- Sensors & Controls

- Radar Market

Radar Market Size, Share, and Growth Forecast, 2025 - 2032

Radar Market By Product Type (Pulse Radar, Continuous Wave (CW), Frequency-modulated Continuous Wave (FMCW), Others), Range (Short Range, Medium/Mid-Range, Long Range), Application (Aerospace & Defense, Automotive, Others), and Regional Analysis for 2025 - 2032

Radar Market Share and Trends Analysis

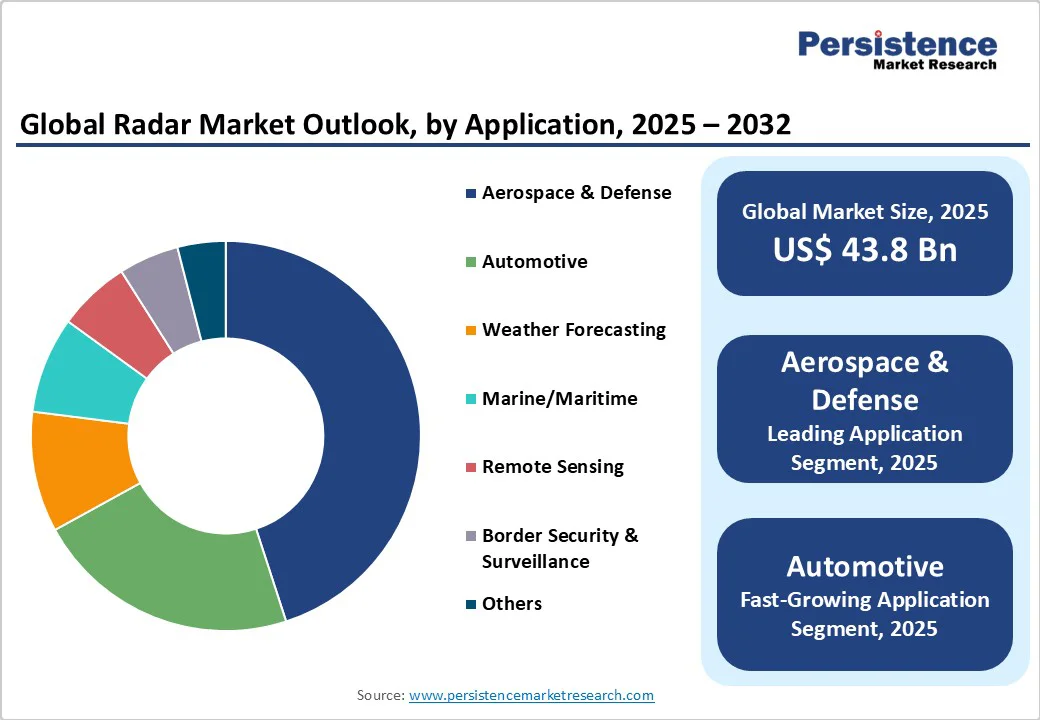

The global radar market size is likely to be valued at US$43.8 billion in 2025. It is estimated to reach US$66.1 billion by 2032, growing at a CAGR of 6.1% during the forecast period 2025 - 2032, driven by the expanding utilization of radars in defense modernization, automotive advanced driver-assistance systems (ADAS), and the increasing adoption of digital radar technologies across industries.

Market growth is driven by rising defense spending, the adoption of autonomous vehicles, and increasing demand for weather and remote sensing systems. Advancements in AI and software-defined radar technologies are further enhancing range, accuracy, and multi-industry applications.

Key Industry Highlights

- Largest & Fastest-growing Applications: Aerospace & defense applications are likely to constitute nearly 45.0% of the radar market share in 2025, while the automotive sector will be the fastest-growing application, driven by demand for autonomous vehicles.

