- Advanced Materials

- Microwave Absorbing Materials Market

Microwave Absorbing Materials Market Size, Share, and Growth Forecast 2025 - 2032

Microwave Absorbing Materials Market By Material Type (Carbon-Based Absorbers, Ferrite-Based Absorbers, Others), Product Type (Radar Absorbing Materials (RAM), Microwave Absorbing Paints and Coatings, Others), Application, and Regional Analysis for 2025 - 2032

Microwave Absorbing Materials Market Size and Trends Analysis

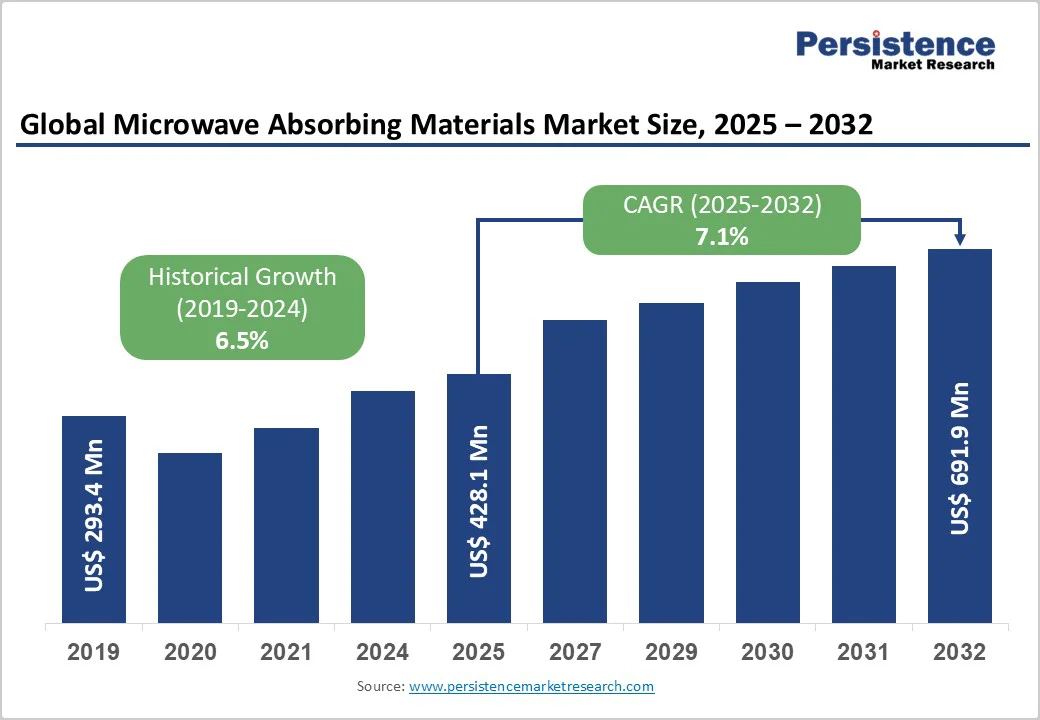

The global microwave absorbing materials market size is likely to be valued at US$428.1 Million in 2025 and is expected to reach US$691.9 Million by 2032, growing at a CAGR of 7.1% during the forecast period from 2025 to 2032, driven by increasing demand for electromagnetic interference (EMI) shielding solutions across the defense, aerospace, and automotive sectors, coupled with the rapid expansion of 5G networks and advanced radar systems requiring sophisticated microwave absorption capabilities.

The growing adoption of Advanced Driver Assistance Systems (ADAS) in automotive applications and the proliferation of electronic devices requiring electromagnetic compatibility across multiple frequency bands will also drive market growth.

