- Hardware & Software IT Services

- Mobile Apps and Web Analytics Market

Mobile Apps and Web Analytics Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Mobile Apps and Web Analytics Market by Component (Solutions, Services, Managed Services, Professional Services), Deployment Model (On-premise, Cloud), Application (Mobile advertising and marketing analytics, Search Engine tracking and ranking, Heat Map Analytics, Marketing Automation, Content Marketing, Email Marketing, Social Media Management), Organization Size, Industrial, and Regional Analysis, 2026 - 2033

Mobile Apps and Web Analytics Market Size and Trend Analysis

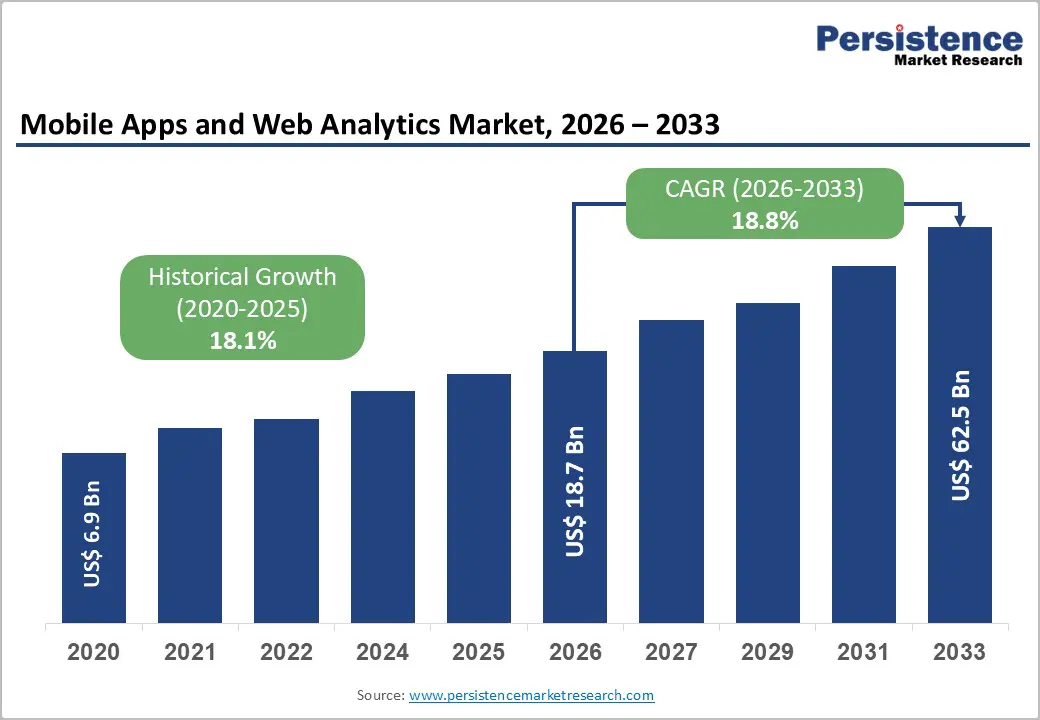

The global mobile apps and web analytics market is projected to reach US$ 18.7 billion in 2026 and US$ 62.5 billion by 2033, growing at a CAGR of 18.8% from 2026 to 2033.

Market growth is primarily driven by the exponential rise in smartphone adoption and the subsequent shift toward mobile-first digital strategies by enterprises. As organizations prioritize data-driven decision-making, the integration of Artificial Intelligence (AI) and Machine Learning (ML) into analytics platforms has become a critical catalyst, enabling real-time predictive insights and hyper-personalization.

