- Specialty & Fine Chemicals

- Monoethanolamine (MEA) Market

Monoethanolamine (MEA) Market Size, Share, and Growth Forecast, 2026-2033

Monoethanolamine (MEA) Market by Grade (Pharmaceutical, Industrial, Others), Application (Surfactants & Emulsifiers, Gas Treatment & Environmental Control, Agrochemical Intermediates, Pharmaceutical Formulation, Others), End-User Industry (Consumer Goods, Oil & Gas, Agriculture, Healthcare, Construction Materials, Textiles Processing), and Regional Analysis for 2026-2033

Monoethanolamine (MEA) Market Share and Trends Analysis

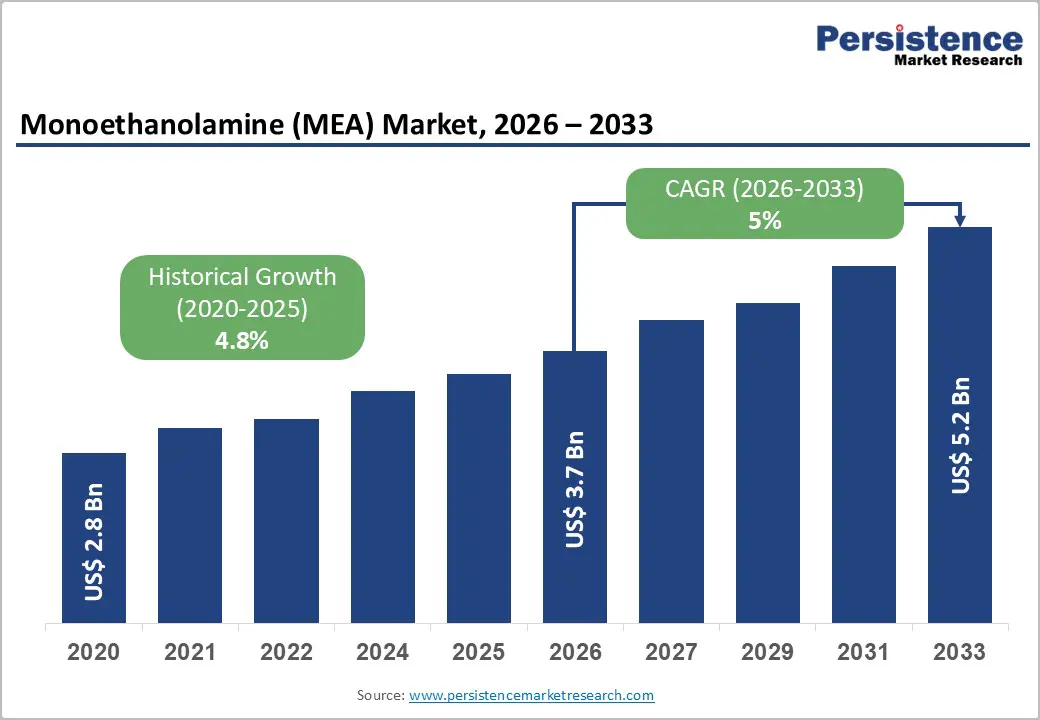

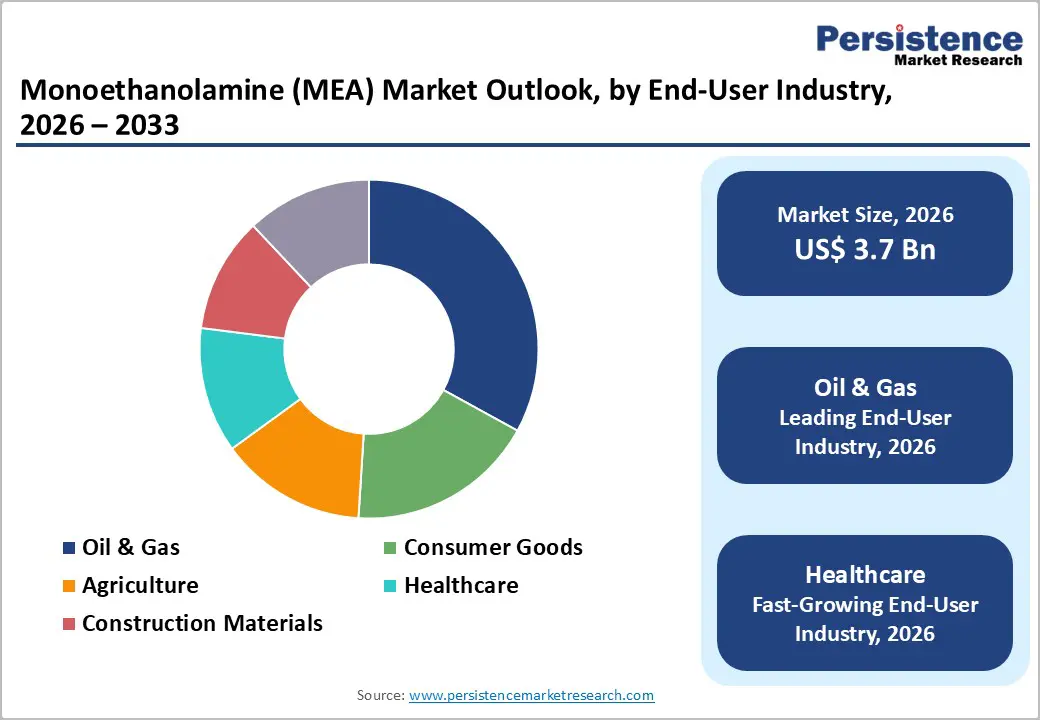

The global monoethanolamine (MEA) market size is likely to be valued at US$ 3.7 billion in 2026, and is projected to reach US$ 5.2 billion by 2033, growing at a CAGR of 5% during the forecast period 2026-2033.

Market growth is being supported by broad industrial utilization across gas treatment, surfactant and emulsifier production, agrochemical intermediates, and pharmaceutical synthesis. In natural gas processing and refinery operations, monoethanolamine (MEA) is serving as a critical absorbent for acid gas removal, particularly carbon dioxide and hydrogen sulfide. In consumer product manufacturing, it is functioning as a key intermediate in detergents, personal care formulations, and cleaning agents.