Key Industry Highlights

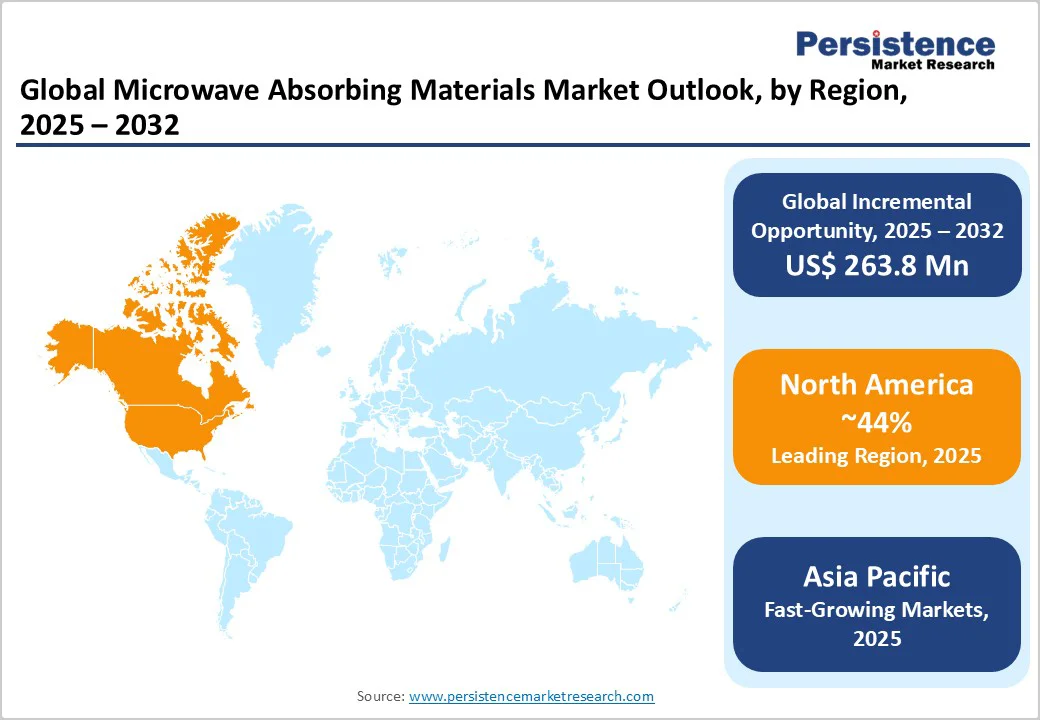

- Leading Region: North America dominates the market with the largest revenue share, driven by substantial defense spending and advanced technology adoption across the aerospace and telecommunications sectors.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing regional market, with China, Japan, and South Korea leading expansion through massive 5G infrastructure investments and electronics manufacturing capabilities.

- Leading Material Type Segment: Carbon-based absorbers maintain a dominant position with 35% market share, offering superior dielectric properties, lightweight characteristics, and versatile application capabilities across multiple industry segments.

