- Aerospace & Defense

- North America eVTOL Aircraft Market

North America eVTOL Aircraft Market Size, Share, and Growth Forecast, 2026 - 2033

North America eVTOL Aircraft Lift Technology (Vectored Thrust, Multirotor, Lift Plus Cruise), Mode of Operation (Piloted, Autonomous, and Semi-Autonomous), Range (0-200 Km, and 200-500 Km), Maximum Take-off Weight (MTOW) (<250 Kg, 250-500 Kg, 500-1500 Kg, and >1500 Kg), Application (Commercial, Military, and Emergency Medical Service), Propulsion Type (Battery-Electric, Hybrid-Electric, and Hydrogen-Electric) Analysis for 2026 - 2033

North America eVTOL Aircraft Size and Trends Analysis

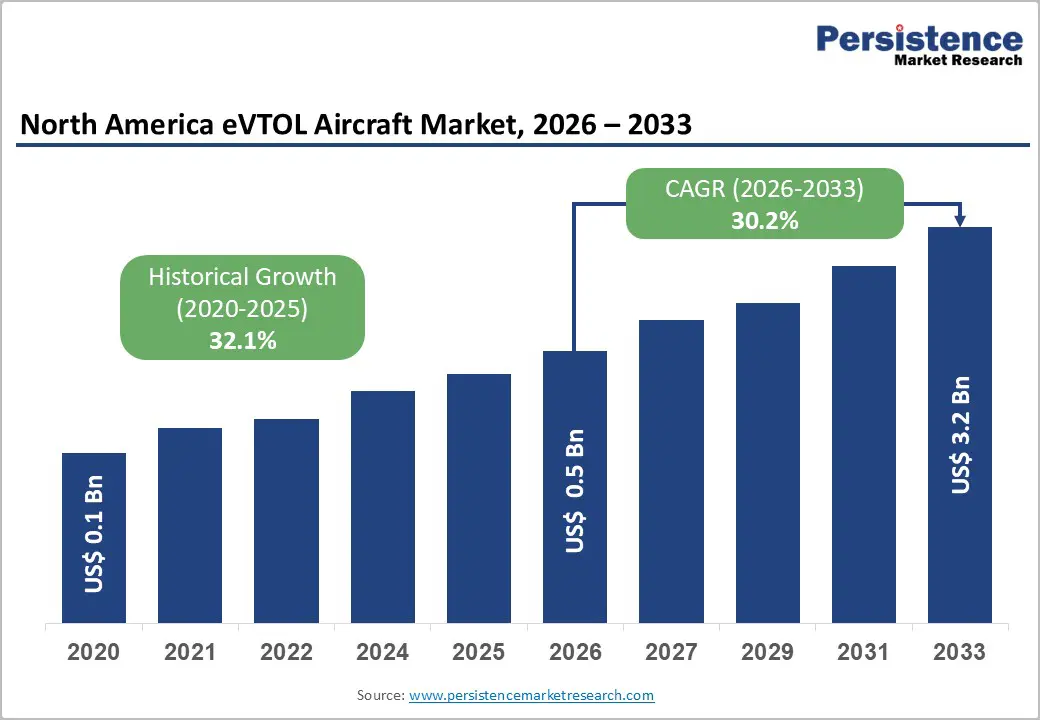

The North America electric vertical take-off and landing (eVTOL) aircraft market size is likely to be valued at US$ 0.5 billion in 2026 and is projected to reach US$ 3.2 billion by 2033, growing at a CAGR of 30.2% between 2026 and 2033. This remarkable expansion is fundamentally driven by the Federal Aviation Administration's formal launch of the eVTOL Integration Pilot Program, establishing public-private partnerships with state, local, and tribal governments alongside U.S.-based developers to accelerate safe deployment, while the air cargo sector processed 83.83 billion freight ton miles, demonstrating substantial logistics infrastructure supporting aerial mobility integration.