These diversified applications are reinforcing stable demand across multiple end-use sectors. Expanding adoption in oil and gas, household goods, and water treatment is strengthening long-term commercial viability. Industrial operators are increasingly relying on monoethanolamine-based systems to meet emission control and wastewater treatment requirements. Sustained economic growth in emerging markets is encouraging capacity expansion in downstream chemical manufacturing. Asia Pacific is witnessing rising chemical production infrastructure investment, which is increasing regional consumption volumes. Environmental regulations are further influencing formulation standards and gas purification processes, thereby supporting continued utilization of amine-based solutions

Key Industry Highlights

- Dominant Grade: Industrial grade is projected to command around 70% revenue share in 2026, while pharmaceutical grade is likely to grow the fastest at an estimated CAGR of 6.2% through 2033, driven by rising demand in high-purity pharmaceutical applications.

- Leading Application: Surfactants & emulsifiers are expected to lead with an estimated 38% share in 2026, while pharmaceutical formulation is anticipated to be the fastest-growing 2026-2033 segment at roughly 6.5% CAGR, reflecting expanding drug manufacturing requirements.

- Dominant End-User Industry: Oil & gas is poised to dominate with approximately 33% share in 2026, while pharmaceuticals & healthcare are likely to register the fastest growth at a CAGR of 6.4% through 2033, supported by rising healthcare expenditure.

