- Specialty & Fine Chemicals

- North America Gypsum Boards Market

North America Gypsum Boards Market Size, Share, and Growth Forecast 2026 - 2033

North America Gypsum Boards Market by Product Type (Wallboard, Ceiling Board, Pre-decorated Board, Other), Application (Wall Covers, Partitions, Fire Resistance, Moisture Resistance, Soundproofing, Aesthetics), End Use (Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

North America Gypsum Boards Market Size and Trend Analysis

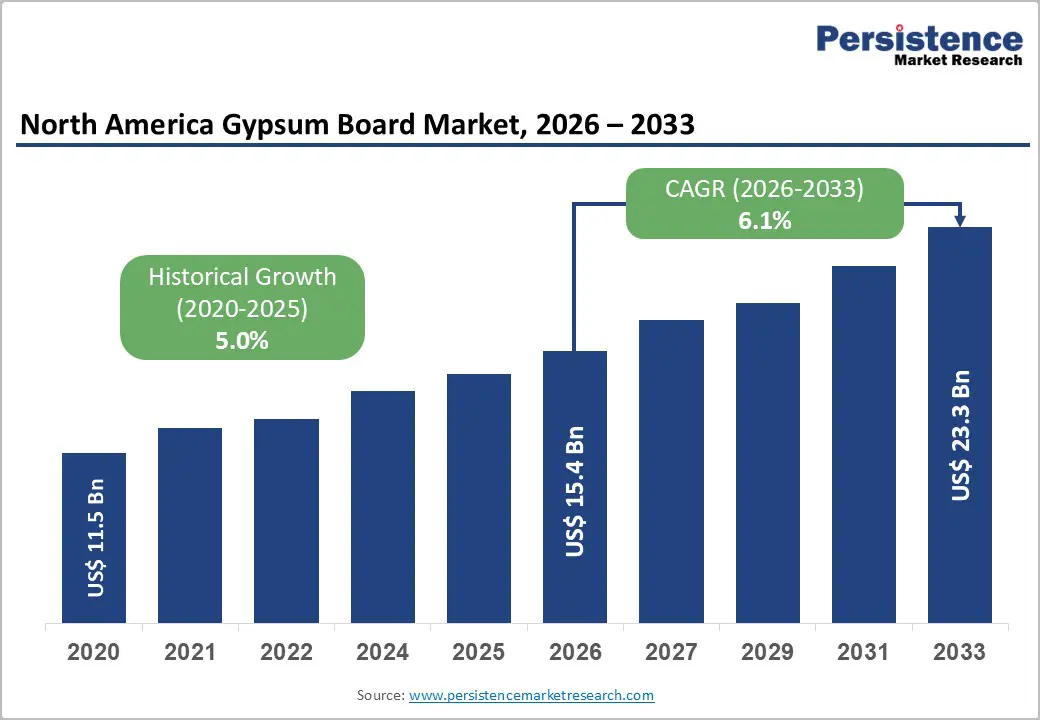

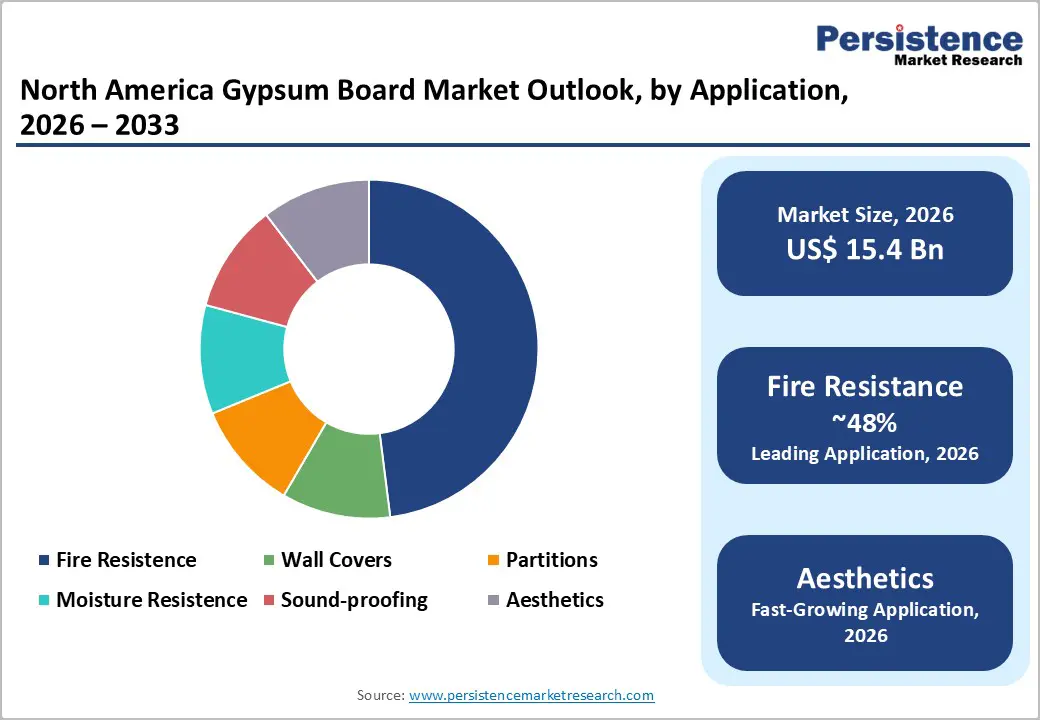

The North America Gypsum Boards market size is valued at US$ 15.4 Bn in 2026 and is projected to reach US$ 23.3 Bn by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