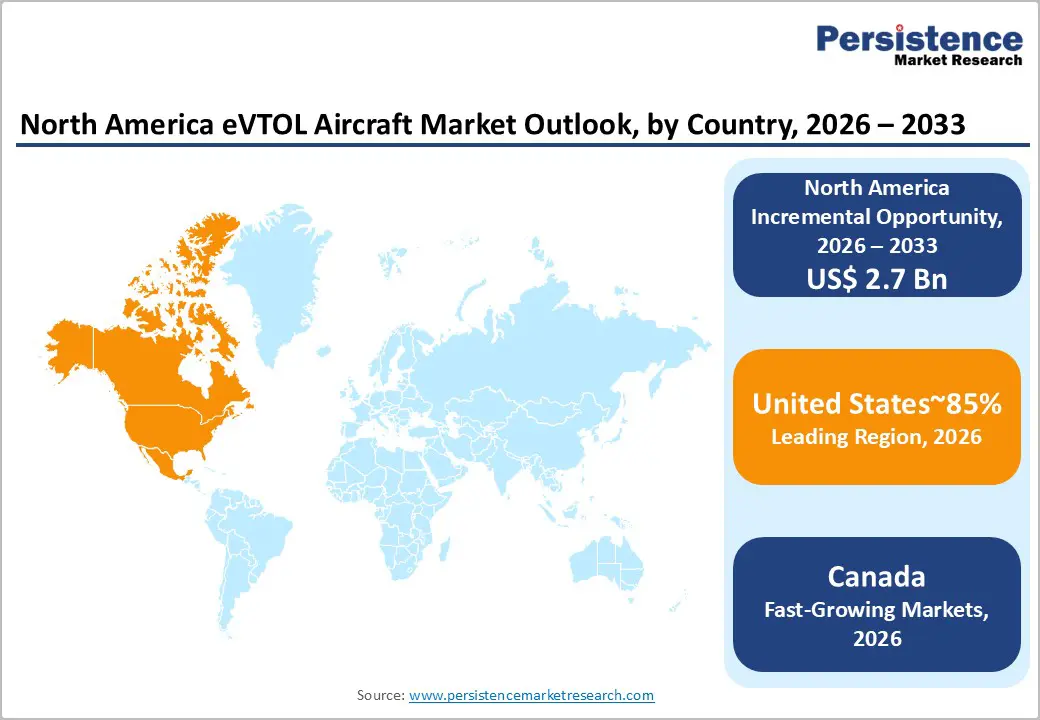

The United States Department of Transportation released the Advanced Air Mobility National Strategy outlining phased rollout from the late twenties through the mid-thirties with emphasis on airspace management and vertiport infrastructure, while North America currently commands around 42% of the global eVTOL market with 45 operational vertiports, 120 under construction, and over 200 planned infrastructure sites signaling comprehensive ecosystem development supporting commercial air taxi operations, emergency medical transport, and autonomous cargo delivery services.

Key Industry Highlights:

