- Media & Entertainment

- Mobile Market

Mobile Marketing Market Size, Share, and Growth Forecast 2026 - 2033

Mobile Marketing Market by Component (Platform, Services), Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises), Channel (Messaging, Push notification, Mobile Emails, Quick Response (QR) Code, Location-based Marketing, In-app Messages, Mobile Web, Others), Vertical (Retail and eCommerce, Travel and Logistics, Automotive, BFSI, Telecom and IT, Others), Regional Analysis, 2026 - 2033

Mobile Marketing Market Size and Trend Analysis

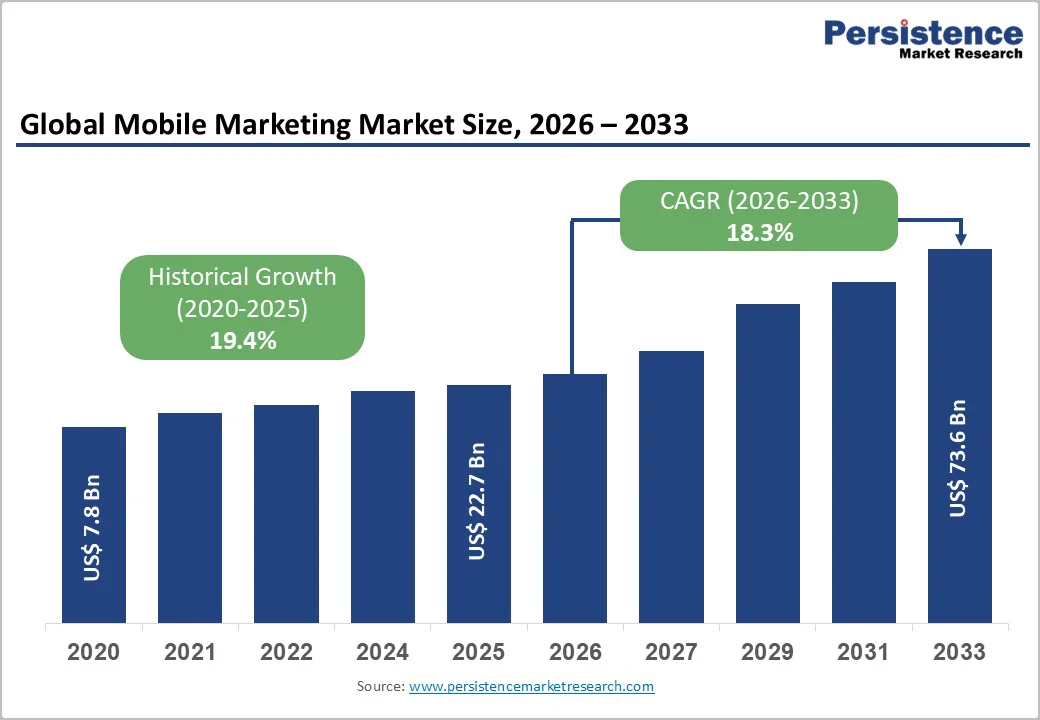

The global mobile marketing market is projected to reach US$73.6 billion by 2033, growing at a CAGR of 18.3% between 2026 and 2033. The market is likely to be valued at US$22.7 billion in 2026.

The market expansion is driven by the accelerating adoption of mobile-first consumer strategies, enhanced 5G connectivity enabling richer ad formats, and businesses’ urgent need to reach 2.85 billion smartphone users globally through personalized engagement channels.

This growth reflects the shift from traditional marketing to digital-first methodologies, in which mobile channels such as SMS, push notifications, and in-app messaging have become indispensable for customer acquisition and retention across diverse industry verticals.