The market is principally driven by strong residential construction activity, rising demand for fire resistant and moisture resistant building materials, and an extensive renovation surge across the United States and Canada. Population growth and urbanization, together with increasingly stringent building regulations under the International Building Code (IBC) requiring the use of fire rated gypsum assemblies, continue to support steady consumption across all end use segments. Furthermore, the expanding adoption of sustainable and lightweight construction solutions is accelerating the market’s overall growth trajectory.

Key Market Highlights

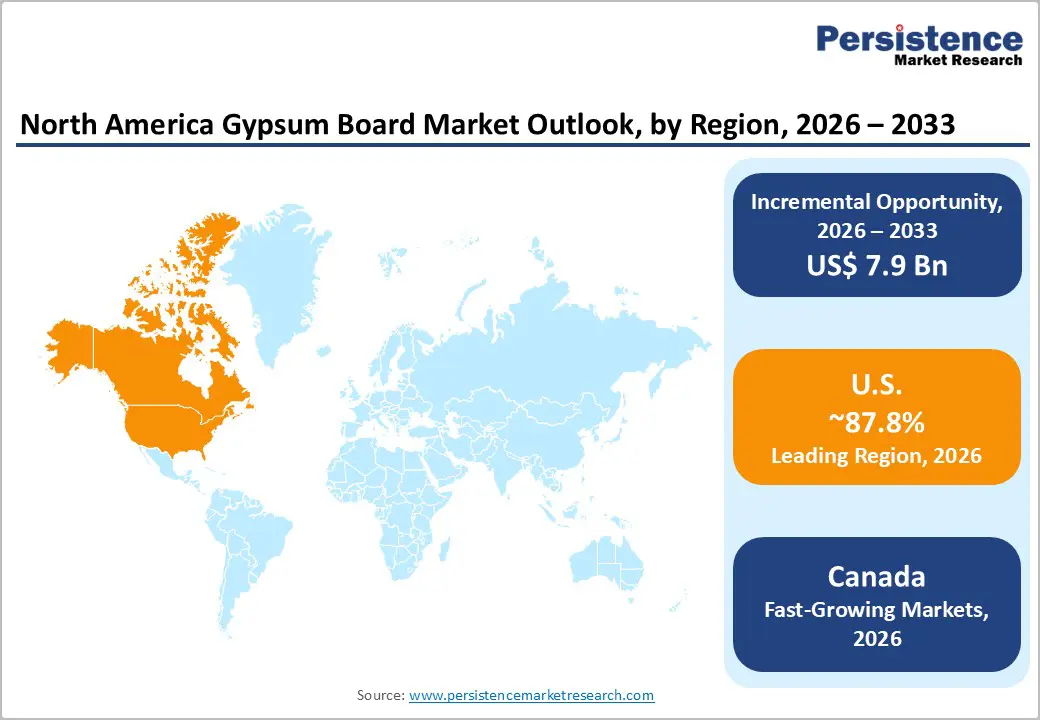

- Leading Region: The United States dominates the North America Gypsum Boards market with approximately 87.8% regional revenue share in 2025, driven by large-scale residential construction, strict fire-safety codes, and a well-established manufacturing ecosystem.