Key Industry highlights:

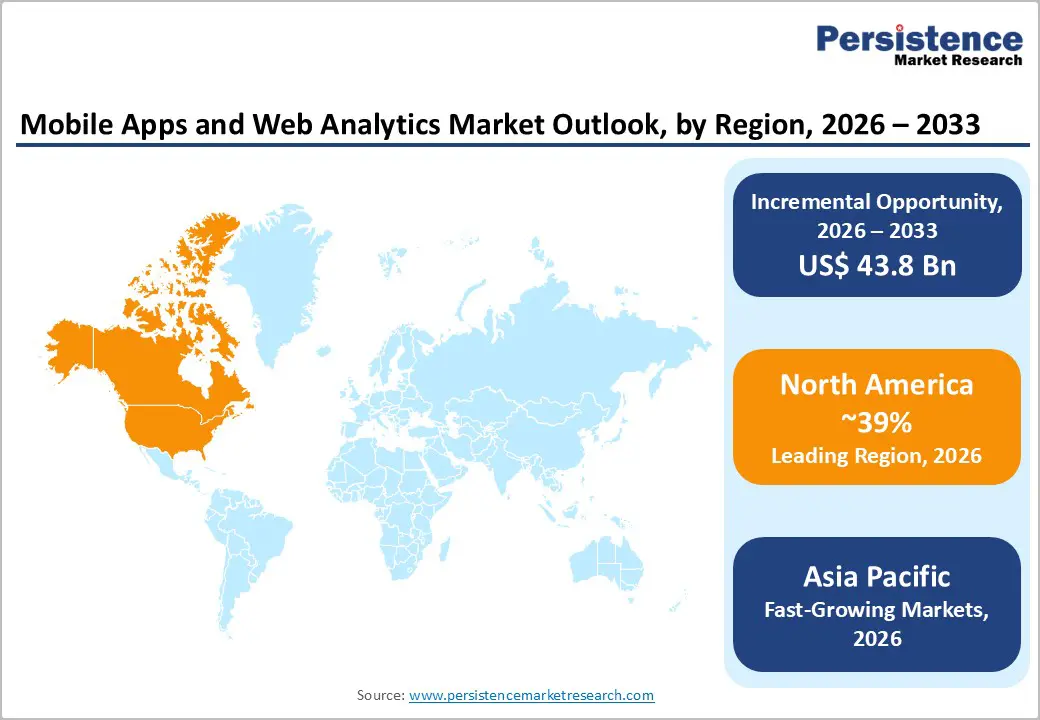

- Leading Region: North America dominates the market share due to early technology adoption and the presence of major analytics vendors.

- Fastest Growing Region: Asia Pacific is expected to witness the highest growth rate, driven by massive smartphone adoption and digital transformation in India and China.

