- Sensors & Controls

- Light Sensor Market

Light Sensor Market Size, Share, and Growth Forecast 2025 - 2032

Light Sensor Market by Function (Proximity Detection, Color and Luminance Measurement, Ambient Light Sensing, Motion and Gesture Recognition, UV Index Detection, Others), Integration (Discrete Light Sensors, Integrated Light Sensor Modules, Smart Sensors), Industry (Consumer Electronics, Automotive, Industrial Automation, Healthcare & Medical Devices, Smart Home & IoT Devices, Aerospace & Defense, Security & Surveillance, Others), by Regional Analysis, 2025 - 2032

Light Sensor Market Size and Trend Analysis

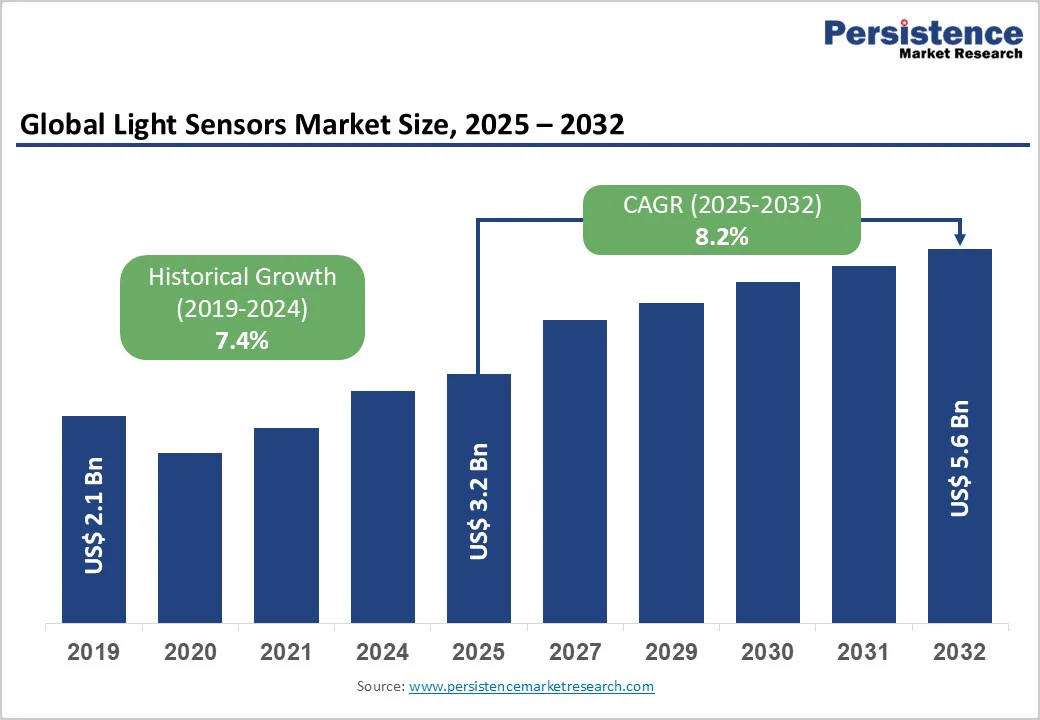

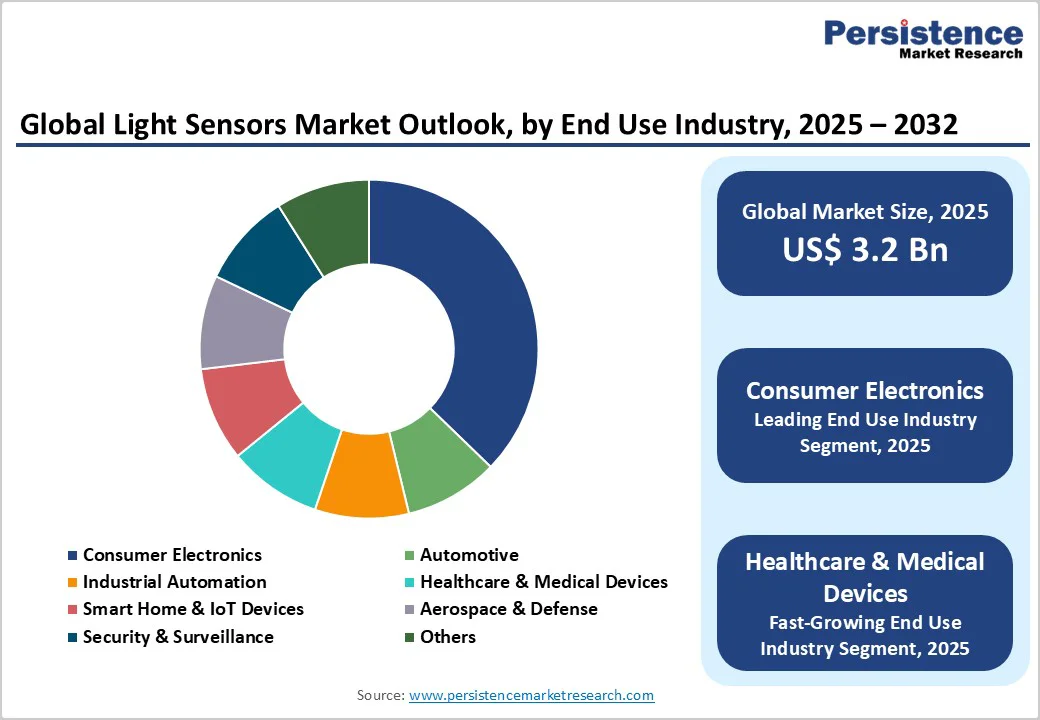

The global light sensors market size is valued at US$3.2 billion in 2025 and projected to reach US$5.6 billion by 2032, growing at a CAGR of 8.2% between 2025 and 2032.

The market expansion is driven by the accelerating adoption of smart devices and IoT applications across multiple industries, coupled with stringent automotive safety