- Plastics, Polymers & Resins

- Vinyl Acetate Monomer Market

Vinyl Acetate Monomer Market Size, Share, and Growth Forecast 2026 - 2033

Vinyl Acetate Monomer Market by Grade (Industrial Grade, Pharmaceutical Grade, and Food Grade), By Application (Polyvinyl Acetate, Polyvinyl Alcohol, Ethylene-Vinyl Acetate, Vinyl Acetate-Ethylene Emulsions, Ethylene-Vinyl Alcohol, and Other), End-Use (Packaging, Construction, Textiles, Automotive, Adhesives and Sealants, Paints and Coatings, Paper and Pulp, Pharmaceuticals, and Others), and Regional Analysis, 2026 - 2033

Vinyl Acetate Monomer Market Size and Trend Analysis

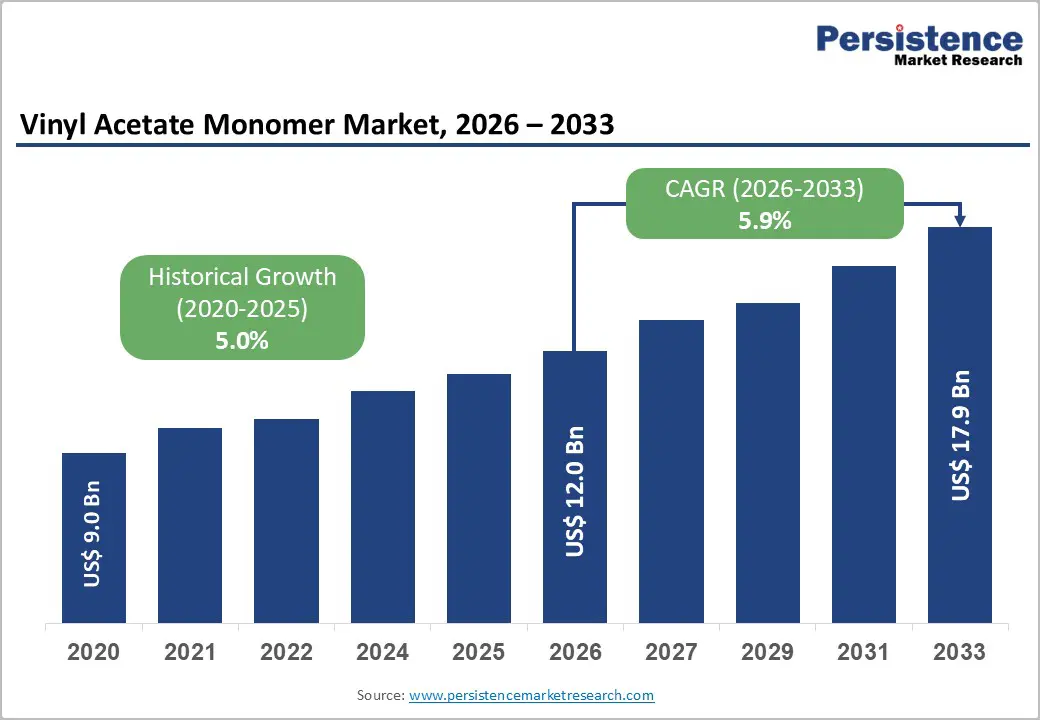

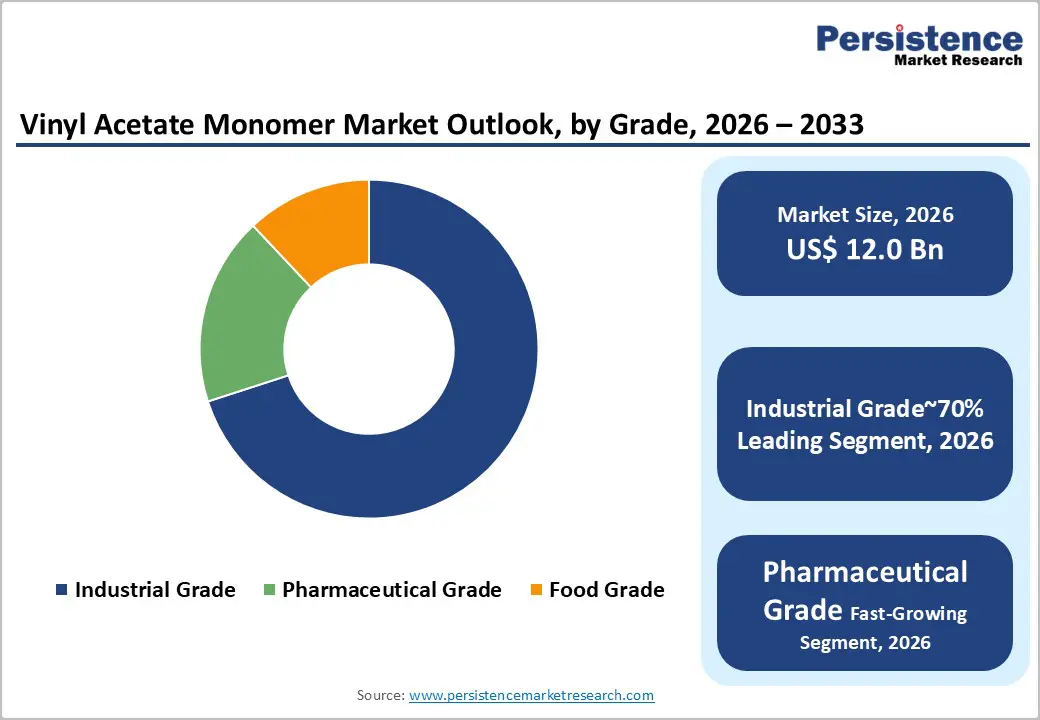

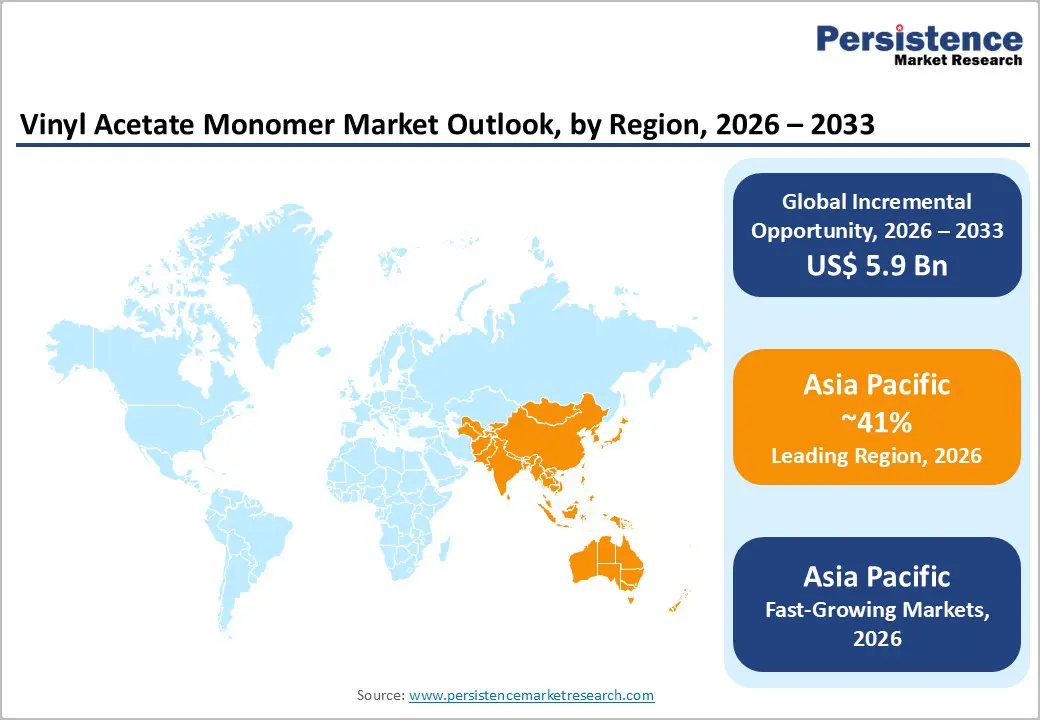

The global Vinyl Acetate Monomer Market size is likely to be valued at US$ 12.0 Billion in 2026 and is expected to reach US$ 17.9 Billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033. This expansion is underpinned by rising demand for polyvinyl acetate (PVAc) and ethylene vinyl acetate (EVA)-based products across construction, packaging, automotive, and textiles, where VAM serves as a key polymerization intermediate for adhesives, coatings, and specialty films.

Key Industry Highlights:

- Leading region: Asia Pacific dominates the Vinyl Acetate Monomer Market with nearly 45% global consumption share, driven by massive construction and packaging demand in China and India.

- Fastest-growing region: Asia Pacific is also the fastest-growing region, supported by integrated petrochemical hubs, infrastructure megaprojects, and solar expansion, accelerating VAM demand at a robust 7% CAGR, significantly outpacing mature markets in Europe and North America.

