- Bulk Chemicals

- Monoethylene Glycol (MEG) Market

Monoethylene Glycol (MEG) Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Monoethylene Glycol (MEG) Market by Application (PET, Polyester Fibers, Antifreeze, Others), End-use (Packaging, Textile, Automotive, Plastics, Others), and Regional Analysis for 2025 - 2032

Monoethylene Glycol Market Size and Trends Analysis

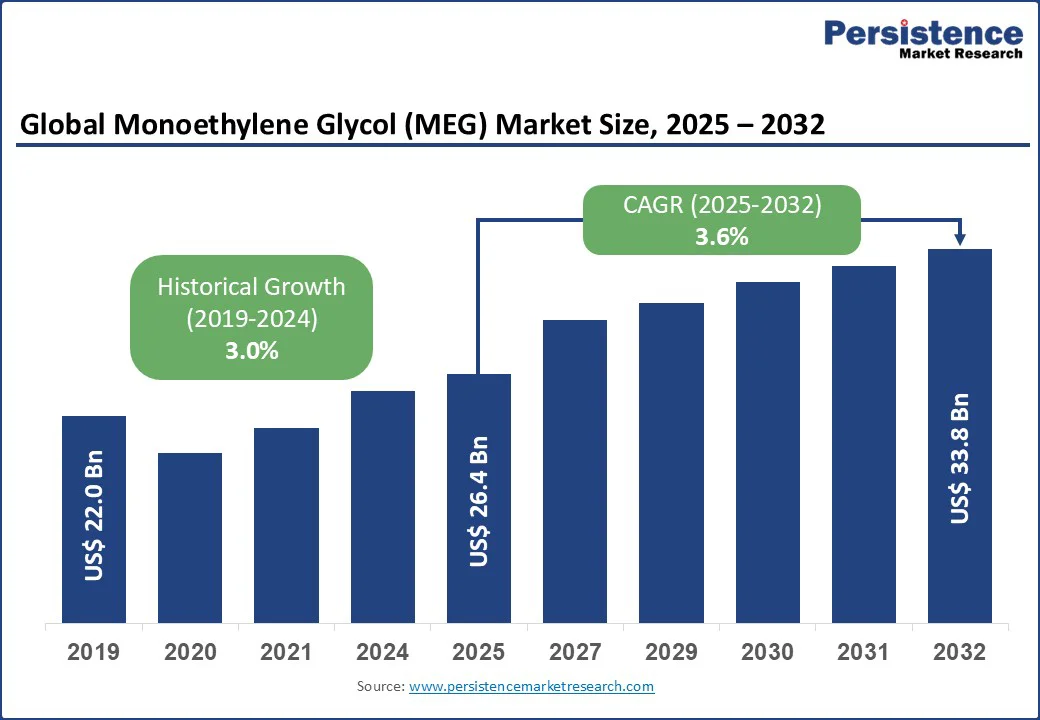

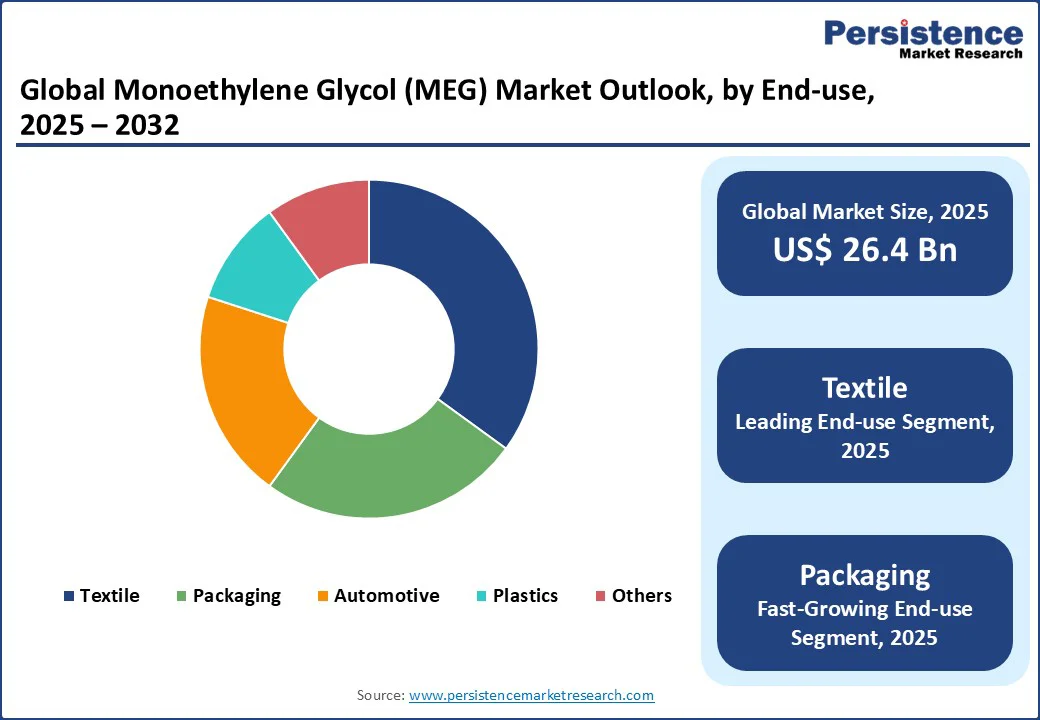

The global monoethylene glycol (MEG) market size is likely to be valued at US$ 26.4 Bn in 2025 and is projected to reach US$ 33.8 Bn by 2032, registering a CAGR of 3.6% during 2025 - 2032.

The monoethylene glycol (MEG) market is driven by its extensive use in producing polyester fibers, polyethylene terephthalate (PET) resins, and antifreeze formulations.

MEG plays a critical role in industries such as textiles, packaging, automotive, and electronics. The demand continues to rise due to the growing consumption of polyester-based apparel and the increasing popularity of PET packaging for beverages and food products. MEG is widely used in coolants and de-icing solutions, supporting automotive and industrial applications.

Key Industry Highlights:

- Leading Application: Polyester Fibers hold a 50% market share in 2025, driven by robust demand in the textile industry.