regulations that require advanced sensing solutions. The increasing demand for energy-efficient lighting systems in commercial and residential buildings, alongside technological advancements in sensor miniaturization and performance enhancement, provides compelling reasons for sustained market growth.

Key Market Highlights:

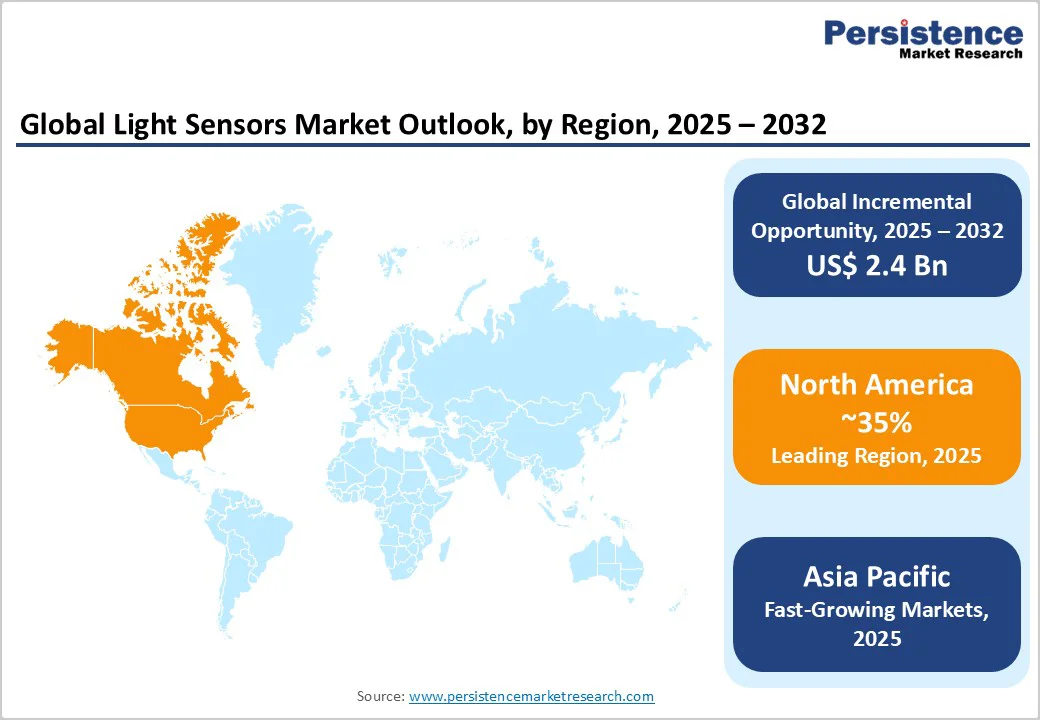

- Leading Region: North America lead the light sensor market in 2025, holding a ~35% share due to stringent automotive safety regulations, advanced manufacturing, and smart city initiatives driving energy-efficient lighting adoption.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market with a projected CAGR above 14% through 2032, fueled by massive smartphone penetration, China’s smart city infrastructure development, and Industry 4.0-driven industrial automation.

- Dominant Function Segment: Ambient light sensing dominates functional applications, with ~32% market share, and is widely integrated in consumer electronics for automatic display brightness control.