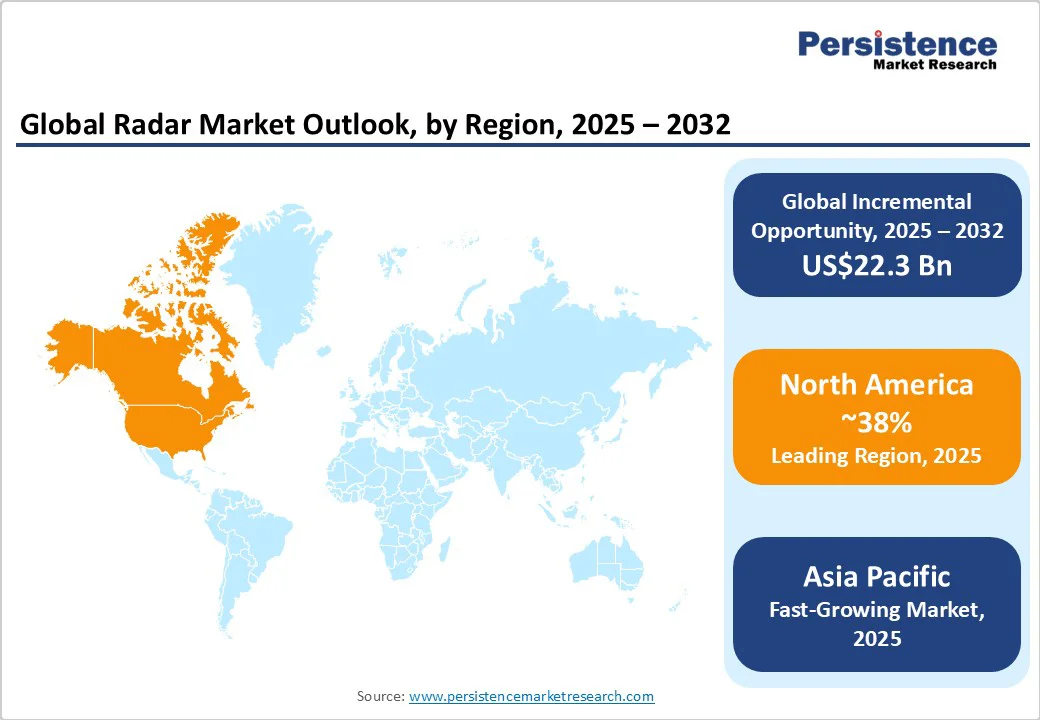

- Dominant Region: North America is slated to lead with a 38.0% share in 2025, sustained by robust U.S. defense investments and innovation in cutting-edge technologies.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing regional market, propelled by the expanding urban mobility projects in India and China.

- Dominant Product Type: Pulse radars are expected to dominate with a 38% share in 2025, due to their reliability in harsh conditions and the precision of their long-range measurements, which are crucial for border surveillance and maritime monitoring.

- September 2025: Krohne launched FMCW radar level transmitters for precise, reliable measurement of liquids and solids, performing effectively in challenging industrial conditions, including dust, vapors, and temperature or pressure fluctuations.

| Key Insights | Details |

|---|---|

| Radar Market Size (2025E) | US$43.8 Bn |

| Market Value Forecast (2032F) | US$66.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Blending of AI and SDR in Radar Systems to Boost Market Growth

The radar market is experiencing growth momentum due to the integration of artificial intelligence (AI) and software-defined radar (SDR) technologies, which enhance system adaptability, signal processing, and target detection accuracy.

According to the U.S. Department of Defense, investments in AI-enabled sensor fusion systems are expected to increase by over 20% annually through 2030, providing cutting-edge capabilities in threat detection and autonomous vehicle navigation.

Industry reports from the Association for Unmanned Vehicle Systems International (AUVSI) highlight that software-defined radar enables dynamic waveform changes and real-time environment adaptation, leading to improved performance under adverse conditions. This technological advancement is expanding radar applications beyond traditional defense to sectors such as automotive safety and environmental monitoring, thereby driving market growth.

AI also facilitates predictive maintenance and anomaly detection in radar hardware, reducing operational costs and enhancing reliability. Stakeholders focusing on AI-integrated radar systems are thus positioned to capitalize on accelerated adoption and robust demand growth worldwide.

Increasing Supply Chain Uncertainties in Semiconductor Components

The radar industry faces significant structural challenges due to vulnerabilities in the global semiconductor supply chain, critically affecting component availability and manufacturing timelines. Data from the Semiconductor Industry Association indicates that lead times for specialized radar chips have surged over 40% since 2023, driven by geopolitical tensions and limited fabrication capacity.

This shortage particularly affects high-frequency front-end modules, which are essential for radar performance, resulting in production delays and increased costs. Automotive and defense sectors are most affected, where timely upgrades are crucial, and analysts such as Deloitte estimate potential revenue losses of up to 8% annually for radar OEMs during 2025 - 2026.

To mitigate these risks, companies are exploring strategies such as diversifying supplier networks and investing in in-house semiconductor design capabilities, though these require substantial capital. Stakeholders must carefully manage inventory while sustaining innovation to navigate supply bottlenecks. Effective planning and strategic investment are critical to maintaining market momentum and ensuring uninterrupted deployment of radar systems throughout 2025-2032.

Transformation of Urban Mobility to Open Lucrative Opportunities

The emergence of smart city initiatives and cutting-edge urban mobility solutions offers attractive opportunities for the expansion of radar technologies, particularly in intelligent traffic management and autonomous public transit systems. According to the International Transport Forum (ITF), global investments are likely to exceed US$20 billion by 2028 in smart infrastructure, including radar-based vehicle-to-infrastructure (V2I) systems, which foster real-time traffic optimization and accident prevention.

