- Plastics, Polymers & Resins

- Pure Monomer Resin Market

Pure Monomer Resin Market Size, Share, and Growth Forecast, 2026 - 2033

Pure Monomer Resin Market by Product Type (Acrylic, Styrene, Vinyl, Others), Application (Adhesives, Coatings, Sealants, Others), End-user (Automotive, Construction, Electronics, Packaging, Others), and Regional Analysis for 2026 – 2033

Pure Monomer Resin Market Size and Trends Analysis

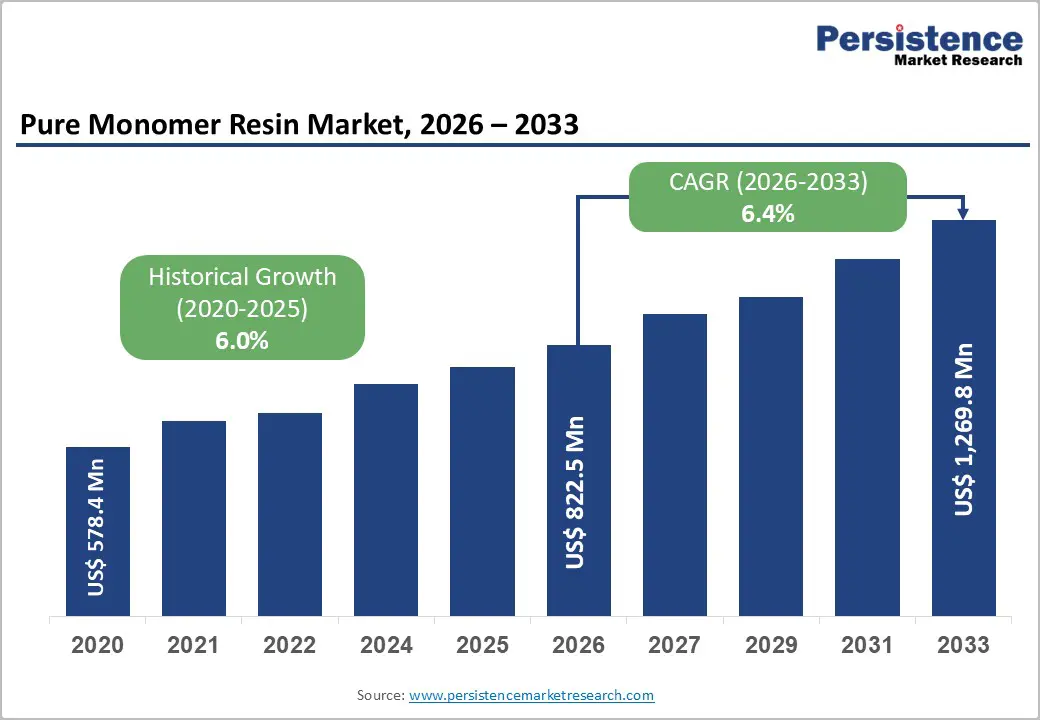

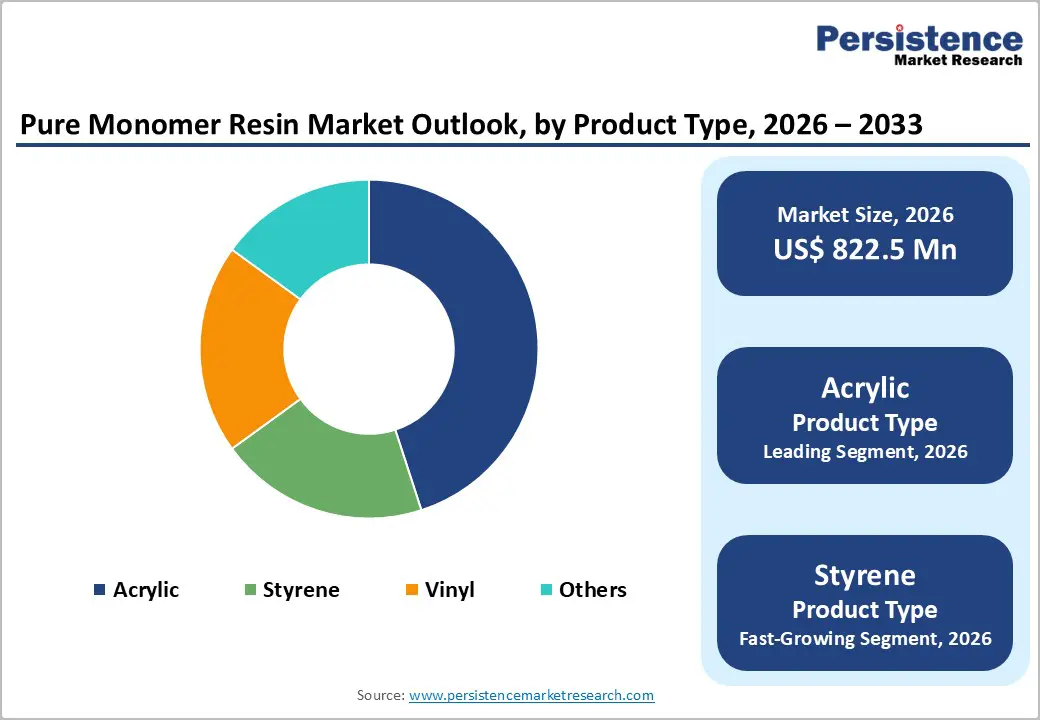

The global pure monomer resin market size is likely to be valued at US$822.5 million in 2026, and is expected to reach US$1,269.8 million by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by the increasing prevalence of high-performance adhesives