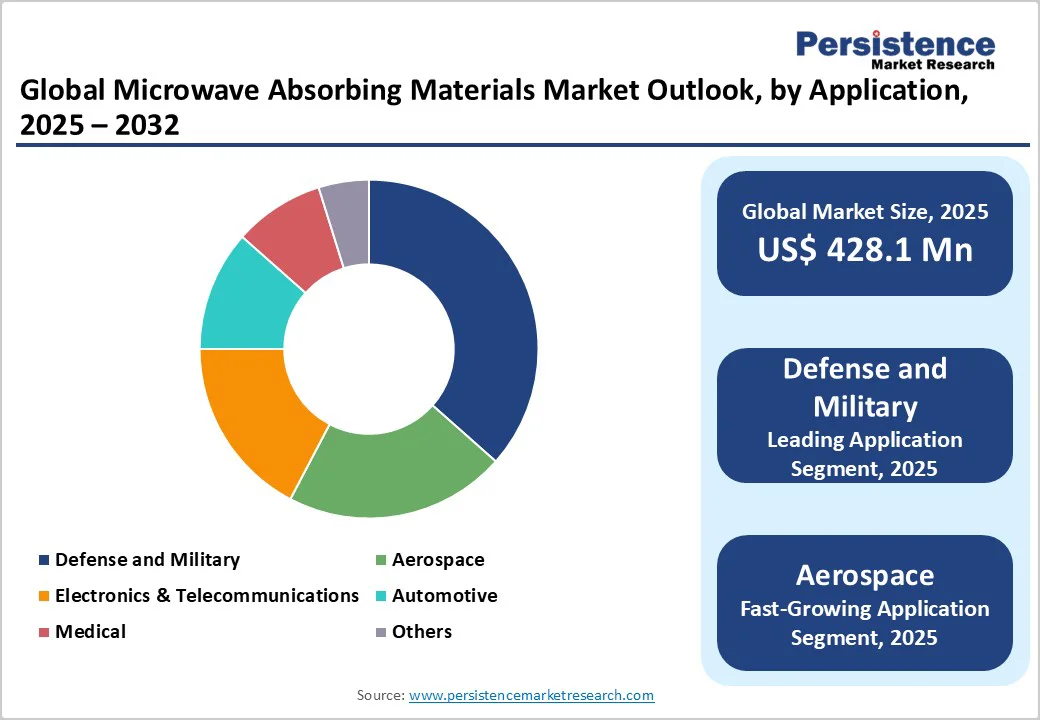

- Leading Application Segment: Defense and Military applications constitute the fastest-growing segment at 38% market share, fueled by global stealth technology investments and electromagnetic warfare capability development programs.

- Key Market Opportunity: Automotive ADAS integration and 5G network deployment represent key market opportunities, driving demand for specialized absorption materials operating at millimeter wave frequencies.

| Key Insights | Details |

|---|---|

| Microwave Absorbing Materials Market Size (2025E) | US$428.1 Mn |

| Market Value Forecast (2032F) | US$691.9 Mn |

| Projected Growth CAGR (2025-2032) | 7.1% |

| Historical Market Growth (2019-2024) | 6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increased Defense Modernization and Stealth Technology Demand

The global defense industry's substantial investments in stealth technology and radar-absorbing materials represent a primary growth catalyst for the microwave absorbing materials market.

Modern military platforms, including fifth-generation fighter aircraft, unmanned aerial vehicles (UAVs), and naval vessels, require advanced microwave absorption capabilities to minimize their radar cross-section (RCS) and enhance survivability. Countries, including the U.S., China, Russia, India, and France, are actively expanding their stealth capabilities due to evolving warfare strategies and regional security challenges.

The development of sophisticated radar detection systems has transitioned from single radar detection to multi-dimensional, multi-band radar networks, necessitating advanced absorbing materials that can operate effectively across broader frequency spectra.

Recent innovations in carbon-based absorbers and ferrite-based materials have demonstrated superior performance, with some achieving reflection loss values exceeding -60 dB while maintaining lightweight characteristics essential for aerospace applications.

5G Infrastructure Expansion and Electromagnetic Compatibility Requirements

The rapid deployment of 5G networks and Internet of Things (IoT) devices has created unprecedented demand for microwave absorbing materials to ensure electromagnetic compatibility and signal integrity. 5G technology operates at significantly higher frequencies, including millimeter wave bands, which intensifies electromagnetic interference challenges and necessitates more sophisticated absorption solutions.

The telecommunications industry expansion, particularly in the Asia Pacific region, including China, Japan, and South Korea, is driving substantial investments in microwave absorbing materials for base stations, antenna systems, and network infrastructure.

Stringent regulatory frameworks such as FCC Part 15 in the U.S., the EMC Directive in Europe, and similar standards globally mandate effective EMI control, compelling manufacturers to integrate advanced microwave absorbing solutions. The miniaturization of electronic devices, coupled with increased integration density, has further amplified the need for materials that can provide effective absorption while maintaining compact form factors.