Radar sensors integrated with AI enable precise object detection for dynamic traffic signal control and pedestrian safety monitoring, addressing unmet needs in urban mobility safety. This opportunity is amplified in the rapidly urbanizing economies of the Asia Pacific and Latin America, where rising population densities necessitate advanced transportation solutions.

Pilot projects in cities such as Singapore and Amsterdam demonstrate the pivotal role played by radars in reducing congestion and emissions, enhancing urban quality of life. For investors and product developers, focusing on modular radar units tailored for smart infrastructure deployment represents actionable growth potential with scalable revenue streams driven by public-private partnerships (PPPs) and government funding.

Category-wise Analysis

Product Type Insights

Pulse radar is expected to maintain its dominant position with an estimated 2025 market share of 38%, reflecting its established effectiveness in long-range military applications and air defense systems where robust target detection capabilities are paramount.

Pulse radars’ leading position stems from their proven reliability in harsh environmental conditions and their ability to provide accurate range measurements across vast distances, making them indispensable for border surveillance and maritime monitoring. Major defense contractors continue investing in pulse radar upgrades, incorporating digital signal processing and enhanced electronic counter-countermeasure capabilities to maintain operational superiority.

Frequency-modulated continuous wave (FMCW) radar is set to emerge as the fastest-growing segment from 2025 to 2032, driven by superior resolution and energy efficiency, aligning with automotive and industrial automation requirements.

The segment's acceleration is propelled by automotive manufacturers' increasing adoption of FMCW systems for adaptive cruise control, collision avoidance, and autonomous driving functions, where precise object detection and velocity measurement are critical. Synthetic aperture radar (SAR) technology is also demonstrating exceptional growth potential, thanks to its unique capability to provide high-resolution imaging regardless of weather conditions or time of day.

Range Insights

Short-range radar is poised to command the largest market share at approximately 42% in 2025, due to its essential role in automotive safety systems, industrial automation, and perimeter security applications.

The dominance of this segment is powered by the widespread deployment of short-range radars in ADAS features such as blind spot detection, parking assistance, and collision avoidance systems, where proximity sensing within 250 meters is sufficient and cost-effective. Manufacturing advancements have enabled miniaturization and cost reduction, making short-range radar accessible for mass-market vehicle integration and smart infrastructure projects.

Long-range radar is expected to be the fastest-growing segment from 2025 to 2032, driven by increasing geopolitical tensions and defense modernization programs that require extended surveillance capabilities.

The segment benefits from rising demand for early warning systems, missile defense applications, and border security solutions where detection ranges exceeding 300 kilometers are essential for strategic defense operations. Investment in next-generation long-range radar systems, which incorporate AI-enhanced target classification and multi-mission capabilities, is driving premium pricing and revenue growth for specialized defense contractors.

Application Insights

Defense & aerospace applications will retain leadership with an estimated 45% radar market revenue share in 2025, supported by sustained global military expenditure exceeding US$2.4 trillion in 2023 and ongoing modernization initiatives across developed and emerging nations.

The continued dominance of this segment reflects critical radar requirements for air defense, missile guidance, battlefield surveillance, and reconnaissance missions, where performance reliability and technological superiority directly impact national security outcomes. Government procurement cycles and multi-year defense contracts provide stable revenue streams for established radar manufacturers.

Automotive applications are expected to exhibit the highest growth trajectory through 2032, driven by the accelerated adoption of ADAS, the advancement of autonomous vehicles, and the implementation of regulatory mandates for enhanced vehicle safety features.

The segment's rapid expansion is supported by declining radar component costs through semiconductor scaling, enabling integration across vehicle segments beyond premium models. Market penetration is further accelerated by regulatory requirements such as Europe's GSR II mandate, China's NCAP upgrades, and NHTSA safety standards in the U.S., creating a mandatory demand for radar-based emergency braking and collision avoidance systems.

Regional Insights

North America Radar Market Trends

North America is anticipated to capture a commanding 38% market share in 2025, owing to the massive defense spending by the U.S. of over US$800 billion annually and its leadership in radar technology innovation.

The regional market is projected to grow at a high CAGR through 2032, supported by robust government funding for military radar modernization, including next-generation air defense systems and space-based surveillance platforms. The U.S. Department of Defense's investment in AI-enabled sensor fusion systems will create significant opportunities for domestic radar manufacturers.

Supporting these factors is the regulatory environment in North America, which facilitates rapid technology validation and deployment through streamlined defense procurement processes and strong industry-government partnerships that foster innovation.

