- Telecommunications

- Point-to-Point Microwave Antenna Market

Point-to-Point Microwave Antenna Market Size, Share, and Growth Forecast, 2025 - 2032

Point-to-Point Microwave Antenna Market by Antenna Type (Parabolic Antennas, Ho Antennas, Patch Antennas, Reflector Antennas, Slot Antennas), Frequency (Sub-GHz (300 MHz - 1 GHz), GHz Range (1 GHz - 10 GHz), Super-GHz (10 GHz - 60 GHz), Extremely High Frequency (EHF - above 60 GHz)), Application, and Regional Analysis for 2025 - 2032

Point-to-Point Microwave Antenna Market Size and Trends Analysis

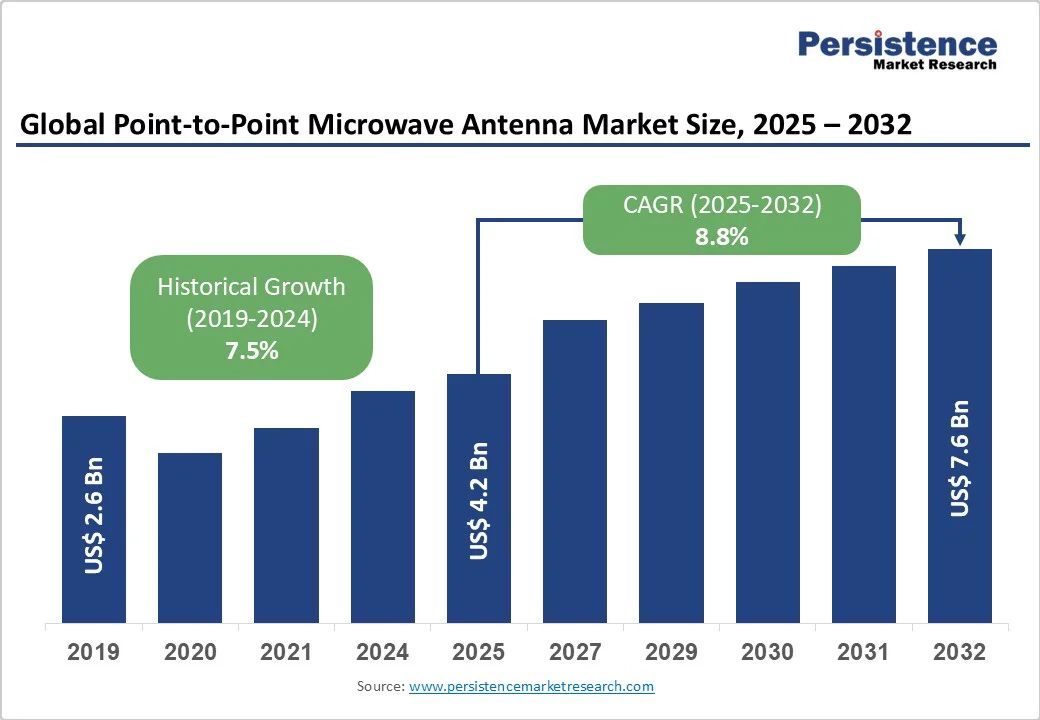

The global point-to-point microwave antenna market size is likely to be valued at US$4.2 Bn in 2025 and expected to reach US$7.6 Bn by 2032, registering a robust CAGR of 8.8% during the forecast period from 2025 to 2032, fueled by the increasing demand for high-speed wireless communication solutions, advancements in antenna technologies, and a global push toward enhancing network infrastructure and connectivity.

