- Retail

- Mono Material Pump Market

Mono Material Pump Market Size, Share, and Growth Forecast 2026 - 2033

Mono Material Pump Market by Material Type (Polyethylene (PE), Polypropylene (PP), Polyolefin, Polyethylene Terephthalate (PET), Poly Vinyl Chloride (PVC), Metal, Others), Pump Type (Lotion Pumps, Spray Pumps, Foam Pumps, Others), Dispense Capacity (Up to 1 cc, 1 cc to 2 cc, Above 2 cc), Application (Beauty & Personal Care, Homecare Products, Food & Beverage, Pharmaceuticals, Others), Distribution Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Mono Material Pump Market Size and Trend Analysis

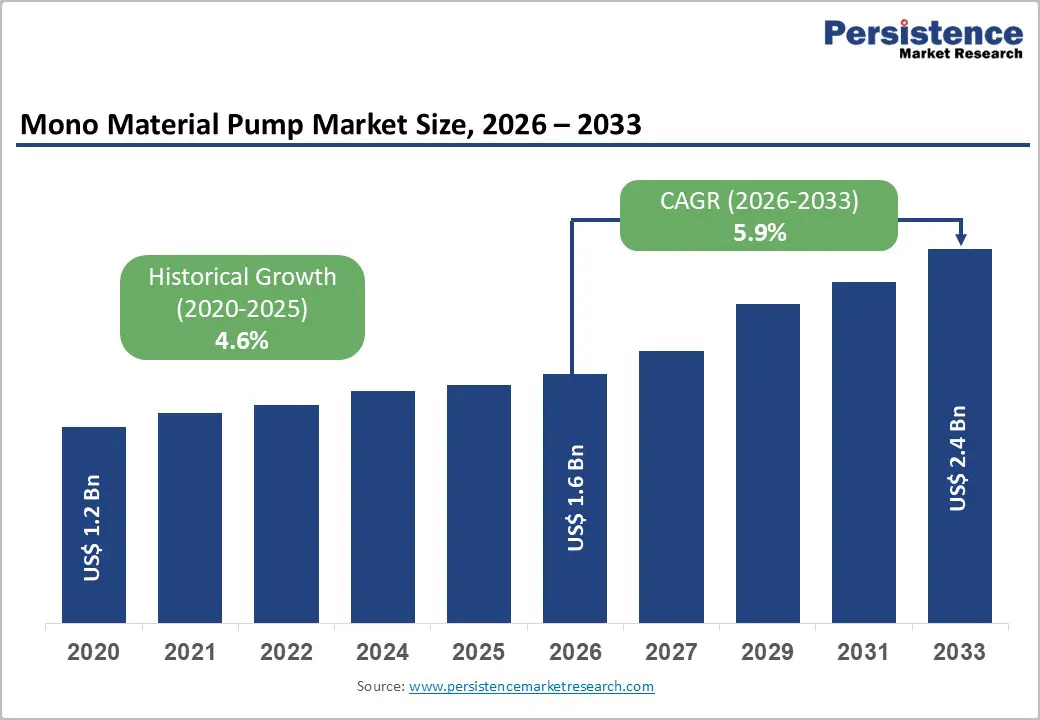

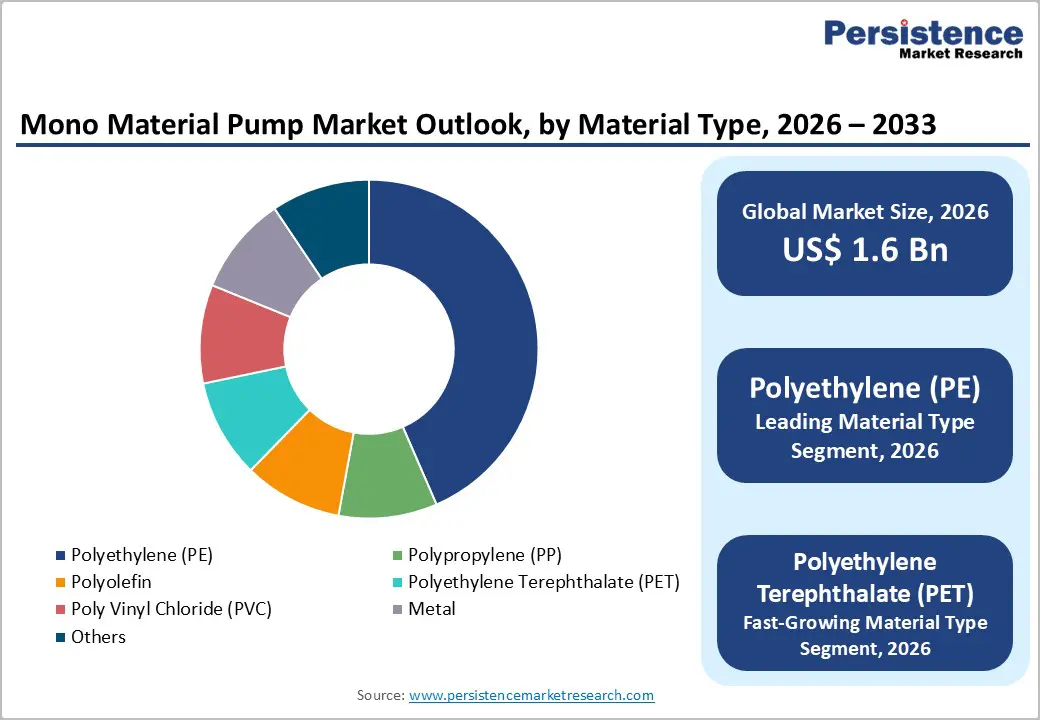

The global mono material pump market size is expected to be valued at US$ 1.6 billion in 2026 and projected to reach US$ 2.4 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