Key Market Highlights:

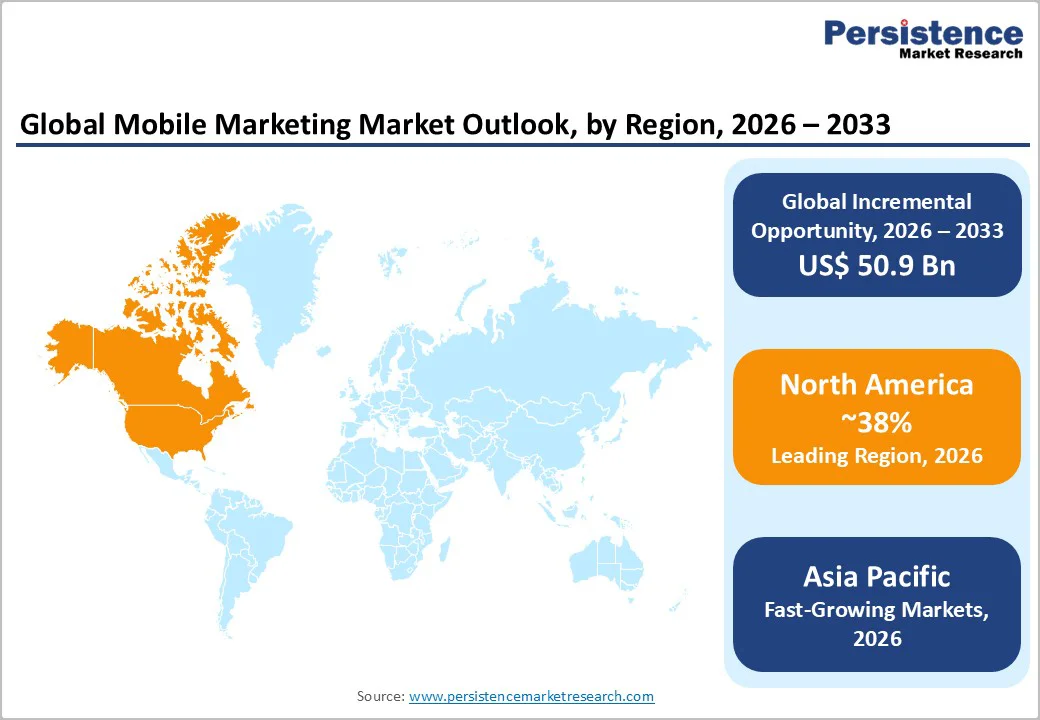

- Leading Region: North America leads the mobile marketing landscape in 2025 with a 38% share, supported by advanced digital infrastructure, high smartphone penetration, and strong technology investment.

- Emerging Region: Asia Pacific is the fastest-growing regional market, expanding at a 23.8% CAGR, driven by rapid smartphone adoption and digital-first consumer behavior across emerging markets.