- Fastest Growing Region: Canada represents the fastest-growing gypsum board market in the region, backed by record housing starts of 259,028 units in 2025 (per CMHC), record rental construction, strong immigration-driven population growth, and government initiatives to resolve the national housing shortage.

- Dominant Segment: The Wallboard product type holds the largest share at approximately 47% in 2024, driven by its widespread use in wood-frame residential construction and its cost-efficient installation advantage over traditional plaster systems.

- Fastest Growing Segment: The Pre-decorated Board segment is the fastest growing product type, growing at a CAGR exceeding 10% globally, as commercial builders and hospitality developers favor factory-finished boards for rapid, cost-efficient interior completion.

- Key Market Opportunity: The shift toward low-carbon, sustainable gypsum boards presents the most strategically significant opportunity, such as federal green procurement policies, LEED v4.1 mandates, and corporate net-zero targets, which unlock premium pricing potential for EPD-certified, recycled-content gypsum solutions.

| Key Insights | Details |

|---|---|

|

North America Gypsum Boards Market Size (2026E) |

US$ 15.4 Bn |

|

Market Value Forecast (2033F) |

US$ 23.3 Bn |

|

Projected Growth CAGR (2026–2033) |

6.1% |

|

Historical Market Growth (2020–2025) |

5.0% |

Market Dynamics

Market Growth Drivers

Surging Residential Construction and Housing Demand in North America

The primary catalyst driving demand in the North America Gypsum Boards market is the rapid expansion of residential construction, supported by persistent housing shortages and sustained population growth. According to the U.S. Census Bureau, the national population reached 340.1 million in July 2024, accompanied by 1.36 million housing starts in 2025. Projections from the Congressional Budget Office indicate that annual housing starts will average 1.68 million units between 2025 and 2029, reflecting strong underlying demand and immigration driven household formation.

Given its extensive use in the wood frame construction prevalent across the region, gypsum wallboard directly benefits from this robust development pipeline. Additionally, the Joint Center for Housing Studies at Harvard University reported housing expenditures of approximately US$472 billion in 2022, while single family housing permits increased by 6.6% in 2024, further reinforcing sustained gypsum board consumption.

Stringent Fire Safety Codes and Green Building Adoption

Evolving building codes and green construction standards are creating a strong structural impetus for the gypsum board market across North America. The International Building Code (IBC) and corresponding state level regulations mandate the integration of fire rated gypsum assemblies in nearly all commercial and multi family residential projects, thereby establishing a consistent regulatory baseline for demand. Complementary sustainability frameworks, such as LEED certification and state programs including California’s Title 24 energy efficiency standards, further reinforce the use of gypsum boards due to their contributions to thermal performance and indoor air quality.

In response, manufacturers have introduced advanced, lower carbon solutions. Remarkably, Saint Gobain launched its CarbonLow gypsum wallboard in October 2024, offering up to 60% reduced embodied carbon. According to the U.S. Green Building Council, the steady expansion of the U.S. green building market continues to solidify gypsum boards’ role in compliant, environmentally responsible construction.

Market Restraints

Vulnerability to Raw Material Price Volatility

Volatility in the prices of key raw materials, including natural gypsum, synthetic gypsum derived as a by product of coal fired power generation, energy inputs, and paper facings, continues to pose a significant challenge for industry participants. According to the U.S. Geological Survey’s Mineral Commodity Summaries, domestic crude gypsum production in North America amounted to approximately 22 million tons, valued at about US$264 million.

As the regional energy transition accelerates and coal based power generation declines, the availability of FGD based synthetic gypsum is expected to diminish, resulting in supply chain constraints and potential upward pressure on prices. Concurrently, rising freight and energy costs are compressing manufacturer margins, delaying planned capacity expansions, and creating the risk of supply demand imbalances. These cost pressures particularly hinder smaller producers, thereby moderating broader market growth.

