- Metalworking & Fabrication

- Machine Tools Market

Machine Tools Market Size, Share, and Growth Forecast, 2026 - 2033

Machine Tools Market by Product Type (Metal Cutting and Metal Forming), by Technology (CNC and Conventional), End-user (Automotive, Mechanical Engineering, Metal Working, Aerospace, Electrical industry and Others) and Regional Analysis for 2026 - 2033

Machine Tools Market Size and Trends Analysis

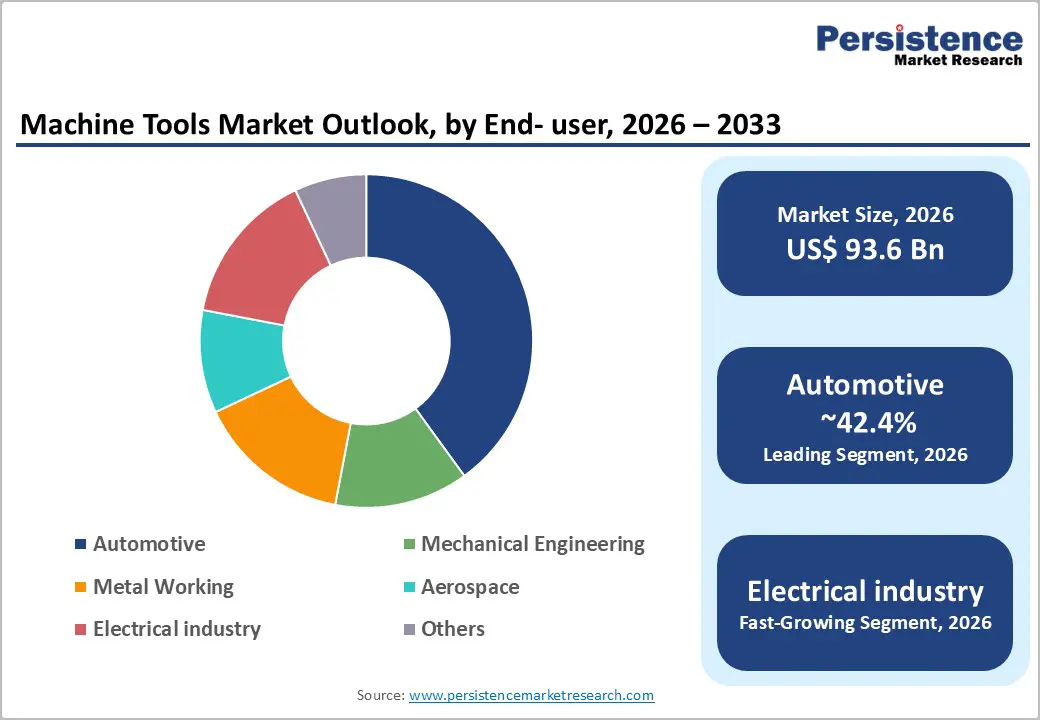

The global Machine Tools Market size is likely to be valued at US$ 93.6 billion in 2026 and is projected to reach US$ 122.3 billion by 2033, growing at a CAGR of 3.9% between 2026 and 2033.

Market expansion is driven by accelerating industrial automation adoption across manufacturing sectors, increasing demand for high-precision components in automotive and aerospace industries, and growing investments in smart manufacturing and Industry 4.0 technologies. The transition toward electric vehicle production, coupled with renewable energy infrastructure development, creates substantial machinery modernization requirements.