- Fastest Growing Application: PET segment fueled by sustainable packaging trends and e-commerce growth.

- Dominates End-use: Textile industry holds a 45% market share, driven by Polyester Fiber applications.

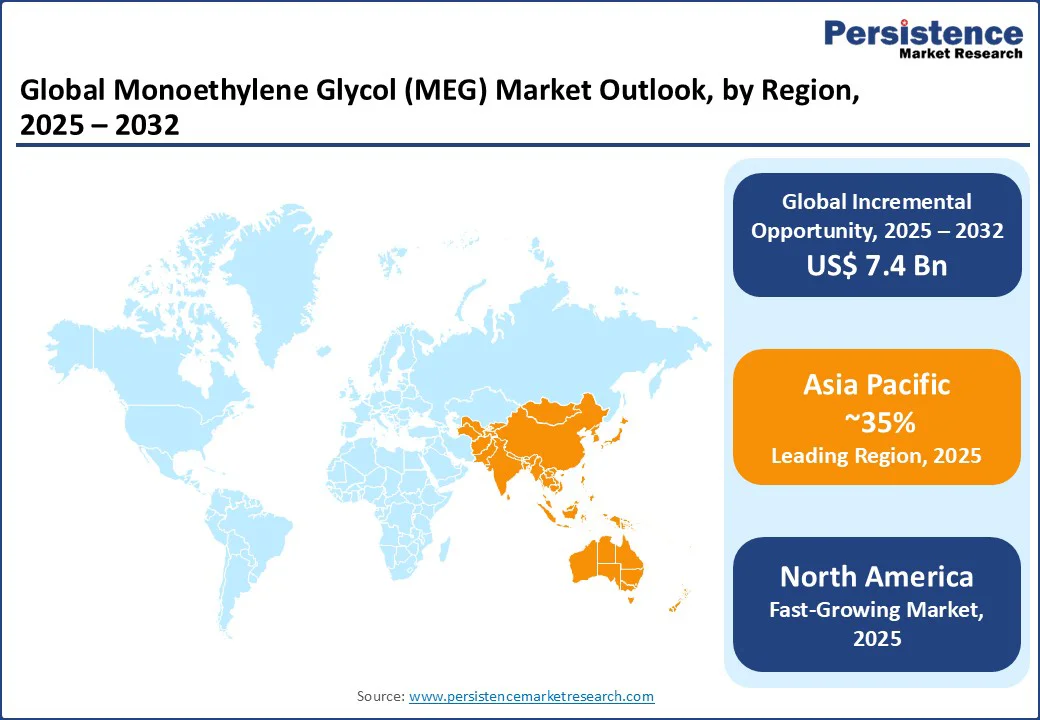

- Leading Region: Asia Pacific accounts for 35% global market share, led by China and India.

- Fastest Growing Region: North America, fueled by rapid industrialization, urbanization, and textile growth.

|

Global Market Attribute |

Key Insights |

|

Monoethylene Glycol Market Size (2025E) |

US$ 26.4 Bn |

|

Market Value Forecast (2032F) |

US$ 33.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2% |

Market Dynamics

Driver - Growing Demand for Polyester Fibers in the Textile Industry

The monoethylene glycol market is significantly driven by the surging demand for polyester fibers in the textile industry, which commands a 50% market share in 2025. Polyester Fibers are highly valued for their durability, affordability, and versatility, making them a preferred choice for apparel, home furnishings, and industrial textiles such as conveyor belts and tire cords. The rise of fast fashion, coupled with increasing consumer spending in emerging economies, has amplified MEG consumption. For instance, global apparel sales are expected to reach US$ 2.5 Tn by 2030, with polyester fibers accounting for over 55% of textile materials used.