Susceptibility to Moisture Damage and Environmental Disposal Issues

Despite their broad utilization across construction applications, standard gypsum boards remain inherently vulnerable to moisture due to their hygroscopic composition. This limitation restricts their suitability for environments characterized by persistent dampness, including basements, bathrooms, and exterior façades. Consequently, alternative materials, such as fiber cement boards, cement backer units, and magnesium oxide (MgO) boards, have increasingly captured market share in high moisture settings.

Furthermore, the disposal of gypsum board waste presents notable environmental challenges, as decomposition in landfills can produce hydrogen sulfide gas and allow sulfur compounds to leach into groundwater. Growing regulatory scrutiny over gypsum landfill practices in several jurisdictions has further elevated compliance and operational costs for manufacturers and contractors. Collectively, these factors temper the broader adoption of gypsum boards across diverse construction scenarios.

Market Opportunities

Explosive Growth Potential in Pre-decorated Gypsum Boards

The pre decorated board segment constitutes one of the most prominent near term growth opportunities within the North America Gypsum Boards market, supported by a marked shift in consumer preferences toward turnkey interior finishing solutions. These boards, equipped with factory applied finishes, textures, and designs, eliminate the need for post installation treatments such as painting or wallpapering, thereby delivering substantial time and cost efficiencies, particularly in commercial retrofit environments.

Rising emphasis on visually refined interiors across hospitality, healthcare, and educational facilities, where minimal construction disruption is essential, continues to accelerate demand. Manufacturers can strategically leverage this trend by advancing customized design capabilities, sustainable surface coatings, and acoustically enhanced pre decorated solutions tailored to the region’s expanding commercial renovation market.

Sustainable and Low-Carbon Gypsum Products Aligned with Net-Zero Commitments

The accelerating regulatory and corporate transition toward net zero carbon buildings is creating a substantial growth avenue for manufacturers of low embodied carbon gypsum board products across North America. Following Saint Gobain Canada’s inauguration of the region’s first zero carbon gypsum wallboard facility in Sainte Catherine, Quebec, in September 2025, which achieves an annual reduction of 44,000 tons of CO emissions, the industry is experiencing a decisive shift toward circular and environmentally responsible manufacturing practices.

Key initiatives, including gypsum board recycling programs, the incorporation of recycled content, and the adoption of renewable energy based production processes, align closely with certification requirements under LEED v4.1 and the WELL Building Standard. Manufacturers offering verified Environmental Product Declarations (EPDs) and certified sustainable gypsum boards are increasingly positioned to secure specification advantages as green procurement mandates expand across federal, state, and institutional construction sectors.

Category-wise Insights

Product Type Analysis

The Wallboard segment maintains a dominant position within the North America Gypsum Boards market, accounting for an estimated 47% share in 2024. Its leadership is attributed to its exceptional versatility, cost effectiveness, and strong alignment with the wood frame construction techniques widely utilized across the region. As the principal interior finishing material for both residential and commercial structures, wallboard effectively replaces traditional plaster and lath systems by offering faster installation, improved surface uniformity, and enhanced labor efficiency.

Growing single family housing activity in high growth Sun Belt states, including Texas, Florida, and the Carolinas, has further reinforced demand. Continued innovation also supports segment expansion; for instance, Georgia Pacific LLC introduced the DensDeck ProFast Prime Roof Board in February 2025, a fiberglass mat reinforced gypsum panel that is 20% lighter than conventional alternatives, demonstrating ongoing advancement within the wallboard product category.

Application Analysis

The Fire Resistance application segment maintains a leading position in the North America Gypsum Boards market, accounting for approximately 48% of total demand in 2025. This dominance is primarily attributable to the extensive regulatory requirements established under the International Building Code (IBC) and the National Fire Protection Association (NFPA), which mandate fire rated separations across a broad spectrum of residential, commercial, and industrial structures.