- Leading End-Use Segment: Consumer electronics lead end-use demand at ~38%, driven by smartphones, tablets, and wearables.

- Key Market Opportunity: Healthcare and wearable biometric monitoring offer significant growth potential, supported by continuous physiological tracking, sensor miniaturization, AI integration, and clinical validation of device accuracy.

| Key Insights | Details |

|---|---|

|

Light Sensors Market Size (2025E) |

US$3.2 billion |

|

Market Value Forecast (2032F) |

US$5.6 billion |

|

Projected Growth CAGR(2025-2032) |

8.2% |

|

Historical Market Growth (2019-2024) |

7.4% |

Market Dynamics

Drivers - Rising Adoption of Smart Devices and IoT Ecosystem Expansion

The proliferation of smart devices and IoT-enabled solutions is fundamentally transforming the light sensors market landscape. Smartphones, wearables, smart home solutions, and connected industrial equipment increasingly incorporate ambient light sensors to optimize display brightness, reduce power consumption, and enhance user experience. The global smartphone penetration, coupled with rising internet connectivity in developing economies, has created unprecedented demand for light sensors. Asia Pacific alone hosts over 1 billion smartphone users, driving substantial adoption of light sensors in consumer electronics.

Additionally, IoT applications in smart cities, connected homes, and industrial automation platforms increasingly rely on sophisticated light-sensing capabilities, including color detection sensors, for real-time environmental monitoring and adaptive control mechanisms. Smart lighting systems utilizing these sensors can achieve energy savings of up to 50% in some deployments, making them appealing to commercial enterprises and residential consumers seeking to reduce operational costs and environmental impact. The integration of artificial intelligence and machine learning with light and color detection sensors enables contextual intelligence, allowing systems to learn user preferences and autonomously adjust lighting conditions for optimized comfort and efficiency.

Automotive Safety Regulations and Advanced Driver Assistance Systems Integration

Automotive manufacturers are increasingly integrating Automotive Sensors, including light sensors, into Advanced Driver Assistance Systems (ADAS) to comply with stringent safety regulations and enhance vehicle safety. Federal Motor Vehicle Safety Standard 108 (FMVSS 108) governs automotive lighting and signaling devices in the United States, while similar regulations exist across Europe, Canada, and other regions. Adaptive driving beam (ADB) headlights, which utilize light sensors to detect oncoming traffic and adjust beam patterns accordingly, are becoming mandatory in many developed markets.

Insurance data from the Highway Loss Data Institute (HLDI) demonstrates that curve-adaptive headlights reduce collision claims by 1.1% and property damage liability claims by 5.8% across seven major original equipment manufacturers. Light sensors, as part of Automotive Sensors, enable automatic headlight adjustment based on ambient lighting conditions, improving visibility during dawn, dusk, and nighttime driving. The implementation of FMVSS No. 127, which mandates Automatic Emergency Braking (AEB) and Pedestrian Automatic Emergency Braking (PAEB) including nighttime scenarios by September 2029, requires advanced sensing technologies including light sensors integrated with cameras and radar systems. These regulatory requirements create sustained demand for high-performance light sensors in the automotive sector.

Restraints - Cost Pressures and Price Competition in Consumer Electronics Segment

The consumer electronics segment, accounting for roughly 36% of light sensor applications, faces significant cost pressures and intense price competition. Smartphone and wearable manufacturers continuously optimize supply chains, driving demand for lower-cost sensors without compromising performance. Expansion of MEMS-based sensor production, which grew 22% in 2024, intensifies market competition and further suppresses prices. Price-sensitive regions, particularly in Asia Pacific, limit adoption of premium sensor solutions. Additionally, slow device replacement cycles and integration of multiple functions into single chips reduce per-unit sensor demand. Manufacturers must balance cost reduction with ongoing R&D investments for next-generation sensors featuring improved accuracy, miniaturization, and energy efficiency.

Technical Challenges in High-Accuracy Applications and Performance Consistency

High-accuracy applications in automotive, aerospace, healthcare, and defense impose strict performance and reliability requirements, creating technical barriers for light sensor manufacturers. Sensors must maintain consistent spectral response across extreme lighting conditions—from bright sunlight to dim indoor environments—and operate reliably under temperature fluctuations, humidity, vibration, and electromagnetic interference. Wearable healthcare devices require noise-free measurements and precise physiological monitoring, while aerospace and defense applications demand robustness under harsh environmental conditions. Achieving these standards requires advanced manufacturing processes, continuous calibration, quality assurance, and regulatory certifications. These technical complexities increase production costs, extend development timelines, and challenge scalability, limiting rapid commercialization of high-performance light sensors.