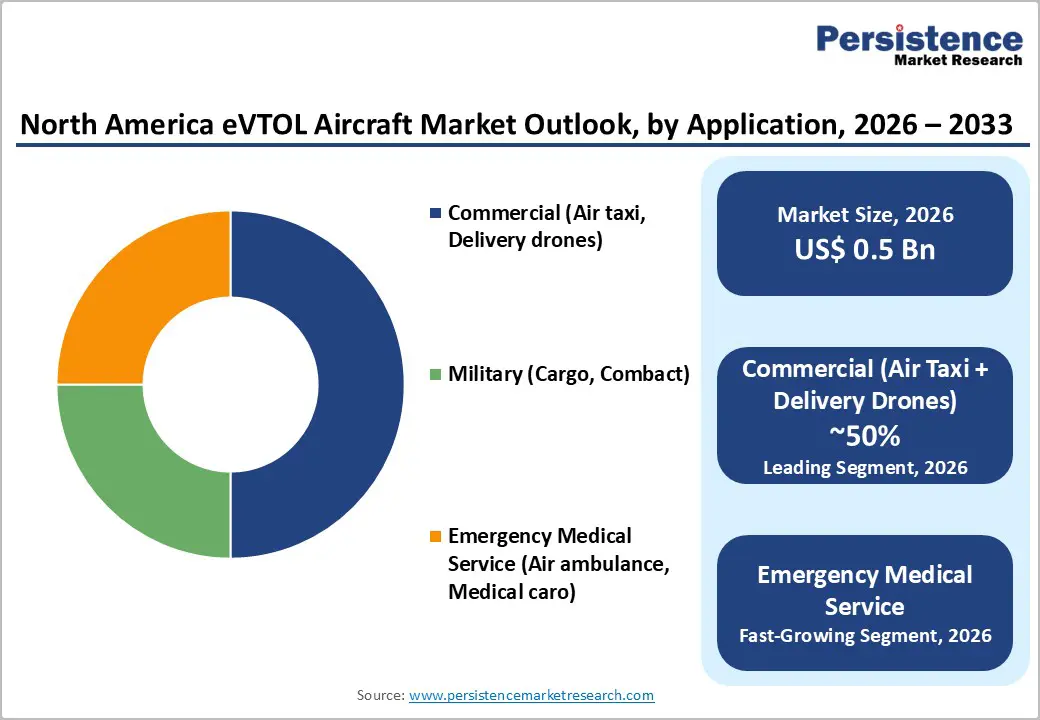

- Leading Applications: Commercial air taxi and delivery applications account for 50% market share, propelled by urban congestion, e-commerce growth, and airline partnerships with Joby Aviation and Archer Aviation.

- Leading Propulsion Type: Hydrogen-electric eVTOLs are the fastest-growing propulsion segment, enabled by extended range capabilities, rapid refueling, and technological advancements from Joby Aviation and Horizon Aircraft.

- Leading Lift Technology: Multirotor eVTOLs hold 45% market share, preferred for vertical takeoff and landing in dense urban environments, offering mechanical simplicity and high operational safety.

- Vectored Thrust Growth Driver: Vectored thrust eVTOLs are the fastest-growing lift configuration, supporting higher speeds, longer ranges, and regional transportation, demonstrated by Joby Aviation and XTI Aerospace designs.

- Strategic Partnerships Expansion: Strategic collaborations with airlines, logistics operators, and regional aviation networks accelerate market adoption, leveraging existing infrastructure and customer bases, e.g., Delta, United, and Helijet.

- Innovation & Investment Momentum: Market growth is fueled by industry developments and funding, including Archer Aviation’s early air taxi deployment, Oshkosh symposium showcases, and Eve Air Mobility’s $150M financing.

| Key Insights | Details |

|---|---|

| eVTOL Aircraft Size (2026E) | US$ 0.5 Bn |

| Market Value Forecast (2033F) | US$ 3.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 30.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 32.1% |

Market Dynamics

Drivers - Urban Congestion and Logistics Infrastructure Transformation

The escalation of metropolitan transportation challenges and evolving freight distribution requirements are fundamentally reshaping demand for Electric Vertical Take-off and Landing (eVTOL) solutions across North American cities and logistics networks. The United States air cargo industry processed 75.14 billion freight ton miles through the first eleven months, while domestic air cargo operations handled 16.14 billion FTMs despite experiencing modest contraction, demonstrating the massive scale of existing aerial logistics infrastructure that Electric Vertical Take-off and Landing aircraft can leverage for cargo delivery, medical supply transport, and emergency response applications.

The Atlantic region demonstrated robust 6.02% growth, expanding from 7.92 billion to 8.40 billion FTMs, while Latin America achieved exceptional 8.23% growth rising to 1.80 billion FTMs, reflecting strengthening trade corridors and nearshoring manufacturing operations that create demand for rapid point-to-point freight movement, where Electric Vertical Take-off and Landing cargo drones offer speed advantages over ground transportation. Urban areas face intensifying road congestion, reducing ground transport efficiency, and increasing delivery times, while e-commerce growth drives demand for last-mile logistics solutions enabling same-day and on-demand delivery services.