Key Industry Highlights:

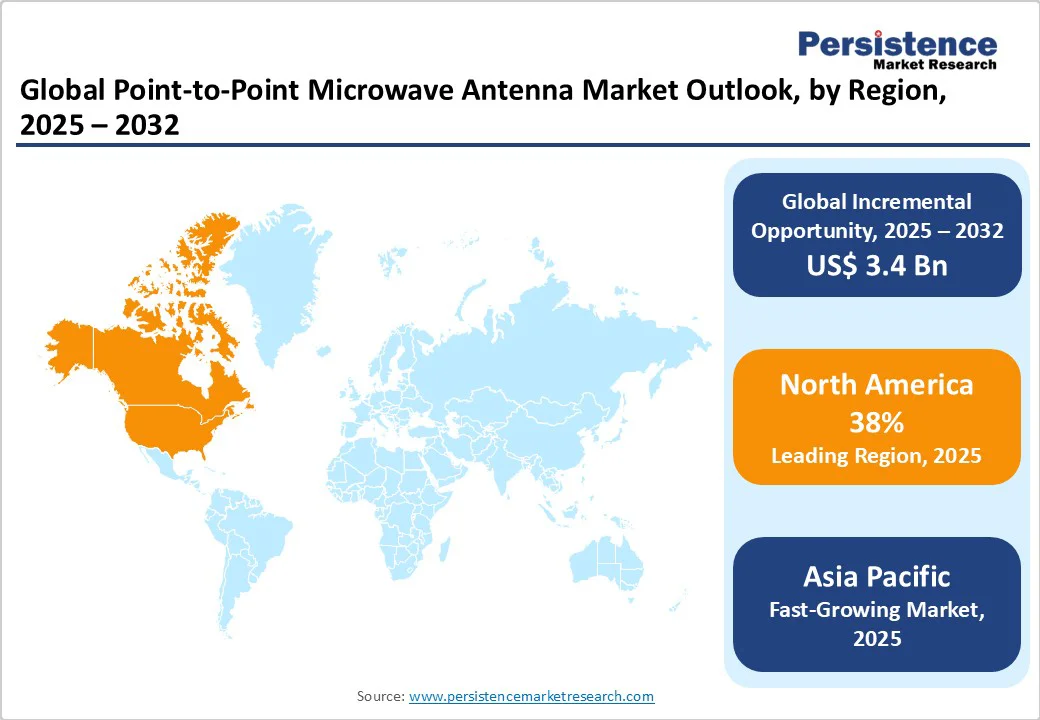

- Leading Region: North America is likely to account for a 38% share in 2025, driven by advanced telecommunications infrastructure, widespread adoption of innovative antennas, and significant investments in network research.

- Fastest-growing Region: Asia Pacific, propelled by increasing prevalence of digital transformation, urbanization, and expanding telecom access in countries such as China and India.

- Dominant Antenna Type: Parabolic Antennas account for approximately 38% of the point-to-point microwave antenna market share in 2025, owing to their critical role in long-range transmission and advancements in high-gain designs.