This robust growth trajectory is primarily driven by stringent regulatory frameworks that mandate recyclable packaging across major economies. The European Union’s Packaging and Packaging Waste Regulation (EU) 2025/40, which entered into force in February 2025, establishes legally binding targets requiring all packaging on the EU market to be recyclable in practice and at scale by 2030, with minimum recycled content thresholds ranging between 30% and 65% for various plastic packaging types by 2030, increasing to 50%-65% by 2040.

Key Industry Highlights:

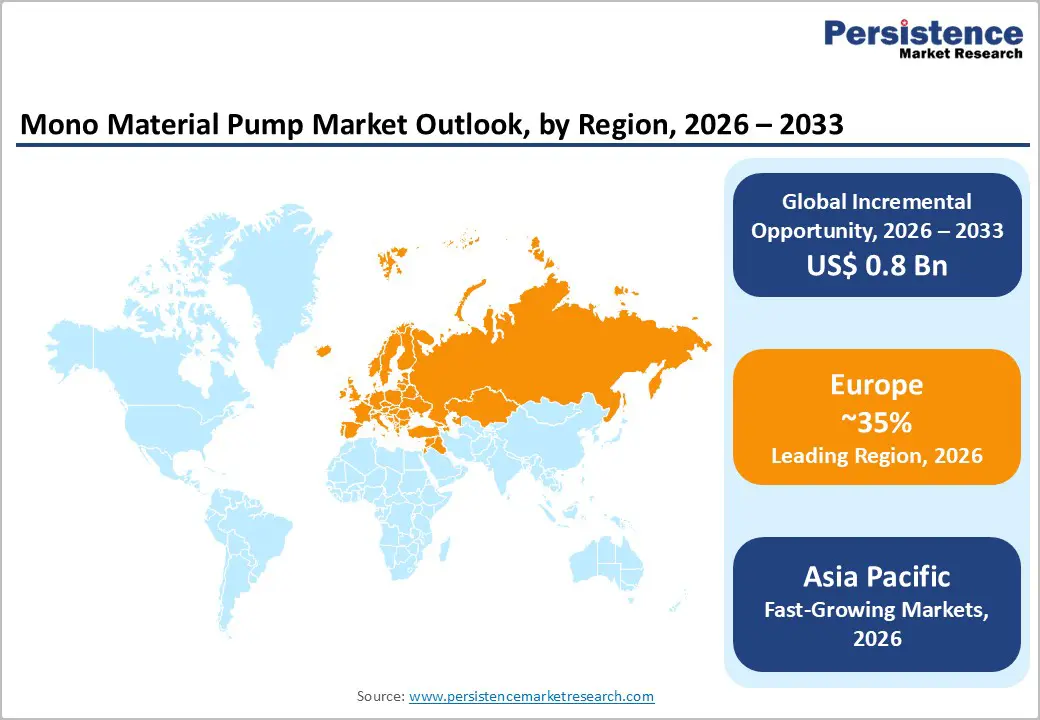

- Leading Region: Europe maintains market leadership with approximately 35% share in 2025, driven by the EU Packaging and Packaging Waste Regulation (PPWR) requiring all packaging to be recyclable by 2030 with minimum recycled content thresholds of 30-65% by 2030 and 50-65% by 2040, creating the world’s most stringent regulatory framework for sustainable packaging.

