- Healthcare Services

- Interventional Pulmonology Market

Interventional Pulmonology Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Interventional Pulmonology Market by Product (Bronchoscopes, Respiratory Endotherapy Devices, ENB Systems, Pleuroscopes, Airway Stents, Bronchial Thermoplasty Systems, Pleural Catheters, Endobronchial Valves), by Indication, by End User, and Regional Analysis from 2026 to 2033

Interventional Pulmonology Market Share and Trends Analysis

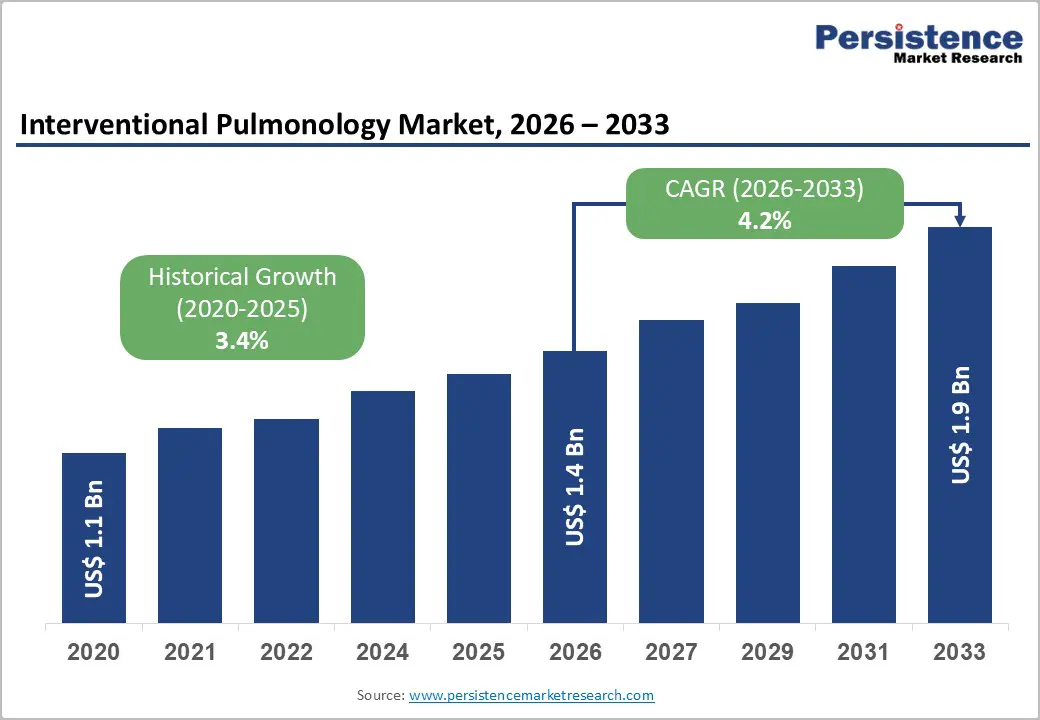

The global interventional pulmonology market is likely to be valued at US$ 1.4 billion in 2026 to US$ 1.9 billion by 2033. The market is projected to record a CAGR of 4.2% during the forecast period from 2026 to 2033.

Chronic obstructive pulmonary disease (COPD) is a general term used to describe the chronic, progressive condition of lung disorders such chronic bronchitis and asthma. According to WHO, 3.5 million individuals died from chronic obstructive pulmonary disease (COPD), which is the fourth most common cause of death globally, in 2021. Nearly 90% of COPD-related deaths in people under the age of 70 actually occur in low- and middle-income nations. Increased COPD instances will ultimately lead to an increasing demand for interventional pulmonary operations, which will lead to market growth.

The majority of COPD cases, according to statistics from the American Lung Association, are brought on by smoking cigarettes. COPD rates are 7 times greater among current smokers and 5 times higher among past smokers when compared to new smokers. Numerous lung problems will be caused by the consumption of tobacco and nicotine-based smoking products in the general population. As a result, there will be a greater need for interventional pulmonary procedures as patients seek diagnosis and treatment options for lung illnesses, ultimately resulting in market expansion.

