- Non-food Packaging

- Cartoning Machines Market

Cartoning Machines Market Size, Share, Trends, Regional Forecasts 2026 - 2033

Cartoning Machines Market by Machine Type (Horizontal Cartoning Machines, Vertical Cartoning Machines), Capacity Range (Up to 70 CPM, 71 to 150 CPM, 151 to 400 CPM, Above 400 CPM), Industry (Food & Beverage, Healthcare & Pharmaceuticals, Consumer Goods, Others), and Regional Analysis from 2026 - 2033

Cartoning Machines Market Share and Trends Analysis

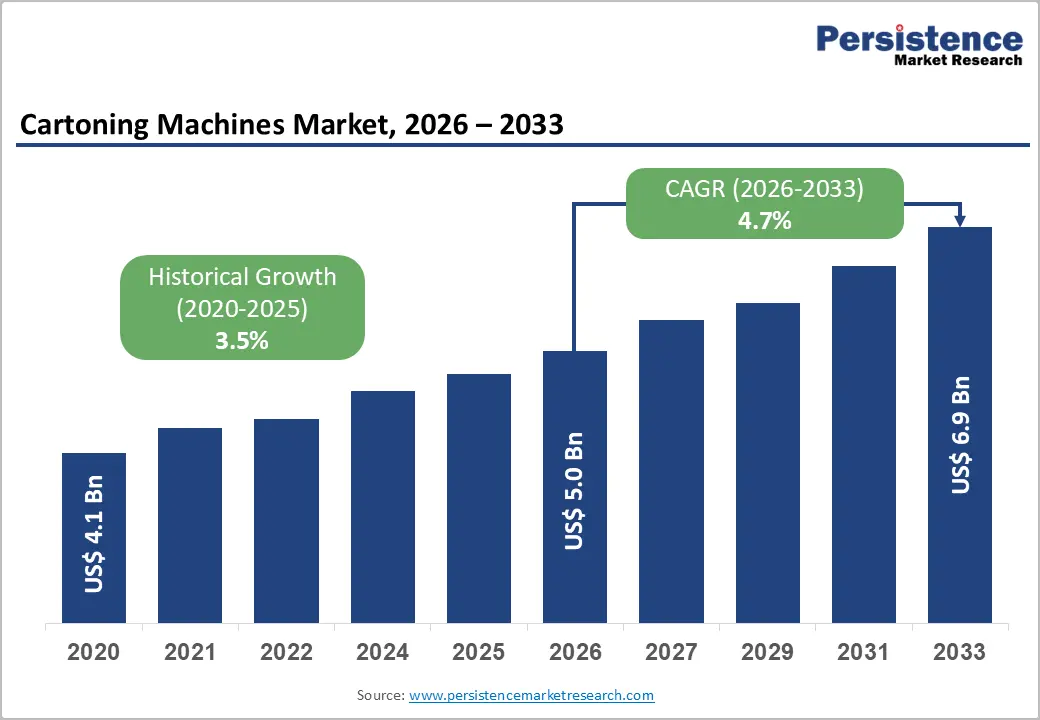

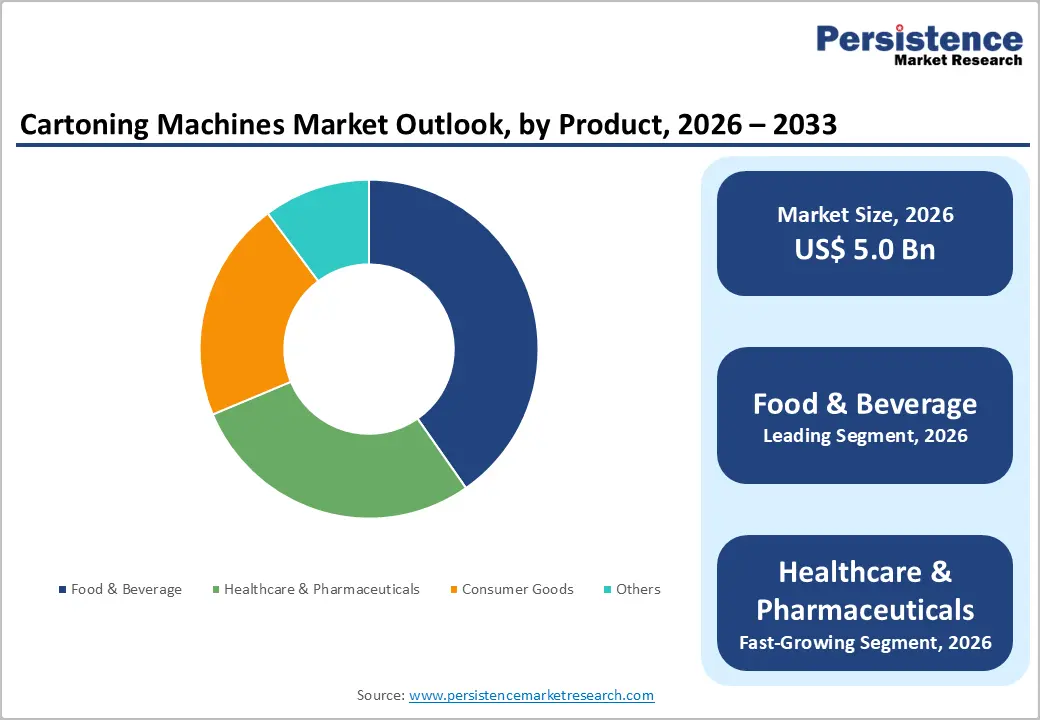