- Fastest Growing Region: Asia Pacific represents the fastest-growing region with a projected CAGR of 7.2% from 2026 - 2033, fueled by China’s beauty and personal care packaging market growing at 10.5% CAGR through 2035, India’s EPR framework mandating 100% plastic recovery by 2026, and expanding middle-class consumption across ASEAN markets.

- Dominant Segment: Polyethylene (PE) dominates the material type segment with a 42% market share in 2025, preferred for its compatibility with PE and PET bottles, enabling complete package recyclability, proven performance across 3,000+ dispensing cycles, and the ability to incorporate PCR content that meets emerging recycled material mandates.

- Emerging Segment: Homecare product applications are the fastest-growing segment, with a 6.8% CAGR from 2026 - 2033, driven by the expanding adoption of recyclable trigger spray pumps for surface cleaning, growing consumer demand for sustainable household products, and progressive retailer sustainability standards requiring recyclable dispensing systems.

- Key Trend: Innovation in bio-based and PCR materials presents the most significant market opportunity, with the European Commission reviewing bio-based plastic packaging by February 2028 for potential legislative allowances, major brands seeking pumps with 30-50% PCR content to meet circular economy commitments, and technical validation of ISCC-certified recycled and bio-resins in precision dispensing applications.

| Key Insights | Details |

|---|---|

| Mono Material Pump Market Size (2026E) | US$ 1.6 billion |

| Market Value Forecast (2033F) | US$ 2.4 billion |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Stringent Global Packaging Regulations Mandating Recyclability

The implementation of comprehensive packaging waste regulations worldwide has emerged as the most significant driver for mono-material pump adoption. The EU Packaging and Packaging Waste Regulation (PPWR) requires that by January 1, 2030, all plastic packaging must contain specified minimum percentages of recycled content recovered from post-consumer plastic waste, with 30% for contact-sensitive PET packaging and 10% for other plastic materials, escalating to 50% and 25% respectively by 2040. Furthermore, the regulation mandates that all packaging placed on the EU market must be recyclable, with design-for-recycling criteria becoming enforceable from 2030 and large-scale recyclability requirements from 2035.

China’s amended green packaging regulation, enforced from June 1, 2025, focuses on reducing packaging waste in the delivery sector, with the express delivery industry handling over 175 billion parcels in 2024. India’s Extended Producer Responsibility (EPR) framework for plastic packaging includes recovery targets ramping up to 100% by 2026, with recycled content requirements starting in 2025. These regulatory frameworks have compelled packaging manufacturers and consumer goods companies to transition from traditional multi-material pumps containing metal springs to mono-material alternatives constructed entirely from polyethylene (PE) or polypropylene (PP), which can be efficiently processed through existing recycling infrastructure.

Growing Consumer Preference for Sustainable Beauty and Personal Care Products

The beauty and personal care industry is undergoing a fundamental shift in consumer purchasing behavior, with sustainability attributes becoming a primary driver of purchase decisions. According to the Statistics Bureau of Japan, revenue from the beauty industry, including makeup and skincare products, reached US$18.12 billion by the end of 2024, a 2.89% increase from 2023, with a significant portion attributed to products with sustainable packaging. The Flexible Packaging Association reports that only 5% of traditional flexible packaging is recycled, highlighting the critical need for improved recyclability in dispensing systems.

Major beauty brands have established ambitious sustainability targets, with Dermalogica committing to 100% reusable, recyclable, or compostable bottles by 2025, successfully implementing AptarGroup’s fully recyclable polyethylene dispensing pump that received an “A” rating from RecyClass and recognition from the Association of Plastics Recyclers (APR) for meeting the Design Meets Preferred Guidance program requirements. AptarGroup, as a member of the Ellen MacArthur Foundation’s New Plastics Economy Global Commitment, pledged to achieve 100% recyclable, reusable, or compostable plastic packaging for dispensing solutions across beauty, personal care, home care, and food and beverage markets by 2025, with a commitment to incorporate 10% recycled content in dispensing solutions.