Key Industry Highlights

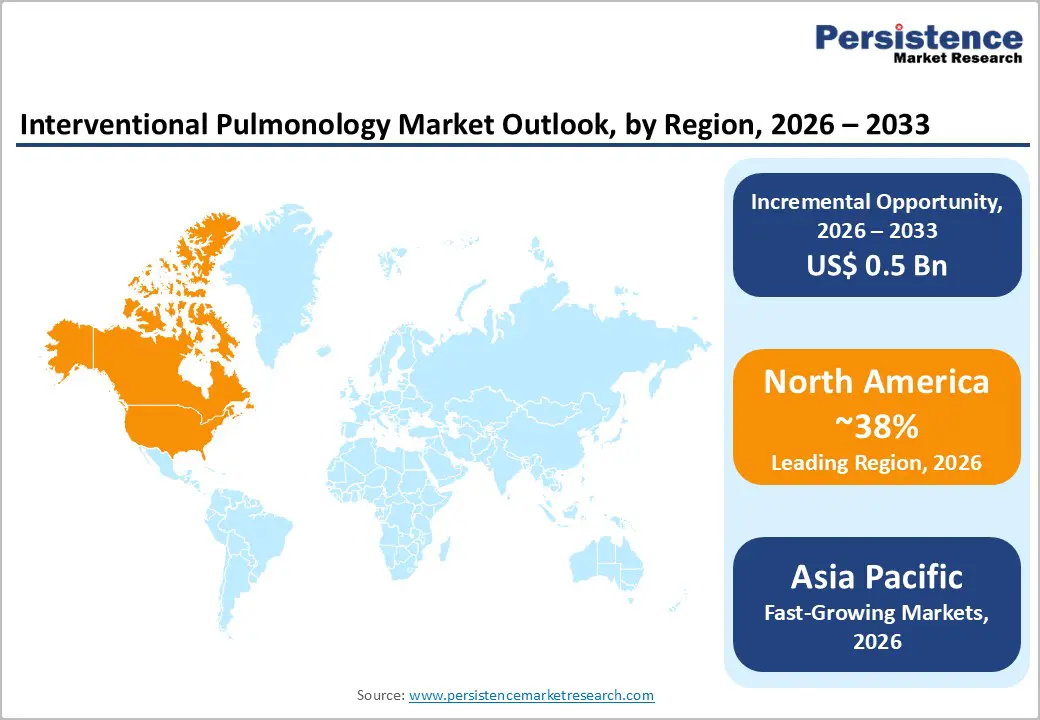

- Leading Region: North America leads interventional pulmonology, supported by advanced respiratory care infrastructure, high disease prevalence, and strong reimbursement ecosystems.

- Fastest Growing Region: Asia Pacific is the fastest-growing, driven by rising COPD and asthma burden, urban pollution, expanding hospitals, and cost-efficient manufacturing.

