for imported components and finished fixtures, with manufacturers often transferring a portion of these costs to end consumers.

Volatility in raw material pricing further complicates production planning, particularly for fixtures that rely heavily on metal components such as aluminum. In addition, recurring shortages of semiconductors and LED drivers, essential components in modern lighting systems, have disrupted manufacturing schedules and inventory management. These challenges disproportionately affect smaller and specialty lighting manufacturers with limited sourcing flexibility, leading to selective market participation and reduced product availability in certain regions.

High Installation Costs and Technical Complexity of Advanced Systems

The deployment of advanced smart lighting and residential automation solutions requires higher upfront investment and specialized technical expertise, creating adoption barriers for cost-conscious homeowners. Installation complexity is especially pronounced in older residential properties that lack compatible electrical or networking infrastructure, increasing reliance on professional installation services.

Integration of smart lighting systems with connectivity standards such as Zigbee, Bluetooth, and Matter, along with required software configuration and voice assistant integration, extends project timelines and elevates labor costs. These financial and operational challenges disproportionately impact middle-income households and renovation-focused projects, limiting penetration of advanced lighting solutions and moderating overall market growth in price-sensitive residential segments.

Opportunity - Decorative Smart Lighting and Personalized Ambiance Solutions

The convergence of aesthetic design trends and smart home functionality is creating strong growth opportunities within the decorative residential lighting segment. Increasing consumer preference for visually distinctive fixtures, such as pendant lights, chandeliers, and accent lighting, is driving manufacturers to integrate smart controls, color tuning, and scene customization features that enhance both design appeal and functionality.

Advancements in AI-driven lighting customization, voice-control compatibility, and interoperability with smart home ecosystems are further elevating the user experience. Decorative outdoor lighting is also gaining momentum as homeowners invest in patios, gardens, and outdoor living spaces, driving demand for motion-enabled, color-adjustable, and ambience-focused fixtures. Emerging interest in circadian rhythm lighting systems that align indoor lighting with natural daylight cycles represents a promising, underpenetrated opportunity for premium residential applications.

Sustainable Retrofitting and Green Building Certification Compliance

Sustainable retrofitting of existing residential buildings presents a significant opportunity for market expansion, particularly as homeowners and developers seek to modernize legacy lighting systems without extensive electrical upgrades. Retrofit-friendly smart lighting solutions enable energy efficiency improvements, automation, and control enhancements while minimizing installation complexity, making them attractive for renovation-focused residential projects.

Growing emphasis on green building certifications and sustainability-driven construction standards is further reinforcing demand for energy-efficient and smart lighting fixtures. Government-backed energy programs, municipal incentives, and evolving provincial and state-level building codes continue to encourage adoption of advanced lighting controls in both new construction and retrofit environments. Increasing use of solar-powered, battery-operated, and daylight-responsive outdoor fixtures aligns well with sustainability objectives and supports long-term growth opportunities across residential segments.

Category-wise Analysis

Product Type Insights

Ceiling fixtures, including recessed downlights, flush mounts, and integrated ceiling panel systems, dominate North America residential lighting fixtures market, accounting for approximately 44% of total revenue share. Their leadership is supported by standardized installation practices, strong contractor preference, and extensive adoption across both new residential construction and renovation projects. Recessed LED downlights are widely specified in newly built homes due to their energy efficiency, low maintenance, and compatibility with contemporary architectural designs.

Decorative lighting fixtures such as pendants and chandeliers represent the fastest-growing product category. Growth is driven by rising consumer emphasis on interior aesthetics, premium finishes, and personalized lighting experiences. Manufacturers are increasingly introducing smart-enabled decorative fixtures offering app-based controls, color tuning, and voice assistant compatibility, positioning decorative lighting as a high-value growth segment.

Usage Insights

Indoor residential lighting remains the dominant usage segment, capturing approximately 55% of total market share, reflecting the essential need for interior illumination across living rooms, bedrooms, kitchens, and bathrooms. High replacement demand, widespread LED penetration, and increasing adoption of smart features such as dimming and scheduling continue to support sustained demand for indoor lighting fixtures.

Outdoor residential lighting is the fastest-growing usage segment, supported by increased homeowner investment in patios, gardens, driveways, and entryways. Demand is rising for decorative and security-focused outdoor lighting solutions, including motion-activated, wireless, and solar-compatible fixtures, as consumers prioritize safety, visual appeal, and functional outdoor living environments.

Material Insights

Metal-based materials, primarily aluminum and steel, account for approximately 40% of total market value, making them the leading material category in residential lighting fixtures. Their dominance is attributed to durability, heat dissipation efficiency, and structural strength across ceiling-mounted, wall-mounted, and outdoor lighting applications. Growing incorporation of recycled metal content further supports adoption amid sustainability-focused manufacturing strategies.

Glass, crystal, and advanced polymer materials form the fastest-growing material segment. Glass and crystal elements are increasingly used in premium decorative fixtures to enhance visual impact, while polymers enable lightweight designs and flexible form factors for smart and wireless lighting. These materials support aesthetic differentiation without compromising functional performance.

Power Source Insights

Hardwired and corded-electric fixtures dominate the market, accounting for approximately 68% of residential lighting installations, driven by their widespread use in permanent indoor and outdoor lighting applications. Established residential electrical infrastructure and consumer familiarity continue to support strong demand for hardwired ceiling-mounted and wall-mounted fixtures requiring a continuous power supply.