Standard specifications such as Type X and Type C fire rated gypsum boards are widely utilized in garage to living space separations, stairwells, and corridor enclosures. The rapidly expanding commercial construction pipeline, including data centers, logistics hubs, and healthcare campuses, continues to reinforce demand for fire resistant assemblies. Concurrently, the soundproofing and Aesthetics sub segments are gaining notable traction in premium residential and hospitality developments, contributing to multi application growth across the region.

End Use Analysis

The Residential segment holds the dominant position in the North America Gypsum Boards market, representing an estimated 45% share in 2024. This leadership is primarily attributed to the substantial volume of single family and multi family residential construction across the region, which continues to generate consistent demand for gypsum based interior systems. The U.S. Census Bureau reports approximately 142 million housing units nationwide, with ongoing additions driving sustained consumption of drywall products.

Both standard and fire resistant gypsum boards remain essential in residential applications, with Type X boards mandated for fire rated garage separations and Type C boards extensively used in multi family corridor assemblies. Meanwhile, the Commercial segment is registering the fastest growth, supported by expanding office fit outs, retail development, and institutional projects where gypsum board systems provide notable advantages in installation efficiency and acoustic performance.

Country-wise Insights

U.S. Gypsum Boards Market Trends

The United States accounts for the majority of North America's gypsum board demand, commanding approximately 87.8% of regional market share. The country's well-established wood-frame residential construction industry, extensive renovation market, and stringent fire-safety building codes collectively underpin this dominance. According to the U.S. Census Bureau, total construction spending in 2024 was approximately US$ 1,696 billion, with residential construction contributing US$ 929.5 billion. The U.S. population reaching 340.1 million in 2024, with the largest year-over-year gain since 2001, is driving incremental housing demand and fueling sustained gypsum board consumption.

On the innovation front, manufacturers are investing heavily in domestic production capacity. In October 2025, Saint-Gobain (CertainTeed) completed a more than US$ 240 million expansion at its Palatka, Florida facility, making it the largest gypsum wallboard manufacturing plant in the world and doubling its production capacity. Georgia-Pacific invested US$ 325 million in a second Sweetwater, Texas plant. These investments reflect strong confidence in long-term U.S. gypsum board demand, especially in the high-growth southeastern and sunbelt states.

Canada Gypsum Boards Market Trends

Canada represents the second-largest gypsum board market in North America, with growing demand supported by robust residential construction and federal housing policy initiatives. The Canada Mortgage and Housing Corporation (CMHC) reported 259,028 housing starts in 2025, the fifth-highest annual total on record and a 5.6% increase from 2024. Record-level rental housing construction, which accounted for over half of all urban starts, is particularly supportive of gypsum board volumes as multi-unit residential projects are intensive consumers of interior wall and ceiling systems. Cities such as Montreal and Calgary saw especially strong activity, partially offsetting slowdowns in Toronto and Vancouver.

Canada is also emerging as a sustainability leader in gypsum board manufacturing. The Saint-Gobain CarbonLow wallboard, produced at North America's first zero-carbon wallboard facility near Montreal, reflects the country's alignment with Canada's federal Net-Zero Emissions by 2050 goal. Canada's National Building Code amendments promoting energy-efficient construction materials, combined with significant immigration-driven population growth, are expected to sustain healthy mid-single-digit gypsum board demand growth through 2033.

Competitive Landscape

The North America Gypsum Boards market exhibits a moderately consolidated structure, characterized by the presence of several dominant manufacturers, most notably Saint Gobain (CertainTeed), Knauf Group (USG Corporation), and Georgia Pacific LLC, who collectively command a substantial share of regional production capacity. These industry leaders prioritize capacity expansion, vertical integration of gypsum raw material supply, and the advancement of sustainable, performance enhancing product innovations as key strategic imperatives. Competitive differentiation is increasingly defined by factors such as fire resistance performance, embodied carbon certifications supported by Environmental Product Declarations (EPDs), acoustic efficiency, and logistical proximity to rapidly expanding Sun Belt markets.

Key Market Developments

- October 2025: Saint-Gobain (CertainTeed) completed a more than US$ 240 million expansion of its CertainTeed Gypsum Facility in Palatka, Florida, making it the largest gypsum wallboard manufacturing facility in the world, doubling production capacity and creating 110 new jobs in the region.