Key Industry Highlights:

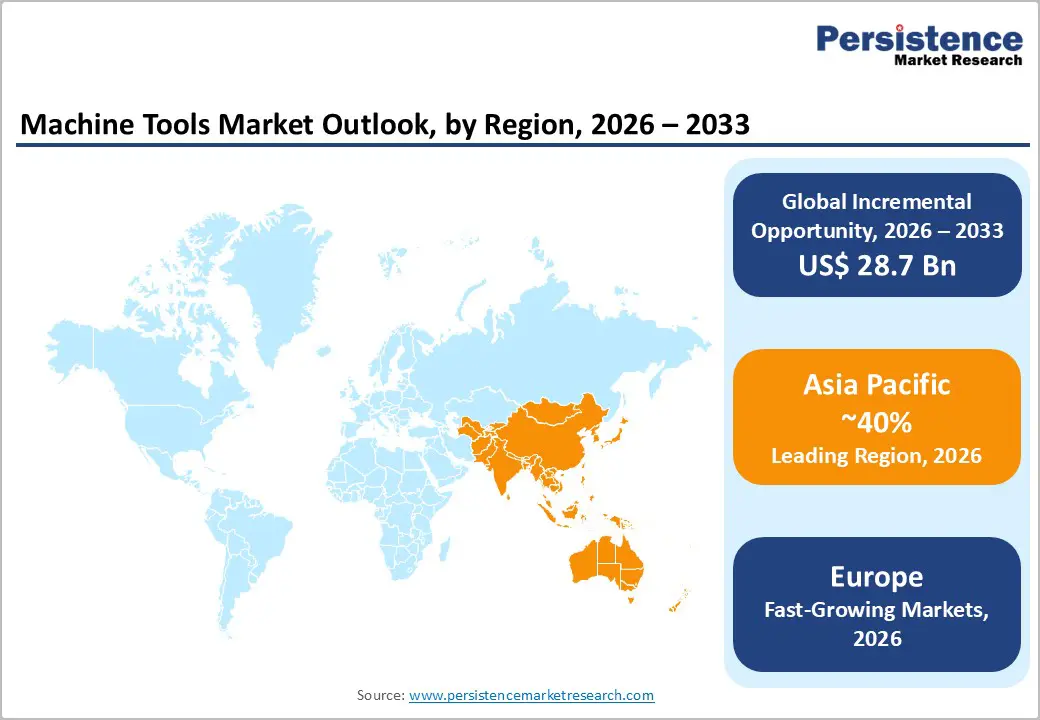

- Asia Pacific Regional Dominance: Asia Pacific commanding 40% global market share, driven by China's 7.0% growth, India's 11.6% CAGR, and Japan's aerospace/precision engineering specialization establishing region as primary growth driver.

- Automotive Industry Leadership: Automotive sector commanding 42.4% market share, driven by global vehicle production supporting 85+ million units annually with electric vehicle expansion creating incremental demand for specialized machining capabilities.

- Electrical Industry Fastest Growth: Electrical equipment sector emerging as fastest-growing end-user segment at 7.2-8.1% CAGR, driven by semiconductor manufacturing, renewable energy equipment production, and smart grid infrastructure development requiring ultra-precision components.

- CNC Technology Dominance: CNC technology commanding 80% market share with metal forming segment fastest-growing at 5.8% CAGR driven by lightweighting material requirements and servo-press technology adoption supporting automotive and aerospace applications.

- Smart Manufacturing Integration Opportunity: IoT-enabled machine tool systems capturing increasing market adoption supporting predictive maintenance, adaptive control, and real-time optimization establishing US$ 18 billion cumulative opportunity through 2033 for advanced digital manufacturing solutions.

- Government-Backed Industrial Modernization: China's "Made in China 2025," India's "Make in India," and Japan's Society 5.0 initiatives driving structural demand for machine tool adoption supporting domestic manufacturing infrastructure modernization and supply chain resilience.