Barrier Analysis - High Manufacturing Costs and Complex Production Processes

The development and production of high-performance microwave absorbing materials involve significant costs due to specialized raw materials and complex manufacturing techniques. Advanced materials such as carbon nanotubes, graphene-enhanced composites, and nanostructured ferrites require sophisticated processing equipment and controlled manufacturing environments, resulting in elevated production costs.

The precision required in achieving optimal electromagnetic properties, including specific permittivity and permeability values, necessitates extensive quality control measures and specialized testing equipment, further increasing manufacturing complexity. These cost factors particularly impact adoption in price-sensitive consumer electronics applications, where manufacturers seek a balance between performance requirements and cost constraints.

Technical Integration Challenges in Miniaturized Electronics

The ongoing miniaturization trend in electronic devices presents significant technical challenges for integrating effective microwave absorbing solutions. As electronic components become increasingly compact and densely packed, traditional absorption materials often cannot be implemented effectively without compromising device functionality or aesthetics.

The challenge is particularly acute in applications such as smartphones, wearable devices, and automotive sensors, where space constraints and weight limitations restrict the use of conventional absorbing materials. Ensuring complete electromagnetic coverage across all surfaces of compact electronics while maintaining thermal management and mechanical integrity also requires innovative material designs and application techniques.

Opportunity Analysis - Automotive ADAS and Electric Vehicle (EV) Integration

The automotive industry's transformation toward EVs and Advanced Driver Assistance Systems (ADAS) presents substantial growth opportunities for microwave absorbing material manufacturers.

Modern vehicles incorporate multiple radar sensors operating at 77 GHz frequency bands for applications, including adaptive cruise control, collision avoidance, blind spot detection, and lane change assistance. The integration of SABIC's LNP STAT-KON compounds and similar advanced materials demonstrates the industry's commitment to addressing electromagnetic interference challenges in automotive radar systems.

EVs introduce additional EMI challenges due to high-voltage power electronics and electric motor operations, requiring comprehensive shielding solutions to protect sensitive electronic systems.

The automotive shielding market is projected to reach US$29.12 Billion by 2030, indicating substantial opportunities for specialized microwave absorbing materials tailored for automotive applications. The trend toward autonomous driving technologies will further intensify demand for reliable radar systems, necessitating advanced absorption materials to ensure system accuracy and safety.

Medical and Healthcare Electronics Expansion

The healthcare sector's increasing adoption of sophisticated electronic medical devices presents significant opportunities for microwave absorbing materials applications.

MRI machines, defibrillators, portable glucose monitors, and wireless health monitoring devices require robust EMI protection to ensure accurate operation and patient safety. The aging global population and rising prevalence of chronic diseases are driving demand for home healthcare technologies and remote patient monitoring systems, which rely heavily on wireless communication and require effective electromagnetic shielding.

Telehealth expansion, accelerated by global healthcare digitization trends, is creating new opportunities for EMI-shielded connected health products.

Stringent medical device regulations governing electromagnetic emissions create a high-value market segment where advanced microwave absorbing materials can command premium pricing due to exacting performance requirements. The development of flexible copper shielding layers and specialized absorbing materials for wearable medical devices represents an emerging growth area with substantial potential.

Category-wise Analysis

Material Type Insights

Carbon-based absorbers dominate the microwave absorbing materials market with approximately 35% market share, driven by their superior dielectric properties and versatile application capabilities.

Carbon-based materials, including carbon black, carbon nanotubes, graphene, and carbon fibers, offer excellent microwave absorption through enhanced dielectric loss mechanisms while maintaining lightweight characteristics essential for aerospace and automotive applications. These materials demonstrate exceptional chemical stability, mechanical durability, and tailorable electromagnetic properties through structural modifications and composite formulations.

Recent innovations in biomass-derived activated carbon composites have achieved remarkable performance metrics, with some formulations exhibiting reflection loss values exceeding -51 dB and effective absorption bandwidths spanning 4 GHz at minimal thickness.

