- Off-Road Equipment & Machinery

- Mobile Explosive Manufacturing Unit Market

Mobile Explosive Manufacturing Unit Market Size, Share, and Growth Forecast 2026 - 2033

Mobile Explosive Manufacturing Unit Market by Production Capacity (Up to 15 Ton, 15 to 25 Ton, Above 25 Ton), Discharge Type (Auger-based, Pump-based), Explosives Type (ANFO, HANFO, Emulsions, Universal/Others), and Regional Analysis, 2026 - 2033

Mobile Explosive Manufacturing Unit Market Size and Trend Analysis

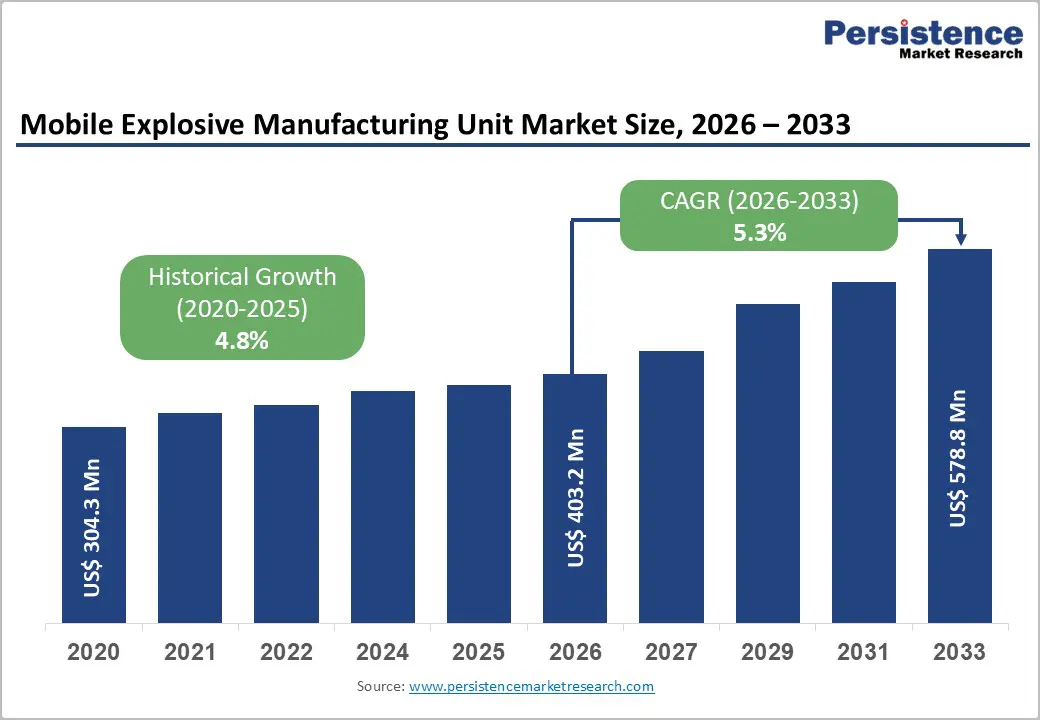

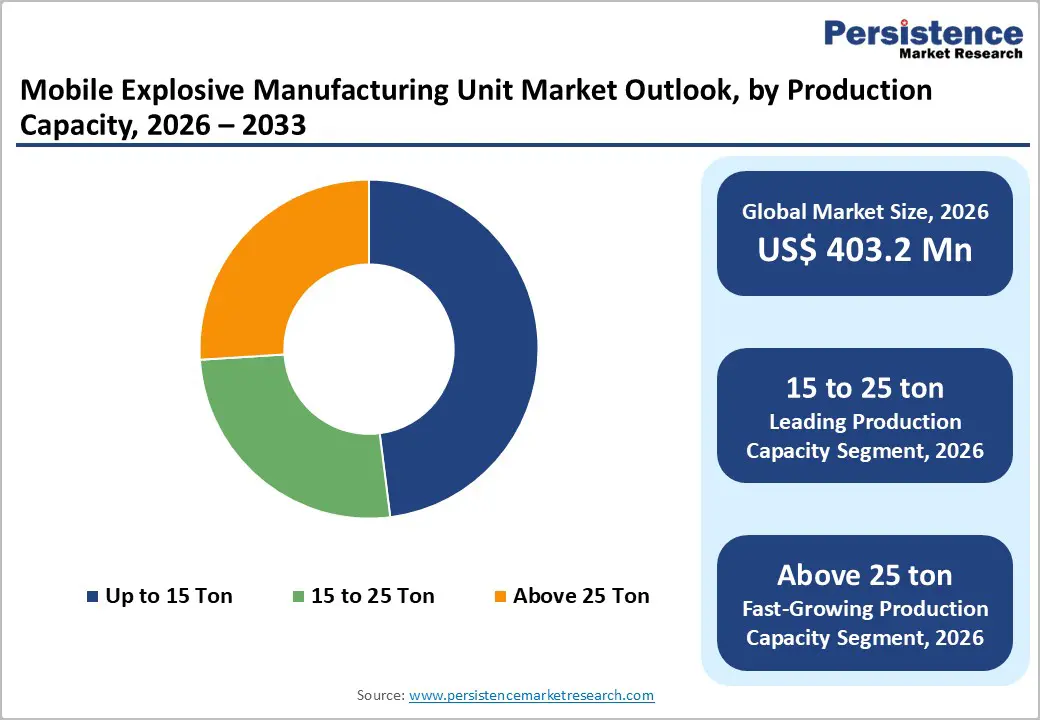

The global mobile explosive manufacturing unit market size is expected to be valued at US$ 403.2 million in 2026 and projected to reach US$ 578.8 million by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

This consistent expansion is primarily driven by rise in mining activities worldwide, particularly in coal, metallic minerals, and aggregate extraction, increasing infrastructure development projects requiring controlled blasting operations, and the operational advantages of on-site explosive manufacturing, including enhanced safety protocols, reduced transportation risks, and improved cost efficiency.