Additionally, advancements in eco-friendly polyester fibers, such as those derived from recycled PET, are aligning with global sustainability trends, further boosting MEG demand. Innovations in textile manufacturing processes, including improved dyeing, and finishing techniques, also enhance the appeal of Polyester Fibers, driving market growth.

Restraint - Volatility in Raw Material Prices

The monoethylene glycol market faces significant challenges due to fluctuating prices of ethylene, its primary feedstock, which is closely tied to crude oil and natural gas markets. In 2025, ethylene prices fluctuated by approximately 15% due to supply chain disruptions, geopolitical tensions in oil-producing regions, and unexpected demand shifts. These fluctuations increase MEG production costs, impacting profit margins, particularly for smaller manufacturers who lack the economies of scale to absorb price volatility. For example, a 10% rise in ethylene costs can increase MEG production costs by 8–12%, squeezing margins in price-sensitive markets.

Additionally, reliance on fossil fuel-based feedstocks exposes the market to environmental regulations, such as carbon taxes, which further complicate cost structures. Limited access to alternative feedstocks in certain regions exacerbates these challenges, hindering market stability and growth for smaller players.

Opportunity - Expansion in Sustainable MEG Production

The development of bio-based monoethylene glycol from renewable feedstocks, such as sugarcane, corn, or biomass, presents a transformative opportunity for the market. The demand for bio-MEG is driven by its adoption in eco-friendly packaging and textile applications. For instance, bio-MEG reduces carbon emissions by up to 20% compared to traditional MEG, aligning with global sustainability goals such as the Paris Agreement.

Companies investing in bio-MEG production can cater to environmentally conscious consumers and industries, particularly in Europe and North America, where regulations such as the EU’s Circular Economy Action Plan encourage sustainable materials. The rise of circular economy initiatives, such as recycling PET into bio-MEG, further enhances market potential. Additionally, government incentives for green technologies and increasing consumer preference for sustainable products create a favorable environment for bio-MEG adoption, offering significant growth opportunities.

Category-wise Analysis

Application Insights

Polyester Fibers dominate the monoethylene glycol market with a 50% share in 2025, driven by their widespread use in textiles for apparel, upholstery, and industrial applications such as geotextiles and tire reinforcement. The global textile industry’s growth, particularly in Asia Pacific, supports this segment’s leadership, with China alone accounting for 40% of global Polyester Fiber production. The segment benefits from the affordability and versatility of Polyester Fibers, which are increasingly used in sustainable textiles made from recycled materials.

The PET segment is the fastest-growing. The rising demand for PET in packaging, particularly for beverage bottles, food containers, and flexible films, is driven by its lightweight, recyclable, and cost-effective properties. The shift toward sustainable packaging, including recycled PET, is fueled by consumer demand and regulatory pressures, such as bans on single-use plastics in Europe and North America. Additionally, the growth of e-commerce and ready-to-eat food products further accelerates PET demand, making it a key growth driver.

End-use Insights

The textile industry leads with a 45% market share in 2025, driven by the extensive use of polyester fibers in apparel, home textiles, and industrial applications. The textile sector’s dominance is supported by robust manufacturing bases in emerging markets such as India, where the textile industry is valued at US$ 100 Bn in 2025, and China, which produces over 50% of global polyester fibers. The segment benefits from increasing consumer spending on apparel and the growing use of technical textiles in industries such as construction and automotive.

The packaging industry is the fastest-growing end-use segment. The rise in e-commerce, drives demand for PET-based packaging for shipping and retail. The food and beverage sector, particularly in North America and Europe, relies on PET for its recyclability and durability, with over 70% of beverage bottles made from PET. The push for sustainable packaging, supported by initiatives such as the EU’s Plastic Strategy, further enhances this segment’s growth. Emerging trends, such as biodegradable PET and lightweight packaging, also contribute to the segment’s rapid expansion.

Regional Insights

North America Monoethylene Glycol Market Trends

North America is expected to account for 30% global market share in 2025, with the U.S. contributing 70% of the regional market. The U.S. market is driven by strong demand in the packaging industry, valued high in 2025, particularly for PET-based beverage bottles and food containers. The automotive sector’s need for antifreeze, especially in cold climate regions, accounts for 15% of MEG consumption in the U.S. The rise of e-commerce and ready-to-eat food products further boosts PET demand, with the U.S. e-commerce market growing at a leading CAGR from 2025 to 2032. Sustainability initiatives, such as recycling programs and bio-MEG adoption, are supported by regulations such as the U.S. EPA’s waste reduction goals. Technological advancements in MEG production, including energy-efficient processes, also drive market growth in the region.