Restraints - Higher Manufacturing Costs and Technical Complexity

The transition to mono-material pump designs presents significant financial and technical challenges for manufacturers. Traditional pumps utilize metal springs and multi-material components that have been optimized over decades for cost-efficiency and performance reliability. Mono-material alternatives require substantial research and development investment to engineer plastic springs and actuators that deliver comparable dispensing performance, durability, and user experience.

AptarGroup reported spending more than two years on design, engineering, and testing before successfully launching the Future pump, their first fully recyclable mono-material solution. The development process requires specialized expertise in polymer science, precision molding technologies, and rigorous testing protocols to ensure dispensing durability of 3,000+ cycle times, which is essential for finishing 1-liter refill pouches used 6 times.

Limited Recycling Infrastructure in Emerging Markets

While mono-material pumps offer superior recyclability in theory, the practical realization of these environmental benefits depends critically on the availability of appropriate collection, sorting, and processing infrastructure. In many emerging economies across the Asia Pacific, Latin America, the Middle East & Africa, recycling systems remain underdeveloped, fragmented, or non-existent. Australia currently faces a low 20% recovery rate for plastic packaging, prompting large-scale reform of current packaging regulation frameworks. The United States generates more than 40 million tons of municipal plastic waste annually, with at least 80% likely to be sent to landfill sites, indicating a practically stagnant plastic recycling rate.

In regions lacking adequate recycling infrastructure, even perfectly recyclable mono-material pumps may end up in landfills or incinerators, negating their environmental advantages and potentially undermining consumer trust in sustainability claims. This infrastructure deficit also creates uncertainty for brands investing in premium-priced sustainable packaging solutions, as the value proposition depends on the successful end-of-life recovery and reprocessing of these materials. The misalignment between regulatory ambitions and operational capabilities in waste management systems represents a significant barrier to achieving the full market potential of mono-material pump technologies.

Opportunity - Expansion in Homecare and Surface Cleaning Product Segments

The home care products category presents a substantial growth opportunity for mono-material pump manufacturers, driven by the increasing adoption of sustainable packaging across household cleaning, surface care, and fabric care applications. The home care segment offers distinct advantages, including higher-volume consumption patterns, lower regulatory barriers than pharmaceutical applications, and growing consumer awareness of cleaning product sustainability. Major retailers, including Sephora, Ulta, and Credo, have established progressive sustainability standards for products carried in their stores, creating commercial pressure for brands to adopt recyclable dispensing systems.

The convergence of regulatory requirements, retailer expectations, and consumer preferences is driving rapid formulation changes in cleaning products, with brands increasingly selecting mono-material pumps to communicate environmental responsibility. Furthermore, the trend toward concentrated refill formats and larger-capacity dispensers in homecare applications aligns well with the technical capabilities of mono-material pump designs, which can accommodate various dispense volumes and viscosity ranges while maintaining recyclability credentials.

Innovation in Bio-Based and Post-Consumer Recycled (PCR) Materials

The integration of bio-based feedstocks and post-consumer recycled content into mono-material pump manufacturing represents a transformative opportunity to enhance sustainability credentials while addressing circular economy objectives. The European Commission is required to review the state of technological development and environmental performance of bio-based plastic packaging by February 12, 2028, and to consider potential legislative proposals allowing bio-based feedstocks to replace post-consumer plastic waste in meeting recycled-content targets, where suitable recycling technologies for food-contact packaging are unavailable.

The New Plastics Economy Global Commitment framework encourages brands to increase recycled content across their packaging portfolios, thereby creating demand for pumps manufactured from PCR PE or PCR PP. Additionally, precision fermentation and vertical farming technologies are becoming mainstream, enabling beauty brands to produce bio-synthetic ingredients with minimal environmental impact, and complementary bio-based packaging materials offer a cohesive sustainability narrative. Market participants who successfully develop mono-material pumps incorporating 30-50% PCR content or bio-based polymers while maintaining performance standards will gain significant competitive advantages in securing contracts with sustainability-focused brands across beauty, personal care, and home care segments.