and coatings demand, rising applications in automotive and construction sectors, and growing adoption of styrene and acrylic resins for enhanced durability. Advances in low-VOC formulations and bio-based monomer alternatives are further increasing uptake by improving environmental compliance and performance. Increasing recognition of pure monomer resins as critical for adhesion strength, weather resistance, and cost efficiency in emerging electronics and packaging markets remains a major driver of market growth.

Key Industry Highlights:

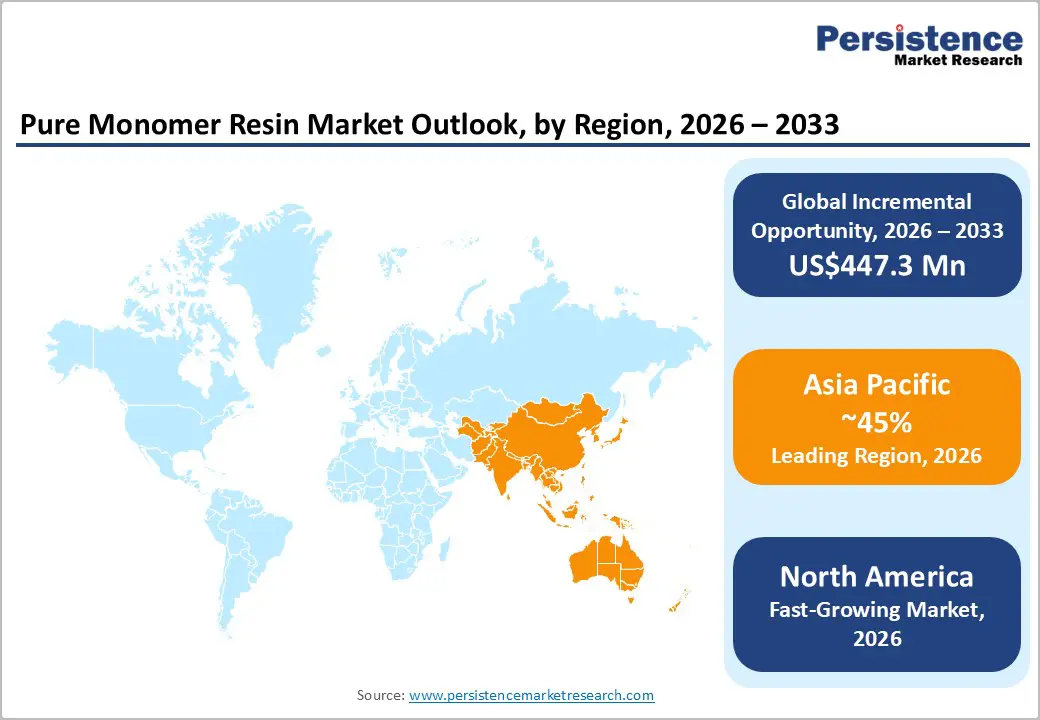

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by rapid industrialization, strong adhesives demand, and expanding automotive production in China and India.