The growing adoption of surface mining techniques, rising demand for construction aggregates, and technological advancements in automated explosive formulation and delivery systems are compelling mining operators and construction companies to deploy mobile explosive manufacturing units that enable real-time production customization, minimize inventory requirements, and ensure regulatory compliance with explosives handling standards.

Key Industry Highlights:

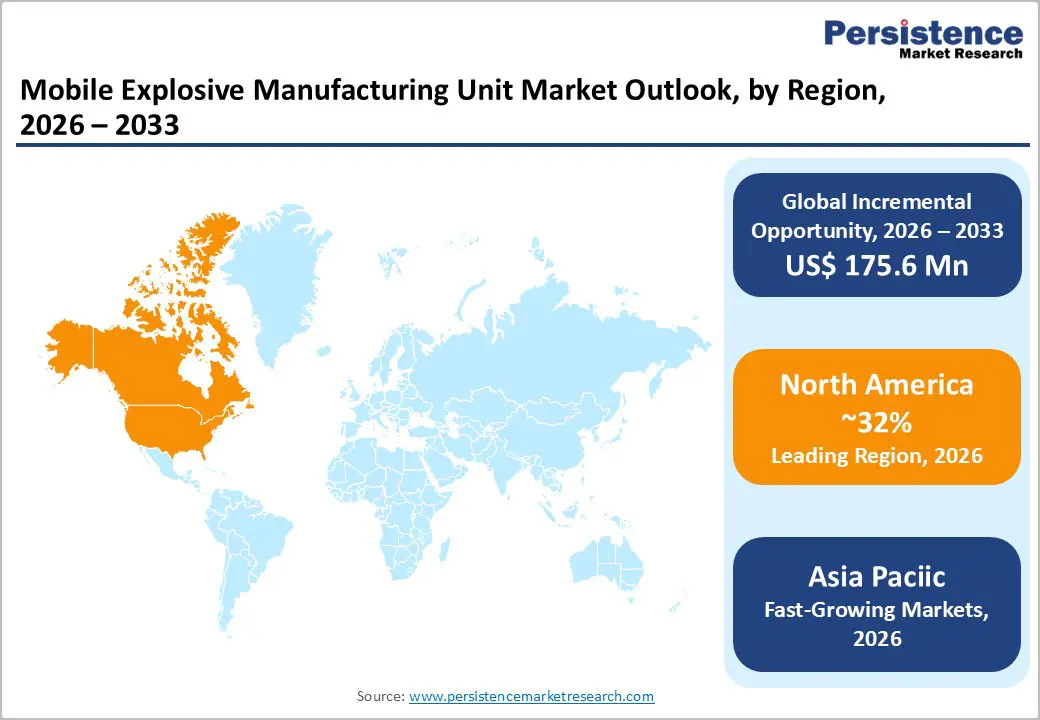

- Leading Region: North America leads the global market in 2025 with around 32% share, supported by large-scale surface mining activity, extensive infrastructure development, and strict regulatory frameworks that encourage on-site explosive manufacturing.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 6.8% during 2026 - 2033, driven by high coal output, accelerating infrastructure investments, and rising mineral extraction across emerging economies.