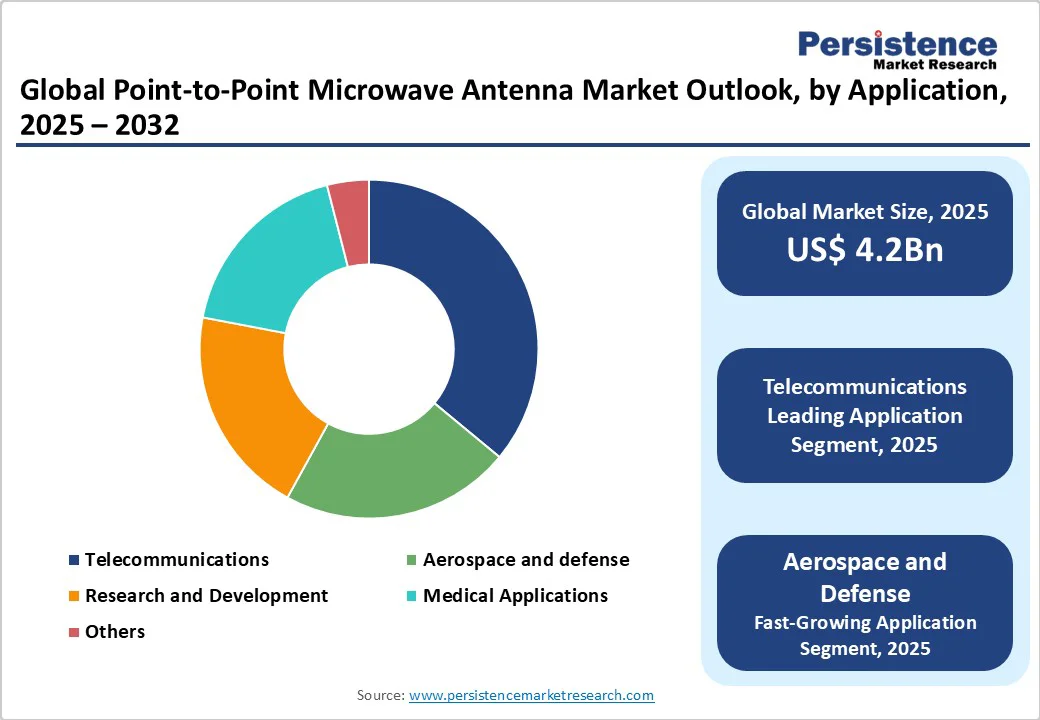

- Leading Application: Telecommunications with a 36% share, reflecting its critical role in backhaul and network expansion procedures.

| Key Insights | Details |

|---|---|

| Point-to-Point Microwave Antenna Market Size (2025E) | US$4.2 Bn |

| Market Value Forecast (2032F) | US$7.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.5% |

Market Dynamics

Driver - Rising Demand for High-Speed Wireless Connectivity Amid Increasing 5G Deployment

The global surge in demand for high-speed wireless connectivity is a primary driver of the point-to-point microwave antenna market. According to the GSMA, 5G connections are projected to reach 2.4 Bn worldwide by the end of 2025, with the technology enabling ultra-reliable low-latency communications essential for IoT ecosystems and smart city initiatives.

This alarming prevalence is exacerbated by an increasing data consumption rate, with global mobile data traffic expected to grow rapidly in the coming years, and rising lifestyle-related digital dependencies, as wireless networks become a leading global connectivity burden.

In response, governments and telecom operators are investing heavily in backhaul infrastructure, with the United States leading in the adoption of microwave antennas for 5G densification to support end-stage urban coverage gaps. In Europe, where 5G rollout cases are steadily increasing, initiatives such as the EU's Digital Decade program highlight the growing focus on spectrum-efficient wireless treatments.

Furthermore, the telecommunications sector, which accounts for a substantial portion of global connectivity expenditure, is increasingly relying on point-to-point microwave antennas to mitigate the impacts of bandwidth constraints in fiber-scarce regions. The burden of data-intensive applications is projected to increase significantly in terms of prevalence, latency requirements, and quality-of-service metrics over the coming decades.

Restraint - High Costs of Production and Stringent Regulatory Compliance

High production costs remain a significant restraint on the expansion of the point-to-point microwave antenna market. Sourcing high-quality materials, particularly for advanced variants such as parabolic designs, requires complex manufacturing and precision engineering techniques, which drive up expenses and challenge the competitiveness of smaller players.

Compliance with stringent regulatory standards from bodies such as the FCC in the U.S. and ETSI in Europe further adds financial and operational burdens, as approval processes for new frequencies often involve long timelines and substantial costs.

Supply chain disruptions and fluctuating component prices have also increased production expenses, especially for high-frequency models. This not only pushes up retail prices but also limits accessibility in emerging markets, where affordability remains a key barrier to adoption. The need for skilled personnel in design and installation adds another layer of complexity, with talent shortages in regions such as Southeast Asia leading to project delays and higher costs.

Potential interference challenges, such as spectrum congestion in dense urban areas, further contribute to operator hesitancy. Collectively, these factors could temper growth rates, particularly in price-sensitive regions, unless mitigated by economies of scale or public infrastructure subsidies.

Opportunity - Innovation in Formulations and E-commerce Expansion

The point-to-point microwave antenna market offers significant opportunities through innovative antenna designs and the rapid growth of digital infrastructure platforms. Operators’ rising demand for multifunctional antennas is driving companies to develop hybrid models that integrate features such as beamforming with advanced materials to enhance signal strength, addressing niche applications such as smart city networks and secure defense communications.