Opportunity - Healthcare and Wearable Biometric Monitoring Applications Expansion

The healthcare and wearable electronics sectors present the fastest-growing opportunity for light sensors, fueled by rising demand for preventive health monitoring and remote patient care. Wearable devices integrate light sensors for continuous measurement of heart rate, blood oxygen saturation (SpO2), and respiratory metrics using photoplethysmography (PPG) technology. Advanced wrist-based systems combine sensors with signal processing to track sleep patterns, cardiac health, and wellness trends. Regulatory approvals for medical wearables and insurance support for remote monitoring enhance adoption potential. Post-pandemic awareness of health tracking, along with aging populations in developed markets, drives sustained interest. As consumer familiarity grows, companies investing in wearable health sensor development can capture significant share in this high-growth, technology-driven segment.

Smart City Infrastructure Development and Environmental Monitoring Requirements

Global smart city initiatives and energy efficiency mandates are creating significant opportunities for light sensor adoption in building automation systems, street lighting, and environmental monitoring. Regulations such as the EU’s Energy Performance of Buildings Directive (EPBD 2024) promote automatic lighting controls within building automation systems, enabling energy savings of up to 30% through adaptive brightness and daylight harvesting. UV and ambient light sensors are increasingly applied in precision agriculture, industrial automation, and water quality monitoring, supporting optimized growth, product quality, and public safety. China’s investment in smart city and renewable energy infrastructure contributes over a quarter of Asia Pacific’s market revenue. Across environmental, industrial, and urban development applications, light sensors emerge as essential enabling technologies for sustainable, intelligent systems.

Category-wise Analysis

Function Insights

Ambient light sensing emerges as the leading functional segment, holding roughly 32% market share in 2025, driven by its widespread adoption in consumer electronics and smart lighting applications. These sensors automatically adjust screen brightness in smartphones, tablets, and laptops, enhancing visibility while conserving battery life. Modern devices increasingly incorporate dual ambient light sensors to optimize performance under varying lighting conditions, exemplified by premium smartphones. The growing emphasis on energy efficiency and user experience ensures continuous integration of ambient light sensing in next-generation consumer electronics, making it a critical feature for mobile devices and automated lighting systems alike.

Integration Insights

Integrated light sensor modules dominate the integration segment with approximately 54% market share in 2025, combining ambient light and proximity detection into a single device with embedded signal processing. These modules simplify system design, reduce PCB space requirements, and lower manufacturing costs compared to discrete sensors. Advances in MEMS technology allow multiple sensing elements and digital circuitry to coexist on a single semiconductor die, enabling context-aware lighting control and enhanced functionality. Their efficiency and compactness make integrated modules the preferred choice for smartphones, wearables, and other high-volume consumer electronics, supporting scalable deployment of sophisticated light sensing systems.

Industry Insights

Consumer electronics leads the end-use industry segment with around 38% market share in 2025, driven by near-universal use of light sensors in smartphones, tablets, laptops, and wearables. The expanding global smartphone base, particularly in Asia Pacific, sustains consistent demand for ambient light and proximity sensing solutions. Light sensors enhance user experience by enabling adaptive screen brightness and intuitive device interactions. Continuous innovation in mobile and personal computing devices, combined with integration into emerging smart home ecosystems, ensures that consumer electronics remain the primary driver of light sensor adoption, maintaining both market scale and technological advancement.

Regional Insights

North America Light Sensor Trends & Insights

North America holds a significant share of the global light sensor market, accounting for around 35% in 2025, driven by advanced automotive infrastructure, high-tech manufacturing, and widespread adoption of smart technologies across consumer and industrial sectors. The U.S. market benefits from stringent automotive safety regulations, such as FMVSS standards, mandating advanced lighting and sensing systems in vehicles, which fuels demand for high-performance sensors in ADAS and adaptive lighting solutions.

Government initiatives promoting smart city development and energy-efficient building standards, including LEED certification, encourage integration of ambient light sensors in automated lighting systems. In Canada, alignment with U.S. automotive standards ensures consistent regional demand. The technology hubs in Silicon Valley and other regions foster innovation in smartphones, wearables, and IoT-enabled smart home solutions, while commercial and residential adoption of daylight-harvesting and occupancy-responsive lighting systems strengthens North America’s position as a leader in light sensor development and deployment.

Europe Light Sensor Market Trends & Insights

Europe represents a mature, innovation-driven light sensor market with strong focus on sustainability and energy efficiency. Regulatory frameworks such as the Energy Performance of Buildings Directive (EPBD 2024) mandate automatic lighting controls and smart readiness indicators, stimulating widespread deployment of sensor-integrated smart lighting in commercial and institutional buildings. Germany, Europe’s automotive hub, drives demand through premium vehicle ADAS and adaptive headlight technologies, with manufacturers integrating sophisticated light sensors for enhanced driving safety.