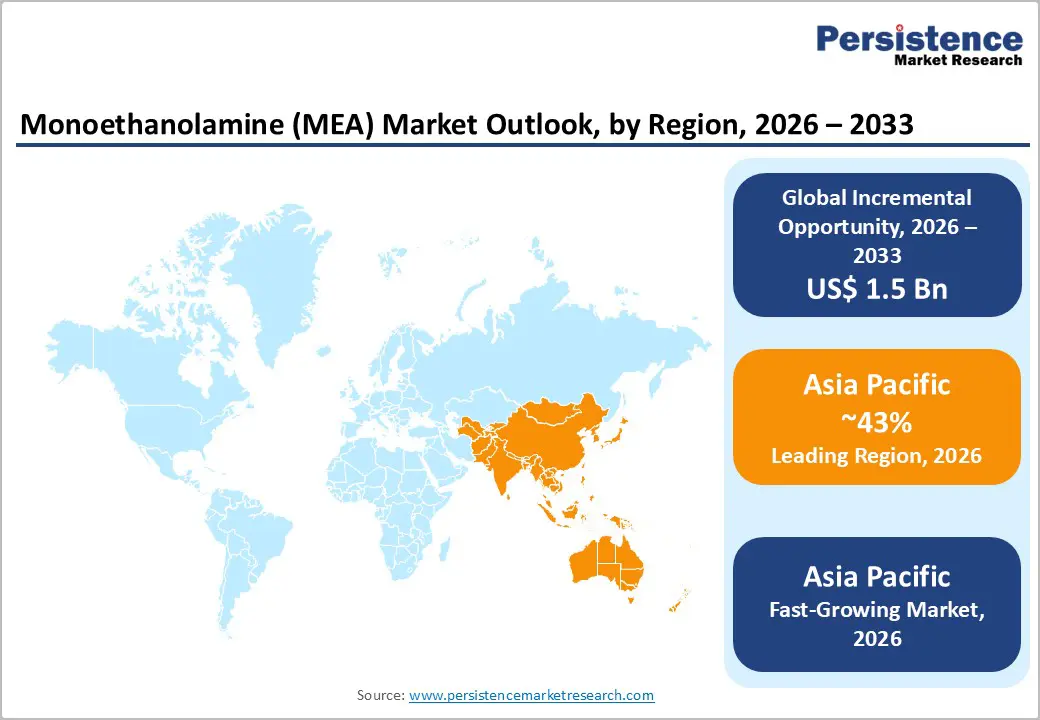

- Regional Leadership: Asia Pacific is expected to lead with an estimated 43% share in 2026 and achieve an approximate 5.8% CAGR through 2033, fueled by growing chemical manufacturing capacity in China, India, and ASEAN countries.

- Competitive Environment: Key strategies include capacity expansions, product quality enhancement initiatives, and innovation in specialty grades, targeting growth across emerging markets and sustainable applications.

| Key Insights | Details |

|---|---|

| Monoethanolamine (MEA) Market Size (2026E) | US$ 3.7 Bn |

| Market Value Forecast (2033F) | US$ 5.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Demand in Gas Treatment and Environmental Applications

The gas treatment and environmental control segment remains one of the most significant drivers for monoethanolamine as it is fundamental for removing CO and HS from natural gas streams, which improves product quality and ensures regulatory compliance in refinery and processing operations. This capability makes MEA indispensable across upstream, midstream, and downstream natural gas infrastructure, particularly as global energy systems transition to cleaner fuels. Stricter emission standards from environmental protection agencies have intensified the need for advanced gas sweetening technologies that rely on MEA’s chemical properties. Industrial expansion of natural gas facilities further reinforces long term MEA consumption.

In November 2025, Germany’s revised Carbon Dioxide Storage and Transport Act (CCS Act) was finalized, establishing legal certainty for industrial?scale carbon capture, utilization, and storage (CCUS) infrastructure. Such major policy steps are having a significant bearing supporting gas treatment technologies that use amine solvents such as MEA. This aligns with broader European Union (EU) decarbonization frameworks that emphasize industrial emissions reduction. As per industry reports, the captured carbon volumes might exceeded 50 million tonnes per year, highlighting accelerating deployment of capture solutions that depend on amine based absorption chemistry, signaling robust demand growth for MEA in environmental and gas treatment applications.

Expanding Applications in Surfactants, Consumer Goods, Pharmaceuticals, and Agrochemicals

Monoethanolamine’s surfactant, emulsifier, and intermediate chemical properties position it as a key input in a diverse array of industrial and consumer products. In consumer goods, MEA contributes to the formulation stability and performance of detergents, shampoos, and household cleaners, sectors that have seen sustained demand growth due to rising urbanization, increasing disposable incomes, and heightened hygiene awareness. Regulatory emphasis on chemical safety and product quality in major markets has reinforced preference for reliable compounds such as MEA in everyday formulations.

Beyond cleaning products, MEA’s use in high?purity pharmaceutical synthesis and agrochemical intermediate production supports broader economic trends. The pharmaceutical sector continues to expand, supported by aging populations and increased healthcare expenditure, while mechanized agriculture and food security initiatives drive agrochemical formulation demand. Industry movement further underlines these trends. For instance, Dow Chemical announced price increases on ethanolamines including MEA, citing persistent demand and feedstock cost pressures. This defines the ongoing industrial and consumer market strength, signaling broad?based MEA adoption across functional applications.

Regulatory & Environmental Compliance Costs

Stringent environmental regulations and compliance requirements continue to pose significant operational challenges for monoethanolamine producers. Chemical manufacturers must invest heavily in emission controls, wastewater treatment, and safety protocols to meet global standards. Regulatory frameworks require detailed risk assessments, reporting, and strict limits on hazardous substance handling, which complicates production and increases operational expenditures. These compliance obligations reduce flexibility for capital investments and capacity expansion, particularly for high-purity or specialty MEA grades.