- Fastest-growing Region: North America, fueled by rising demand for low-VOC and bio-based resins across automotive, electronics, and sustainable construction applications.

- Dominant Product Type: Acrylic, to hold approximately 45% of the market share, as it remains the preferred choice for high-performance adhesives and coatings.

- Leading Application: Adhesives, which account for nearly 48% of market revenue, owing to extensive use in automotive and construction bonding.

- Regulatory Advancement on Low-VOC Resin Use in the U.S.: The U.S. Environmental Protection Agency (EPA) implemented National VOC emission standards for architectural coatings and industrial resin products to reduce ground-level ozone and improve air quality. These regulations have accelerated the shift toward low-VOC pure monomer resins, encouraging compliant and more sustainable manufacturing practices.

| Global Market Attributes | Key Insights |

|---|---|

| Pure Monomer Resin Market Size (2026E) | US$822.5 Mn |

| Market Value Forecast (2033F) | US$1,269.8 Mn |

| Projected Growth CAGR (2026-2033) | 6.4% |

| Historical Market Growth (2020-2025) | 6.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Demand in Automotive and Construction Sectors

Growth in the automotive and construction sectors has become a major driver of the pure monomer resin market, as these industries consume advanced polymer materials for performance-critical applications. Vehicle manufacturing extensively uses resins in lightweight components such as interior trims, bumpers, and structural parts, thereby supporting fuel efficiency and strength requirements in both conventional and electric vehicles. India’s automotive sector produced over 28 million vehicles in FY-2023-24, making it one of the world’s largest producers and indicating substantial downstream demand for polymer-based materials used in assembly and component production.

Construction industry expansion further increases resin demand, as infrastructure and building projects require durable, weather-resistant adhesives, coatings, sealants, and composite materials formulated from pure monomer resins. Government capital expenditure on construction and infrastructure in India reached US$133 billion in fiscal year 2024-25, equivalent to about 3.4% of GDP, reflecting significant public investment in housing, urban development, and public works. These large and growing end-use markets drive resin manufacturers to innovate and scale production of pure monomer resins tailored to the mechanical performance, chemical resistance, and long-term stability demanded in automotive and construction applications.

Focus on Low-VOC and Sustainable Formulations

Regulatory pressure and consumer demand for healthier indoor environments are driving formulators and manufacturers toward low-VOC (volatile organic compound) and more sustainable resin solutions. In coatings, adhesives, sealants, and elastomers, traditional high-VOC systems contribute to indoor air pollution and can exceed permitted emissions limits in residential and commercial buildings. Low-VOC resins reduce harmful emissions during application and throughout the product's life cycle, improving air quality for occupants and helping builders and manufacturers meet tightening environmental and health standards. For example, U.S. Environmental Protection Agency (EPA) regulations set national emissions standards for hazardous air pollutants from industrial coatings and other resin-based products to control VOC output, influencing material selection and reformulation across industries.

Sustainable formulations also incorporate renewable feedstocks, recyclable polymers, and designs that enhance end-of-life recovery, aligning with corporate sustainability commitments and circular economy principles. Manufacturers are reformulating products to minimize reliance on non-renewable raw materials while maintaining performance characteristics such as adhesion strength, durability, and weather resistance. This trend enables brands to differentiate offerings in markets increasingly driven by environmental credentials and green building certifications such as LEED and WELL. Improved sustainability performance enhances market acceptance, supports regulatory compliance, and fosters long-term growth as industries shift toward lower-impact materials in construction, automotive, packaging, and consumer goods applications.