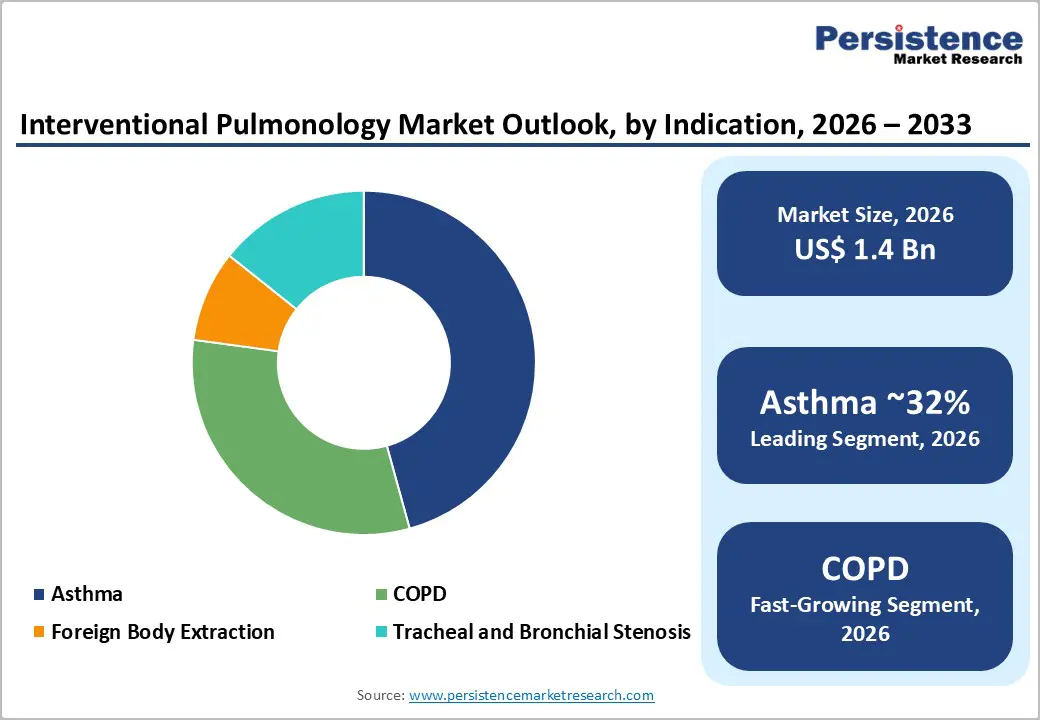

- Dominant Segment: Asthma is the dominant indication, reflecting extensive global patient pools and growing adoption of bronchial thermoplasty and advanced bronchoscopy.

- Fastest Growing Segment: COPD is the fastest-growing indication, propelled by ageing populations, smoking exposure, and interventional options such as valves and denervation.

| Key Insights | Details |

|---|---|

| Interventional Pulmonology Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 1.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.4% |

Market Dynamics Driver

“Increasing Healthcare Spending and Improving Healthcare Infrastructure”

The adoption and use of advanced medical devices in healthcare facilities like hospitals would be supported by improved healthcare infrastructure and increased healthcare expenditures by the relevant public bodies. The need for interventional pulmonology would rise as a result. India, Brazil, and Mexico are examples of emerging economies with high COPD patient populations. Patients with COPD frequently need respiratory assistance. Due to the significant demand for the treatment of respiratory disorders in these countries, interventional pulmonology devices manufacturers have a great opportunity. Growth in patient disposable income and economic development in these emerging economies will help to secure the market's long-term viability.

“Rising Demand for Improved Bronchoscopy Technique”

The growth of the global market is also a result of bronchoscopy's technological developments. The development of bronchoscopy techniques has been accelerated by developments in electronics and microtechnology. The earlier and safer diagnosis of lung disorders made possible by bronchoscopy's technological advancements has led to better patient outcomes. As a result, the demand for improved bronchoscopy techniques will cause the global interventional pulmonary market to grow throughout the course of the forecast period.

Restraints - Lack of Awareness Regarding Symptoms of Asthma & COPD

The vast majority of individuals with respiratory illnesses suffer undetected and untreated as a result of the lack of awareness about the symptoms of asthma and COPD. This is a significant factor impeding the market for interventional pulmonary. Majority of the COPD-related deaths occur in low-income countries, and many people with COPD symptoms are unaware of such conditions due lack of awareness.

Availability of Non-Invasive Options and Strict Rules

The development of non-invasive diagnostic techniques like liquid biopsies and magnetic resonance spectroscopy, among others, is inhibiting market expansion. The market is being hampered by laws that are becoming more stringent, such as post marketing approval. An average of three to seven years is needed to bring a product to market. Pre-market approval (PMA), the most stringent procedure required for device approval by the FDA, is necessary for Class III devices. Due to the much higher risks to patients, such devices require clinical evidence to warrant the application. Thus, the market is being hampered by the increasingly strict rules.

