- Automotive Components & Materials

- ADAS Sensors Market

ADAS Sensors Market Size, Share, and Growth Forecast, 2026 – 2033

ADAS Sensors Market by Application Type (Adaptive Cruise Control (ACC), Blind Spot Detection System (BSD), Others), Vehicle (Passenger Cars, Commercial Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle), and Regional Analysis for 2026 – 2033

ADAS Sensors Market Size and Trends Analysis

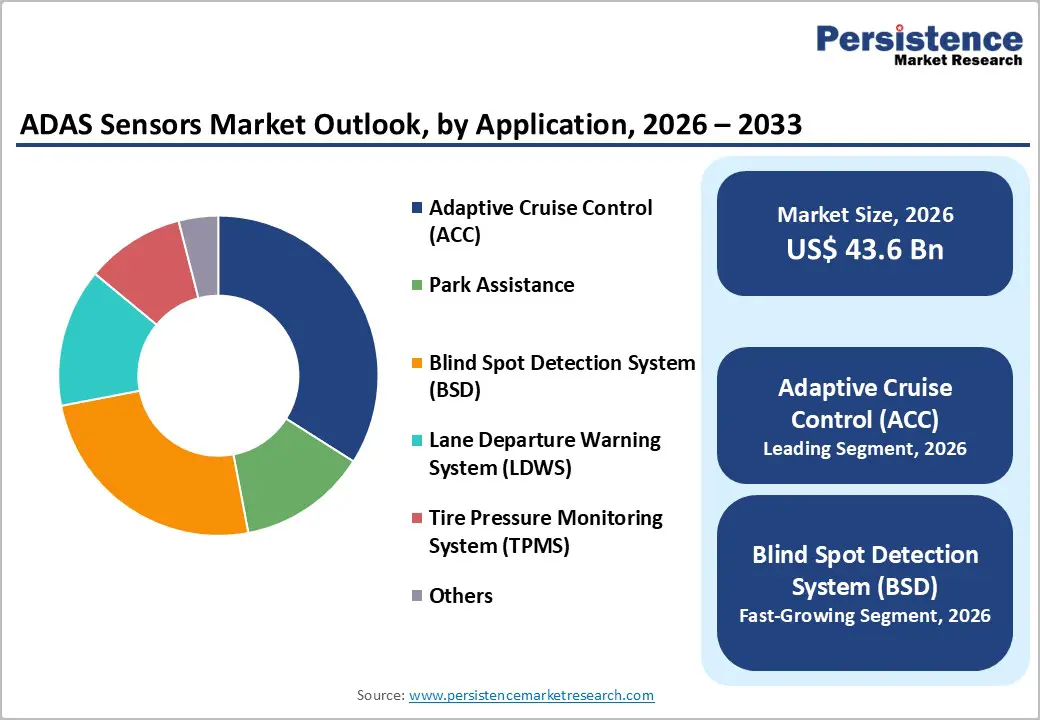

The global ADAS sensors market size is likely to be valued at US$43.6 billion in 2026 and is expected to reach US$97.6 billion by 2033, growing at a CAGR of 12.2% during the forecast period from 2026 to 2033, driven by increasing integration of camera, radar, LiDAR, ultrasonic, and infrared sensors across passenger and commercial vehicles.

A key growth catalyst is the enforcement of stringent vehicle safety regulations worldwide, mandating the adoption of (advanced driver assistance system) ADAS functions such as automatic emergency braking and lane departure warning. The rapid rise in electric vehicles and semi-autonomous driving is increasing sensor demand, as these platforms rely heavily on high-precision perception systems. Continuous advancements in AI-based sensor fusion, machine vision, and automotive semiconductors are enhancing detection accuracy, system reliability, and real-time decision-making, strengthening OEM confidence in large-scale deployment. The growing consumer awareness of vehicle safety, coupled with increasing urbanization and traffic density, is reinforcing the need for advanced driver assistance technologies.