The Vertical Flight Society documented over 1,100 eVTOL designs in its World eVTOL Aircraft Directory, including significant North American contributions from Joby Aviation, Wisk, Jaunt Air Mobility, and XTI Aerospace, demonstrating extensive innovation addressing urban mobility and freight logistics challenges. The North America Electric Vertical Take-off and Landing Aircraft Market benefits directly from this convergence of urban transportation constraints and logistics infrastructure evolution, as multirotor and vectored thrust aircraft provide vertical takeoff capabilities, eliminating runway requirements while delivering passengers and cargo directly between origin and destination points, fundamentally transforming metropolitan mobility patterns and supply chain efficiency.

Federal Regulatory Framework and Government Policy Support

The establishment of comprehensive regulatory pathways and direct government support through pilot programs represents a transformative driver accelerating North American eVTOL commercialization and infrastructure deployment. The Federal Aviation Administration launched the eVTOL Integration Pilot Program, forming public-private partnerships with at least five state, local, tribal, or territorial governments alongside U.S. based private sector partners experienced in eVTOL development, manufacturing, or operations to demonstrate scalable, safe urban air mobility and operational readiness.

The U.S. Department of Transportation, led by Secretary Sean P. Duffy, unveiled the initiative establishing partnerships with companies including Joby Aviation, Archer Aviation, and BETA Technologies to accelerate safe, scalable Advanced Air Mobility operations encompassing short-range air taxis, cargo, medical transport, and automation enhancements over a three year pilot period reinforcing U.S. leadership. The Presidential Executive Order formally positioned drones and eVTOL aircraft as critical to national innovation, mandating accelerated safe integration of unmanned aircraft into the National Airspace System, expanding Beyond Visual Line of Sight operations, promoting domestic manufacturing and exports, and calling for AI assisted FAA approvals, signaling comprehensive federal support.

The FAA Reauthorization Act established mechanisms for aviation infrastructure owners to safely accommodate powered lift aircraft meeting safety requirements, updated airport district office guidance regarding heliport and vertiport design standards, and extended pilot programs to include urban air mobility operations at existing airport and heliport infrastructure. Joby Aviation achieved Type Inspection Authorization in November progressing to Stage 4 of the five-stage certification process, positioning the company for Type Certificate issuance in the near term, enabling commercial air taxi operations, while Archer Aviation completed over 400 test flights, demonstrating full transition envelope and expects Type Inspection Authorization shortly based on current progress.

The North America eVTOL Aircraft Market benefits from this coordinated federal regulatory development, establishing clear certification pathways, safety standards, and operational frameworks that reduce commercialization uncertainty while providing infrastructure support mechanisms, accelerating vertiport deployment, and airspace integration critical for scaled eVTOL operations.

Restraint - Certification Complexity and Regulatory Timeline Uncertainty

The unprecedented nature of eVTOL aircraft configurations creates substantial certification challenges and timeline unpredictability that constrain market commercialization pace and investment confidence. The Federal Aviation Administration certification process comprises five distinct stages spanning Application Acceptance, Certification Basis Established, Compliance Testing, Type Inspection Authorization, and Type Certificate Issuance, with manufacturers requiring multiple years to progress through testing validation and conformity inspections before receiving commercial operation authorization. Joby Aviation became the first eVTOL manufacturer to reach Stage 4 in November, positioning for potential Type Certificate issuance pending final production aircraft conformity inspections, while Archer Aviation submitted updated means of compliance documentation addressing battery safety protocols, emergency landing procedures, and continued safe flight requirements, expecting Type Inspection Authorization in the near term based on current testing progress.

The certification process addresses novel technical considerations, including distributed electric propulsion reliability across multiple independent motors, battery thermal management under varied environmental conditions, fly-by-wire flight control system redundancy meeting equivalent safety standards, and autonomous flight capabilities requiring complex system validation.

The FAA typically requires extensive documentation spanning airframe design, propulsion systems, flight controls, and safety redundancies with evaluation periods extending six to twelve months for application acceptance alone, while compliance demonstration testing and conformity inspections add a substantial additional timeline before commercial authorization. This regulatory pathway complexity creates commercialization uncertainty affecting investment decisions, operational planning, and market entry timing for eVTOL manufacturers and service operators.