| Key Insights | Details |

|---|---|

|

Machine Tools Market Size (2026E) |

US$ 93.6 Bn |

|

Market Value Forecast (2033F) |

US$ 122.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.9% |

|

Historical Market Growth (CAGR 2020 to 2024) |

3.3% |

Market Dynamics

Drivers - Industrial Automation and Smart Manufacturing Adoption Expansion

Global manufacturing sector digitalization and automation adoption establishes primary market growth driver, with Industry 4.0 technologies including IoT integration, AI-driven predictive maintenance, and digital twin simulation transforming production capabilities across sectors. China's machine tool market expansion at 7.0% CAGR reflects massive industrial automation investments supporting automotive, electronics, and aerospace manufacturing requirements. India's machine tool market growth at 11.6% CAGR demonstrates rapid industrial modernization driven by "Make in India" initiatives and government incentives promoting smart factory adoption. Japan's machine tool orders increasing for fifth consecutive month in 2025, with orders from Aircraft/Shipbuilding/Transport Equipment sector exceeding USD 900 million annualized, reflects sustained capital investment cycles in advanced manufacturing technology. Smart manufacturing integration with real-time monitoring systems, predictive maintenance capabilities reducing downtime by 20%, and automated quality control drives consistent technology upgrades across manufacturing facilities globally.

Precision Manufacturing Demand from Automotive and Aerospace Sectors

Automotive and transportation segment commanding 42.4% market share establishes dominant demand driver, with electric vehicle production requiring specialized high-precision components including battery housings, electric drivetrains, and lightweight chassis structures. Global automotive production supporting electric vehicle platforms demands 5-axis CNC machining centers capable of producing complex battery components with micrometer-level precision. Aerospace manufacturing segment growing at 3.7% CAGR, driven by aircraft production expansion with Boeing 737 MAX reintroduction, Airbus A320 production increases, and Chinese commercial aircraft programs including C919 development, creating substantial demand for specialized titanium, Inconel, and composite material machining capabilities. Medical device manufacturing segment growth at 5.2% CAGR requires ultra-precision surgical instruments and implant production demanding nanometer-level tolerance specifications. Aerospace OEMs requiring 5-axis machines for single-setup component manufacturing drives adoption of advanced machining technologies supporting complex geometry production with exceptional surface finish quality.

Restraints - High Capital Investment Requirements and Equipment Cost Barriers

CNC machine tool system acquisition costs ranging from US$ 50,000 to US$ 2 million+ per installation create substantial capital barriers particularly for small and medium-sized manufacturers in emerging economies. Installation, tooling, and software integration costs representing 30% of total equipment investment restrict market penetration among cost-constrained operators. Equipment financing availability constraints in developing regions limit technology adoption despite productivity improvement potential. Maintenance and spare parts costs representing 15-20% of annual equipment operating expenses discourage replacement cycles among operators with constrained operational budgets.

Skilled Labor Shortage and Operator Competency Constraints

Global shortage of CNC machine operators and programming experts constrains production capacity utilization across manufacturing sectors, with developed nations experiencing operator shortage rates exceeding 15-20% of required capacity. Training and competency development programs requiring 12-18 months for operational proficiency create extended ramp-up periods delaying productivity realization. Geographic disparity in technical expertise with concentrated competency in developed nations creates competitive disadvantages for emerging market manufacturers requiring specialized technical support.

Opportunity - Electrical Industry Expansion and Electronics Manufacturing Growth

Electrical industry segment emerging as fastest-growing end-user category with projected 7.2% CAGR driven by semiconductor component manufacturing expansion, renewable energy equipment production, and smart grid infrastructure development. India's electronics manufacturing sector growth at 12% annually supported by government Production-Linked Incentive schemes creates US$ 2.5 billion cumulative opportunity by 2033 for precision machine tool deployment. Semiconductor equipment production requiring ultra-precision machining with sub-micrometer tolerances drives demand for advanced multi-axis grinding and finishing centers. Renewable energy equipment, including wind turbine components, solar tracking systems, and battery manufacturing equipment requires specialized metal forming and cutting capabilities supporting consistent demand growth across electrical equipment manufacturers.

Metal Forming Technology Innovation and Lightweight Material Processing

Metal forming segment fastest-growing technology category with projected 5.8-6.4% CAGR driven by automotive lightweighting requirements for fuel efficiency and EV range extension, aerospace composite material processing, and structural steel component manufacturing. Servo-press and hydroforming technology adoption enabling complex part geometry production with 30-40% material waste reduction establishes competitive advantage for manufacturers. Composite and advanced alloy processing capabilities supporting aerospace and automotive applications represent US$ 3.2-4.8 billion opportunity through 2033. Hybrid additive-subtractive manufacturing systems integrating 3D printing with traditional machining enable rapid prototyping and low-volume custom component production, attracting aerospace and medical device manufacturers requiring quick iteration cycles.