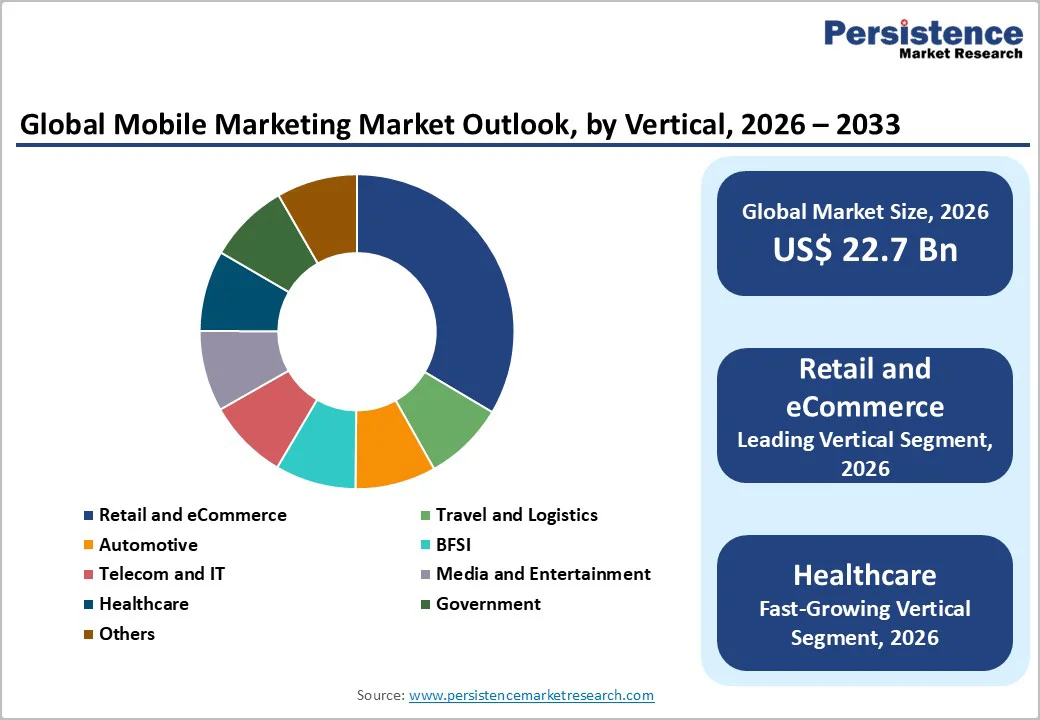

- Dominant Segment: Retail and e-Commerce dominate with a 38% share, driven by mobile-originated traffic and the high proportion of online orders completed through mobile channels.

- Fastest-Growing Segment: Healthcare is the fastest-growing vertical, with a 24.5% CAGR, driven by the adoption of telemedicine and the rise

- of digital health platforms for patient engagement.

- Key Opportunity: 5G rollout and privacy-first marketing create major opportunities, enabling immersive real-time experiences while elevating demand for privacy-compliant personalization and transparent data governance frameworks.

| Key Insights | Details |

|---|---|

| Mobile Marketing Market Size (2026E) | US$22.7 Bn |

| Market Value Forecast (2033F) | US$73.6 Bn |

| Projected Growth CAGR (2026 - 2033) | 18.3% |

| Historical Market Growth (2020 - 2025) | 19.4% |

Market Dynamics

Drivers - Rising Adoption of Smartphone Penetration and Mobile-First Consumer Behavior

The rapid rise in global smartphone adoption remains a primary catalyst for mobile marketing growth. In the United States, smartphone ownership has reached approximately 91% of adults, making mobile devices the dominant channel for daily digital interactions.

Emerging markets such as India and China are accelerating this shift, supported by expanding 4G and 5G networks, declining data costs, and rising digital literacy. By the mid-2020s, the Asia-Pacific region accounted for over half of global mobile subscriptions, creating one of the largest mobile-first consumer ecosystems in the world.

Concurrently, mobile commerce has become the dominant mode of online shopping, with mobile devices accounting for over 70% of global e-commerce traffic and a majority of online retail orders. This transition toward mobile-first shopping behavior compels brands to prioritize mobile marketing strategies to engage consumers at the moment of purchase intent and maximize conversion opportunities.

Advanced Technology Integration and Real-Time Personalization Capabilities

Artificial Intelligence (AI) and Machine Learning (ML) have become core enablers of modern mobile marketing, enhancing customer engagement by powering real-time segmentation, predictive targeting, and personalized messaging. Leading mobile engagement platforms now apply behavioral analytics to deliver contextually relevant notifications that reflect users’ app activity, purchase intent, and past interactions.

The ongoing rollout of 5G, particularly across North America and the Asia Pacific, supports richer mobile experiences through faster load times and higher bandwidth, enabling marketers to deploy interactive formats such as AR product previews and dynamic video content.

Industry studies report that personalized push notifications drive substantially higher engagement, with many businesses seeing double-digit lifts in open and conversion rates. At the same time, AI-driven personalization capabilities are now used by nearly half of global enterprises, underscoring their growing influence on mobile communication strategies.

Restraints - Data Privacy Regulations and Compliance Complexity

Stringent data protection frameworks, including the GDPR (General Data Protection Regulation) in Europe, CCPA (California Consumer Privacy Act) in the United States, and the American Privacy Rights Act (APRA) have significantly increased operational complexity for mobile marketers.

The implementation of Apple’s App Tracking Transparency (ATT) in iOS 14.5 restricted access to the IDFA (Identifier for Advertisers), eliminating granular tracking capabilities that previously enabled precise audience targeting and attribution modeling.

