- Semiconductor Materials & Components

- Global Metallized Polypropylene Dielectric Film Capacitors Market

Global Metallized Polypropylene Dielectric Film Capacitors Market Size, Share, and Growth Forecast 2026 – 2033

Metallized Polypropylene Dielectric Film Capacitors Market by Product Type (Standard Metallized Polypropylene Film Capacitors, Self-Healing Metallized Film Capacitors, High-Voltage Metallized Film Capacitors, and Pulse Metallized Film Capacitors), Capacitance Range (Below 1 µF, 1 µF – 10 µF, 10 µF – 100 µF, and Above 100 µF), Voltage Rating (Below 100 V, 100 V – 500 V and Others), and Regional Analysis

Metallized Polypropylene Dielectric Film Capacitors Market Size and Share Analysis

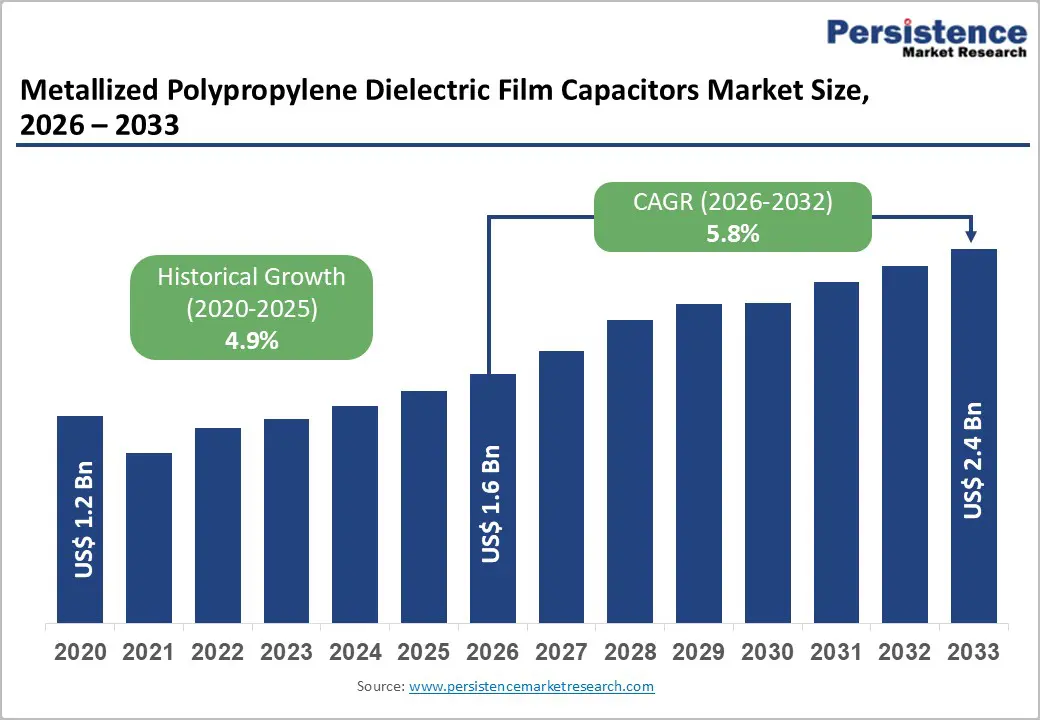

The global Metallized Polypropylene Dielectric Film Capacitors Market size was valued at US$ 1.6 Bn in 2026 and is projected to reach US$ 2.4 Bn by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

Market expansion is driven by accelerating electric vehicle electrification with 28% growth in EV penetration creating exponential demand for battery management capacitors and power conversion equipment, with polypropylene film capacitors accounting for 62% of metallized film capacitor market share due to superior self-healing properties and 22% lower dielectric loss versus polyester alternatives. Renewable energy sector expansion including solar inverter installations rising 24% annually and wind turbine power conversion systems establishes critical infrastructure growth driver requiring high-reliability energy storage and conditioning components.