Category-wise Analysis

Product Type Insights

Metal cutting equipment commanding 74.2% market share establishes dominant product segment driven by universal applicability across diverse material types and manufacturing processes, including machining centers, turning machines, grinding machines, and milling equipment. Metal cutting equipment versatility supporting engine components, transmission systems, chassis parts, and precision aerospace components reinforces market dominance positioning. CNC-controlled machining centers representing 45-50% of metal cutting segment benefit from standardized software platforms, expanding supplier ecosystems, and proven reliability across production environments. The metal forming product segment growing faster than metal cutting, with a projected 5.8% CAGR driven by lightweighting material requirements, complex geometry production demands, and servo-press technology adoption. The metal forming equipment including presses, bending machines, and stamping systems, increasingly incorporate IoT monitoring, digital control systems, and predictive maintenance capabilities supporting competitive differentiation.

Technology Insights

CNC (Computer Numerical Control) technology commanding 80% market share establishes a dominant technology segment reflecting superior precision, repeatability, and automation advantages over conventional equipment. CNC machines enabling 0.01-0.005mm tolerance specifications, supporting high-precision automotive and aerospace component production establish competitive advantage over conventional manual systems. CNC technology integration with AI, IoT, and digital twin simulation creates next-generation smart factory capabilities, including predictive maintenance, reducing downtime by 25%, and adaptive machining, optimizing tool life by 20%.

The conventional machine tool segment maintains niche positioning with an estimated 3.5% CAGR driven by cost-sensitive small and medium manufacturer segments, prototype development requirements, and specialized manual operations. Conventional equipment representing 15-20% of developing market adoption reflects capital cost constraints and limited skilled operator availability limiting CNC technology deployment.

Industry Insights

Automotive industry is likely to command 42.4% share establishes dominant end-user segment driven by global vehicle production supporting 85+ million annual unit output requiring engine components, transmission systems, chassis parts, and body panel precision manufacturing. Electric vehicle production acceleration with global EV sales exceeding 14 million units annually creates incremental demand for battery housing, electric motor component, and lightweight structural manufacturing capabilities. Mechanical engineering sector representing 25% market share includes industrial machinery, heavy equipment, and specialized equipment production requiring robust machining capabilities. Electrical industry segment emerging as fastest-growing end-user category with 7.2% CAGR driven by semiconductor manufacturing, renewable energy equipment production, and smart grid infrastructure components requiring ultra-precision machining.

Regional Insights

North America Machine Tools Market Trends

North America commanding estimated 22% global market share with growth rate of 3.2% CAGR driven by advanced manufacturing capabilities concentration, research and development investment strength, and innovation ecosystem maturity. United States market dominance reflects major aerospace OEM presence including Boeing, Lockheed Martin, and Raytheon requiring specialized machine tool capabilities supporting military and commercial aircraft component production. Automotive manufacturing sector investment continuation supporting domestic vehicle production and EV component manufacturing infrastructure development drives consistent demand for advanced machining solutions.

Canadian machine tools sector supporting automotive component suppliers and aerospace Tier-1 manufacturers maintain steady growth trajectory. United States reshoring initiatives including CHIPS Act investments promoting domestic semiconductor manufacturing and automotive electrification infrastructure create incremental demand for precision machine tools supporting new production facility startup. North American manufacturers emphasizing technology innovation, customized solutions, and premium customer service supporting competitive positioning in developed market segments requiring specialized technical support.