Associated Side Effects of Bronchoscopy Procedures

The risks associated with bronchoscopy procedures such as contamination and post-bronchoscopy infection are reducing adoption rates. Additionally, limiting the market are the bronchoscopy complications, which include bleeding, breathing difficulties, and low blood oxygen levels during the examination. The advent of methicillin-resistant Staphylococcus aureus and other resistant bacteria has led to an increase in the likelihood that a patient would develop a post-bronchoscopy infection.

Opportunity - Advancement in Technology

Technological advancement remains a major opportunity shaping the growth of the interventional pulmonology market. Manufacturers are increasingly adopting advanced, non-reactive materials such as silicone-based coatings to improve device safety and durability. The integration of antimicrobial surface coatings on bronchoscopes helps reduce microbial film formation, lowering infection risks and improving patient outcomes. In parallel, ongoing innovations in optics and imaging have enabled the use of higher-resolution cameras, allowing clinicians to achieve clearer visualization of airway structures and enhancing diagnostic and therapeutic precision.

Device engineering has also focused on improving ergonomics and usability. Flexible insertion tubes with enhanced rotational capability have been developed to reduce operator fatigue during prolonged procedures, improving procedural efficiency. Additionally, miniaturization of endoscopic equipment has enabled the introduction of ultra-slim bronchoscopes, which facilitate access to smaller and more distal bronchi that were previously difficult to reach. These design improvements support safer navigation, better maneuverability, and expanded procedural applications. Collectively, such technological advancements improve clinical outcomes, increase physician adoption, and strengthen the overall value proposition of interventional pulmonology devices, thereby creating sustained market growth opportunities.

Category-wise Analysis

By Product Type Insights

Bronchoscopes constitute the leading product category in the interventional pulmonology market, accounting for an estimated 34% share in 2025, driven by their indispensable role across diagnostic and therapeutic applications. These devices are routinely used for airway visualization, bronchoalveolar lavage, tissue biopsy, and foreign body removal, making them central to routine pulmonary care. Flexible video bronchoscopes and fiberoptic models are widely preferred due to their maneuverability and suitability for outpatient procedures, while rigid bronchoscopes continue to be used in complex interventions such as airway stenting, tumor debulking, and management of massive hemoptysis in tertiary hospitals. Utilization data from developed healthcare systems indicate bronchoscopy rates exceeding 140 procedures per 100,000 population, highlighting the extensive procedural reliance on these instruments. Ongoing product enhancements, including high-definition imaging, endobronchial ultrasound compatibility, and the growing adoption of single-use bronchoscopes, continue to strengthen the dominance of bronchoscopes over other interventional pulmonology products such as airway stents, pleural drainage systems, and bronchial thermoplasty devices.

By Indication Insights

Asthma represents a significant indication within the interventional pulmonology market, accounting for approximately 32% of market share in 2025, largely due to its high global prevalence and unmet clinical needs in severe disease. A substantial proportion of asthma patients remain poorly controlled despite optimized medical therapy, leading to increased consideration of bronchoscopic interventions in specialized care settings. Procedures such as bronchial thermoplasty have gained acceptance for patients with severe, refractory asthma, contributing to sustained procedural volumes. Additionally, bronchoscopy is frequently used during asthma exacerbations to evaluate airway inflammation, identify infections, and assess structural abnormalities, further supporting market demand. Global clinical guidelines highlight the growing burden of asthma across both adult and pediatric populations, reinforcing the need for advanced diagnostic and interventional approaches. Expanding reimbursement coverage for bronchial thermoplasty and accumulating clinical evidence demonstrating improvements in symptom control, quality of life, and reduced exacerbation frequency are expected to support continued growth of asthma-related interventional pulmonology procedures.

Regional Insights

North America Interventional Pulmonology Market Trends

North America interventional pulmonology market is strongly influenced by the rising prevalence of asthma, particularly in the U.S., which accounted for approximately 90.7% of the regional market share in 2025. Asthma remains one of the most widespread chronic respiratory conditions in the country, affecting nearly 25 million individuals, or roughly one in every thirteen people. More than 20 million adults aged 18 years and above live with asthma, with a higher prevalence observed among adult females compared to males.