Barrier Analysis – Health and Safety Concerns

Workplace exposure to unreacted monomers and related chemicals during the production and processing of pure monomer resins poses significant health and safety risks that constrain market growth. Regulatory agencies such as the U.S. Occupational Safety and Health Administration (OSHA) list hazardous substances such as styrene, which is widely used in resin manufacturing, as potential occupational hazards that can irritate the skin, eyes, and respiratory tract, as well as central nervous system effects, including headache and fatigue, with prolonged exposure. Agencies have set permissible exposure limits (PELs) to mitigate risk, such as an OSHA limit of 50 ppm for styrene averaged over an 8-hour work shift, which requires careful monitoring and control in industrial settings to protect employees.

Exposure control adds complexity and cost for resin producers, who must invest in ventilation, personal protective equipment, training, and monitoring systems to ensure compliance with health and safety standards. These safety measures are essential because monomer vapors and other hazardous air pollutants emitted during resin production are subject to regulations under the U.S. Environmental Protection Agency's National Emission Standards for Hazardous Air Pollutants (NESHAP), which aim to limit toxic emissions from polymers and resins. Ensuring worker safety while maintaining production efficiency increases operational burden and can limit expansion, especially for smaller manufacturers facing tight margins.

Competition from Alternative Materials

Competition from alternative materials presents a significant restraint on the pure monomer resin market by reducing demand for traditional petrochemical-based resins and shifting customer preferences toward more sustainable options. Innovations in bio-based polymers, recycled plastics, and engineered composites offer performance characteristics that exceed those of conventional resins in applications such as coatings, adhesives, and engineered plastics. These alternatives often appeal to manufacturers and end users who prioritize environmental impact, regulatory compliance, and circular-economy principles, thereby diverting market share away from pure monomer resins derived predominantly from non-renewable feedstocks.

The rise of such alternatives also influences strategic sourcing and product development in key end-use industries, including automotive, construction, and packaging. OEMs and brand owners are increasingly incorporating bio-polymers and recycled resin blends to meet internal sustainability targets, reduce carbon footprints, and align with consumer expectations for greener products. As technology improves, cost differentials between traditional monomer resins and alternative materials are narrowing, strengthening the competitive position of bio-based and recycled solutions.

Opportunity Analysis –Bio-Based and Low-VOC Pure Monomer Resins

Growing interest in bio-based and low-VOC (volatile organic compound) pure monomer resins represents a strong opportunity for market expansion, as industries seek materials that align with environmental, health, and regulatory priorities. Bio-based resins are derived from renewable resources such as plant oils, sugars, and biomass, thereby reducing dependence on finite petrochemical feedstocks and supporting circular-economy goals. According to the U.S. Environmental Protection Agency, the National VOC standards for architectural coatings are estimated to reduce VOC emissions by about 113,500 tons per year, reflecting the regulatory drive toward lower?VOC formulations in coatings and related resin applications. These limits encourage the adoption of compliant low-VOC materials in industrial and consumer products.

Low-VOC resin formulations improve indoor and industrial air quality. The U.S. Environmental Protection Agency regulates VOC emissions through programs such as the National Volatile Organic Compound Emission Standards, which drive manufacturers to develop coatings, adhesives, and sealants with reduced VOC content to meet compliance thresholds. These trends create market opportunities for pure monomer resin producers to develop formulations that combine high performance with lower environmental impact and regulatory compliance.

Electronics and Packaging Applications

The growing demand for high-performance materials in electronics and packaging is creating significant opportunities for the pure monomer resin market. In electronics, resins are widely used as encapsulants, adhesives, coatings, and circuit board materials to provide insulation, chemical resistance, and thermal stability. Advanced monomer resins ensure reliable performance under high temperatures and electrical loads, supporting miniaturization and durability in devices such as smartphones, laptops, and consumer electronics. Governments and industries are emphasizing safety and longevity standards, which drives the adoption of resins with consistent purity and predictable properties to prevent failure in sensitive electronic components.

In the packaging sector, monomer resins are critical for producing durable, lightweight, and chemically resistant films, containers, and laminates. Food and beverage packaging increasingly demands materials that maintain product integrity, extend shelf life, and comply with regulatory standards for food contact. The U.S. Food and Drug Administration (FDA) regulates resin-based food packaging, ensuring that materials are safe and meet performance criteria, thereby supporting the growth of high-quality monomer resin applications. These applications, ranging from electronic components to consumer packaging, drive innovation in resin formulations with tailored mechanical, thermal, and chemical properties, thereby expanding the market for pure monomer resins across multiple high-value industries.