- Dominant Segment: The 15 to 25 ton production capacity segment dominates in 2025 with approximately 44% market share, as it best aligns with daily explosive consumption requirements, operational flexibility, and mobility needs of medium- to large-scale mining operations.

- Fastest Growing Region: Pump-based discharge systems are the fastest-growing segment through 2033, benefiting from higher productivity, improved loading precision, and superior performance in wet or complex borehole conditions compared to alternative systems.

- Key Opportunities: Opportunities are driven by increasing adoption of automation and digital controls, rising infrastructure investment in emerging markets, and a global shift toward environmentally improved emulsion explosive formulations.

| Key Insights | Details |

|---|---|

| Mobile Explosive Manufacturing Unit Market Size (2026E) | US$ 403.2 million |

| Market Value Forecast (2033F) | US$ 578.8 million |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Expanding Global Mining Activities and Mineral Extraction Demand

The continuous expansion of mining operations globally represents a fundamental driver for mobile explosive manufacturing units, with increasing demand for coal, metallic ores, industrial minerals, and construction aggregates necessitating efficient blasting solutions. According to the International Council on Mining and Metals (ICMM), the global mining industry contributes over US$ 1.7 trillion annually to the world economy, with significant portions reliant on controlled blasting operations for ore extraction. The U.S. Geological Survey (USGS) reports that domestic mining operations extracted over 3 billion metric tons of non-fuel mineral commodities in 2024, with surface mining accounting for approximately 90% of total production requiring regular blasting operations.

Mobile explosive manufacturing units enable mining operators to produce explosives on-site based on specific geological conditions, hole configurations, and blasting requirements, eliminating transportation costs and storage risks associated with pre-manufactured explosives. The Mine Safety and Health Administration (MSHA) emphasizes that on-site explosive production significantly reduces handling incidents and transportation accidents, which historically account for 12-15% of explosives-related safety events. Countries including Australia, Canada, Brazil, and South Africa are witnessing substantial mining expansion with major operators increasingly adopting mobile manufacturing units to optimize blasting efficiency, reduce operational costs, and maintain flexible production capabilities aligned with variable mining schedules and geological conditions.

Infrastructure Development and Construction Industry Growth

Large-scale infrastructure projects including highways, tunnels, railways, dams, and urban development initiatives require extensive rock excavation and controlled demolition operations, driving sustained demand for mobile explosive manufacturing capabilities. The American Road and Transportation Builders Association (ARTBA) reports that the United States infrastructure construction market exceeded US$ 350 billion in 2024, with significant portions involving rock excavation requiring blasting operations. The Infrastructure Investment and Jobs Act allocated US$ 1.2 trillion for infrastructure improvements across the United States, including major tunnel projects, highway expansions, and bridge construction that necessitate precision blasting capabilities.

Mobile explosive manufacturing units provide construction contractors with on-demand explosive production customized to specific project requirements, geological formations, and proximity to populated areas requiring carefully controlled blast parameters. The International Tunnelling and Underground Space Association (ITA) documents that global tunnel construction has increased by 25% over the past five years, with projects including the Brenner Base Tunnel in Europe and various metro systems in Asia requiring specialized explosive formulations produced on-site. The European Construction Industry Federation (FIEC) reports that construction blasting operations in Europe exceed 500 million cubic meters of rock excavation annually, with mobile manufacturing units enabling contractors to minimize logistical complexity, ensure quality consistency, and adapt formulations to varying rock hardness and environmental conditions throughout project lifecycles.

Restraints - Stringent Regulatory Requirements and Licensing Complexities

The mobile explosive manufacturing industry faces substantial regulatory challenges with comprehensive licensing requirements, stringent safety protocols, and extensive compliance documentation mandated by national and international authorities. The Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) in the United States enforces rigorous federal explosive manufacturing licenses under 27 CFR Part 555, requiring extensive background checks, facility inspections, security protocols, and ongoing compliance reporting.