Key Market Highlights

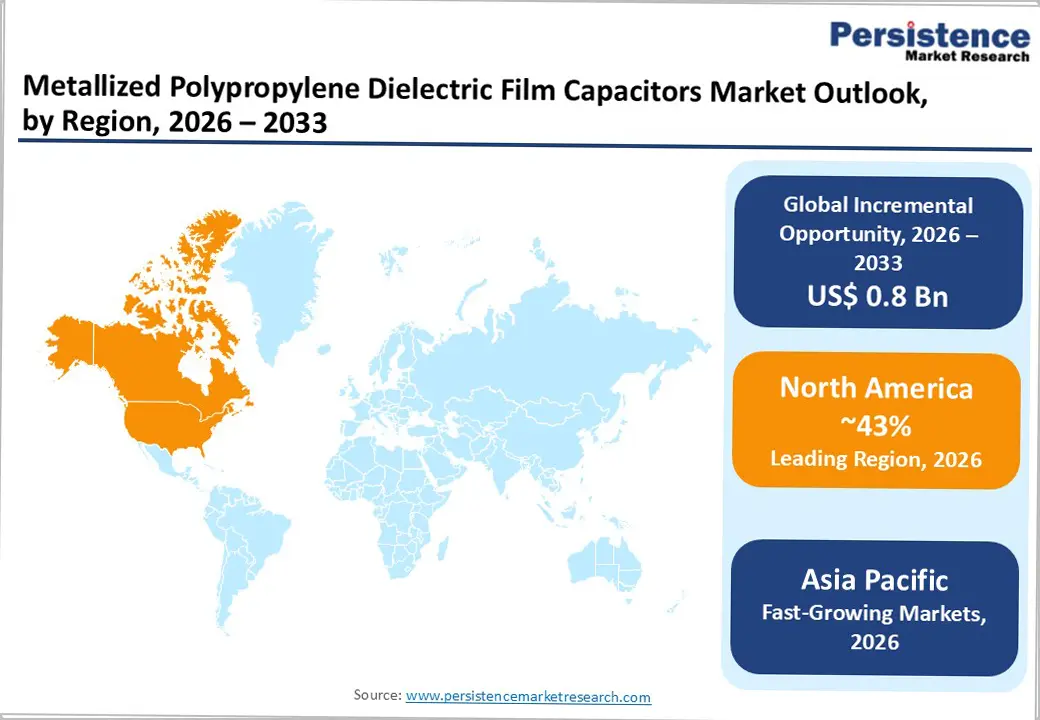

- Leading Region: North America maintains market leadership anchored by United States with 43.4% global demand share, electric vehicle adoption acceleration, 62% of DC fast chargers utilizing polypropylene film capacitors, renewable energy expansion, and data center power management requirements driving sustained market growth.

- Fastest Growing Region: Asia-Pacific commands fastest expansion driven by China's consumer electronics dominance, explosive EV manufacturing growth, India's Make-in-India government initiatives, Japan's quality-focused specialization in automotive applications, and ASEAN emerging manufacturing hubs supporting robust market expansion.

- Dominant Product Type: Self-healing metallized film capacitors command market dominance with 65% market share, driven by inherent failure prevention through Joule heating mechanism, defect isolation in <10 microseconds, predictable capacitance degradation, and superior reliability eliminating catastrophic failure risk.

- Key Market Opportunity: Electric vehicle electrification with 28% EV penetration growth, renewable energy expansion with 24% inverter installation growth, ultra-thin film technology advancement enabling 18% efficiency gains, and industrial automation efficiency optimization creating multi-billion-dollar market expansion opportunity through advanced capacitor integration.

| Key Insights | Details |

|---|---|

| Global Metallized Polypropylene Dielectric Film Capacitors Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.4 Bn |

| Projected Growth CAGR(2026-2033) | 5.8% |

| Historical Market Growth (2020-2025) | 4.9% |

Market Dynamics

Market Growth Drivers

Renewable Energy Infrastructure Expansion and Grid Modernization Driving Market Growth

Renewable energy sector expansion with solar inverter installations rising 24% annually and wind turbine power conversion systems proliferating across developed and emerging markets establishes exceptional growth opportunity for polypropylene film capacitors. Power factor correction applications across solar farms, wind installations, and grid interconnection points requiring robust, reliable filtering and energy conditioning systems drive substantial equipment demand. Energy efficiency regulations particularly in Europe and North America promoting low-loss power conversion and minimal transmission losses create compelling economic justification for advanced capacitor integration.