The global cartoning machines market size is anticipated at US$ 5.0 Billion in 2026 and is projected to reach US$ 6.9 Billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

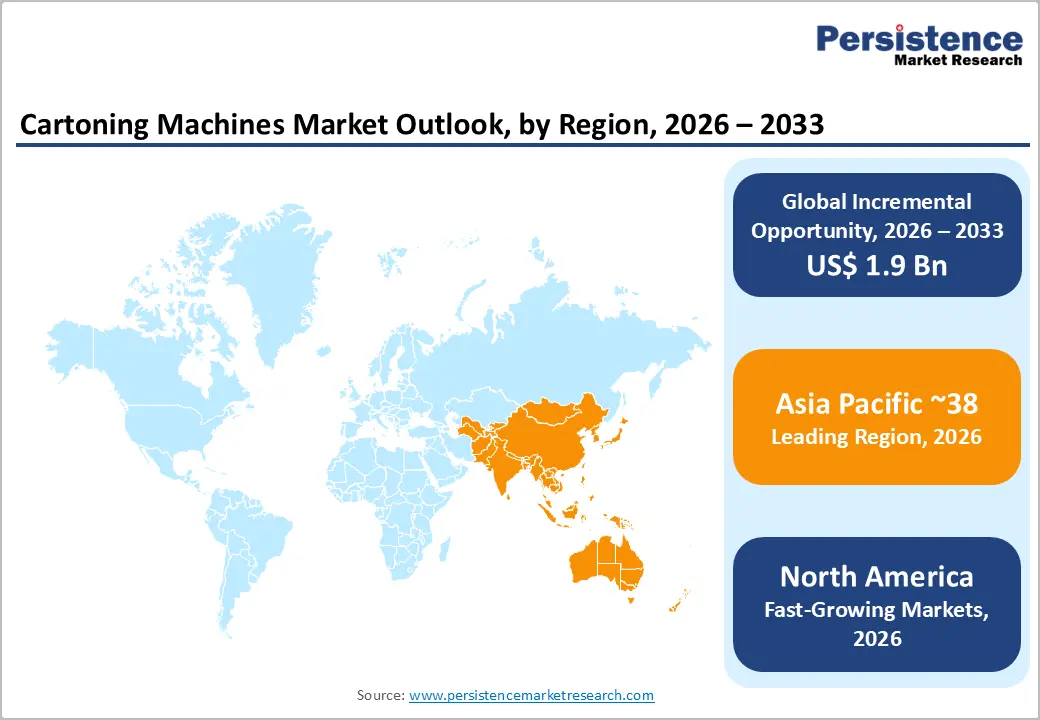

Market expansion is driven by automation and efficiency improvements in food and beverage, specialized cartoning for pharmaceuticals and healthcare, and AI and IoT integration, enabling smart monitoring and predictive maintenance. North America grows at 4.3% CAGR with automation leadership, Europe benefits from manufacturing excellence and compliance, and Asia Pacific leads with 38% share, driven by FMCG growth and emerging market production expansion.