Countries, including the UK, France, and Spain, reinforce energy-efficient lighting adoption through public sector building renovations and private commercial upgrades. Adaptive Driving Beam (ADB) headlights exemplify advanced technology adoption, optimizing illumination while preventing glare. Industry associations like LightingEurope actively influence regulatory development, shaping market growth. European automotive suppliers and sensor manufacturers maintain technological leadership, developing next-generation solutions for automotive, consumer electronics, and industrial applications, ensuring continued expansion in both domestic and export markets.

Asia Pacific Light Sensor Market Analysis

Asia Pacific is the fastest-growing regional market for light sensors, projected to expand at a CAGR exceeding 14% from 2025 to 2032, driven by rapid urbanization, industrial automation, and government-backed smart city initiatives. China dominates the region, leveraging extensive consumer electronics manufacturing and Industry 4.0 initiatives, with MEMS-based light sensor production growing 22% year-over-year in 2024. Japan continues to lead in sensor miniaturization and design, supplying high-performance solutions for automotive and consumer electronics sectors.

India is emerging as a key growth market, fueled by rising smartphone penetration and government initiatives promoting renewable energy and smart grid deployment. South Korea, Taiwan, and ASEAN countries, including Vietnam, Thailand, and Malaysia, strengthen regional manufacturing capabilities, supplying global device manufacturers while supporting domestic demand. Expanding industrial automation, smart city infrastructure, and IoT-based energy management systems drive adoption across consumer, commercial, and industrial segments throughout Asia Pacific.

Competitive Landscape

The competitive landscape of the light sensors market is moderately consolidated, driven by a blend of global semiconductor leaders and specialized sensor innovators competing across automotive, consumer electronics, wearables, and industrial applications. Companies strengthen their positioning through broad product portfolios, deep R&D capabilities, and strong integration of sensing, signal processing, and communication technologies.

Leading players increasingly focus on miniaturization, energy efficiency, and next-generation sensing architectures to meet rising demand from compact devices and smart systems. Strategic differentiation centers on advanced manufacturing, AI-enabled sensing algorithms, and seamless integration with IoT, ADAS, and digital health platforms. While mergers and acquisitions occur selectively, market growth is primarily propelled through organic innovation and targeted product development. Specialized manufacturers further enhance competitiveness by offering application-specific solutions tailored for healthcare monitoring, automotive safety compliance, and industrial automation.

Key Market Developments

- January 2025: ams-OSRAM unveiled its EVIYOS™ HD 25 adaptive headlight technology and new capacitive sensing solutions at CES 2025, reinforcing advancements in automotive lighting, touchless entry, and intelligent vehicle safety systems.

- July 2025: STMicro announced a deal to acquire part of NXP’s sensor business for up to US$ 950 million, significantly boosting its MEMS and light-sensor capabilities for automotive and industrial applications.

Companies Covered in Light Sensor Market

- ams-OSRAM AG

- Sharp Corporation

- Broadcom Inc.

- Apple, Inc.

- Elan Microelectronic Corp.

- Vishay Intertechnology, Inc.

- Heptagon

- Everlight Electronics Co., Ltd.

- Sitronix Technology Corporation

- Maxim Integrated Products, Inc.

- ROHM Co., Ltd.

- Samsung Electronics Co., Ltd.

- STMicroelectronics

- Renesas Electronics Corporation

- Analog Devices, Inc.

- Sensortek

- ActLight

- Ambiq Micro

Frequently Asked Questions

The light sensors market is valued at US$ 3.2 billion in 2025 and is projected to reach US$ 5.6 billion by 2032 at a CAGR of 8.2%.

Demand is driven by growing smart device adoption, stricter automotive safety regulations, energy-efficient building automation mandates, rising wearable health monitoring, and Industry 4.0 automation requirements.

Ambient Light Sensing leads with around 32% share due to universal use in consumer electronics for brightness control, power optimization, and smart lighting applications.

Asia Pacific is the fastest-growing region with a CAGR above 14%, supported by massive smartphone usage, rapid urbanization, smart city investments, and rising industrial automation.

Healthcare and wearable biometric monitoring offer the strongest opportunity, with a 13.26% CAGR driven by rising demand for continuous health tracking and remote patient monitoring.

ams-OSRAM, STMicroelectronics, Broadcom, Sharp, Apple, Samsung, and Maxim Integrated lead through strong semiconductor portfolios, miniaturization expertise, OEM partnerships, and sustained R&D investment.