Opportunities - Integration with Existing Aviation and Logistics Networks

The extensive aviation infrastructure and mature logistics operations across North America create substantial opportunities for eVTOL integration, leveraging established facilities, customer relationships, and operational expertise, accelerating commercialization timelines.

Joby Aviation established partnerships with Delta Air Lines planning to launch operations across New York and Los Angeles markets, connecting airports to city centers and eliminating ground transportation delays, while Archer Aviation supports United Airlines route network across San Francisco, Los Angeles, and Chicago metropolitan areas, operating from existing heliport infrastructure adapted for eVTOL operations. These airline partnerships provide immediate access to established customer bases, loyalty program integration, booking systems, and operational facilities, reducing market entry barriers and customer acquisition costs compared to standalone eVTOL operators building brands and distribution channels from inception.

The October development saw Helijet place firm orders for Beta Technologies all electric eVTOL aircraft, planning to integrate them into its existing network for passenger, cargo, and emergency services in southwestern British Columbia and the Pacific Northwest, marking major commercial eVTOL adoption leveraging established regional aviation operations.

AIR raised USD 23 million in Series A funding to accelerate U.S. expansion and scale production of both crewed and uncrewed eVTOL aircraft, including the AIR ONE and autonomous cargo models, positioning to meet FAA MOSAIC certification standards and support demand for advanced air mobility and logistics solutions. The cargo-focused opportunities prove particularly compelling given the United States air cargo industry's 83.83 billion FTM annual throughput with established freight forwarding relationships, logistics hub infrastructure, and customer demand for faster delivery options.

The Atlantic region's 6.02% growth and Latin America's 8.23% expansion in FTMs demonstrate robust international trade corridors where eVTOL cargo aircraft provide time sensitive delivery capabilities for high value goods, medical supplies, and e-commerce packages leveraging existing cargo terminals and customs facilities. The North America eVTOL Aircraft Market benefits from these partnership opportunities as established aviation and logistics operators provide validation, operational expertise, infrastructure access, and customer relationships accelerating commercial deployment while reducing execution risk associated with greenfield market development.

Hydrogen Electric Propulsion Technology Advancement

The development of hydrogen fuel cell propulsion systems represents a transformative opportunity enabling extended range capabilities and operational flexibility beyond battery electric limitations, supporting broader eVTOL application categories and mission profiles

Joby Aviation showcased its SHy4 hydrogen powered aircraft achieving a 561mile flight at the 4th Annual H2 Aero Symposium hosted by the Vertical Flight Society in Long Beach, California, highlighting integration of hydrogen propulsion in eVTOLs and advancement of sustainable aviation technologies demonstrating substantial range improvements over battery electric platforms.

The Vertical Flight Society convened the symposium where North American eVTOL leaders presented developments in hydrogen-powered aircraft reflecting industry momentum toward alternative propulsion technologies, addressing range limitations constraining battery electric operations. Horizon Aircraft selected Pratt & Whitney's PT6A turboprop engine for its full scale Cavorite X7 eVTOL aiming to deliver enhanced speed, range, efficiency, and reliability while reducing emissions by up to 30% compared to conventional aircraft, with the Pratt & Whitney Canada partnership strengthening Horizon's hybrid eVTOL program.

Horizon Aircraft received a USD 2 million INSAT grant to fund Project CRYSTAL, an all weather eVTOL initiative in partnership with the University of Toronto and Flight Centre of Excellence focusing on developing advanced ice detection, protective coatings, and vertical propulsion systems for the Cavorite X7 enabling safe operations in challenging weather conditions, expanding operational capabilities in medical, disaster relief, and defense applications. The hydrogen electric propulsion advancement addresses critical operational constraints of battery electric systems, including limited range restricting route networks to short urban trips, lengthy charging times constraining aircraft utilization rates, and payload capacity penalties from heavy battery weight limiting passenger or cargo capacity.