Category-wise Analysis

Product Type Insights

Acrylic is expected to dominate the market, accounting for approximately 45% of the market in 2026, driven by its versatility and widespread industrial applications. They offer excellent clarity, weather resistance, UV stability, and chemical resistance, making them ideal for coatings, adhesives, sealants, electronics, and packaging applications. Acrylic resins also enable the formulation of low-VOC and high-performance solutions, aligning with regulatory and sustainability trends. DIC Corporation’s acrylic resin product line includes acrylic binders and emulsions used extensively in coatings, adhesives, and industrial applications. DIC’s acrylic resins are designed for automotive, architectural, and electronics coatings, offering transparency, weather resistance, and durability across a range of industrial settings.

Styrene is the fastest-growing product type, with broad applicability across industries. It serves as a key monomer for producing polystyrene, ABS, and other copolymers used in packaging, automotive components, construction materials, and electrical appliances. Styrene’s high reactivity, excellent thermal and chemical resistance, and versatility in molding and extrusion processes make it suitable for high-performance applications. For example, manufacturers such as Kolon Industries are developing styrene grades targeting EV components, enabling highly robust delivery, and showing promising results in thermal-resistance studies for advanced applications. INEOS Styrolution is a global leader in styrenics. INEOS Styrolution produces and supplies styrene monomer and styrenic polymers, including polystyrene, ABS, and SAN, which are widely used in packaging, automotive parts, electronics housings, and consumer products. These materials are valued for their strength, heat resistance, and ease of processing, which underpin strong demand across multiple industries.

End-user Insights

Automotive is expected to dominate the market, contributing nearly 35% of revenue in 2026, driven by the need for lightweight, durable, and high-performance materials. Resins are extensively used in interior components, bumpers, exterior trims, adhesives, and coatings, improving fuel efficiency, structural strength, and aesthetic appeal. Growth in electric and hybrid vehicle production further increases demand for polymers with excellent thermal and chemical resistance. Ford Motor Company uses advanced polymer composites in vehicle production to improve fuel economy and performance. The U.S. Department of Energy reports that the use of plastics and composite materials in light vehicles increased by almost 40% between 1995 and 2014, reflecting the growing shift toward resin-based components in automotive manufacturing.

Electronics is the fastest-growing end user, driving demand for high-performance, durable, and heat-resistant materials in devices. Resins are widely used in printed circuit boards, encapsulants, adhesives, coatings, and insulating components to ensure reliability, chemical resistance, and thermal stability in smartphones, laptops, consumer electronics, and industrial equipment. Rapid growth in miniaturization, wearable electronics, and IoT devices is driving demand for resins that enable compact designs without compromising performance. Huntsman Corporation’s epoxy resin portfolio is widely used to encapsulate, insulate, and protect circuit boards and electronic components in devices such as computers, smartphones, and industrial electronics. Epoxy resins from Huntsman are formulated to provide excellent electrical insulation, thermal stability, and moisture resistance, key performance attributes required in modern electronics assemblies.

Regional Insights

North America Pure Monomer Resin Market Trends

North America is projected to be the fastest-growing segment, driven by advanced manufacturing, strong research and development capabilities, and high public awareness of performance benefits. Distribution systems in the U.S. and Canada provide extensive support for pure monomer resin programs, ensuring wide accessibility across acrylic, adhesives, and automotive populations. Increasing demand for high-performance, convenient, and easy-to-formulate forms is further accelerating adoption, as these formats improve efficiency and reduce barriers associated with traditional resins.

Innovation in pure monomer resin technology, including stable bio-based resins, improved low-VOC delivery, and targeted electronics enhancement, is attracting significant investment from both the public and private sectors. Government initiatives and EPA campaigns continue to promote use to mitigate environmental risks, performance concerns, and emerging sustainability threats, thereby creating sustained market demand. The growing focus on construction grades and specialty uses, particularly for adhesives and others, is expanding the target applications for pure monomer resins.