- Dominant segment: Industrial-grade VAM leads the market with approximately 70% share, driven by its extensive use in EVA, PVAc, and VAE emulsions for construction adhesives, coatings, and packaging applications.

- Fastest-growing segment: EVA-based applications are the fastest-growing segment, driven by surging demand for flexible packaging and solar panel encapsulation, now holding a double-digit consumption share and expanding at an estimated 7.5% CAGR globally.

- Key market opportunity: Bio-based and low-carbon VAM production offers a high-value opportunity, as climate regulations and ESG commitments drive demand for sustainable adhesives, coatings, and packaging materials.

| Key Insights | Details |

|---|---|

|

Vinyl Acetate Monomer Market Size (2026E) |

US$ 12.0 Billion |

|

Market Value Forecast (2033F) |

US$ 17.9 Billion |

|

Projected Growth CAGR (2026–2033) |

5.9% |

|

Historical Market Growth (2020–2025) |

5.0% |

Market Dynamics

Drivers - Construction Boom and Low-VOC Regulations Driving Strong Growth in VAM-Based Adhesives and Coatings Worldwide

Rapid urbanization and large-scale infrastructure development across both developed and emerging economies are strongly driving demand for VAM-based adhesives and coatings, which form the core of the Vinyl Acetate Monomer Market. In China, government investment in affordable housing, transport networks, and urban expansion has significantly increased the use of PVAc emulsions in tile adhesives, flooring systems, and architectural coatings. Construction-related applications now account for more than 40% of regional VAM consumption.