Distributed energy resource systems including microgrid installations and hybrid renewable systems necessitate sophisticated voltage regulation and harmonic filtering implemented through advanced film capacitor solutions. Government stimulus programs and renewable energy incentives supporting infrastructure modernization across multiple continents establish multi-year procurement commitments, ensuring sustained market expansion through forecast period.

Industrial Automation, Robotics, and Smart Manufacturing Accelerating High-Frequency Capacitor Demand

Rapid adoption of Industry 4.0, factory automation, and advanced robotics is creating a strong secondary growth driver for the metallized polypropylene film capacitors market. Modern variable frequency drives (VFDs), servo drives, programmable logic controllers, and industrial power supplies increasingly operate at higher switching frequencies and tighter efficiency tolerances, driving demand for capacitors with low equivalent series resistance, high ripple current endurance, and superior thermal stability. Metallized polypropylene film capacitors are being widely specified in DC-link circuits, snubber networks, and EMI suppression applications to ensure system reliability under continuous-duty industrial environments.

The growing use of wide-bandgap semiconductors in industrial drives further amplifies this demand, as higher switching speeds require capacitors with minimal dielectric losses and stable capacitance over temperature. Leading suppliers such as Murata Manufacturing Company, TDK Corporation, and Vishay Intertechnology are expanding ruggedized polypropylene capacitor lines designed for long operational lifetimes exceeding 100,000 hours. As global manufacturing investments accelerate across Asia Pacific, Europe, and North America, demand for high-reliability film capacitors in automation-intensive industries is expected to remain a sustained market growth catalyst throughout the forecast period.

Market Restraints

High Manufacturing Complexity and Cost Pressures Limiting Market Penetration

Precision manufacturing requirements including vacuum metal deposition, ultra-thin film control to 3-4 micron tolerance, and precision winding create capital-intensive production processes with elevated manufacturing costs. Quality assurance demands including extensive testing for self-healing capability, dielectric stability, and reliability certification increase operational complexity limiting cost-competitive expansion particularly in price-sensitive developing markets. Raw material price volatility for polypropylene film and metal deposition materials combined with energy-intensive processing creates margin pressure limiting market expansion velocity.

Temperature Sensitivity and Performance Degradation Over Extended Operating Life

Voltage derating requirements with 2% per °C DC derating above 85°C in automotive applications limit operating flexibility and design optimization opportunities. Capacitance drift over extended operational life requiring predictive maintenance and scheduled replacement impacts total cost of ownership and adoption in cost-conscious segments, creating adoption barriers in price-sensitive markets.

Market Opportunities

Ultra-Thin Film Technology and Advanced Metallization Innovation Creating Premium Market Segments

Ultra-thin metallized polypropylene films with 3-4 micron thickness enabling 18% volumetric efficiency improvement create exceptional opportunity for next-generation compact power systems. Advanced zinc-aluminum alloy metallization achieving 25% faster fault isolation speed in self-healing mechanisms establishes superior reliability advantage supporting premium pricing strategies. High-frequency switching capability exceeding 50 kHz operation combined with silicon carbide and gallium nitride semiconductor compatibility enables next-generation power electronics architectures requiring low equivalent series resistance and minimal dielectric loss.

Segmented film designs with controlled micro-fuse self-healing providing predictable capacitance degradation create smart maintenance opportunities supporting extended equipment lifespan optimization. Integration of IoT monitoring and cloud-based diagnostics enabling predictive maintenance and real-time performance optimization creates value-added service opportunities establishing sustained premium market growth through forecast period.

Healthcare, Aerospace and Defense Application Expansion with Extreme Reliability Requirements

Healthcare sector expansion including implantable medical devices, portable monitoring systems, and miniaturized biosensors creates specialized high-reliability market segment requiring compact, extremely reliable capacitors. Pacemakers and neural implants necessitating compact, reliable electrical components establish mission-critical application requirements justifying premium pricing. Aerospace and defense sector modernization requiring radiation-hardened components and extreme environmental resistance for satellite communications, radar systems, and avionics creates specialized market opportunity.

Electromagnetic pulse applications including rail gun and laser systems requiring instantaneous energy release capability establish pulsed power application niche. Military and defense system modernization across multiple continents combined with space exploration program expansion creates multi-billion dollar investment opportunity, establishing sustained growth trajectory through forecast period.