Recent policy developments underscore this challenge. The European Union’s stringent green regulatory requirements were reported to impose more than $20?billion in annual compliance costs on chemical companies, highlighting the substantial economic impact on producers operating in or exporting to Europe. The EU Council’s “Stop-the-Clock” mechanism in September 2025 further postponed the enforcement of new chemical classification and labelling regulations until 2028, reflecting recognition of the significant regulatory burden. These measures collectively illustrate the tension between environmental protection objectives and cost pressures on MEA manufacturers, which can limit operational agility.

Feedstock Price Volatility and Supply Chain Challenges

Volatility in raw materials, particularly ethylene oxide, ethane, and ammonia, remains a major restraint on MEA production. Fluctuating feedstock prices directly affect production costs and profit margins, especially for bulk industrial grades where cost pass-through is limited. Supply disruptions, logistical challenges, and geopolitical factors can exacerbate price swings, creating downstream cost sensitivity for industrial process additives and chemical intermediates. Manufacturers must manage procurement carefully and maintain inventory buffers, adding complexity to operational planning.

The global feedstock markets faced notable volatility. Supply and pricing of ethylene derivatives, including ethylene oxide, were impacted by shifting trade flows and rising demand in Asia. For instance, China significantly increased U.S. ethane imports to optimize production costs, influencing global raw material availability and price structures. Such fluctuations create financial and operational uncertainty, constraining production planning and investment for MEA producers, while emphasizing the importance of agile supply chain strategies and risk mitigation practices.

Growth in Bio based and Low Impurity MEA Grades

Emerging demand for bio based chemicals and low impurity MEA presents a significant opportunity for innovation and premium positioning within the monoethanolamine market. Sustainable formulations aligned with green chemistry principles allow producers to differentiate products, reduce environmental impact, and meet rising safety standards in pharmaceuticals and personal care. Low impurity MEA enhances performance in sensitive applications such as cosmetics, hygiene products, and high-value industrial additives, while regulatory preference for cleaner inputs reinforces adoption across multiple sectors. These trends are amplified by increasing consumer and industrial emphasis on sustainability, circular production, and reduced carbon footprints, making bio-based MEA strategically valuable.

This opportunity is reinforced by strategic policy initiatives for instance, the European Chemicals Industry Action Plan encouraged industrial uptake of bio based chemical production, innovation, and investment in circular and renewable value chains, creating a favorable regulatory environment for sustainable MEA products. In December 2025, the Circular Bio based Europe Joint Undertaking (CBE JU) announced a €170.7?million work program for 2026 to accelerate bio based chemicals, targeting biorefineries, feedstock diversification, and large-scale adoption across pharmaceuticals, hygiene, and industrial sectors. Measures such as these signal strong policy-backed momentum for bio-derived and low-impurity MEA grades and provide early-mover advantages for producers investing in green technologies.

Penetration in Emerging Markets and Environmental Solutions

Rapid industrialization and expanding chemical manufacturing ecosystems in Asia Pacific and Africa create high-growth opportunities for MEA. These regions are experiencing strong demand across consumer goods, oil & gas, construction materials, and textiles, where MEA serves as a core intermediate and functional ingredient. Growing urbanization, infrastructure development, and industrial output provide scalable platforms for market penetration, while strategic capacity expansions in countries such as India enhance long-term growth potential. Rising government incentives and private investments in chemical parks and industrial zones further reinforce the attractiveness of these emerging markets for MEA producers looking to scale.

MEA’s role in carbon capture and environmental technologies further strengthens its market prospects. India allocates approximately US$ 2.4 billion towards CCUS initiatives, promoting deployment of acid gas removal and CO capture technologies that rely on MEA. This governmental commitment highlights a supportive environment for MEA adoption in industrial decarbonization, positioning the chemical as a critical enabler at the intersection of emerging-market growth and global sustainability trends. The combination of industrial expansion and policy-driven environmental investments provides a dual growth lever for MEA demand in both commercial and green applications.

Category-wise Analysis

Grade Insights

Industrial grade MEA is expected to dominate by commanding approximately 70% of the monoethanolamine market revenue share, as well as volume share, in 2026. Its widespread use spans gas sweetening, industrial cleaning, agrochemical intermediates, and textile processing, with relatively lower purity requirements making it the preferred choice for bulk operations. Ongoing demand from upstream and midstream oil & gas facilities and strong penetration in mature markets ensures this grade remains the anchor segment. Its dominance is further supported by infrastructure scale and efficiency, exemplified by the Eni-Q8 Priolo biorefinery project in Italy, repurposing existing industrial chemical facilities into a biofuels and sustainable products hub. Such industrial repositioning reinforces demand for MEA in evolving chemical and energy ecosystems.