Battery-powered and solar-integrated lighting fixtures represent the fastest-growing power source category. Growth is supported by increasing demand for flexible, wireless solutions suited to renovations, temporary installations, and outdoor areas without direct electrical access. Advances in LED efficiency and battery performance are further enhancing adoption across residential settings.

Sales Channel Insights

Offline distribution channels, including electrical wholesalers, distributors, and specialty lighting stores, account for approximately 55% of total residential lighting fixture sales. These channels remain essential for contractor-driven purchases, large residential projects, and premium fixtures that benefit from in-person consultation and professional specification support.

Online retail channels are the fastest-growing sales segment, driven by consumer preference for convenience, broader product selection, and transparent pricing. Digital platforms facilitate easier comparison of smart lighting features, installation guidance, and customer reviews, accelerating the adoption of LED and connected lighting fixtures through e-commerce channels.

Regional Insights

U.S. Residential Lighting Fixtures Trends

The United States represents the dominant regional market within North America, accounting for approximately 76.6% of the regional smart lighting market share. Strong demand is supported by high residential renovation activity, widespread smart home adoption, and strong consumer purchasing power. The presence of major lighting manufacturers, advanced distribution infrastructure, and active federal programs promoting energy-efficient lighting further reinforces the country’s leadership across both conventional and smart residential lighting segments.

Regional demand patterns vary across the U.S., with stronger growth observed in western and northeastern states due to technology adoption, sustainability awareness, and renovation-driven upgrades of aging housing stock. ENERGY STAR rebate programs and LEED-aligned building practices continue to accelerate LED and smart fixture adoption, while homeowners increasingly prioritize lighting aesthetics, automation, and ambiance-enhancing solutions alongside energy efficiency.

Canada Residential Lighting Fixtures Trends

Canada’s residential lighting fixtures market is witnessing steady expansion, driven by stringent energy efficiency regulations, progressive building codes, and strong government support for sustainable home technologies. The Canadian smart home market is projected to grow at a CAGR of 7.8%, reflecting increasing adoption of connected lighting systems as part of broader home automation trends. Federal and provincial initiatives actively promote energy-efficient lighting upgrades to support national emission reduction targets.

Regulatory alignment with U.S. energy efficiency standards has streamlined cross-border product availability and encouraged manufacturer standardization. Canadian consumers demonstrate high environmental awareness, favoring LED and smart lighting solutions that reduce energy consumption. A large stock of older residential properties presents strong retrofit opportunities, supported by government-backed financing programs and tax incentives encouraging investment in advanced residential lighting systems.

Competitive Landscape

The North America residential lighting fixtures market is characterized by moderate consolidation, with large multinational manufacturers operating alongside regional specialists and emerging smart lighting technology providers. Market structure remains balanced due to high entry barriers such as significant research and development investment, manufacturing scale requirements, and established retail and distribution relationships, which limit excessive fragmentation while supporting niche-focused competition.

Competitive strategies increasingly emphasize product innovation, digital-first sales models, and ecosystem-based offerings aligned with growing demand for smart and energy-efficient lighting solutions. Key differentiators include integrated smart lighting platforms, broad portfolios covering both decorative and functional fixtures, sustainability-focused product design, and compatibility with multiple home automation systems. Industry participants are also expanding service-oriented models, including professional installation partnerships and value-added software features.

Key Market Developments:

- In September 2025, Signify introduced the Hue Bridge Pro, a significantly upgraded smart home lighting control hub supporting 150 connected lights and 50 accessories, featuring a processor five times more powerful than its predecessor and memory 15 times larger, enabling storage of 500+ custom lighting scenes and advanced motion-sensing capabilities through Hue Motion Aware technology.

- In June 2024, Retrofit installations accelerated to comprise 58.6% of smart lighting deployment activity across North America, driven by the cost-effectiveness of modernizing existing building stock without comprehensive electrical infrastructure overhauls and increasing availability of wireless smart lighting solutions compatible with legacy wiring systems.

Companies Covered in North America Residential Lighting Fixtures Market

- Kichler Lighting LLC

- NBG Homes/Quoizel

- Generation Lighting(Generation Brand)

- Progress Lighting(Hubble)

- HINKLEY, INC

- Minka Lighting Inc.

- Progressive Lighting, Inc.

- Maxim Lighting

- Artika

- Globe Electric

- Golden Lighting

- Hudson Valley Lighting Group

- Elite Lighting

- Livex Lighting

- Elegant Lighting

Frequently Asked Questions

North America’s residential lighting fixtures market is valued at US$ 15.6B in 2026, projected to reach US$ 27.1B by 2033 at 8.2% CAGR, driven by LED adoption, smart home integration, and residential renovations.

Growth is fueled by 75% energy-saving LEDs, rising smart home lighting adoption, US residential renovations of US$ 498.3B in 2024, energy rebate programs, and LED efficacy mandates.

Ceiling fixtures, including recessed downlights, flush mounts, and integrated panels, dominate with 44% market share, while decorative smart pendants and chandeliers are the fastest-growing.

The U.S. leads with 76.6% smart lighting market share, driven by high disposable incomes, smart home adoption, renovation activity, and concentrated manufacturer presence.

Circadian rhythm lighting systems offer growth potential by enhancing sleep, mood, and cognitive performance, with market expansion at 18.5% CAGR.

Major players include Philips Hue, Acuity Brands, Hubbell Lighting, GE Lighting (Current), WAC Lighting, Cree Innovations, and IKEA TRÅDFRI, competing via innovation and smart home integration.