Category-wise Insights

Product Type Analysis

Self-healing metallized film capacitors represent dominant market segment commanding 65% market share driven by inherent self-healing properties eliminating catastrophic failure risk. Self-healing mechanism utilizing Joule heating to vaporize metal around defects achieving defect isolation in less than 10 microseconds with only microwatt power consumption establishes unique reliability advantage. Controlled self-healing through micro-fuse segmented film designs limiting healing current and isolating defects to defined sections prevents gradual capacitance degradation characteristic of uncontrolled healing.

KYOCERA AVX advanced controlled self-healing standard providing predictable capacitance decrease modeling enables accurate lifetime prediction and optimal service scheduling. Self-healing capability ensuring no catastrophic failure conditions combined with extensive and continuous reliability under misapplication scenarios through gradual capacitance decrease establishes superior operational safety profile. Self-healing polypropylene film capacitors commanding dominant positioning throughout forecast period due to proven reliability advantage and established supply ecosystems.

Capacitance Range Analysis

Medium capacitance range of 1 µF – 10 µF representing approximately 45% market share dominates polypropylene film capacitor applications across diverse end-user segments. Suitability for power electronics, DC-DC converters, and moderate power applications establishes universal applicability across consumer electronics, industrial, automotive, and renewable energy sectors.

Cost-effectiveness combined with performance adequacy for general purpose filtering, coupling, and decoupling applications drives widespread adoption. 1 µF – 10 µF capacitance range perfectly suited for battery management systems, automotive electronics, and renewable inverter applications where balance between capacitance requirement and physical size creates optimal trade-off point. Established manufacturing processes and supply chain maturity for medium-range capacitance ensure cost competitiveness and availability, maintaining dominant market position throughout forecast period.

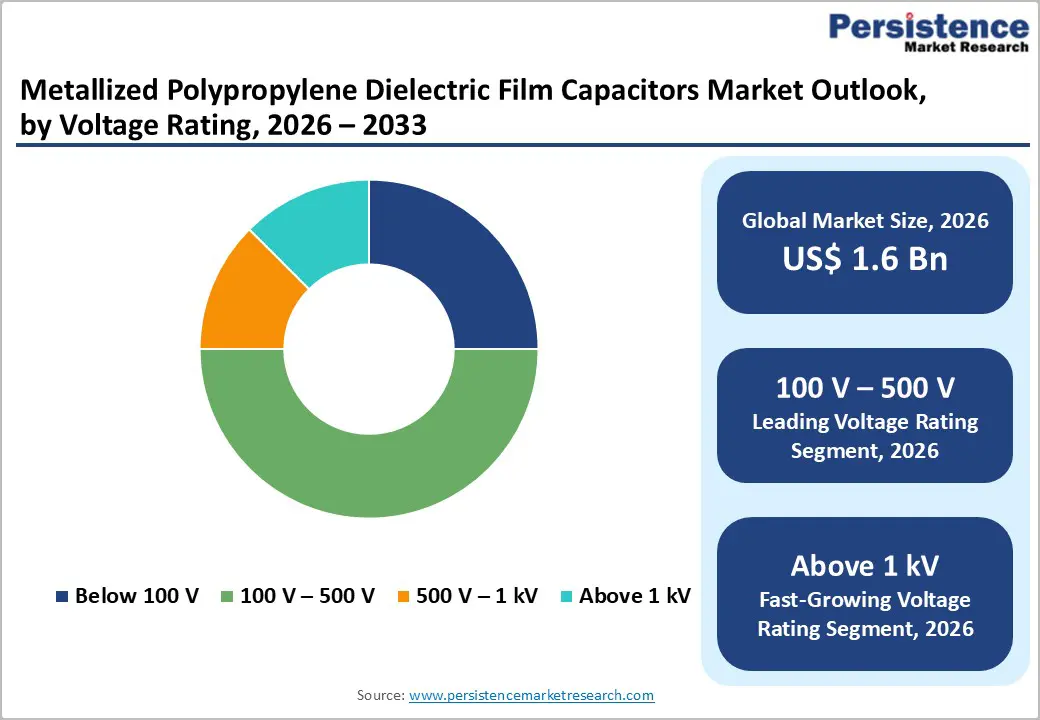

Voltage Rating Analysis

Medium-voltage range of 100 V – 500 V representing 55% market share commands dominant positioning driven by suitability for industrial, consumer electronics, and emerging automotive applications. Standard voltage rating adequacy for power supply applications, consumer electronics, and industrial automation equipment establishes universal requirement across diverse customer segments. Cost-effectiveness versus high-voltage alternatives combined with ease of integration into conventional equipment designs drives widespread adoption.