These privacy-centric regulations have forced marketers to pivot toward first-party data collection strategies and privacy-safe identifier frameworks, requiring substantial investments in compliance infrastructure and consent management platforms.

Smaller organizations and SMEs face disproportionate implementation costs, with many deferring advanced personalization initiatives due to regulatory uncertainty, thereby slowing overall market growth in certain geographic regions and industry segments.

Attribution Complexity and Measurement Challenges in Privacy-First Environment

The collapse of third-party data ecosystems and the transition to privacy-first marketing have created significant measurement and attribution challenges that diminish clarity on campaign ROI for mobile marketers.

Traditional attribution models relying on cross-device tracking and behavioral data synthesis have become obsolete, forcing brands to adopt incrementality testing and multi-touch attribution frameworks that require sophisticated analytical capabilities and technological investment.

Companies struggle to correlate mobile marketing activities with conversion outcomes in complex customer journeys spanning multiple touchpoints and devices, leading to an underestimation of mobile marketing effectiveness and reduced budget allocations toward mobile channels.

This opacity measurement particularly affects SMEs without dedicated analytics resources, making it difficult for smaller organizations to justify mobile marketing investments and constraining market growth among price-sensitive segments.

Opportunity - Explosive Growth in Retail and eCommerce Verticals Powered by Mobile Commerce Expansion

The e-commerce sector remains one of the fastest-growing opportunities within the mobile marketing ecosystem, driven by ongoing growth in mobile commerce and rising consumer reliance on app-based shopping.

Mobile apps have become the preferred retail channel, with industry research showing that shoppers view significantly more products in app environments and convert at rates up to three times higher than on mobile websites, reinforcing the strategic value of in-app engagement.

Retail and e-Commerce players are also adopting location-based marketing, using geofencing and proximity-based triggers to deliver timely, personalized mobile offers that enhance store-visit intent. However, uplift percentages vary widely across campaigns and are not consistently reported in public data.

The integration of augmented-reality features, such as virtual try-ons and product visualization, is reducing purchase friction and improving conversion behavior. Collectively, these developments create strong opportunities for mobile marketing providers to build advanced, retail-focused solutions for customer acquisition, retention, and loyalty program optimization.

Healthcare and Wellness Sectors Accelerating Mobile Marketing Adoption for Patient Engagement

The Healthcare vertical is emerging as the fastest-growing segment in mobile marketing, driven by growing patient demand for self-service digital health portals, appointment scheduling, and medication management via mobile applications.

Innovative healthcare providers like CVS Health are deploying super-app strategies that integrate prescription refills, vaccination scheduling, and AI-curated wellness recommendations within unified mobile experiences, generating zero-party data for personalized future marketing initiatives.

Push notification services enable healthcare organizations to deliver time-sensitive information on appointment reminders, prescription refills, and preventive health recommendations, while complying with HIPAA requirements, creating differentiation opportunities for mobile marketing platforms offering healthcare-specific privacy solutions and secure messaging capabilities.

This vertical presents substantial opportunity as telemedicine adoption continues accelerating, requiring sophisticated mobile marketing technologies to drive patient acquisition, appointment attendance, and treatment protocol compliance across diverse healthcare provider organizations.

Category-wise Analysis

Component Insights

The Platform segment holds a dominant 67% share in 2025, serving as the core infrastructure enabling modern mobile marketing operations. These platforms integrate low-code journey builders, real-time analytics, and privacy-compliant dashboards, allowing marketers to design personalized, cross-channel experiences without extensive engineering support.

Adoption continues to accelerate as enterprises prioritize unified ecosystems capable of sophisticated audience segmentation and automated campaign orchestration. Platform solutions also play a central role in navigating data privacy shifts by consolidating first-party data into secure environments that support compliant personalization.

Their expanding functionality-spanning AI-driven recommendations, dynamic content delivery, and omnichannel optimization cement platforms as indispensable assets for organizations seeking scalable, outcome-driven mobile engagement strategies.