Similar growth is visible in India, where national infrastructure programs and rising residential projects have made adhesives and sealants the largest VAM end-use segment. Additionally, stricter environmental regulations in the U.S. and Europe, promoting low-VOC, water-based products, are encouraging the shift toward VAM-based emulsions. Polyvinyl acetate offers strong bonding, flexibility, and cost efficiency, making it a preferred choice over solvent-based alternatives. This regulatory support is creating stable, long-term demand across the construction and coatings industries.

Rising Packaging Demand and Expanding Solar Industry Accelerating EVA Consumption Across Key Global Markets

The packaging and flexible film sector represents a major growth driver for the vinyl acetate monomer market, largely due to the rising use of ethylene vinyl acetate copolymers. EVA is widely applied in food packaging, laminated films, and solar panel encapsulation because of its clarity, flexibility, and strong sealing properties. In Asia Pacific, rapid e-commerce expansion and increasing consumption of packaged food products are significantly boosting demand for EVA-based films. The EVA applications now account for a double-digit share of total VAM consumption, with growth exceeding the overall market average in several Asian countries. At the same time, the solar energy sector is creating new opportunities, as EVA encapsulants protect photovoltaic cells from moisture and mechanical stress. With aggressive renewable energy targets in China and India, demand for EVA in solar applications is rising steadily, further strengthening long-term VAM consumption.