Key Industry Highlights:

- Horizontal cartoning machines command 64% market share, reflecting versatility and broad application suitability, while Vertical machines expand at 3.8% CAGR supporting pharmaceutical and healthcare specialization requirements.

- 71-150 CPM capacity dominates at 34% share, reflecting optimal cost-performance balance, while Above 400 CPM segment expands at 6.1% CAGR, supporting high-volume mass-production requirements.

- Food & Beverage applications lead at 40% market share, while Healthcare & Pharmaceuticals expands at 6% CAGR as fastest-growing segment supporting regulatory requirements and product safety emphasis.

- Europe maintains 23% market share with manufacturing excellence emphasis, Asia Pacific dominates 38% with China at 7.0% and India at 6.5% CAGR supporting FMCG and pharmaceutical expansion, and North America grows at 4.3% CAGR with automation and technology leadership.

- Econocorp launches Spartan Mon PACK EX (October 2024), WK Packaging introduces CH 4 with 20% energy reduction (April 2024), and ELITER showcases GRAN SONATA at Shanghai Packaging (November 2023) demonstrating technology advancement and automation momentum.

| Key Insights | Details |

|---|---|

|

Cartoning Machines Market Size (2026E) |

US$ 5.0 billion |

|

Market Value Forecast (2033F) |

US$ 6.9 billion |

|

Projected Growth CAGR (2026-2033) |

4.7% |

|

Historical Market Growth (2020-2025) |

3.5% |

Market Dynamics Analysis

Driver - Automation and Production Efficiency Driving Cartoning Machine Adoption Across Industries

Automation and production efficiency improvements are systematically driving cartoning machine adoption, as manufacturers increasingly invest in high speed solutions to address rising production requirements across food, pharmaceutical, and consumer goods industries. Fully automatic horizontal cartoning machines achieved 46% market share in 2025, enabling significant labor cost reduction while ensuring consistent output quality and operational reliability. Demand is concentrated around the 100 to 200 cartons per minute capacity sweet spot, balancing throughput, flexibility, and capital efficiency.

Turnkey cartoning solutions integrating overall equipment effectiveness metrics enhance real time monitoring, reduce manual labor dependency, and support predictive maintenance. Advanced systems offer seamless downstream operation integration, automated carton forming and sealing, and compatibility with existing production lines, improving quality assurance, uptime, and packaging efficiency.

Pharmaceutical and Healthcare Industry Specialization Requirements Supporting Technology Advancement

Pharmaceutical and healthcare industry expansion is systematically accelerating advanced cartoning machine development, as healthcare and pharmaceuticals emerge as the fastest growing end use segment at a 6% CAGR. Rising demand for specialized vertical cartoning solutions addresses precise handling of vials, ampoules, and pre filled syringes while supporting stringent compliance driven packaging requirements. Pharmaceutical carton specialization focuses on dimensional accuracy, gentle product transfer, and contamination prevention to protect product safety and integrity.

Manufacturers increasingly integrate regulatory compliance assurance features, including serialization and track and trace capability, to meet global standards. Advanced cartoning systems also support cold chain compatibility requirements, ensuring packaging stability for temperature sensitive drugs while maintaining efficiency, reliability, and consistent quality across high volume pharmaceutical production environments globally.

Restraint - High Capital Investment and Maintenance Costs Limiting Small and Medium Enterprise Adoption

Cartoning machine market expansion is constrained by high upfront capital investment, as advanced and AI integrated systems require substantial spending that limits adoption among small and medium manufacturers in cost sensitive segments. Equipment purchase costs for new machinery remain significant, compounded by installation, commissioning, and line integration expenses. Additional financial pressure arises from skilled operator training requirements, ongoing maintenance and service contracts, and spare parts inventory management.

Software licensing for AI and IoT features further increases total cost of ownership. Moreover, downtime and temporary production losses during maintenance or upgrades negatively impact operational efficiency, delaying return on investment cycles globally.