Category-wise Analysis

Material Type Insights

Polyethylene (PE) holds the leading position in the mono-material pump market, accounting for approximately 42% of the market in 2025, due to its superior recyclability and compatibility with existing polyolefin recycling streams. Its technical flexibility enables the development of durable plastic springs and actuators that can withstand more than 3,000 dispensing cycles while maintaining consistent dosing performance. PE integrates efficiently with commonly used bottle materials such as PET, supporting fully recyclable packaging systems.

The material also incorporates post-consumer recycled and bio-based content, aligning with circular-economy objectives. As regulatory mandates for recycled content intensify through 2030, PE-based mono-material pumps are expected to experience sustained demand growth.

Pump Type Insights

Lotion pumps constitute the largest pump type segment, accounting for approximately 38% of the market in 2025, primarily driven by extensive use across skincare, body care, and cosmetic formulations. Their dominance stems from the high frequency of lotion-based product use, which requires precise and hygienic dispensing mechanisms. The shift from traditional multi-material designs to mono-material constructions has enhanced recyclability without compromising product protection or user convenience.

Mono-material lotion pumps provide a consistent dosage suitable for creams, hand lotions, and liquid soaps, aligning with sustainability targets set by major beauty brands. As companies pursue fully recyclable packaging portfolios by 2025-2030, this segment is positioned for continued expansion.

Dispense Capacity Insights

The 1 cc to 2 cc dispense capacity segment dominates the market, accounting for nearly 45% of the market in 2025, reflecting its optimal balance between functional efficiency and product economy. This range provides sufficient volume for single-use applications while minimizing product waste and extending container lifespan. It supports a range of viscosities, from lightweight serums to thick creams, ensuring broad formulation compatibility. Additionally, this capacity aligns with long-established consumer usage patterns, eliminating the need for behavioral adaptation when transitioning to sustainable pump alternatives. Its ability to serve both premium and mass-market personal care products reinforces its leadership position within mono-material pump configurations.

Application Insights

Beauty and personal care applications account for approximately 48% of the mono material pump market in 2025, driven by strong sustainability commitments and frequent product replenishment cycles. The sector’s emphasis on recyclable packaging and environmental transparency has accelerated the adoption of mono-material dispensing solutions. Skincare and personal hygiene products require controlled, hygienic dispensing systems, making mono-material pumps a strategic fit.

Furthermore, the segment benefits from premium pricing structures that can absorb incremental costs associated with sustainable packaging. As major brands integrate circular economy principles into packaging design, demand from beauty and personal care applications is expected to remain dominant.

Distribution Channel Insights

Offline distribution channels lead the market with nearly 58% share in 2025, supported by the continued relevance of physical retail environments in personal care purchasing decisions. Supermarkets, specialty beauty stores, and pharmacies enable product testing, tactile evaluation, and immediate purchase fulfillment, which are critical in influencing consumer choice. Packaging aesthetics and dispensing functionality are directly experienced at the point of sale, thereby reinforcing the value proposition of mono-material pumps.

Although e-commerce penetration is expanding, physical retail remains a primary sales channel. Consequently, mono-material pump manufacturers continue to prioritize compatibility with traditional retail distribution channels.

Regional Insights

North America Mono Material Pump Market Trends and Insights

North America represents a mature and innovation-driven mono material pump market, led by the United States. Growth is supported by strong demand from the beauty and personal care sector, increasing preference for organic and natural products, and rising adoption of sustainable packaging formats. The expansion of Extended Producer Responsibility (EPR) legislation across multiple U.S. states is creating a progressively stringent regulatory environment that favors recyclable mono material dispensing solutions. Advanced manufacturing ecosystems in California, New York, and Texas enable the rapid commercialization of sustainable pump technologies.

Premiumization trends further strengthen adoption, as consumers are willing to pay higher prices for products with verified recyclability credentials. Additionally, the expansion of e-commerce and direct-to-consumer channels requires durable yet recyclable pump designs that can withstand logistics stress. Strategic collaborations between packaging suppliers and technology providers are enhancing PCR integration and cost efficiency, reinforcing long-term regional growth prospects.