Restraints - Fluctuating Ethylene and Acetic Acid Prices Creating Cost Pressure and Limiting Profit Stability for VAM Producers

Price volatility of key raw materials remains a major challenge for the Vinyl Acetate Monomer Market, particularly for ethylene and acetic acid, which are closely linked to global oil and gas markets. Ethylene accounts for a large share of VAM production costs and experienced sharp annual price fluctuations exceeding 20% between 2022 and 2024.

Acetic acid prices have also remained volatile due to changes in methanol and natural gas markets. This unpredictability pressures profit margins for producers and complicates long-term planning for capacity investments. Many companies are forced to rely on hedging strategies or flexible production schedules to manage cost risks. In Europe, where ethylene production costs are significantly higher than in North America, producers face added competition from lower-cost imports. These cost pressures limit the ability to pass increases to customers and restrain overall market expansion.

Tight Environmental Compliance and Safety Regulations Increasing Operational Costs and Slowing Capacity Expansions

The Vinyl Acetate Monomer Market is increasingly affected by strict environmental and safety regulations, particularly in North America and Europe. VAM is classified as a flammable chemical with potential health risks, requiring advanced storage systems, emission controls, and worker safety measures. Regulatory agencies such as the U.S. EPA and the European Chemicals Agency have introduced tighter rules on air emissions, wastewater treatment, and workplace exposure levels.

These regulations force producers to invest heavily in pollution-control equipment, monitoring systems, and process upgrades, raising operational and capital costs. In addition, approval timelines for new plants or capacity expansions have become longer, especially in densely populated regions. Growing public focus on sustainability and plastic waste is also encouraging some end-users to explore alternative materials. Although still at early stages, these shifts create long-term substitution risks and increase regulatory uncertainty across the VAM value chain.

Opportunity - Development of Bio-Based VAM Solutions Opening Sustainable Growth Opportunities and Premium Market Segments

The development of bio-based and low-carbon VAM production represents a significant opportunity for the Vinyl Acetate Monomer Market, aligning with global sustainability goals and corporate net-zero commitments. Major producers such as Celanese and LyondellBasell are actively investing in research to use bio-ethylene and bio-acetic acid as alternative feedstocks. Early studies suggest that bio-based VAM can reduce greenhouse gas emissions by 20% compared to conventional fossil-based routes. This makes it attractive for environmentally conscious coatings, adhesives, and packaging products.

Government support through grants, carbon credits, and green chemistry initiatives is helping to offset higher production costs during the early commercialization stages. European research programs are also exploring efficient bio-ethanol-to-ethylene conversion technologies. Companies that successfully scale sustainable VAM solutions can access premium markets, strengthen ESG positioning, and build long-term customer loyalty in environmentally regulated regions.

Asia Pacific Petrochemical Expansion and Regional Integration: Creating New Production Hubs and Demand Centers

Asia-Pacific presents strong growth opportunities for the Vinyl Acetate Monomer Market, driven by large-scale capacity additions and integrated petrochemical complexes. Countries such as China, India, and Southeast Asian nations are expanding ethylene and acetic acid production, creating ideal conditions for downstream VAM manufacturing. In China, national chemical-industry strategies focus on vertical integration, with refinery-petrochemical hubs incorporating VAM, EVA, and PVAc units to maximize value creation.

Several state-owned enterprises have announced multi-billion-dollar investments in advanced materials projects that will directly increase VAM demand. In India, government policies that support domestic chemical manufacturing and infrastructure development are encouraging the establishment of new VAM facilities and joint ventures. International players such as Dow and LyondellBasell are exploring expansion opportunities to serve rapidly growing construction and packaging markets. Locating production near feedstock sources improves cost efficiency, reduces logistics expenses, and strengthens regional supply chains.