Advancements in millimeter-wave technologies have further improved capacity, making these solutions highly attractive to telecom providers struggling to meet escalating data demands fueled by 5G expansion.

Increasing R&D investments are also creating new possibilities, with studies confirming the role of high-frequency antennas in reducing latency for IoT applications and broadcasting. These developments are opening doors to cross-sector integrations, unlocking additional revenue streams for manufacturers and suppliers.

The rapid rise of digital procurement platforms is facilitating market penetration by enabling direct-to-operator models that reduce costs and improve accessibility, particularly in the Asia Pacific, where online infrastructure adoption is accelerating. Industry marketplaces are expanding their reach to underserved rural operators, while public-private partnerships, such as national digitalization initiatives and network subsidies, are further promoting adoption.

Category-wise Analysis

Antenna Type Insights

The point-to-point microwave antenna market is segmented into parabolic antennas, horn antennas, patch antennas, reflector antennas, and slot antennas. Parabolic Antennas dominate, holding approximately 38% of the market share in 2025, due to their proven efficacy in long-distance transmission, high gain, and integration into standard network protocols. Parabolic Antennas are widely used in telecom backhaul, offering focused beam capabilities that reduce interference.

Ho Antennas are the fastest-growing segment, driven by increasing demand for compact solutions in urban environments. Ho Antennas offer versatile deployment options, with advancements in miniaturization and durability making them suitable for long-term use in densely populated areas.

Frequency Insights

The point-to-point microwave antenna market is segmented into sub-GHz (300 MHz - 1 GHz), GHz range (1 GHz - 10 GHz), super-GHz (10 GHz - 60 GHz), and extremely high frequency (EHF) ranges (above 60 GHz). Super-GHz (10 GHz - 60 GHz) dominates, holding approximately 38% of market share in 2025, due to their balance of range and capacity, precise signal delivery, and integration into standard telecom regimens. Super-GHz frequencies are widely used in mid-range links, offering reliability that reduces downtime.

Extremely high frequency (EHF) is the fastest-growing segment, driven by increasing demand for high-bandwidth applications in 5G. EHF offers ultra-high capacity as an advanced therapy, with advancements in mmWave technology and spectrum allocation making it suitable for long-term use in high-data populations.

Application Insights

The point-to-point microwave antenna market is segmented into telecommunications, aerospace and defense, broadcasting, research and development, and medical applications. Telecommunications dominate, holding approximately 36% of market share in 2025, due to their proven efficacy in backhaul networks, capacity support, and integration into mobile protocols. Telecommunications are widely used in operator networks, offering bandwidth boosts that reduce congestion.

Aerospace and defense are the fastest-growing segments, driven by increasing demand for secure communication in military operations. These applications provide reliable links as adjunct systems, with advancements in rugged designs and encryption making them suitable for long-term use in strategic populations.

Regional Insights

North America Point-to-Point Microwave Antenna Market Trends

North America dominates the global point-to-point microwave antenna market, expected to account for 38% of market share in 2025, driven by a robust telecommunications ecosystem, high infrastructure investments, and a cultural emphasis on digital connectivity and innovation.

The U.S. leads this regional dominance, with its market projected to grow significantly due to the prevalence of 5G rollouts and a rapidly expanding wireless sector. Trends here include a surge in demand for mmWave antennas amid skepticism toward fiber alternatives, supported by advanced supply chains and technology-driven marketing on platforms such as industry forums.

Key drivers include rising telecom spending and endorsements from regulatory bodies, such as the FCC, which highlight the spectrum efficiency of antennas. Deployment levels continue to grow steadily year over year.

Additionally, the expanding urban population fuels adoption for IoT and broadcasting support, while Canada’s multilingual network campaigns and local manufacturing initiatives strengthen cross-border growth. Overall, North America’s mature regulatory environment ensures deployment safety and positions it as a hub for innovation.

However, challenges such as high production costs persist, even as the region continues to capture a significant share of global R&D investments in wireless technology.