Europe Pure Monomer Resin Market Trends

Europe is supported by increasing awareness of the sustainable and performance benefits, robust regulatory systems, and government-led circular-economy programs. Countries such as Germany, France, the U.K., and Italy have well-established industrial frameworks that support routine pure monomer resin use and encourage adoption of innovative resin delivery methods, including bio-based and low-VOC solutions. These high-compliance formulations are particularly appealing to adhesive manufacturers, regulatory-conscious manufacturers, and coatings users, improving performance and coverage rates.

Technological advancements in pure monomer resin development, such as enhanced biosynthesis, application-specific delivery, and improved styrene grades, are further enhancing market potential. European authorities are increasingly supporting research and trials of resins for both routine and specialized applications, thereby strengthening market confidence. The growing emphasis on convenient, eco-friendly options aligns with the region’s focus on reducing VOC emissions and industrial sustainability. Public awareness campaigns and promotional drives are expanding reach in both the automotive and construction sectors, while suppliers are investing in sustainable feedstocks and novel variants to enhance efficacy.

Asia Pacific Pure Monomer Resin Market Trends

Asia-Pacific is expected to dominate, accounting for 45% of revenue in 2026, driven by rising industrialization awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting resin campaigns to address manufacturing growth and emerging performance needs. Pure monomer resins are particularly attractive in these regions due to their cost-effective administration, ease of integration, and suitability for large-scale automotive and electronics drives in both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-deploy pure monomer resins that withstand challenging production conditions and minimize cost dependence. These innovations are critical for reaching domestic manufacturers and improving overall coverage. Growing demand for acrylic, adhesives, and automotive applications is contributing to market expansion. Public-private partnerships, increased industrial expenditure, and rising investment in resin research and production capacity are further accelerating growth. The convenience of resin delivery, combined with improved durability and reduced risk of failure, positions it as a preferred choice.

Competitive Landscape

The global pure monomer resin market is characterized by competition between established chemical industry leaders and emerging bio-based specialists focused on sustainable and high-performance solutions. In North America and Europe, companies such as Synthomer PLC and Cray Valley maintain leadership positions through robust research and development, extensive distribution networks, and strong industrial partnerships. Their investments in innovative acrylic and styrene resin programs enhance product performance, enabling applications in coatings, adhesives, electronics, and automotive sectors, while ensuring durability, chemical resistance, and process reliability.

In the Asia Pacific region, Kolon Industries is driving growth by offering localized and cost-competitive resin solutions that improve accessibility for manufacturers across the automotive, construction, and packaging industries. Acrylic resins support high adhesion strength, reduce material failure risks, and enable integration into large-scale industrial processes. Strategic partnerships, collaborations, and acquisitions further expand product portfolios and accelerate the commercialization of advanced resin technologies.

Key Industry Developments:

- In July 2025, Loop Industries launched Twist™, a circular polyester resin made entirely from textile waste. The product, originally developed as fiber-grade PET resin, was rebranded to highlight its role in reducing reliance on virgin materials and traditional bottle-to-textile recycling. Loop engaged apparel brands for offtake agreements tied to a planned joint venture in India, where Twist™ would be supplied as a branded offering.

Companies Covered in Pure Monomer Resin Market

- Synthomer PLC

- Kolon Industries

- Rain Industries (Rain Carbon Germany GmbH)

- Kraton Corporation

- Cray Valley (TotalEnergies)

- VNK AS

- Yasuhara Chemical

- Neville Chemical Company

- Puyang Tiancheng Chemical

Frequently Asked Questions

The global pure monomer resin market is projected to reach US$822.5 million in 2026.

Increasing production of lightweight vehicles, electric cars, and advanced electronic devices is driving demand for high-performance resins with strong adhesion, thermal stability, and chemical resistance.

The pure monomer resin market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Increasing focus on circular economy models and renewable raw materials creates opportunities for manufacturers to develop bio-based, recyclable, and low-carbon monomer resins tailored for eco-conscious automotive, packaging, and construction sectors.

Synthomer PLC, Kolon Industries, Rain Industries, Kraton Corporation, and Cray Valley are the key players.