The condition affects about 9.8% of adult females and 6.1% of adult males, highlighting a significant gender-based disease burden. Asthma is also the most common chronic illness among children, with nearly 5.1 million affected under the age of eighteen. This substantial and growing patient pool increases the need for advanced diagnostic and therapeutic interventions, including bronchoscopic procedures. As disease awareness and treatment accessibility improves, demand for interventional pulmonology solutions across North America is expected to continue rising.

Asia and Pacific Interventional Pulmonology Market Trends

The Asia Pacific interventional pulmonology market is witnessing steady growth, largely driven by the rapidly expanding geriatric population across the region. China plays a dominant role, accounting for approximately 52.8% of the East Asia interventional pulmonology market in 2025, reflecting its large patient base and evolving healthcare infrastructure. According to World Health Organization estimates, China has one of the fastest-growing ageing populations globally. Rising life expectancy combined with declining birth rates is expected to result in nearly 28% of the country’s population being aged over 60 by 2040.

This demographic shift is expected to significantly increase the prevalence of age-related respiratory disorders such as chronic obstructive pulmonary disease, lung infections, and airway obstructions. Elderly patients often require minimally invasive diagnostic and therapeutic pulmonary procedures due to higher surgical risks, supporting greater adoption of interventional pulmonology techniques. As healthcare access and awareness improve across the Asia Pacific, the expanding geriatric population is expected to create sustained demand and long-term growth opportunities for the interventional pulmonology market.

Competitive Landscape

The interventional pulmonology market is moderately fragmented, featuring a mix of global medtech leaders and specialized device manufacturers that compete across bronchoscopes, airway stents, pleural products, and navigation systems. Large players such as diversified endoscopy and imaging companies leverage broad portfolios, strong brands, and global distribution networks, while mid-sized firms differentiate through niche innovations in valves, catheters, and single?use scopes. Competitive strategies increasingly focus on integrated platforms that combine imaging, navigation, and therapeutic tools, alongside recurring revenue from disposables and service contracts. Strategic collaborations, acquisitions, and joint development agreements are common as companies seek to enhance R&D capabilities, expand geographic reach, and accelerate regulatory approvals for next-generation devices.

Key Industry Developments:

- In November 2025, Yashoda Hospital, Hitech City, partnered with Qure.ai and AstraZeneca to launch a cutting-edge AI-powered Lung Nodule Clinic, designed to enhance early detection and timely treatment of lung cancer and other significant pulmonary diseases.

- In September 2023, Interventional pulmonologists at AtlantiCare's Lung Nodule Clinic observed notable clinical benefits from an AI-assisted detection system, which accelerated the pathway from lung cancer diagnosis to treatment.

Companies Covered in Interventional Pulmonology Market

- Olympus Corporation

- Medtronic PLC

- Boston Scientific Corporation

- Becton, Dickinson and Company

- Cook Medical Inc.

- Karl Storz GmbH & Co. KG

- Richard Wolf GmbH

- Pentax Medical Company (Hoya Corporation)

- FUJIFILM Holdings Corporation

- Smiths Group PLC

- Vygon SA

- Clarus Medical LLC

- Huger Medical Instrument Co. Ltd

- Others

Frequently Asked Questions

The global interventional pulmonology market is projected to be valued at US$ 1.4 Bn in 2026.

Rising respiratory disease burden, preference for minimally invasive procedures, technological bronchoscopy advancements, aging populations, and expanding specialist pulmonology infrastructure.

The global interventional pulmonology market is poised to witness a CAGR of 4.2% between 2026 and 2033.

Growth in emerging markets, expanding therapeutic bronchoscopy indications, AI-guided navigation systems, outpatient adoption, and increased physician training programs.

North America is the leading region in the global interventional pulmonology market.