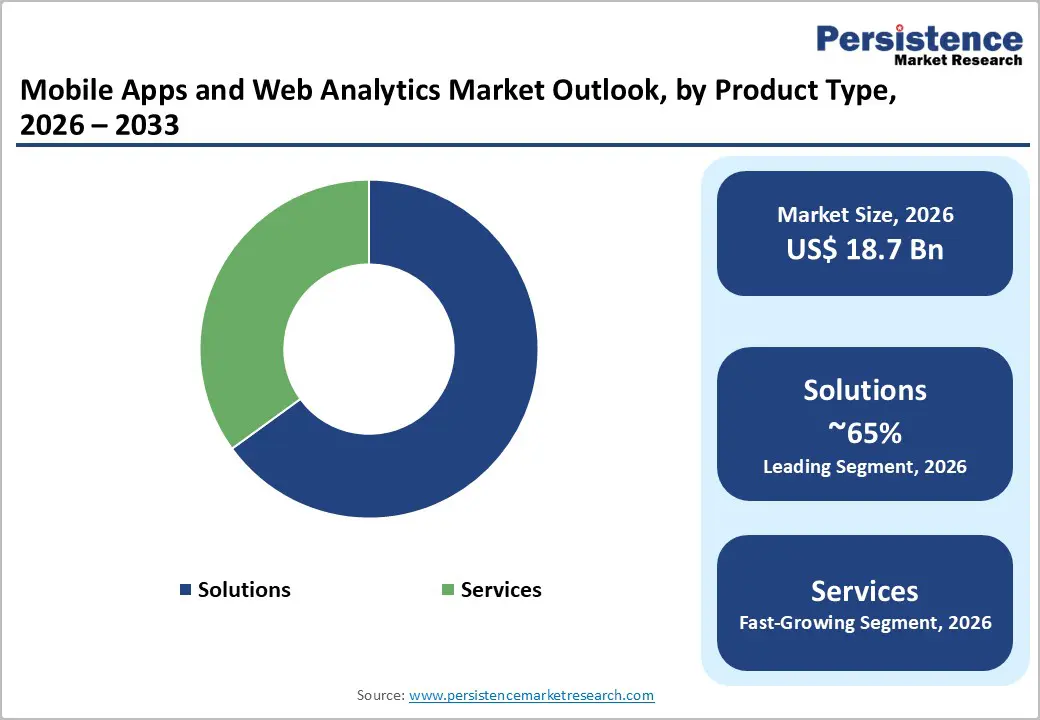

- Dominant Segment: The Solutions component captures the majority of revenue, offering comprehensive, end-to-end data analysis platforms for enterprises.

- Fastest Growing Segment: The Mobile advertising and marketing analytics application is expanding rapidly as budgets shift decisively toward mobile-first ad strategies.

- Key Opportunity: Expansion into the Healthcare vertical with privacy-compliant, predictive analytics tools represents a significant untapped revenue pocket.

| Key Insights | Details |

|---|---|

| Mobile Apps and Web Analytics Market Size (2026E) | US$ 18.7 Billion |

| Market Value Forecast (2033F) | US$ 62.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 18.8% |

| Historical Market Growth (2020 - 2025) | 18.1% |

Market Dynamics

Drivers - AI-driven Predictive and Prescriptive Analytics Enhancing Customer Intelligence, Personalization, and Operational Decision-Making across Digital Platforms

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into analytics platforms is a major factor driving market growth. Organizations are increasingly shifting from basic descriptive analytics to advanced predictive and prescriptive analytics to anticipate user behavior and future outcomes. AI-powered platforms can now predict customer churn with accuracy levels exceeding 85%, enabling businesses to take proactive actions to retain high-risk customers. Leading digital platforms such as Netflix and Spotify use AI-driven analytics to deliver personalized content recommendations, helping improve user engagement by nearly 30%. These technologies enable enterprises to automate complex data analysis, uncover hidden patterns in customer journeys, and deliver real-time personalization at scale. As a result, businesses can significantly improve customer lifetime value (CLV), reduce operational inefficiencies, and make faster, data-driven decisions. The growing need for intelligent automation and predictive insights across industries continues to accelerate the adoption of AI- and ML-enabled analytics solutions.

Rising Smartphone Usage Accelerating Mobile-First Business Models and Driving Demand for Advanced Mobile Analytics Solutions

The widespread adoption of smartphones has fundamentally changed how consumers interact with digital platforms, creating a strong demand for advanced mobile analytics solutions. This shift has encouraged businesses across sectors such as Retail and BFSI to adopt mobile-first strategies, where mobile applications serve as the primary customer engagement channel.

As a result, companies increasingly rely on analytics tools that track session duration, in-app navigation paths, crash reports, and behavioral patterns. These insights help organizations optimize user interface design, enhance app performance, and reduce customer friction points. Businesses are investing heavily in mobile analytics platforms to gain visibility into real-time user experiences and improve conversion rates. The growing importance of mobile commerce, digital banking, and app-based services continues to drive strong demand for specialized mobile and web analytics software worldwide.

Restraints - Strict Global Data Privacy Regulations Increasing Compliance Costs and Limiting the Depth of User-Level Analytics Insights

Strict data privacy regulations represent a major challenge for the growth of the analytics market. Laws such as the General Data Protection Regulation (GDPR) in Europe, the California Consumer Privacy Act (CCPA) in the United States, and the emerging American Privacy Rights Act (APRA) of 2024 impose tight controls on data collection, storage, and processing. These regulations require organizations to obtain explicit user consent, limit tracking activities, and anonymize personal data.