The versatility of carbon-based absorbers enables their integration into various product forms, including paints, coatings, sheets, and structural composites, making them suitable for diverse applications across multiple industries.

Product Type Insights

Radar Absorbing Materials (RAM) represent the leading product segment, capturing approximately 40% market share due to their critical importance in defense and aerospace applications.

Traditional RAM technologies have evolved from basic ferrite-based coatings to sophisticated multi-layer structures incorporating Jaumann absorbers, Salisbury screens, and advanced metamaterial designs. Modern RAM systems achieve broadband absorption performance across multiple radar frequency bands while maintaining structural integrity and environmental resistance required for military platforms.

The development of nanotechnology-enhanced RAM has revolutionized the industry, enabling multi-band absorption capabilities with superior performance-to-weight ratios compared to conventional materials. Spray-on coatings and conformal absorbing materials have gained significant traction for their application flexibility and ability to conform to complex geometric surfaces of aircraft and naval vessels.

Recent advances in adaptive RAM technologies incorporate real-time adjustments to absorption characteristics, providing dynamic stealth capabilities for military assets operating in varied electromagnetic environments.

Application Insights

Defense and military applications command the largest market share at approximately 38%, reflecting the sector's substantial investments in stealth technology and electromagnetic warfare capabilities. Military applications encompass stealth aircraft, naval vessels, ground vehicles, missiles, and electronic warfare systems, all requiring advanced microwave absorption to minimize detection signatures.

The defense segment's growth is sustained by ongoing modernization programs across major military powers and increasing focus on multi-spectral stealth capabilities that operate across radar, infrared, and visual spectrums.

Aerospace applications represent the second-largest segment, driven by commercial aviation's adoption of advanced radar systems, satellite communications, and avionics requiring electromagnetic compatibility.

The electronics and telecommunications sector demonstrates rapid growth potential, fueled by 5G infrastructure deployment and increasing electromagnetic pollution concerns in urban environments. Automotive applications are emerging as a high-growth segment, with ADAS systems and EV technologies creating new demand for specialized absorption materials operating at millimeter wave frequencies.

Regional Insights

North America Microwave Absorbing Materials Market Trends

North America maintains market leadership in microwave absorbing materials, anchored by substantial defense spending and technological innovation capabilities concentrated in the U.S. The region's dominance stems from major defense contractors, including Lockheed Martin, Boeing, Raytheon, and Northrop Grumman, driving demand for advanced stealth technologies and radar-absorbing materials.

U.S. military standards such as MIL-STD-461 and MIL-STD-464 establish stringent electromagnetic compatibility requirements, creating a robust regulatory framework that supports market growth. The presence of leading materials companies, including 3M Company, Parker Hannifin Corporation, and Rogers Corporation provides strong domestic supply capabilities and continuous innovation in microwave absorption technologies.

The region's 5G infrastructure deployment and IoT adoption are accelerating demand for EMI shielding solutions across telecommunications and automotive sectors. North America is expected to grow at a CAGR of 7.03% during the forecast period, driven by rapid deployment of next-generation communication technologies and increased investments in electrified automotive platforms.

Europe Microwave Absorbing Materials Market Trends

Europe represents a significant market for microwave absorbing materials, driven by stringent electromagnetic compatibility regulations and advanced manufacturing capabilities in Germany, the U.K., France, and Spain.

The European Union's EMC Directive and REACH compliance requirements establish comprehensive regulatory frameworks governing microwave absorbing materials, ensuring high safety and environmental standards. Germany's automotive industry leadership, particularly in EVs and ADAS technologies, creates substantial demand for specialized absorption materials supporting radar sensors and electromagnetic compatibility.

France's aerospace and defense sector, including Airbus operations and military aviation programs, drives demand for advanced radar-absorbing materials and stealth technologies.

The region's emphasis on sustainable materials and environmental regulations is fostering innovation in bio-based microwave absorbers and recyclable electromagnetic shielding solutions. Europe's market benefits from strong research and development capabilities, with numerous universities and research institutions contributing to materials science advancement and electromagnetic compatibility technologies.