Category-wise Analysis

By Grade Insights

Within the grade category, Industrial Grade dominates the vinyl acetate monomer market, accounting for nearly 70% of total consumption worldwide. This strong leadership is mainly driven by its extensive use as a core raw material for producing polyvinyl alcohol (PVA), ethylene-vinyl acetate (EVA), vinyl acetate ethylene (VAE) emulsions, and other industrial copolymers that together form the majority of global VAM demand. Industrial-grade VAM is specially formulated to deliver high polymerization efficiency, consistent quality, and cost advantages, making it ideal for large-scale manufacturing operations.

It is widely used in the production of adhesives, architectural coatings, flexible packaging films, and construction chemicals where performance reliability is essential. The continuous expansion of industrial manufacturing, infrastructure development, and consumer goods production across emerging and developed markets further strengthens the dominance of industrial-grade vinyl acetate monomer in the global market.

By Application Insights

Among all applications, Polyvinyl Acetate (PVA) remains the largest consumer of vinyl acetate monomer, capturing approximately 30% of the total application-based market share. PVA emulsions and dispersions are extensively used across industries due to their strong bonding strength, flexibility, fast drying properties, and water resistance. These materials are commonly used in wood adhesives for furniture manufacturing, paper and paperboard coatings for packaging, textile sizing processes, and construction-grade binders for building materials.

The rising demand for ready-to-assemble furniture, the expanding packaging sector, and the steady growth in residential and commercial construction in emerging economies are significantly boosting PVA consumption. In addition, manufacturers prefer PVA-based systems because of their cost efficiency and environmental compatibility, which aligns with increasing regulatory focus on low-VOC and sustainable material solutions.

By End-user Insights

The construction sector is the leading end-use industry for vinyl acetate monomer, accounting for approximately 35% of total global demand. This strong presence is driven by the extensive use of VAE emulsions and PVA-based binders in essential building applications, including tile adhesives, flexible flooring systems, exterior insulation finishing systems, waterproof coatings, and repair mortars. These materials provide superior bonding strength, flexibility, durability, and resistance to environmental stress, making them ideal for modern construction needs.

Rapid urbanization, population growth, and large-scale infrastructure development projects across Asia-Pacific, Europe, and Latin America continue to drive strong demand for construction chemicals and adhesive systems. Furthermore, increasing investments in residential housing, commercial complexes, and renovation activities are reinforcing the construction industry’s role as the primary driver of global vinyl acetate monomer consumption.

Regional Insights

North America Vinyl Acetate Monomer Market Trends

North America represents a mature yet stable vinyl acetate monomer market, supported by strong demand from construction, packaging, automotive, and furniture industries. The United States leads regional consumption, driven by widespread use of PVAc adhesives in wood processing and water-based architectural coatings in residential construction. Environmental regulations enforced by the U.S. EPA have accelerated the shift toward low-VOC formulations, further supporting VAM-based emulsions. The region benefits from cost-competitive ethylene feedstocks derived from shale gas, providing producers with a significant cost advantage compared to Europe.

Major companies such as Dow, Celanese, and LyondellBasell operate integrated production chains linking acetic acid, VAM, and downstream polymers, improving operational efficiency. Ongoing investments in energy efficiency, plant modernization, and emission-reduction technologies are helping North American manufacturers maintain competitiveness while meeting regulatory requirements, ensuring stable long-term market performance.

Europe Vinyl Acetate Monomer Market Trends

The European Vinyl Acetate Monomer Market is strongly shaped by environmental regulations, specialty chemical applications, and advanced manufacturing standards. Countries such as Germany, France, and the United Kingdom are key consumers, driven by demand for high-quality adhesives, coatings, and polymer dispersions. Water-based architectural coatings and industrial adhesives containing VAM are widely adopted due to strict VOC restrictions under EU environmental policies.

Germany remains a major production and innovation hub, with companies such as Wacker Chemie and Arkema supplying specialty PVAc, EVA, and PVOH products across Europe. However, European producers face high feedstock costs, particularly for ethylene, which are significantly higher than in the U.S. This has encouraged capacity optimization and a shift toward higher-value specialty products. Increasing focus on sustainable materials, recyclable packaging, and bio-based polymers is helping the region maintain market growth despite structural cost challenges.