As a result, analytics providers face increased operational complexity and reduced access to detailed user-level information. Non-compliance can result in severe penalties, including fines of up to 4% of global annual revenue. To mitigate risks, companies must invest heavily in compliance management, legal expertise, and secure data infrastructure. These requirements increase costs and limit the effectiveness of traditional analytics models, slowing adoption rates and creating barriers for smaller firms with limited compliance resources.

Fragmented Enterprise Data Systems and Integration Complexities Hindering Unified Analytics and Accurate Customer Insights

Data silos and integration issues continue to restrict market growth by limiting the effectiveness of analytics solutions. Large enterprises often operate multiple legacy systems in which customer data is stored across disconnected platforms, such as marketing tools, CRM systems, and customer support databases. Integrating these systems to create a unified view of customer behavior is technically complex and time-consuming.

Fragmented data environments result in incomplete insights, inconsistent reporting, and inaccurate decision-making. Addressing these challenges requires significant investment in data integration tools, skilled IT resources, and custom middleware solutions. The high cost and technical complexity associated with breaking down data silos discourage many small and mid-sized organizations from adopting comprehensive analytics platforms. As a result, integration challenges remain a key restraint affecting market expansion.

Opportunity - Growing Adoption of Predictive Analytics in Healthcare and Government Creating New Revenue Opportunities for Analytics Providers

Significant growth opportunities exist for analytics vendors in expanding predictive analytics solutions into non-traditional verticals such as Healthcare and Government. While the retail and BFSI sectors were early adopters, healthcare organizations are increasingly digitizing patient engagement through mobile apps and online portals. Predictive analytics can help forecast patient adherence to treatment plans, optimize appointment scheduling, and improve care outcomes. Similarly, government agencies are using analytics tools to enhance citizen service portals, improve resource allocation, and optimize digital interactions.

However, these sectors require industry-specific and highly compliant solutions, such as HIPAA-compliant analytics platforms for healthcare applications. Vendors that develop customized modules addressing unique regulatory, operational, and security requirements can unlock substantial new revenue streams. As digital transformation accelerates across public and social infrastructure, demand for compliant, predictive, and user-focused analytics tools is expected to rise steadily.

Emergence of Voice and Visual Search Transforming Consumer Behavior and Creating New Frontiers for Advanced Analytics Platforms

The rapid adoption of voice assistants and visual search technologies presents a strong opportunity for innovation within the analytics market. As voice-based interactions become more common, traditional text-focused analytics and SEO tools are no longer sufficient. Analytics platforms that can interpret voice commands, conversational queries, and visual inputs provide businesses with a competitive advantage.

This trend is particularly important in the E-commerce sector, where visual search enables consumers to shop by uploading images instead of typing keywords. Vendors that offer analytics to track voice and visual interactions can help brands optimize content, product discovery, and digital marketing strategies. As consumer behavior evolves, solutions that support these new engagement formats will play a critical role in shaping next-generation digital analytics.

Category-wise Analysis

Component Insights

The solutions segment currently dominates the market, accounting for approximately 62% of the total share. This dominance is driven by the strong adoption of comprehensive analytics platforms that offer end-to-end capabilities such as data collection, visualization, reporting, and insight generation. Enterprises increasingly prefer integrated solutions that can manage both web and mobile data within a single platform. These solutions provide real-time dashboards, automated reporting, and AI-driven insights without requiring extensive customization.

Continuous innovation by leading vendors, including the integration of machine learning and predictive analytics features, further strengthens the position of the Solutions segment. In contrast, services are often used as supporting components rather than core offerings. The growing demand for scalable, ready-to-deploy analytics software ensures that solutions remain the preferred choice for organizations seeking faster implementation and measurable business outcomes.