Hydrogen fuel cells provide higher energy density, enabling 500-plus mile ranges supporting regional transportation routes, rapid refueling comparable to conventional aircraft, maintaining high utilization rates, and weight advantages at longer ranges where hydrogen system mass becomes favorable compared to battery alternatives. The North America eVTOL Aircraft Market benefits from hydrogen propulsion development as technology maturation enables new application categories, including intercity transportation, remote area access, offshore operations, and defense missions requiring extended endurance beyond battery electric capabilities, substantially expanding the total addressable market opportunity and supporting diverse operator requirements across commercial, military, and emergency services segments.

Category-wise Analysis

Application Insights

Commercial applications command 50% market share encompassing air taxi services and delivery drones, driven by substantial urbanization creating demand for alternative transportation modes, bypassing ground congestion and e-commerce growth requiring rapid last mile logistics capabilities. Joby Aviation achieved Type Inspection Authorization positioning for commercial air taxi launch in the near term through Delta Air Lines partnership connecting airports to city centers across New York and Los Angeles markets, while Archer Aviation completed over 400 test flights of its Midnight eVTOL, demonstrating full transition envelope and targeting operations supporting United Airlines across San Francisco, Los Angeles, and Chicago metropolitan areas.

The air taxi segment benefits from airline partnerships providing established customer bases and operational infrastructure, while consumer surveys indicate 98% of airline fliers would consider using an eVTOL, reflecting strong market acceptance. The delivery drone component addresses logistics transformation as demonstrated by the United States air cargo sector processing 75.14 billion FTMs with companies pursuing eVTOL cargo applications for medical supply transport, e-commerce packages, and time-sensitive freight leveraging vertical takeoff capabilities, eliminating runway requirements and enabling direct facility-to-facility delivery, reducing ground transportation dependencies.

Emergency Medical Service represents the fastest segment encompassing air ambulance, medical cargo, and EMS operations driven by urgent healthcare access requirements and operational advantages over traditional helicopters.

Lift Technology Insights

Multirotor configurations command approximately 45% market share driven by mechanical simplicity enabling reliable operations, vertical takeoff and landing capabilities eliminating runway requirements, and hovering precision suitable for confined vertiport operations and urban environments. The multirotor design utilizes multiple propellers providing lift and control through differential thrust across rotors, creating inherent stability and control redundancy where individual motor failures do not result in complete loss of control authority enhancing safety for passenger and cargo operations.

The 19th Annual Electric Aircraft Symposium hosted by the Vertical Flight Society in Oshkosh, Wisconsin showcased leading North American eVTOL companies including Joby Aviation and Wisk highlighting testing of production configurations with multirotor architectures representing significant portion of designs progressing toward certification. The multirotor segment benefits from lower technical complexity compared to vectored thrust systems reducing certification challenges, established operational experience from unmanned drone applications providing validation of propulsion architecture reliability, and manufacturing scalability with simpler mechanical systems, reducing production costs, supporting commercial viability.

Vectored Thrust represents the fastest segment transitioning from vertical flight to wing-borne cruise flight through tilting rotors or propulsion units, enabling higher forward speeds and improved range efficiency compared to multirotor configurations. The Vertical Flight Society's World eVTOL Aircraft Directory surpassed 1,100 designs with significant North American contributionse including vectored thrust configurations from companies such as Joby Aviation and others pursuing higher performance capabilities. XTI Aerospace applauded the FAA's eVTOL Integration Pilot Program supporting development of its TriFan 600 powered lift aircraft for regional transportation, air medical, and defense applications, demonstrating industry momentum toward vectored thrust architectures.

Propulsion Type Insights

Battery electric propulsion commands 55% share driven by technological maturity with extensive automotive and consumer electronics battery development providing proven energy storage systems, zero direct emissions supporting urban environmental regulations, and lower operational complexity compared to hybrid alternatives. Joby Aviation and Archer Aviation both pursue battery electric architectures for their initial commercial platforms progressing through FAA certification, with Joby achieving Type Inspection Authorization and Archer completing over 400 test flights, demonstrating battery electric viability for urban air mobility applications.