Pharmaceutical grade MEA is anticipated to be the fastest-growing segment, projected to grow at a CAGR of 6.5% during the 2026-2033 forecast period, driven by its rising demand in drug synthesis, high-purity intermediates, and specialty formulations. Stringent regulatory requirements for low-impurity chemicals and the global expansion of healthcare infrastructure increase the need for pharmaceutical-grade MEA. The growth trajectory is supported by expanding R&D investments and specialty chemical production capacity, positioning pharmaceutical-grade MEA as a high-value, rapidly expanding segment within the market.

End-User Industry Insights

The oil & gas industry is poised to account for an estimated 33% of the MEA market revenues in 2026, making it the largest end-user segment. MEA’s critical role in acid gas removal, CO? and H?S scrubbing, and refinery processing underpins its extensive adoption in upstream and midstream operations. Industrial-scale gas treatment facilities, refineries, and LNG plants rely heavily on MEA for operational efficiency and regulatory compliance, driving sustained consumption across major producing regions. The segment’s stability is reinforced by mature infrastructure, ongoing energy production, and continual upgrades to gas treatment and refinery processes, which ensure robust demand for industrial-grade MEA over the long term.

The pharmaceuticals & healthcare sector represents around 8% of global MEA demand and is projected to grow at a CAGR of 7% from 2026 to 2033, making it the fastest-growing end-user segment. Rising healthcare expenditure, aging populations, and increasing prevalence of chronic diseases drive higher demand for chemical intermediates used in drug synthesis and formulation. MEA’s functionality in producing high-purity intermediates positions it as a key enabler of modern pharmaceutical manufacturing processes. Growth is further supported by the PreCheck pilot program of the U.S. Food and Drug Administration (FDA), designed to expedite approvals for new pharmaceutical manufacturing facilities, enabling faster scaling of production and better compliance with quality standards. Expansion of specialty chemical production and R&D capacity, along with global healthcare infrastructure growth, continues to reinforce this sector’s accelerated uptake of pharmaceutical-grade MEA.

Regional Insights

North America Monoethanolamine (MEA) Market Trends

North America is a major regional contributor to the monoethanolamine market growth, driven by well-established industrial, energy, and pharmaceutical sectors. The United States leads consumption due to its extensive refinery networks, natural gas infrastructure, and chemical manufacturing capabilities, while Canada adds demand through its industrial chemical and energy sectors. MEA adoption spans oil & gas, consumer goods, and specialty chemical applications, where the chemical’s functionality in gas treatment, acid gas removal, and industrial process optimization ensures operational efficiency. Regional demand is further reinforced by a combination of mature infrastructure, skilled workforce, and high standards for product safety and handling.

Key growth drivers include ongoing expansion in oil & gas refining, strong industrial and consumer product demand, and regulatory frameworks that mandate emissions control and chemical safety compliance. The U.S. chemical industry outlook projects continued production growth due to low-cost feedstock sources, abundant energy resources, and advanced manufacturing capabilities, supporting consistent MEA demand. Investments in capacity expansions, process optimization, and high-purity MEA production facilities ensure that North America remains a stable, resilient, and strategically important regional market within the monoethanolamine industry.

Europe Monoethanolamine (MEA) Market Trends

Europe remains a vital market for MEA, with demand spread across industrial processes, detergents, gas treatment, and specialty chemical applications. Countries such as Germany, the U.K., France, and Spain lead consumption, driven by a combination of advanced manufacturing, sustainable product requirements, and evolving industrial standards. Compliance with regulations such as REACH ensures that chemical production prioritizes safety and environmental responsibility, encouraging companies to adopt cleaner manufacturing practices. At the same time, regional supply chains are well-established, enabling efficient distribution to both industrial and consumer-focused sectors. The focus on high-purity and specialty-grade MEA further strengthens Europe’s market relevance in global chemical production.

Innovation and regulatory support continue to shape growth trajectories. The European Commission (EC) Chemicals Industry Action Plan reinforces competitiveness through clear regulatory guidance, fiscal incentives, and support for sustainable technology adoption. Leading producers are concentrating on upgrading production facilities, lowering emissions, and expanding specialty MEA capacities to meet stricter safety and environmental standards. Meanwhile, rising demand in personal care and pharmaceuticals is driving companies to refine product quality and diversify offerings. These developments solidify Europe as a mature, innovation-driven, and steadily growing regional market for monoethanolamine.