Deployment Model Insights

Cloud-based deployment holds the leading market share, estimated at around 65%, and continues to outperform on-premise solutions. Organizations favor cloud analytics due to lower upfront costs, faster deployment, and flexible scalability. Cloud platforms allow businesses to process large data volumes without investing in expensive infrastructure. The rise of remote work and geographically distributed teams has further increased demand for cloud-accessible dashboards and collaboration tools.

Major vendors such as Google and Adobe primarily offer their advanced analytics solutions through cloud models, ensuring automatic updates and enhanced security. Cloud platforms are also better equipped to handle traffic spikes during high-demand periods, such as major retail events. These advantages make cloud deployment the preferred option across industries, supporting its continued market leadership.

Application Insights

Mobile advertising and marketing analytics represent the largest application segment, capturing approximately 34% of the market share. This leadership reflects the rapid shift of advertising budgets from traditional channels to mobile and digital platforms. Organizations rely on analytics tools to measure return on ad spend (ROAS), monitor campaign performance, and optimize user acquisition strategies in real time.

These solutions enable marketers to evaluate which channels, creatives, and formats deliver the highest-quality traffic. Granular insights into attribution and conversion behavior help businesses maximize marketing efficiency and revenue generation. As mobile commerce and app-based engagement continue to grow, the importance of mobile marketing analytics remains strong, reinforcing this segment’s dominant position.

Organization Size Insights

Large enterprises dominate the market by organization size, holding approximately 58% of the total share. These organizations generate massive volumes of data that require advanced analytics platforms with strong processing capabilities and high security standards. Large companies in sectors such as Banking and Telecommunications have the financial capacity to invest in premium analytics solutions and custom integrations. Their need for advanced reporting, compliance, and dedicated support services further supports adoption. However, small and medium-sized enterprises (SMEs) are emerging as the fastest-growing segment. The availability of affordable, subscription-based SaaS analytics tools is lowering entry barriers, enabling SMEs to adopt data-driven strategies without large capital investments.

Industrial Insights

The BFSI sector leads the market, accounting for approximately 38% of the total share. This dominance is driven by the rapid digital transformation of financial services and the critical importance of security, fraud detection, and customer experience. Banks and financial institutions use analytics tools to monitor user behavior, improve interface security, and reduce transaction drop-offs. The growth of fintech platforms and neobanks has increased the need for personalized financial offerings based on user insights. Given the high lifetime value of customers in this sector, BFSI organizations are willing to invest heavily in advanced analytics platforms to enhance retention, compliance, and profitability.

Regional Insights

North America Mobile Apps and Web Analytics Market Trends

North America continues to dominate the global mobile apps and web analytics market due to its advanced digital ecosystem and early adoption of data-driven business models. The region benefits from the strong presence of leading technology providers such as Google, Adobe, Microsoft, and IBM, which continuously innovate analytics platforms with AI and Generative AI capabilities. The United States remains the primary growth engine, where enterprises across BFSI, Retail, Media, and Healthcare heavily rely on analytics to optimize customer experience and operational efficiency.

Strict regulatory frameworks such as the California Consumer Privacy Act (CCPA) have accelerated the development of privacy-compliant analytics solutions, including server-side tracking and consent management platforms. North America also possesses a highly mature cloud infrastructure, enabling widespread adoption of SaaS-based analytics tools. The combination of technological leadership, high digital maturity, and strong enterprise spending ensures sustained market leadership in the region.

Europe Mobile Apps and Web Analytics Market Trends

Europe represents a mature yet steadily evolving market, strongly shaped by its regulatory-first approach to data privacy and digital governance. The implementation of the General Data Protection Regulation (GDPR) has significantly influenced how analytics platforms operate, positioning Europe as a global hub for privacy-by-design and consent-driven analytics solutions. Enterprises across Germany, the United Kingdom, France, and the Nordic countries are shifting away from third-party data dependencies toward first-party data strategies.