Hydrogen Electric represents the fastest segment leveraging fuel cell technology converting hydrogen to electricity with only water vapor emissions, enabling extended range capabilities beyond battery limitations and rapid refueling supporting high utilization operations. Joby Aviation showcased its SHy4 hydrogen-powered aircraft, achieving a 561-mile flight at the H2 Aero Symposium, demonstrating substantial range improvements over battery electric platforms, addressing operational constraints for regional transportation and longer missions. Horizon Aircraft selected Pratt & Whitney's PT6A turboprop engine for its Cavorite X7, targeting enhanced range and efficiency while reducing emissions by 30%, with USD 2 million INSAT grant funding Project CRYSTAL development of all-weather capabilities expanding the operational envelope.

Competitive Landscape

The North America eVTOL aircraft market is consolidated, dominated by a few well-funded and technologically advanced players due to high entry barriers such as stringent safety regulations, certification requirements, and significant R&D investments. Leading companies like Joby Aviation, Archer Aviation, Beta Technologies, Bell Textron, Textron Inc., and Eve Holdings have established strong positions through prototype development, strategic partnerships, and early certification programs. Joby Aviation leads with its JAS4 model and extensive flight testing, while Archer Aviation focuses on public-private partnerships and pre-commercial agreements to secure future urban air mobility demand.

Beta Technologies targets both passenger and cargo eVTOL solutions with sustainable electric propulsion, and Bell Textron and Textron Inc. leverage decades of aerospace experience to develop hybrid-electric vertical lift aircraft. Eve Holdings, in collaboration with Embraer, emphasizes scalable urban air mobility solutions with certified safety systems. Market consolidation is further reinforced by mergers, acquisitions, and collaborations as companies compete for technological leadership and regulatory approval.

Key Developments:

- In December 2025, Archer Aviation collaborated with multiple cities to implement initial air taxi operations, including early deployment in Huntington Beach, California, aligning with the Department of Transportation’s National Advanced Air Mobility Strategy. This development positions Archer as a first-mover in commercial eVTOL services and directly impacts market adoption, infrastructure planning, and urban air mobility integration in North America.

- In July 2025, The symposium in Oshkosh, Wisconsin showcased leading North American eVTOL companies like Joby Aviation and Wisk, highlighting extensive testing of production configurations, hybrid-electric and hydrogen-electric propulsion advances, and regulatory support from the FAA and MOSAIC rules. This event emphasized technological readiness and industry momentum in the U.S., reinforcing investor confidence and market growth potential.

- On January 20, 2026, Eve Air Mobility secured $150 million in debt financing to accelerate eVTOL development, certification, and commercialization, reinforcing its position in the U.S. Urban Air Mobility market and enabling the company to scale operations, strengthen partnerships, and advance its integrated eVTOL ecosystem across North American cities.

Companies Covered in North America eVTOL Aircraft Market

- Joby Aviation

- Archer Aviation

- Beta Technologies

- Bell Textron

- Textron Inc.

- Eve Holdings

- Kitty Hawk

- Volocopter GmbH

- Lilium GmbH

- Airbus S.A.S.

- EHang

- Urban Aeronautics

Frequently Asked Questions

North America eVTOL Aircraft is projected to be valued at US$ 0.5 Bn in 2026.

The Commercial (Air taxi, Delivery drones) segment is expected to account for approximately 50% of the North America eVTOL Aircraft by Application in 2026.

The market is expected to witness a CAGR of 30.2% from 2026 to 2033.

North America eVTOL Aircraft growth is driven by urban congestion and logistics infrastructure transformation, robust federal regulatory support including FAA pilot programs and executive mandates, and technological innovation from leading players like Joby Aviation, Archer Aviation, and BETA Technologies.

Key market opportunities in North America eVTOL Aircraft lie in integration with existing aviation and logistics networks for passenger and cargo operations, strategic airline partnerships for rapid commercial deployment, and advancements in hydrogen-electric propulsion enabling longer-range and diverse mission profiles.

Key players in eVTOL Aircraft include Joby Aviation, Archer Aviation, Beta Technologies, Bell Textron, Textron Inc., Eve Holdings, Kitty Hawk.