The United Nations Economic Commission for Europe (UNECE) establishes international standards for explosives transport and storage through the Recommendations on the Transport of Dangerous Goods, creating complex regulatory frameworks that vary across jurisdictions. Mobile manufacturing unit operators must maintain multiple permits including manufacturing licenses, storage authorizations, transportation permits, and environmental clearances, with non-compliance resulting in operational shutdowns and substantial penalties. The regulatory burden is particularly challenging for smaller operators and contractors entering new geographical markets, with licensing processes typically requiring 6-18 months and substantial legal and compliance costs that can exceed US$ 100,000 per jurisdiction according to industry sources.

High Capital Investment and Maintenance Costs

Mobile explosive manufacturing units represent significant capital expenditures with sophisticated equipment, specialized vehicles, and comprehensive safety systems creating substantial financial barriers to market entry and fleet expansion. Advanced mobile manufacturing units incorporating automated mixing systems, precision dosing equipment, temperature controls, and integrated safety mechanisms can cost between US$ 1.5 million to US$ 5 million per unit depending on capacity and technological sophistication.

The National Institute for Occupational Safety and Health (NIOSH) mandates extensive safety features including explosion suppression systems, continuous monitoring equipment, and emergency shutdown mechanisms that compound equipment costs. Maintenance requirements for mobile units operating in harsh mining environments demand specialized technical expertise, regular component replacement, and comprehensive safety inspections that can represent 15-20% of initial capital costs annually. The complexity of maintaining multiple chemical storage systems, precision mixing equipment, and hydraulic discharge mechanisms requires trained personnel and substantial spare parts inventory, creating ongoing operational expenses that challenge profitability, particularly during mining industry downturns or periods of reduced construction activity.

Opportunity - Adoption of Automated and Digitally-Controlled Manufacturing Systems

The integration of automation technologies, digital controls, and Internet of Things connectivity in mobile explosive manufacturing units presents substantial opportunities for manufacturers to deliver next-generation solutions with enhanced precision, safety, and operational efficiency. The Institute of Makers of Explosives (IME) promotes advanced manufacturing technologies that improve explosive quality consistency, reduce human error, and enable real-time production monitoring aligned with Industry 4.0 principles. Modern mobile units are incorporating automated ingredient weighing systems, computerized mixing protocols, temperature and density sensors, and GPS-enabled batch tracking that ensure consistent product quality while generating comprehensive documentation for regulatory compliance.

The International Society of Explosives Engineers (ISEE) reports that automated mobile manufacturing systems can reduce formulation errors by over 90% while improving production speeds by 30-40% compared to manually-controlled units. Leading manufacturers are developing cloud-connected systems that enable remote monitoring, predictive maintenance alerts, and automated inventory management, with data analytics platforms optimizing formulations based on geological conditions, weather parameters, and blast performance feedback. Mining operators are increasingly specifying automated systems that integrate with mine management software, providing real-time production data, consumption tracking, and cost analysis that enhance operational visibility and decision-making capabilities throughout blasting operations.

Emerging Markets Infrastructure Development and Mining Expansion

Rapid economic development in emerging markets across Asia, Africa, and Latin America is driving unprecedented infrastructure investment and natural resource extraction, creating substantial growth opportunities for mobile explosive manufacturing unit suppliers. The Asian Development Bank (ADB) estimates that Asia alone requires US$ 1.7 trillion in annual infrastructure investment through 2030, with significant portions involving tunneling, road construction, and mining activities requiring blasting capabilities. India's National Infrastructure Pipeline encompasses over 7,400 projects worth US$ 1.4 trillion through 2025, including highways, railways, and mining developments that will drive explosive consumption.

The African Development Bank reports that African countries are investing heavily in infrastructure with major projects including the Grand Ethiopian Renaissance Dam, trans-African highway networks, and expanding mining operations in countries including Democratic Republic of Congo, Zambia, and Ghana. These emerging markets often lack established explosive distribution infrastructure, making mobile manufacturing units particularly valuable for remote mining operations and infrastructure projects in areas with limited transportation networks. The Latin American Energy Organization (OLADE) documents significant mining expansion across Chile, Peru, and Brazil, with copper, lithium, and iron ore projects requiring flexible blasting solutions that mobile manufacturing units can efficiently provide while minimizing logistical complexity in geographically challenging regions.