This transition has increased adoption of server-side tagging, anonymized tracking, and integrated consent management tools. Furthermore, growing emphasis on data sovereignty has fueled demand for regional and sovereign cloud deployments to ensure data residency compliance. While regulatory complexity may slow adoption in some cases, it also drives innovation in compliant analytics technologies, allowing European businesses to maintain insight quality while protecting user privacy.

Asia Pacific Mobile Apps and Web Analytics Market Trends

Asia Pacific is projected to be the fastest-growing region in the mobile apps and web analytics market, driven by rapid digitalization and expanding smartphone penetration. Countries such as China, India, Indonesia, and Vietnam are experiencing a surge in mobile internet usage, making mobile app analytics a higher priority than traditional web analytics. In China, the dominance of super apps such as WeChat, Alipay, and Meituan has created demand for specialized ecosystem-based analytics solutions.

Meanwhile, India and ASEAN markets are witnessing accelerated growth in BFSI, E-commerce, and digital payments, leading to increased demand for scalable and cost-effective analytics platforms. The region’s growing startup ecosystem and adoption of cloud-based SaaS models further support market expansion. Additionally, the rising deployment of IoT-enabled devices in manufacturing and smart infrastructure is broadening analytics use cases beyond consumer applications, strengthening long-term regional growth prospects.

Competitive Landscape

The global mobile apps and web analytics market is characterized by a moderately consolidated structure at the top, with a fragmented tail of niche providers. Tech behemoths such as Google, Adobe, and Microsoft command a significant portion of the market share due to their comprehensive ecosystems and ability to bundle analytics with other cloud and advertising services. However, the market also hosts a vibrant array of specialized players focusing on specific niches like heat-mapping, privacy-focused analytics, or mobile-only tracking. Competitive strategies among leaders revolve heavily around AI innovation and acquisition. Market leaders are actively acquiring smaller AI startups to enhance their predictive capabilities. Furthermore, there is a growing trend of "platformization," where vendors offer unified customer data platforms (CDP) that combine analytics, marketing automation, and data warehousing into a single subscription, creating high switching costs for customers.

Key Market Developments:

- In July 2025: Microsoft launched Clarity for Shopify, an integrated analytics app that brings session replays, heatmaps, and AI-generated summaries of user behavior into the Shopify dashboard, helping merchants visualize and improve customer journeys more efficiently.

- In June 2025: Google announced a major Google Analytics 4 update that expands its Enhanced Measurement to auto-track interactions like form engagement and file downloads without coding and introduced a new Cost Data Import feature to bring external cost data into GA4 reporting.

- In June, 2025: Adobe introduced advanced AI-driven capabilities in Adobe Analytics designed to automatically surface meaningful data relationships and identify valuable customer segments using machine learning to speed up insights and improve decision-making.

Companies Covered in Mobile Apps and Web Analytics Market

- Microsoft

- Oracle

- SAP

- AWS

- IBM

- Teradata

- Adobe

- SAS Institute

- Micro Focus

Frequently Asked Questions

The global market is projected to reach a value of US$ 62.5 Billion by 2033, growing at a significant CAGR during the forecast period.

Key drivers include the widespread integration of Artificial Intelligence for predictive insights, the global proliferation of smartphones, and the increasing shift of businesses toward mobile-first digital strategies.

The mobile advertising and marketing analytics segment currently holds a leading position as organizations prioritize real-time tracking of ad performance and return on investment.

North America is the leading region, attributed to its mature digital infrastructure, early adoption of advanced analytics technologies, and the concentration of key market players.

A significant opportunity lies in developing specialized, privacy-compliant analytics solutions for non-traditional verticals such as Healthcare and Government, which are rapidly digitizing their services.

Prominent companies in the market include Google, Microsoft, Adobe, Oracle, IBM, SAP, AWS, Teradata, SAS Institute, and Micro Focus.