- September 2025: Saint-Gobain Canada inaugurated North America's first zero-carbon (scopes 1 and 2) gypsum wallboard plant at Sainte-Catherine, Quebec, reducing CO2 emissions by 44,000 tons per year and boosting capacity by up to 40% through full electrification powered by renewable energy.

- October 2023: Georgia-Pacific officially opened its new gypsum wallboard production facility in Sweetwater, Texas. Initially announced in September 2020, the $325 million facility is our second gypsum wallboard production facility in Nolan County, and the first Georgia-Pacific has built since 2004.

Top Companies in the North America Gypsum Boards Market

Saint-Gobain (Malvern, U.S.), operating through its subsidiary CertainTeed, is the undisputed market leader in North American gypsum board manufacturing, commanding significant production capacity across more than 60 manufacturing facilities in the U.S. and Canada. With €46.6 billion in global sales in 2024 and more than 6,900 CertainTeed employees, the company leverages its scale to drive product innovation, including low-carbon CarbonLow wallboard and the world's first net-zero gypsum plant in Quebec, reinforcing its leadership in sustainable construction.

Georgia-Pacific LLC (Atlanta, U.S.), a subsidiary of Koch Industries, is one of North America's largest gypsum board producers, having invested approximately US$ 325 million to build a second gypsum wallboard plant at Sweetwater, Texas, creating a combined capacity exceeding 93 million m²/year at the site. Since 1965, the company has maintained a reputation for innovation through its ToughRock® and high-performance Dens® product families, targeting demanding commercial and industrial applications. The 2025 launch of DensDeck ProFast Prime underscores its commitment to next-generation product development.

Knauf Group (Iphofen, Germany), having acquired USG Corporation in 2019, operates one of the most extensive gypsum manufacturing and distribution networks in North America under the iconic Sheetrock® brand. In June 2024, USG commenced gypsum production at its new Avery Quarry in Iosco County, Michigan, targeting 550,000 tons in 2025 to offset declining synthetic gypsum supply. The combined Knauf-USG entity benefits from deep vertical integration, global R&D capabilities, and a broad product portfolio spanning standard, lightweight, and specialty fire-rated boards catering to diverse North American market needs.

Companies Covered in North America Gypsum Boards Market

- Saint-Gobain (CertainTeed)

- Knauf Group (USG Corporation)

- America Gypsum Company LLC

- Gold Bond Building Products, LLC.

- Etex Group

- Georgia-Pacific LLC

- Eagle Material Inc.

- PABCO Gypsum

- Pioneer Material West

- Armstrong World Industries

Frequently Asked Questions

The North America Gypsum Boards Market is valued at US$ 15.4 Bn in 2026 and is projected to reach US$ 23.3 Bn by 2033, growing at a CAGR of 6.1% during the forecast period of 2026-2033. The market registered a historical CAGR of 5.0% between 2020 and 2025.

The primary demand drivers include accelerating residential construction fueled by persistent housing shortages, with the Congressional Budget Office (CBO) projecting housing starts to average 1.68 million units annually from 2025 to 2029, mandatory fire-resistance standards under the International Building Code (IBC), growing adoption of LEED-certified green buildings, and increasing renovation activity across both residential and commercial building stock in the region.

The Wallboard segment is the leading product type in the North America Gypsum Boards Market, holding approximately 47% market share in 2024. Its dominance is attributed to its cost efficiency, versatility in residential and commercial applications, and widespread adoption in wood-frame construction, the predominant building method in North America.

The United States dominates the regional market, accounting for approximately 87.8% of North America's total gypsum board revenue in 2025. The U.S. leadership is underpinned by robust residential and commercial construction, a well-developed manufacturing base, and a comprehensive regulatory framework that mandates fire-rated gypsum assemblies across diverse building types.

The most significant market opportunity lies in sustainable and low-carbon gypsum board products. As LEED v4.1, corporate net-zero commitments, and federal green procurement mandates tighten, manufacturers offering EPD-certified, recycled-content gypsum products, such as Saint-Gobain's CarbonLow range with up to 60% lower embodied carbon, are well-positioned to capture premium pricing and specification preference in institutional and government-funded construction projects.