Europe Monoethylene Glycol Market Trends

Europe accounts for a 20% global market share in 2025, led by Germany, the UK, and France. Germany dominates the regional market, contributing 35% of Europe’s MEG demand, driven by its robust textile and automotive industries. The German textile sector, is highly valued in 2025, relies on polyester fibers for technical textiles and apparel. The UK’s focus on sustainable packaging, supported by the EU’s Circular Economy Action Plan, drives bio-MEG adoption, with the UK packaging market growing at a CAGR of 3.5% by 2032.

France’s food and beverage packaging sector, valued at US$ 25 Bn, boosts PET demand, particularly for bottled water and soft drinks. Stringent EU regulations, such as the Single-Use Plastics Directive, promote recyclable and bio-based MEG, driving market growth. Innovations in sustainable production and recycling technologies further strengthen Europe’s market position.

Asia Pacific Monoethylene Glycol Market Trends

Asia Pacific leading with a 35% global market share in 2025, led by China, India, and Japan. China accounts for over 50% of the regional market, driven by its massive textile industry, which produces 40% of global polyester fibers. China’s textile exports fuel MEG demand. India’s textile and apparel market, drives polyester fiber consumption, supported by government initiatives such as “Make in India.” Japan’s automotive and electronics industries contribute to MEG demand for antifreeze and PET applications, with the automotive sector growing at a CAGR of 3%. Rapid industrialization, urbanization, and rising consumer spending on textiles and packaged goods make Asia Pacific the fastest-growing region. The region’s focus on expanding production capacities and adopting sustainable practices further enhances market growth.

Competitive Landscape

The global monoethylene glycol (MEG) market is characterized by intense competition among established players and regional manufacturers, all striving to strengthen their market presence through innovation, sustainability, and strategic expansion. Leading companies such as MEGlobal, SABIC, India Glycols Ltd., Shell, and LyondellBasell N.V. have positioned themselves at the forefront by leveraging advanced production technologies and sustainable practices. These companies are actively investing in bio-based MEG (bio-MEG) production to address the growing demand for environmentally friendly solutions, reduce dependency on fossil fuels, and comply with stringent environmental regulations. Digitalization and process optimization are becoming essential competitive tools, enabling improved operational efficiency and reduced production costs. Overall, the market is witnessing a shift toward green chemistry, strategic alliances, and technological advancements, making sustainability a central pillar of competitive differentiation in the MEG industry.

Key Developments:

- In 2024, ?Indian Oil Corporation (IOC) awarded a contract to Versalis SPA for technology licensing at its proposed Paradip petrochemical complex in Odisha. This initiative includes a 400,000-tonnes-per-year cumene unit, integrating with IOC's existing 15-million tonnes/year refinery. The project is estimated at INR 610.77 Bn (USD 7.39 Billion), aims to produce ethylene, polypropylene, polyethylene variants, polyvinyl chloride, monoethylene glycol, phenol, and isopropyl alcohol, enhancing India's petrochemical self-reliance.

- In 2023: SABIC announced the initial startup activities of the Ethylene Glycol Plant - 3 at its manufacturing affiliate, Jubail United Petrochemical Company (United), with an estimated annual production capacity of 700,000 metric tons of mono-ethylene glycol. Saudi Basic Industries Corporation, known as SABIC, is a Saudi chemical manufacturing company. Saudi Aramco owns 70% of SABIC's shares. It is active in petrochemicals, chemicals, industrial polymers, fertilizers, and metals.

Companies Covered in Monoethylene Glycol (MEG) Market

- MEGlobal

- Ishtar Company, LLC

- Raha Group

- India Glycols Ltd.

- Kimia Pars Co.

- LyondellBasell N.V.

- Arham Petrochem Pvt. Ltd.

- Indian Oil Corp. Ltd.

- Pon Pure Chemicals Group

- Acuro Organics Ltd.

- SABIC

- Euro Industrial Chemicals

- Shell

- UPM Biochemicals

- Others

Frequently Asked Questions

The monoethylene glycol market is projected to reach US$ 26.4 Bn in 2025, driven by textile and packaging demand.

Surging demand for polyester fibers in textiles and PET in packaging fuels market growth.

The monoethylene glycol market grows at a CAGR of 3.6% from 2025 to 2032, reaching US$ 33.8 Bn by 2032.

Sustainable bio-MEG production and expansion in emerging markets drive growth opportunities.

Key players include MEGlobal, SABIC, India Glycols Ltd., Shell, and LyondellBasell N.V.