100 V – 500 V range perfectly positioned for automotive onboard electronics, battery management systems, and DC-DC converter applications where medium voltage provides optimal safety and performance balance. Established market standards, manufacturing expertise, and supplier competition for medium-voltage segments ensure cost competitiveness and innovation, maintaining sustained market leadership throughout forecast period.

Application Analysis

Consumer electronics commanding approximately 38% of total capacitor market consumption represents largest application segment for metallized polypropylene film capacitors. Smartphones, computers, appliances, power supplies, and entertainment equipment requiring high-reliability filtering and energy conditioning components establish enormous installed base supporting sustained market demand. 5G telecommunications and IoT device proliferation creating incremental capacitor demand for signal conditioning, power management, and filtering applications.

Miniaturization imperatives across consumer electronics driving adoption of ultra-thin polypropylene films with 3-4 micron thickness enabling 18% volumetric efficiency improvement create technology differentiation opportunity supporting premium pricing. Consumer electronics segment commanding dominant market share with sustained growth trajectory through forecast period.

Regional Insights

North America Metallized Polypropylene Dielectric Film Capacitors Trends

North America maintains developed market maturity with United States commanding regional leadership accounting for 43.4% global demand in 2026. Automotive electrification acceleration with 62% of newly installed DC fast chargers utilizing polypropylene film capacitors establishes critical growth catalyst for market expansion. Industrial automation efficiency gains of 15% requiring power factor correction and filtering capacitors drive sustained demand across manufacturing facilities.

Renewable energy expansion and data center power management requirements create secondary growth drivers supporting market acceleration. Regulatory emphasis on energy efficiency combined with grid modernization initiatives establish structural support for advanced capacitor adoption, ensuring sustained market expansion through forecast period.

Europe Metallized Polypropylene Dielectric Film Capacitors Trends

Europe represents advanced developed market with Germany commanding regional manufacturing base leadership. Stringent environmental regulations and ambitious carbon reduction targets create compelling demand for energy-efficient, low-loss capacitor solutions. 31% of European manufacturers embrace hybrid capacitor designs emphasizing cost-efficiency and performance optimization.

EU regulations promoting sustainability and circular economy principles drive innovation in metallized film capacitor design for enhanced performance and environmental responsibility. Advanced technology ecosystem in Germany, France, and United Kingdom supporting next-generation capacitor development, ensuring sustained innovation leadership, establishing market growth momentum through forecast period.

Asia Pacific Metallized Polypropylene Dielectric Film Capacitors Trends

Asia-Pacific commands fastest-growing regional market with China establishing epicenter status for production and consumption of metallized polypropylene film capacitors. Rapid industrialization combined with explosive consumer electronics growth including smartphones, computers, and emerging IoT devices creates enormous demand base for film capacitor solutions. Electric vehicle manufacturing expansion with China producing world-leading EV volumes establishes primary growth driver, ensuring sustained market expansion.

India experiencing accelerating growth with government Make-in-India initiatives supporting local electronics and capacitor manufacturing expansion. Japan maintaining quality-focused, high-precision specialization in niche automotive, defense, and medical applications where reliability and performance excellence command premium positioning. ASEAN region including Malaysia, Thailand, and Vietnam emerging as secondary manufacturing hubs supporting regional growth trajectory, establishing sustained Asia-Pacific expansion through forecast period.

Competitive Landscape for the Metallized Polypropylene Dielectric Film Capacitors Market

The metallized polypropylene dielectric film capacitors market exhibits moderate competitive consolidation dominated by global industrial leaders including KEMET, Murata, TDK, Vishay, Panasonic, and Nichicon commanding substantial combined market share through comprehensive product portfolios, established customer relationships, and manufacturing scale. Tier 1 manufacturers leveraging advanced R&D capabilities, precision manufacturing expertise, and global distribution networks maintain competitive advantages in demanding automotive and renewable energy segments.