Asia Pacific Microwave Absorbing Materials Market Trends

Asia Pacific emerges as the fastest-growing regional market, with China, Japan, India, and South Korea leading manufacturing expansion and technological adoption. China's massive investments in 5G infrastructure, defense modernization, and electronics manufacturing create unprecedented demand for microwave absorbing materials across multiple industry sectors.

The country's Belt and Road Initiative and smart city development programs further amplify requirements for electromagnetic compatibility solutions. Japan's advanced materials research capabilities and electronics industry expertise position the country as a key innovation hub for high-frequency microwave absorbing materials.

South Korea's leadership in semiconductor manufacturing and consumer electronics drives demand for sophisticated EMI shielding solutions supporting miniaturized device designs. India's expanding aerospace and defense sector, coupled with growing telecommunications infrastructure, creates substantial market opportunities for microwave absorbing materials.

The region benefits from cost-effective manufacturing capabilities and strong government support for electronic manufacturing and technology development, making it an attractive destination for global materials companies.

Competitive Landscape

The global microwave absorbing materials market is moderately consolidated, with established players dominating major segments while specialized firms cater to niche applications.

Market competition is driven by diverse strategies such as product portfolio expansion, geographic reach, technological innovation, and targeted R&D investments. Leading companies maintain their positions by offering a wide range of solutions optimized for performance, durability, and cost-efficiency across various industries.

Emerging players focus on high-growth segments through innovation in advanced materials, including graphene composites, metamaterials, and bio-based absorbers. The competitive edge is achieved via superior absorption across multiple frequency bands, lightweight designs, tailored thickness, and environmentally resilient solutions suited for defense, automotive, and telecommunications applications.

Key Industry Developments

- In October 2024, Rogers Corporation reported a strategic expansion of its Advanced Electronics Solutions division, investing US$50-60 Million in capital expenditures to support growth in EV/HEV and renewable energy markets, focusing on scaling production and enhancing advanced material offerings for automotive and electronics applications.

- In March 2024, 3M Company introduced next-generation EMI absorbers incorporating specialized magnetic particles for broadband frequency coverage from <1 MHz to 10 GHz, targeting automotive and telecommunications applications, improving electromagnetic interference mitigation, and enabling more reliable performance across electronic systems.

- In October 2024, a microwave absorbing material developed for ADAS applications achieved 67% RF absorption at the 77 GHz frequency band, demonstrating high-efficiency performance for automotive radar and sensing systems.

Companies Covered in Microwave Absorbing Materials Market

- Laird Technologies

- ESCO Technologies Corporation

- ARC Technologies Inc.

- Cuming Microwave

- MAST Technologies

- KEMET Corporation

- SEKISUI POLYMATECH

- T-Global Technology

- KITAGAWA INDUSTRIES

- Murata Manufacturing

- 3M Company

- Rogers Corporation

- Parker Hannifin Corporation

- Panashield

- Leader Tech Inc.

Frequently Asked Questions

The microwave absorbing materials market is projected to reach US$691.9 Million by 2032, growing from US$428.1 Million in 2025 at a CAGR of 7.1%.

Key demand drivers include 5G network expansion, defense modernization programs, ADAS integration in automotive applications, and increasing electromagnetic compatibility requirements across the electronics industry.

Carbon-based absorbers dominate the market with approximately 35% share, offering superior dielectric properties, lightweight characteristics, and versatile application capabilities.

North America maintains market leadership, driven by substantial defense spending, advanced technology adoption, and the presence of major aerospace and telecommunications companies.

Automotive ADAS integration and the EV adoption present substantial growth opportunities, creating demand for specialized absorption materials operating at 77 GHz frequency bands.

Key market players include 3M Company, Parker Hannifin Corporation, Rogers Corporation, Laird Technologies, KEMET Corporation, and MAST Technologies.