Asia Pacific Monoethanolamine (MEA) Market Trends

Asia Pacific is estimated to account for a 43% of the monoethanolamine market share in 2026, making it the largest and fastest-growing regional market for MEA, with a projected CAGR of 6.8% over the 2026-2033 forecast period. The market here is driven by rapid industrialization, expanding chemical production, and growing consumer populations across China, India, and ASEAN countries. China leads in demand due to its extensive chemical manufacturing and refining infrastructure, while India is increasing output to support healthcare and specialty chemical sectors. Japan and ASEAN nations contribute through industrial, agrochemical, and consumer applications, creating a diverse and resilient demand base. Urbanization, infrastructure development, and rising standards for industrial efficiency further reinforce the region’s position as a key market for MEA.

The growth is underpinned by strong demand for surfactants in detergents, agrochemical intermediates, industrial process additives, and construction materials, which are essential for multiple end-use industries. The China Nanshan Group refinery project in Indonesia highlights ongoing investment in industrial capacity, supporting downstream chemical requirements including MEA for gas treatment and processing. Domestic producers in China and India are expanding production with government incentives and competitive energy costs, while investments in personal care grade MEA and agrochemical formulation facilities provide additional growth potential.

Competitive Landscape

The global monoethanolamine market structure is moderately consolidated, with major players such as Dow Chemical, BASF, Huntsman Corporation, OQ Chemicals, and LyondellBasell holding significant global and regional production capacity. These companies leverage strong industrial relationships, technical expertise, and large-scale manufacturing infrastructure to maintain market leadership. Investments in process optimization, high-purity MEA, and sustainable chemical technologies allow them to meet evolving regulatory standards and customer demands across oil & gas, pharmaceuticals, and specialty chemicals.

Regional and niche producers, including Shandong Nanshan Group, Shandong Haihua, and Aditya Birla Chemicals, focus on specific markets or specialty grades, supplying high-purity or industrial applications. Barriers such as feedstock volatility, compliance costs, and capital-intensive operations limit new entrants. Industry trends such as carbon capture adoption, bio-based MEA development, and downstream chemical integration are opening innovation and partnership opportunities. Market consolidation is expected to continue as established players expand capacity, acquire regional producers, and invest in technology upgrades.

Key Industry Developments

- In January 2026, Westlake Corporation expanded its specialty materials footprint in Europe by acquiring the global compounding solutions businesses of the ACI/Perplastic Group. This strategic move added manufacturing capabilities in Portugal and Romania, strengthening Westlake’s presence in high-value industrial compounds.

- In November 2025, INPEX officially commenced operations at its Kashiwazaki Hydrogen & Ammonia Demo Plant in Niigata Prefecture, Japan. The facility integrates blue hydrogen and ammonia production with CO? capture and local utilization for power and industrial needs, employing BASF HiPACT® CO? absorption technology and Tsubame BHB low-temperature ammonia synthesis.

- In November 2025, Kyndryl and Dow announced a strategic collaboration to enhance AI and automation capabilities across chemical manufacturing operations. The partnership focuses on improving operational efficiency, predictive maintenance, and digital workflow automation, highlighting the increasing adoption of intelligent process control in chemical plants.

Companies Covered in Monoethanolamine (MEA) Market

- BASF SE

- Huntsman Corporation LLC

- LyondellBasell Industries N.V.

- Nippon Shokubhai Co., Ltd.

- AkzoNobel N.V.

- Sasol Limited

- Jiaxing Jinyan Chemical

- Helm AG

- Sasol Fushun Huafeng

- Mitsui Chemicals

- Amines & Plasticizers Limited

- SABIC

- INEOS

- Tata Chemicals

- Helm AG

Frequently Asked Questions

The global monoethanolamine (MEA) market is projected to reach US$ 3.7 billion in 2026.

Growing demand for MEA in oil & gas, consumer goods, pharmaceuticals, and industrial applications is driving the market.

The market is poised to witness a CAGR of 5% from 2026 to 2033.

Expansion in bio-based and low-impurity MEA grades, adoption in emerging markets, and carbon capture applications represent key opportunities.

Dow Chemical, BASF, Huntsman Corporation, OQ Chemicals, and LyondellBasell are some of the leading players in the market.