The regional competitive landscape features established defense contractors such as Raytheon Technologies, Lockheed Martin, and Northrop Grumman, alongside emerging startups specializing in automotive and commercial radar applications. Investment trends emphasize the integration of AI, software-defined radar architectures, and semiconductor supply chain resilience, positioning the region for sustained technological leadership and market expansion.

Asia Pacific Radar Market Trends

The Asia Pacific is well-positioned to emerge as the fastest-growing regional market, with the highest CAGR through 2032, driven by the rapidly expanding defense budgets, urbanization initiatives, and manufacturing capabilities of China, Japan, India, and the ASEAN nations.

Rising defense expenditure, aggressive smart city development projects, and extensive growth in the automotive industry support the region. China leads regional growth with defense spending increases and substantial investments in radar technology for border security and maritime surveillance. At the same time, India focuses on indigenous radar development to reduce import dependency.

Key growth factors include defense modernization programs addressing regional security challenges, the expansion of the automotive industry with increasing adoption of ADAS, and the development of smart infrastructure, which requires traffic management and environmental monitoring radar systems.

The regulatory environment shows continuous improvement through simplified technology transfer procedures, local manufacturing incentives, and government support for indigenous radar development programs.

The competitive landscape encompasses both global players establishing regional manufacturing and R&D facilities and domestic companies innovating in cost-effective radar solutions tailored for local market requirements. Investment trends highlight digital radar production capabilities, application-specific sensor development, and supply chain localization efforts.

Europe Radar Market Trends

Europe is set to account for consistent growth in 2025, with Germany, the U.K., France, and Spain serving as primary contributors through their aerospace, defense, and automotive sectors.

The regional market is forecast to expand, influenced by the actions of NATO and the defense industrial policies of the European Union (EU), promoting technological sovereignty and coordinated research funding through programs such as the European Defense Industrial Development Program (EDIDP).

Regulatory harmonization efforts facilitate cross-border collaboration and technology transfer, particularly benefiting the development of radar for aerospace and automotive applications.

Primary growth drivers include increasing defense expenditure in response to geopolitical tensions, the automotive industry's transformation toward electric and autonomous vehicles, which require advanced radar sensors, and climate monitoring initiatives necessitating upgraded weather radar systems.

The region's competitive environment balances multinational corporations such as Thales, BAE Systems, and Leonardo with innovative small and medium enterprises developing specialized radar solutions for niche applications. Investment flows emphasize sustainability considerations, dual-use technology development, and supply chain localization to reduce dependency on non-European suppliers.

Competitive Landscape

The global radar market structure is moderately consolidated, with the top five companies controlling approximately 55% of the market share as of 2025. Leading players include large defense contractors and specialized electronics manufacturers, maintaining dominance through extensive R&D, broad product portfolios, and global distribution networks.

The market also features numerous emerging firms focusing on niche segments such as automotive radar and software-defined radar modules, contributing to competitive innovation. Product differentiation and strategic partnerships are key competitive drivers, enabling leaders to sustain technology leadership and cost efficiencies in an evolving market environment.

Key Industry Developments

- In October 2025, Germany chose Raytheon’s SPY-6 radar for new frigates, enhancing air and missile threat detection, situational awareness, and naval defense capabilities, reflecting its modernization efforts and the strategic role of advanced radar technology in maritime security.

- In September 2025, NASA-ISRO’s NISAR satellite captured its first radar images, using dual L- and S-band systems to monitor forests, wetlands, and agricultural areas, enhancing disaster response, ecosystem tracking, and land movement analysis with unprecedented detail.

- In August 2025, Bosch launched two radar SoCs enhancing ADAS with improved object detection, higher sensor integration, lower power use, and reduced system costs, reinforcing its automotive radar leadership and supporting global safety regulations.

Companies Covered in Radar Market

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Thales Group

- BAE Systems plc

- Leonardo S.p.A.

- Hensoldt AG

- Saab AB

- L3Harris Technologies, Inc.

- Elbit Systems Ltd.

- Nokia Corporation

- Rohde & Schwarz GmbH & Co KG

- Furuno Electric Co., Ltd.

- Hanwha Systems Co., Ltd.

- Kongsberg Gruppen ASA

Frequently Asked Questions

The radar market is projected to reach US$43.8 Billion in 2025.

Increased government defense budgets and industry investments in innovative radar systems that enhance range and accuracy are driving the market.

The market is poised to witness a CAGR of 6.1% from 2025 to 2032.

Expanding utilization of radars in defense modernization, automotive advanced driver-assistance systems (ADAS), and the convergence of radar systems with AI and software-defined technologies are key market opportunities.

Raytheon Technologies Corporation, Northrop Grumman Corporation, and Lockheed Martin Corporation are some of the key players in the radar market.