Category-wise Analysis

Production Capacity Insights

The 15 to 25 ton production capacity segment holds a leading market position, accounting for around 44% share in 2025, due to its strong alignment with operational requirements of medium- to large-scale surface mining and construction projects. This capacity range effectively supports typical daily explosive consumption patterns without necessitating multiple units or excessive on-site storage. It offers an optimal balance between output capability and mobility, enabling efficient deployment across geographically dispersed sites. Units in this segment are designed with advanced mixing technologies and multiple ingredient storage systems while remaining compliant with road transport regulations. As a result, the 15-25 ton segment is widely preferred by mining contractors and aggregates producers seeking operational flexibility, reliability, and cost efficiency.

Discharge Type Insights

Pump-based discharge systems dominate the market, capturing approximately 62% share in 2025, driven by their superior loading precision and compatibility with modern explosive formulations. These systems use positive displacement pumps to deliver consistent explosive density directly into blast holes, regardless of depth or inclination. Their ability to support continuous loading operations significantly improves productivity while minimizing explosive handling risks. Pump-based systems are particularly well suited for emulsion explosives, which require controlled and uniform placement to achieve optimal blast performance. Advanced automation features, including pressure monitoring and density control, further enhance operational accuracy. Consequently, pump-based discharge systems are increasingly adopted in complex blasting environments where precision, safety, and efficiency are critical.

Explosives Type Insights

Emulsion explosives represent the largest explosives type segment, holding nearly 38% share in 2025, reflecting a clear industry shift toward safer and more adaptable blasting solutions. These formulations provide excellent water resistance, adjustable energy output, and lower fume generation compared to conventional alternatives. Their inherent safety during manufacturing and handling makes them suitable for stringent regulatory environments. Emulsions also perform consistently across varying geological and climatic conditions, supporting their widespread adoption in surface and underground mining. Mobile manufacturing units enable on-site formulation adjustments, allowing blast engineers to tailor explosive properties to specific rock characteristics. This flexibility, combined with improved fragmentation control, continues to strengthen emulsion explosives’ market leadership.

Regional Insights

North America Mobile Explosive Manufacturing Unit Market Trends and Insights

North America maintains a leading regional position with approximately 32% market share in 2025, underpinned by extensive surface mining operations, substantial aggregates production, and comprehensive infrastructure development activities across the United States and Canada. The U.S. Geological Survey reports that domestic mining operations produce over 1.4 billion metric tons of crushed stone, 950 million metric tons of sand and gravel, and substantial metallic mineral output annually, with the majority requiring blasting operations that drive mobile explosive manufacturing unit demand.

The regulatory environment significantly influences market dynamics, with the Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) enforcing comprehensive explosive manufacturing and storage regulations, while the Mine Safety and Health Administration (MSHA) mandates strict safety protocols for explosive handling at mining operations. The National Institute for Occupational Safety and Health (NIOSH) conducts ongoing research into explosive safety technologies, promoting adoption of advanced manufacturing systems with enhanced safety features.

Canada's mining sector, particularly operations in Ontario, Quebec, and British Columbia, demonstrates strong mobile manufacturing unit adoption driven by remote mine locations, harsh climate conditions, and preference for on-site production capabilities that eliminate transportation challenges. The Natural Resources Canada agency reports sustained mining investment with particular growth in critical minerals extraction supporting electrification and clean energy transitions, creating new opportunities for specialized explosive formulations and manufacturing capabilities.

Europe Mobile Explosive Manufacturing Unit Market Trends and Insights

Europe demonstrates steady market performance characterized by stringent safety regulations, environmental consciousness, and emphasis on sustainable blasting technologies across mining and civil construction applications. The European Federation of Explosives Engineers (EFEE) promotes best practices in explosive manufacturing and application, with member countries implementing harmonized safety standards aligned with European Union directives. Germany leads regional demand through its extensive aggregates production, tunnel construction projects, and remaining coal mining operations, with the German Mining Association reporting continued investment in modernized blasting technologies despite energy transition policies.

The United Kingdom's quarrying industry and civil engineering sector maintain consistent demand for mobile explosive manufacturing units, with the Quarry Products Association documenting annual production exceeding 200 million tonnes of aggregates requiring blasting operations. France demonstrates growing adoption in major infrastructure projects including tunnel construction, highway development, and urban redevelopment initiatives requiring precision blasting near sensitive structures.