Europe Machine Tools Market Trends

Europe represents estimated 20% global market share with moderate growth at 3.5% CAGR driven by established manufacturing infrastructure, strict quality standards, and renewable energy transition requirements. Germany commanding 35-40% European market share reflecting industrial engineering expertise, automotive sector dominance, and machine tool manufacturing heritage. German machine tool manufacturers including Trumpf, Hermle, and Chiron serving global aerospace, automotive, and precision engineering sectors establish technology leadership positioning.

European Union renewable energy transition initiatives supporting wind turbine manufacturing, solar tracking system production, and battery manufacturing equipment development drive specialized metal forming and cutting requirements. United Kingdom industrial sectors including aerospace and automotive maintain sustained demand for precision machine tools despite economic uncertainty. Southern European markets including Spain and Italy experiencing recovery-driven equipment investment cycles supporting automotive supplier base modernization.

Asia Pacific Machine Tools Market Trends

Asia Pacific dominating global market commanding 40% market share with strongest regional growth projection at 5.1% CAGR driven by massive automotive production concentration, electronics manufacturing expansion, and government-backed industrial modernization initiatives. China maintaining dominant regional position with estimated 40.5% Asia Pacific market share reflecting world's largest automotive producer supporting 30 million annual vehicle output and electronics manufacturing dominance producing 40%+ global smartphone and consumer electronics volumes.

China's "Made in China 2025" strategy mandating increased CNC machine adoption and automation technology integration creates structural demand growth supporting machinery modernization across manufacturing sectors. India's machine tools market growth at 11.6% CAGR represents fastest-growing national market globally driven by "Make in India" initiatives, government incentive schemes supporting small and medium enterprise modernization, and automotive sector expansion supporting domestic vehicle production. Japan maintaining technological leadership positioning with machine tool orders increasing for fifth consecutive month in 2025 supporting aerospace, medical device, and automotive precision manufacturing specialization.

Competitive Landscape

The machine tools market demonstrates moderate consolidation with leading global manufacturers including Yamazaki Mazak (Japan), DMG MORI (Japan), Trumpf (Germany), AMADA (Japan), Okuma (Japan), Haas Automation (USA), and Makino (Japan) collectively commanding estimated 40% global market share. Yamazaki Mazak commanding estimated 12% global market share establishes leading manufacturer position through multi-tasking machine specialization, 5-axis machining technology leadership, and smart factory integration capabilities.

Market structure reflects substantial technical expertise requirements, established original equipment manufacturer relationships, comprehensive technical service capabilities, and significant research and development investment creating barriers protecting incumbent manufacturers. Emerging manufacturers in China, Taiwan, and South Korea compete through cost-effective positioning and customized equipment solutions supporting emerging market penetration.

Key Industry Developments:

- In May 2025, TRUMPF Inc. opens a smart factory in Connecticut that showcases fully networked sheet-metal fabrication workflows.

- In April 2025, InCompass acquires Bridgeport Machine Tool Company, expanding its vertical-milling product line and aftermarket parts catalogue.

- In March 2025, Mastercam completes eight acquisitions in 2025, adding CAD/CAM resellers and probing technology to deepen its CAM ecosystem.

Companies Covered in Machine Tools Market

- Amada Machine Tools Co., Ltd.

- CHIRON GROUP SE

- DMG MORI. CO., LTD.

- DN Solutions

- Georg Fischer Ltd.

- HYUNDAI WIA CORP

- JTEKT Corporation

- Komatsu Ltd

- Makino Inc.

- Okuma Corporation

- Hurco Companies, Inc.

- Others Key Players

Frequently Asked Questions

The Machine Tools market is estimated to be valued at US$ 93.6 Bn in 2026.

The key demand driver for the Machine Tools market is the growing need for advanced, precise, and automated manufacturing capabilities, which comes primarily from expanding industrial and manufacturing activities across major end-use sectors.

In 2026, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Machine Tools market.

Among the Application, Automotive hold the highest preference, capturing beyond 32.7% of the market revenue share in 2026, surpassing other Application.

The key players in Machine Tools are AMADA Co., Ltd, Bystronic Laser AG, Coherent Corp. and DAIHEN Corporation.