Supply Chain Disruptions and Component Availability Constraints Affecting Production

Cartoning machine market expansion is constrained by supply chain vulnerabilities impacting the availability of critical components such as servo motors, control systems, and specialized sensors, leading to production delays and extended lead times. These challenges particularly affect emerging markets with limited local supplier networks, slowing customer adoption. Additional pressures arise from global logistics disruptions, supplier consolidation reducing alternative sources, and quality assurance constraints that complicate component sourcing.

Geopolitical risks further exacerbate supply instability, affecting reliability and cost predictability. Together, these factors hinder timely delivery, limit production scalability, and create barriers to market growth for advanced cartoning machine manufacturers globally.

Opportunity - Modular and Flexible Cartoning Systems Supporting SME and Product Diversification

Modular and flexible cartoning machine platforms represent a significant emerging opportunity, driven by growing demand for rapid changeover and multi-format machines that enable efficient handling of diverse SKUs. These solutions are particularly suited for small and medium enterprises, offering cost effective automation that supports dynamic market responsiveness and operational scalability. Modular design capabilities allow manufacturers to customize configurations for specific production needs, while rapid changeover features minimize downtime and enhance throughput. Multi-SKU flexibility ensures seamless adaptation to varying product lines, supporting product innovation and faster time to market. Scalable configurations enable gradual capacity expansion, while competitive entry pricing facilitates SME market penetration, driving adoption and long-term growth in emerging and mature markets alike.

Sustainability and Eco-Friendly Packaging Solutions Supporting Premium Positioning

Sustainability and eco-friendly packaging solutions are emerging as a key opportunity in the cartoning machine market, with manufacturers increasingly designing systems compatible with recyclable and biodegradable materials to meet evolving environmental standards. Advanced machine designs achieve 20%+ energy consumption reduction, contributing to operational efficiency while supporting premium market positioning. These solutions enable waste reduction optimization, carbon footprint minimization, and adherence to circular economy principles, aligning with global sustainability initiatives.

Compatibility with recyclable and biodegradable cartons ensures versatile product handling, while energy-efficient operation reduces overall production costs. By integrating regulatory compliance advantages and sustainable practices, manufacturers can drive adoption of environmentally responsible packaging, strengthen brand reputation, and capitalize on growing demand for eco-conscious packaging solutions globally.

Category-wise Analysis

Machine Type Insights

Horizontal cartoning machines command 64% of market share, representing dominant machine type reflecting versatility, affordability, and broad application suitability across food and beverage, pharmaceuticals, and personal care segments with high-speed capability and flexible carton accommodation supporting broad market adoption.

Vertical cartoning machines expand as fastest-growing machine category, driven by pharmaceutical and healthcare specialization requirements supporting emerging demand for precision packaging of delicate and small products including vials, ampoules, syringes, and weight-based food items reflecting regulatory requirements and product safety emphasis.

Capacity Insights

71-150 cartons per minute segment commands 34% of market share, representing industry standard capacity reflecting optimal balance between speed, flexibility, and cost supporting mid-to-large scale manufacturers across diverse industries with practical production volume and changeover capability. Mid-range speed capability. Optimal cost-performance balance. Flexibility advantage over high-speed. Industry standard specification. Broad application suitability. Maintenance efficiency support. Wide market adoption.

Above 400 cartons per minute segment expands by 6.1% CAGR as fastest-growing category, driven by high-volume production requirements from major beverage, confectionery, and pharmaceutical manufacturers supporting emerging demand for maximum-throughput solutions in mass-production and large-scale manufacturing environments requiring premium equipment investment justification.

Industry Insights

Food and beverage applications command 40% of market share, representing dominant end-use segment reflecting largest cartoning requirement across beverage, snack, dairy, and confectionery segments with high-volume production and packaging diversity supporting broad market penetration and sustained demand. Healthcare and pharmaceuticals expand as fastest-growing end-use segment with 6.0% CAGR, driven by pharmaceutical industry expansion and specialized cartoning requirements for medication boxes, medical device packaging, and healthcare product safety, supporting emerging segment growth exceeding overall market rates reflecting regulatory emphasis and product integrity requirements.

Pharmaceutical carton specialization. Medical device packaging. Healthcare product safety focus. Regulatory compliance requirements. Track-and-trace integration. Cold chain support. Emerging healthcare market growth.