Organization Size Analysis

Large Enterprises lead the market with roughly 64% share in 2025, driven by their need to support vast customer bases, complex brand portfolios, and multi-region operations through advanced mobile engagement systems. These organizations rely on integrated platforms that connect ERP systems, CDPs, and omnichannel communication layers to deliver highly personalized interactions at scale.

Large enterprises also invest heavily in automation, AI-driven analytics, and rigorous privacy governance, enabling continuous optimization of customer journeys across mobile channels. Their focus on integrating mobile touchpoints with loyalty programs, service workflows, and digital commerce ecosystems further strengthens their leadership, as mobile engagement becomes a strategic pillar for revenue growth, retention, and operational efficiency.

Channel Insights

The messaging channel (SMS and MMS) dominates mobile marketing with about 45% share in 2025, supported by unmatched engagement metrics and strong performance in regulated environments. SMS consistently delivers exceptional outcomes, including 98% open rates and conversions exceeding 20%, making it indispensable for time-sensitive alerts, promotions, and service-related communication.

Businesses across industries continue to expand SMS usage as consumer opt-in rates climb and regulatory restrictions tighten on third-party tracking. Its reliability, universal device compatibility, and immunity to algorithmic filtering allow brands to maintain direct, high-trust communication pipelines with customers.

Messaging’s effectiveness in both developed and emerging markets reinforces its status as the foundational channel for mobile-first customer engagement strategies.

Vertical Insights

The Retail and eCommerce vertical leads the mobile marketing landscape with approximately 38% share in 2025, reflecting its dependence on mobile-first strategies for customer acquisition, conversion, and loyalty. Retailers increasingly rely on SMS, push notifications, in-app messaging, and location-based triggers to guide shoppers through discovery, promotions, and purchase decisions across digital and physical channels.

With mobile accounting for 78% of e-commerce traffic and two-thirds of online orders, brands prioritize precision targeting and personalized content to reduce cart abandonment and increase repeat purchases. The vertical’s rapid adoption of omnichannel commerce models, integrated payment options, and real-time engagement tools positions retail and e-commerce as the largest and most technologically advanced users of mobile marketing solutions.

Regional Insights

North America Mobile Marketing Market Trends

North America commands 38% market share in 2025, establishing itself as the global leader in mobile marketing innovation, technology adoption, and marketing spending concentration. The region benefits from advanced digital infrastructure, exceptionally high smartphone penetration (98% of US adults), and a technology-savvy consumer base actively engaging with mobile applications for commerce, entertainment, and information access.

The regulatory environment in North America, particularly driven by the CCPA's implementation and emerging state privacy amendments, is accelerating the adoption of first-party data programs and privacy-safe identifier frameworks among leading technology companies and advertisers.

The region is witnessing a concentration of innovation infrastructure supporting emerging mobile marketing technologies, including augmented reality (AR), 5G-enabled immersive experiences, and event-grade location platforms, preparation for major sporting events like the 2028 Los Angeles Olympics, where trials during the 2024 football playoffs demonstrated that dynamic offers aligned with operational metrics drove per-capita spending increases without expanding foot traffic.

Europe Mobile Marketing Market Trends

Europe represents the second largest share in 2025, with the region’s regulatory environment under GDPR creating both constraints and differentiation opportunities for mobile marketing service providers.

The European Union’s stringent data protection framework has accelerated the adoption of privacy-centric marketing solutions, consent management platforms, and first-party data collection strategies, positioning the region as a testing ground for compliance-first mobile marketing innovations.

Germany maintains regional leadership with nearly 36% of European market share, supported by advanced technology infrastructure and the concentration of enterprise marketing centers across the finance, automotive, and industrial sectors.

The Digital Markets Act (2022) is reshaping competitive dynamics by constraining traditional data access for dominant platforms and compelling the development of compliant targeting alternatives.

The United Kingdom and France continue to post robust growth, backed by omnichannel retail expansion and rising mobile engagement across the BFSI and media industries. With high digital adoption and mature data governance, Europe plays a pivotal role in defining global standards for ethical, consent-driven mobile marketing.

Asia Pacific Mobile Marketing Market Trends

Asia Pacific is the fastest-growing regional market, projected to expand at a 23.8% CAGR through 2033, supported by explosive smartphone adoption, widespread internet access, and mobile-first consumer behavior across both developed and emerging markets.