Regional manufacturers including Matsuo Electric, NEC Tokin, and Iljin Electric establish competitive positions through specialized expertise, local market knowledge, and responsive customer service. Technology differentiation strategies emphasizing ultra-thin film innovations, zinc-aluminum alloy metallization, and controlled self-healing advancement create sustained competitive advantage. R&D investment focus on high-frequency capability, miniaturization, and reliability optimization supporting continuous market leadership.

Key Market Developments

- In March 2025, TDK Corporation announced the expansion of its automotive-grade metallized polypropylene film capacitor production in Japan and China, targeting high-voltage DC-link applications for electric vehicles and silicon-carbide–based traction inverters, strengthening supply security for next-generation EV power electronics.

- In January 2025, Panasonic Corporation introduced advanced low-ESR metallized polypropylene film capacitors optimized for high-frequency switching above 50 kHz, supporting wide-bandgap semiconductor adoption in fast chargers, data center power supplies, and grid-connected energy storage systems.

- In July 2024, Vishay Intertechnology launched a new series of high-temperature metallized polypropylene dielectric film capacitors rated up to 125 °C, designed for renewable energy inverters and industrial drives, addressing growing demand for long-lifetime capacitors in harsh operating environments.

Companies Covered in Global Metallized Polypropylene Dielectric Film Capacitors Market

- AFM Microelectronics Inc.

- Johanson Dielectrics Inc.

- AVX Corporation

- KEMET Electronics Corporation

- Murata Manufacturing Company

- Knowles Corporation

- CSI Capacitors

- Matsuo Electric Co. Ltd.

- NEC Tokin Corporation Inc.

- Maxwell Technologies Inc.

- Panasonic Corporation

- Samsung Electro-Mechanics Co Ltd

- Nichicon Corporation

- TDK Corporation

- Vishay Intertechnology

Frequently Asked Questions

The global Metallized Polypropylene Dielectric Film Capacitors Market is projected to reach US$ 2.4 billion by 2033, expanding from US$ 1.6 billion in 2026 at a CAGR of 5.8%, driven by electric vehicle electrification with 28% EV penetration growth, renewable energy expansion with 24% inverter installation growth, industrial automation efficiency gains of 15%, and miniaturization imperatives across consumer electronics and IoT applications.

Market demand growth is driven by multiple converging factors including electric vehicle electrification with 28% EV penetration growth in battery management systems and power converters, renewable energy sector expansion with 24% annual solar inverter installation growth, industrial automation efficiency optimization generating 15% performance improvement, 62% of DC fast chargers utilizing polypropylene film capacitors, ultra-thin film technology enabling 18% volumetric efficiency improvement, and grid modernization initiatives promoting energy-efficient power conditioning.

Self-healing metallized film capacitors command market dominance with 65-75% market share, driven by inherent failure prevention through Joule heating mechanism, defect isolation in less than 10 microseconds, predictable capacitance degradation enabling accurate lifetime prediction, and superior reliability eliminating catastrophic short circuit failure risk.

North America maintains market leadership anchored by United States with 23.4% global demand share, supported by electric vehicle adoption acceleration, 62% of DC fast chargers utilizing polypropylene film capacitors, renewable energy expansion, data center power management requirements, and advanced manufacturing technology ecosystem.

Major market opportunities include ultra-thin metallized polypropylene films (3-4 microns) enabling 18% volumetric efficiency improvement for EV traction inverters and fast-charging infrastructure; zinc-aluminum alloy metallization achieving 25% faster fault isolation for extreme reliability applications; high-frequency switching capability exceeding 50 kHz for silicon carbide and gallium nitride semiconductor integration; aerospace, defense, and healthcare segment expansion with radiation-hardened and biocompatible solutions; and IoT monitoring and predictive maintenance integration creating value-added service opportunities.

Leading market players include KEMET Electronics Corporation with North American leadership and automotive-grade R75 series featuring >200,000 hours operational life; Murata Manufacturing commanding Asia-Pacific dominance through high-reliability solutions and integrated passive technologies; Vishay Intertechnology providing MKP1848 automotive-grade DC-link capacitors with high-temperature capability and silicon capacitor co-development initiatives; and TDK Corporation advancing EPCOS film capacitor portfolio for DC-link applications and high-frequency switching capability.