The European Union's ATEX Directive (2014/34/EU) establishes comprehensive equipment safety requirements for explosive atmospheres, compelling manufacturers to incorporate advanced safety features and explosion protection systems. Spain's mining sector and extensive quarrying operations in regions including Catalonia and Andalusia support market demand, while the European Commission's emphasis on sustainable construction practices is driving interest in blasting technologies that minimize environmental impact, reduce emissions, and optimize material utilization efficiency.

Asia Pacific Mobile Explosive Manufacturing Unit Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market with an anticipated CAGR of 6.8% during 2026-2033, propelled by massive infrastructure development, expanding coal and metallic mineral mining, and increasing aggregates demand across rapidly developing economies. China dominates regional consumption through its position as the world's largest coal producer and consumer, extensive non-ferrous metal mining, and unprecedented infrastructure construction, with the National Bureau of Statistics of China reporting coal production exceeding 4.5 billion tonnes annually requiring substantial blasting operations. The Belt and Road Initiative continues to drive regional infrastructure investment with major tunnel, highway, and railway projects across participating countries creating sustained explosive demand.

India represents a high-growth opportunity market driven by expanding coal production to meet energy demand, growing metallic minerals extraction, and ambitious infrastructure development under programs including Bharatmala for highways and Sagarmala for port connectivity. The Ministry of Mines reports significant production increases in coal, iron ore, and bauxite with surface mining predominating and requiring mobile explosive manufacturing capabilities.

Australia's mining sector, while mature, maintains robust demand through large-scale iron ore, coal, and gold operations, with the Minerals Council of Australia reporting the industry's economic contribution exceeding US$ 200 billion annually. Indonesia, Vietnam, and Mongolia demonstrate accelerating mining activities and infrastructure development, with the Association of Southeast Asian Nations (ASEAN) infrastructure investment projected to exceed US$ 3 trillion through 2030, creating substantial opportunities for mobile explosive manufacturing unit suppliers serving geographically dispersed projects with limited existing explosive distribution infrastructure.

Competitive Landscape

The global mobile explosive manufacturing unit market is characterized by a moderately consolidated structure, with a limited number of established participants accounting for a significant share of installed capacity and service contracts. Market structure is shaped by high entry barriers, including stringent safety regulations, capital-intensive manufacturing requirements, and the need for specialized technical expertise. Competitive strategies largely center on vertical integration, enabling suppliers to deliver end-to-end blasting solutions that combine equipment manufacturing, explosive formulation, and on-site technical services.

Differentiation increasingly relies on technology-led offerings, such as automation, digital monitoring, and advanced safety systems that enhance operational efficiency and regulatory compliance. In addition, service-oriented business models are gaining prominence, with players emphasizing long-term contracts, technical support, and operator training to deepen customer engagement. Geographic expansion into emerging mining regions and sustained investment in environmentally improved formulations and digitally enabled systems further define competitive positioning across the market.

Key Developments

- April 2025 - Dyno Nobel unveiled world’s first mine-ready electric mobile processing unit (MPU) for explosives delivery, featuring a 390 kWh battery and regenerative braking to reduce emissions and enhance sustainable mining operations.

Companies Covered in Mobile Explosive Manufacturing Unit Market

- Orica Limited

- Transmanut

- NIPIGORMASH

- Enaex

- Dyno Nobel Pty Limited

- Austin Powder Holdings Company

- EPC Group

- Dahana

- Timberland Equipment Limited

- AECI

- Maxam Corp

- Sasol Limited

- Solar Industries India Limited

- LSB Industries

- Nelson Brothers

Frequently Asked Questions

The mobile explosive manufacturing market is expected to reach about US$ 403.2 million in 2026, supported by steady growth in mining and infrastructure activities.

Demand is driven by expanding mining operations, large-scale infrastructure development, improved on-site safety, and lower transportation and operating costs.

North America leads the market, supported by extensive surface mining activity, strong infrastructure spending, and strict regulatory frameworks.

Key opportunities include automation and digital integration, rising infrastructure investment in emerging markets, and increasing adoption of emulsion explosives.

Leading manufacturers include Orica Limited, Dyno Nobel Pty Limited, AECI, Austin Powder Holdings Company, Enaex, Maxam Corp, and Solar Industries India Limited.