Asia Pacific Vinyl Acetate Monomer Market Trends

Asia-Pacific is the largest and fastest-growing region in the vinyl acetate monomer market, led by China, India, Japan, and the ASEAN countries. China alone accounts for nearly 40–50% of global VAM consumption, driven by massive construction activity, packaging expansion, and strong manufacturing output of PVAc, EVA, and PVOH. Government infrastructure programs and rising household incomes continue to boost demand for adhesives, paints, and flexible films. India is emerging as a major growth hub, supported by housing development, textile production, and the packaging industry, as well as government initiatives that promote domestic chemical manufacturing. Japan and South Korea maintain stable demand in specialty coatings and advanced films, while Southeast Asia is experiencing rapid industrialization and urban expansion. The region’s strong feedstock availability, large consumer base, and ongoing capacity expansions make Asia Pacific the central growth engine of the global VAM market.

Competitive Landscape

The global vinyl acetate monomer market is moderately consolidated, with several large global chemical companies controlling a significant share of production capacity. Major players including Dow, Celanese Corporation, LyondellBasell, Wacker Chemie, Arkema, and Kuraray operate integrated manufacturing systems that provide strong cost advantages and supply reliability. These companies benefit from access to key feedstocks, advanced processing technologies, and diversified downstream product portfolios. Alongside these global leaders, regional producers in Asia and the Middle East serve local markets with competitive pricing and flexible supply models. Leading companies are actively investing in capacity expansions, technology improvements, and sustainability initiatives to strengthen market positioning. Strategic partnerships, long-term supply contracts, and joint ventures are increasingly common to secure raw materials and customer demand. Many firms are also developing bio-based VAM solutions and low-VOC product lines to align with environmental regulations and evolving customer preferences.

Key Developments:

- In February 2025: Celanese expanded its acetyl chain sustainable product portfolio to include low-carbon VAM derivatives aimed at eco-friendly adhesives and coatings, reflecting strengthened ESG alignment and regulatory compliance efforts in North America and Europe.

- In January 2025: Sinopec mechanically completed the second-phase expansion of its Zhenhai Refinery in China, scaling up advanced polymer units that will boost EVA and PVAc production capacity, thereby increasing VAM demand from packaging and construction industries.

- In October 2024: LyondellBasell introduced an enhanced EVA grade tailored for solar-module encapsulants, supporting rapid growth in the photovoltaic industry across Asia and Europe and reinforcing the role of VAM-based materials in renewable-energy applications.

Companies Covered in Vinyl Acetate Monomer Market

- Solventis

- Sipchem Company

- LyondellBasell Industries Holdings B.V.

- Wacker Chemie AG

- Arkema

- Celanese Corporation

- Dow

- Pcitc information technology Co., LTD.

- Exxon Mobil Corporation

- Innospec

- KURARAY CO., LTD.

- DuPont de Nemours, Inc.

- Borealis AG

- Sumitomo Chemical Co., Ltd.

- Versalis S.p.A.

Frequently Asked Questions

The Vinyl Acetate Monomer Market was valued at US$ 9.0 Billion in 2020, expanded to US$ 12.0 Billion in 2026, and is projected to reach US$ 17.9 Billion by 2033, reflecting steady growth driven by construction, packaging, and coatings demand.

Rapid construction growth, low-VOC regulations boosting water-based adhesives/coatings, rising packaging demand, and expanding solar EVA applications are the primary demand drivers.

Industrial-grade VAM dominates the market, accounting for nearly 70% of total global consumption.

Asia Pacific leads the Vinyl Acetate Monomer Market, with China and India together consuming over half of global VAM volumes, supported by rapid urbanization, infrastructure development, and a large manufacturing base.

A major opportunity lies in bio‑based and low‑carbon VAM production, which can meet growing environmental regulations and ESG commitments while supplying sustainable adhesives, coatings, and packaging materials.