Regional Insights

North America Cartoning Machines Market Trends

North America expands at 4.3% CAGR, driven by automation leadership, diverse industry adoption, regulatory frameworks, and technology innovation supporting market development and equipment modernization. North American market characterized by technology leadership and diverse industry adoption with manufacturers investing in high-speed servo-driven solutions. Strong emphasis on automation and efficiency supporting competitive advantage. Established supply chains and service networks enabling rapid deployment. Premium positioning supporting advanced technology integration and innovation.

Europe Cartoning Machines Market Trends

Europe maintains 23% market share with considerable growth pace, driven by manufacturing excellence, sustainability emphasis, regulatory harmonization, and advanced technology adoption supporting market leadership and premium positioning. Manufacturing heritage and expertise. Sustainability focus on eco-friendly solutions. Regulatory harmonization across EU. Advanced machinery integration. European market characterized by regulatory compliance emphasis and manufacturing excellence with established brands including IWK, Schubert, and Uhlmann driving innovation. Strong emphasis on sustainability and energy efficiency supporting environmental compliance. Technical standards supporting reliability and precision. Partnership ecosystems enabling innovation and market development.

Asia Pacific Cartoning Machines Market Trends

Asia Pacific dominates at 38% market share, driven by rapid FMCG growth, manufacturing scale, cost-competitive production, and emerging market expansion supporting market growth exceeding global averages. FMCG sector expansion and growth. Pharmaceutical manufacturing scaling in China and India. Asia Pacific market characterized by rapid growth and diverse manufacturing opportunities with China leading through massive beverage and food processing scale. India emerging as high-growth pharmaceutical and FMCG hub. Cost-competitive production attracting global supply chain development. Government support programs and infrastructure investment accelerating adoption.

Competitive Landscape

The global cartoning machines market exhibits moderate consolidation, with multinational leaders like Robert Bosch, Marchesini Group, and Econocorp driving growth through integrated technology platforms, global distribution, and service support. Regional specialists such as Jacob White Packaging, IMA Group, and Uhlmann Pac-Systeme focus on geographic and application niches, while emerging players capture opportunities with innovative, cost-effective designs enabling technology-driven competitive differentiation.

Strategic Developments (Post-2023)

- In October 2024, Econocorp introduced latest Spartan Mon PACK EX International secondary machine demonstrating advanced automation capabilities and supporting market demand for high-efficiency cartoning solutions across diverse industries and applications.

- In April 2024, WK Packaging introduced CH 4 modular horizontal cartoning machine achieving over 20% energy consumption reduction while designed for pharmaceutical containers including vials and fragile materials, demonstrating technology advancement and sustainability focus.

- In November 2023, ELITER unveiled GRAN SONATA end-load cartoner for larger and medium-sized cases supporting secondary and tertiary packaging automation, demonstrating emerging market technology adoption and automation momentum.

Companies Covered in Cartoning Machines Market

- Robert Bosch LLC

- Marchesini Group

- Econocorp Inc.

- Jacob White Packaging Ltd.

- IMA Group

- Uhlmann Pac-Systeme

- IWK Verpackungstechnik

- Schubert

- ADCO Manufacturing

- PMI Cartoning Systems

- Bradman Lake Inc.

- Molins

- Cama Group

- WK Packaging

Frequently Asked Questions

The global cartoning machines market size is anticipated at US$ 5.0 Billion in 2026 and is projected to reach US$ 6.9 Billion by 2033.

Market growth is propelled by automation-led efficiency gains, strong food & beverage and FMCG demand (40% share), and pharmaceutical specialization expanding at 6% CAGR, supported by high-speed horizontal machines and vertical systems for medical packaging.

The market is projected to expand at a 4.7% CAGR between 2026 and 2033.

Key opportunities lie in Asia Pacific expansion led by China (7.0% CAGR) and India (6.5% CAGR), sustainable and energy-efficient machines delivering 20%+ savings, and modular, flexible cartoners enabling rapid changeovers and SME adoption.

The market is led by Bosch, Marchesini Group, IMA, Uhlmann, Econocorp, Jacob White Packaging, and WK Packaging, with recent innovations such as energy-efficient and modular cartoners reinforcing competitive differentiation.