Europe Mono Material Pump Market Trends and Insights

Europe is the most regulation-driven regional market, with adoption strongly influenced by the EU ackaging and Packaging Waste Regulation (PPWR), which mandates recyclability and targets for increasing recycled content through 2030 and beyond. These requirements are accelerating the transition from multi-material to mono-material pump systems that meet strict design-for-recycling criteria. Germany remains a technological leader in sustainable packaging innovation, while Italy demonstrates strong growth in premium and luxury packaging segments.

Third-party validation through RecyClass certification strengthens market credibility and speeds brand conversion. Major European beauty and consumer goods companies, including L’Oréal, Beiersdorf, and Henkel, have committed to fully recyclable packaging portfolios, reinforcing demand for compliant mono-material dispensing solutions. Harmonized labeling and recyclability standards across EU member states further create a unified and opportunity-rich market landscape.

Asia Pacific Mono Material Pump Market Trends and Insights

Asia Pacific is the fastest-growing mono material pump market, supported by the rapid expansion of beauty and personal care consumption, urbanization, and tightening environmental regulations. China leads regional growth, driven by premiumization trends, strong e-commerce penetration, and new green packaging mandates linked to its large-scale logistics sector. Domestic manufacturers are upgrading automation and precision molding capabilities to deliver recyclable and performance-oriented pump solutions.

India shows the highest growth potential, supported by rising disposable incomes and an evolving EPR framework that sets ambitious recycling and recycled-content targets. Japan’s mature beauty market continues to demand packaging solutions that combine aesthetic appeal with environmental responsibility. Meanwhile, ASEAN countries provide cost-efficient manufacturing bases with expanding technical capabilities, positioning the region as both a high-growth consumption market and a global production hub supplying Europe and North America.

Competitive Landscape

The mono material pump market is moderately consolidated, characterized by a mix of global packaging conglomerates and niche sustainable packaging innovators. Large players benefit from integrated manufacturing networks, advanced R&D infrastructure, and established relationships with multinational consumer goods companies, creating high entry barriers for smaller participants. Product development cycles are resource-intensive, requiring significant investment in engineering, material science, and performance testing to meet recyclability and durability standards.

Competition is increasingly strategy-driven, centered on certified recyclability, incorporation of post-consumer recycled and bio-based resins, and compatibility with e-commerce distribution requirements. Companies are prioritizing design-for-recycling principles while maintaining dispensing precision across diverse viscosities. Strategic partnerships with resin suppliers ensure stable access to certified sustainable materials, while co-development agreements with brand owners enable customized, application-specific solutions. The market is also witnessing rising merger and acquisition activity, as larger firms expand sustainable technology portfolios and smaller innovators seek scale, geographic expansion, and production capacity enhancement.

Key Developments:

- September, 2024: ALPLAhana unveiled a new mono-material dispenser pump with an innovative down-lock function made entirely of polypropylene, enhancing recyclability and reducing components for liquid dispensers ahead of its Beautyworld Middle East debut.

- October, 2024: Virospack unveiled its first fully recyclable monomaterial Eco-Pump made entirely from polypropylene (PP) to simplify recycling and support sustainable beauty and personal care packaging.

Companies Covered in Mono Material Pump Market

- APackaging Group

- AptarGroup, Inc.

- SeaCliff Beauty

- Rieke Packaging Corp. (TriMas Packaging)

- Albéa Beauty Holdings S.à.r.l. (Fasten)

- CVP Packaging

- O.Berk Company

- DTS-EUROPE (Wista Packaging)

- ZHEJIANG UKPACK PACKAGING CO. LTD.

- SR Packaging

- FusionPKG

- Lumson S.p.A.

- Berlin Packaging

- Quadpack Industries

- HCP Packaging

Frequently Asked Questions

The global mono material pump market is projected to reach US$ 1.6 billion in 2026, supported by steady growth in sustainable packaging adoption.

The market is driven by stringent recyclability regulations under the EU Packaging and Packaging Waste Regulation (PPWR) and rising consumer demand for sustainable beauty and personal care packaging.

Europe leads the market with around 35% share in 2025, driven by strict PPWR regulations and strong brand sustainability commitments.

Expansion into homecare and surface cleaning applications, along with higher PCR and bio-based resin integration, represents the key growth opportunity.

Key participants include AptarGroup Inc., Albéa Beauty Holdings, Rieke Packaging Corp., Berlin Packaging, and Quadpack Industries.