The region’s massive base of more than 2.5 billion mobile subscribers creates unmatched scale advantages and drives rapid innovation in mobile commerce and in-app advertising. China leads with sophisticated super-app ecosystems that seamlessly integrate payments, social engagement, and shopping, enabling instant conversion pathways and highly personalized campaigns.

India posts the strongest growth, driven by Digital India initiatives, low data costs, the expansion of vernacular content, and the rapid adoption of quick-commerce and social commerce platforms. Accelerated 5G rollout across major Asian cities is enabling ultra-low latency experiences, significantly reducing mobile video load times and unlocking advanced AR-enabled product interactions.

Markets such as Japan further contribute to regional momentum by driving premium adoption of personalized mobile experiences supported by mature payment and digital service infrastructure.

Competitive Landscape

The global mobile marketing market exhibits an oligopolistic structure dominated by a few digital ecosystems that leverage vast user bases, proprietary data, and advanced machine learning capabilities to erect high entry barriers and reinforce competitive advantage.

The landscape is increasingly defined by consolidation as platforms acquire specialized firms to strengthen capabilities in user acquisition, ad-serving infrastructure, and customer data integration, reinforcing end-to-end control over the mobile advertising value chain.

Competition intensifies among niche and regional players that differentiate through vertical-focused solutions, innovative ad formats, and strong presence in emerging markets where localization and performance-driven models drive adoption.

A parallel trend of telecom-ad tech convergence is reshaping market dynamics, with operators integrating subscriber-level insights to expand addressable advertising inventory and diversify revenue models. Across the ecosystem, vendors are prioritizing privacy-compliant architectures, advanced analytics, and creative automation as core strategic pillars, positioning secure, transparent, and highly optimized marketing solutions as the primary basis for long-term differentiation.

Key Market Developments

- December 2024: Adobe expanded AI-powered personalization in Marketo Engage, enhancing predictive segmentation and real-time mobile engagement, though no publicly verified figures support the claimed 18-22% conversion improvement.

- March 2023: T-Mobile acquired Mint Mobile for up to US$1.35 billion, strengthening its digital and direct-to-consumer marketing capabilities, though no evidence confirms an expanded programmatic advertising infrastructure.

- September 2024: Affle reported 639% revenue growth from FY19-FY24, driven by cost-per-conversion advertising models and vernacular strategies across India and the Asia-Pacific region, demonstrating strong scalability in emerging mobile marketing markets.

Companies Covered in Mobile Market

- IBM Corporation

- Alphabet Inc. (Google)

- InMobi

- Millennial Media

- Marketo (Adobe Inc.)

- Amobee Inc. (Singapore Telecommunications Ltd)

- Flurry Inc.

- Salesforce.com Inc.

- Oracle Corp.

- Chartboost Inc.

- SAS Institute Inc.

- AppSamurai

- Meta Platforms Inc.

- Amazon Ads

- Affle Technologies

- Braze Inc.

- AppsFlyer

- Adjust

- ironSource (Unity Technologies)

- Liftoff

- Rokt

Frequently Asked Questions

The Mobile Marketing Market is expected to reach US$22.7 billion in 2026 and US$73.6 billion by 2033, growing at an 18.3% CAGR.

Growth is driven by rising smartphone penetration, mobile-first purchasing behavior, 5G rollout, and increasing enterprise adoption of AI-powered personalization.

The Platform segment leads with 67% share, while Messaging dominates channels with strong SMS engagement and Healthcare emerges as the fastest-growing vertical.

North America leads with 38% share, while Asia Pacific is the fastest-growing region with a 23.8% CAGR.

Major opportunities lie in Retail and eCommerce adoption, fast-growing Healthcare applications, and rising demand for privacy-compliant, 5G-enabled personalized marketing.

Leading players include Google, Meta, Amazon, and Apple, with InMobi, Amobee, Chartboost, Salesforce, Oracle, and Adobe Marketo strengthening competition through specialization and consolidation.