Europe Point-to-Point Microwave Antenna Market Trends

Europe is a key region in the point-to-point microwave antenna market, supported by stringent quality standards and a strong preference for efficient network products. Germany, France, and the U.K. lead growth, with the EU’s digital policies and supportive initiatives driving adoption. In Germany, rising data demands are driving the need for high-frequency formulations, which is supported by substantial R&D investments.

France benefits from smart city initiatives, tourism projects, and sustainable development trends that create demand for advanced wireless solutions. Meanwhile, the U.K.’s post-Brexit focus on domestic production enhances supply chain resilience and supports the local sourcing of antenna variants.

Common trends across these countries include the growing integration of antennas into broadcasting and communication networks, with enhanced links gaining wide adoption. ETSI approvals further ease market entry across the region. While price sensitivity in Southern Europe and Brexit-related tariffs pose challenges, scalable and multi-application designs aligned with Europe’s Green Deal promise sustainable long-term growth.

Asia Pacific Point-to-Point Microwave Antenna Market Trends

Asia Pacific is the fastest-growing region in the point-to-point microwave antenna market, driven by rapid urbanization, a large population base, and rising digital connectivity needs. China and India lead the area, with China’s strong telecom industry and government initiatives such as the Digital China plan accelerating the adoption of advanced antennas.

The growing use of technology applications, expanding connections, and hybrid network designs further strengthen demand. In India, the wireless market benefits from a booming mobile user base and expanding urban populations; however, affordability challenges persist in rural areas, limiting accessibility.

Emerging trends in the region include rapid growth of online supply channels and innovations in affordable antenna models that cater to applications such as broadcasting and IoT. Japan’s network subsidies and South Korea’s emphasis on technology applications in sectors such as healthcare are also fueling adoption. Despite regulatory hurdles and interference concerns in informal markets, the Asia Pacific region remains a high-potential arena for long-term growth.

Competitive Landscape

The global point-to-point microwave antenna market is highly competitive, with international and regional players striving to strengthen their presence through innovation, competitive pricing, and reliable performance. The growing adoption of mmWave-integrated designs and advanced technologies has intensified rivalry, pushing companies to cater to varied network demands. Strategic partnerships, mergers, acquisitions, and adherence to stringent quality certifications are emerging as critical differentiators shaping market leadership.

Key Developments

- July 2024: Nokia showcased a breakthrough in backhaul technology by demonstrating full-duplex fixed point-to-point wireless links in the D-Band spectrum (130-175 GHz). The innovation enables equal high throughput in both directions over a single channel, significantly enhancing network efficiency and next-generation 5G backhaul capacity.

- September 2025: Novocomms (UK) launched a cutting-edge 5G mmWave Fixed Wireless Access (FWA) solution designed to deliver fibre-like data speeds. Targeting regions where fibre deployment is costly or impractical, the innovation enhances connectivity, bridging gaps in broadband access and supporting next-generation digital infrastructure.

Companies Covered in Point-to-Point Microwave Antenna Market

- CommScope Holding Company, Inc.

- Infinite Electronics International, Inc.

- Radio Frequency Systems

- mWAVE Industries, LLC

- Rosenberger

- TESSCO Incorporated

- Wireless Excellence Limited

- LEAX Arkivator Telecom AB

- Astrec Baltic Ltd.

- Kavveri Telecoms

Frequently Asked Questions

The point-to-point microwave antenna market is projected to reach US$4.2 Bn in 2025.

Rising demand for high-speed connectivity, technological advancements in designs, and government initiatives for networks are key drivers.

The industry is poised to witness a CAGR of 8.8% from 2025 to 2032.

Innovations in mmWave sourcing and multi-application designs, such as targeted links, present significant growth opportunities.

CommScope Holding Company, Inc., Infinite Electronics International, Inc., Radio Frequency Systems, mWAVE Industries, LLC, Rosenberger, TESSCO Incorporated, Wireless Excellence Limited, LEAX Arkivator Telecom AB, Astrec Baltic Ltd., and Kavveri Telecoms are among the leading players, known for their innovative antenna solutions.