Key Industry Highlights:

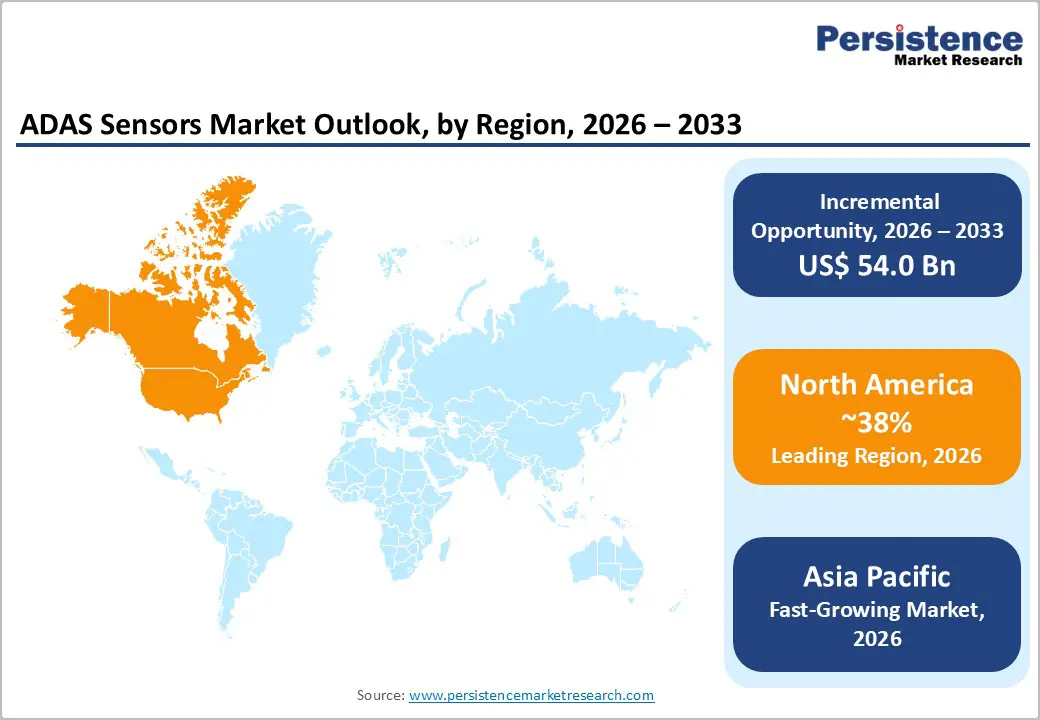

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by strong regulatory enforcement, high adoption of advanced safety features, rapid EV penetration, and the presence of leading automotive technology providers.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the ADAS sensors in 2026, supported by rapid vehicle production, expanding EV adoption, supportive safety regulations, and cost-efficient sensor manufacturing across key economies.

- Leading Application Type: Adaptive cruise control (ACC) is projected to represent the leading application type in 2026, accounting for 24% of the revenue share, driven by its widespread integration in modern vehicles.

- Leading Vehicle Segment: Passenger cars are anticipated to be the leading vehicle type, accounting for over 73% of the revenue share in 2026, supported by high safety feature adoption in urban and personal mobility segments.

| Key Insights | Details |

|---|---|

| ADAS Sensors Market Size (2026E) | US$43.6 Bn |

| Market Value Forecast (2033F) | US$97.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory Mandates and Safety Standards

Compelling automakers to integrate advanced sensing technologies as standard vehicle features. Governments and safety agencies across major automotive regions are tightening regulations to reduce road fatalities and enhance vehicle safety. Programs such as Euro NCAP in Europe, NHTSA in the U.S., C-NCAP in China, and Bharat NCAP in India increasingly reward or mandate systems such as automatic emergency braking (AEB), lane departure warning, adaptive cruise control, blind spot detection, and tire pressure monitoring. These regulations directly increase the per-vehicle sensor count, increasing demand for radar, camera, ultrasonic, and LiDAR sensors. Commercial vehicle regulations are also becoming stricter, with mandatory AEB, pedestrian detection, and blind-spot monitoring systems aimed at reducing accidents involving trucks and buses.

Harmonized safety standards and consumer safety ratings are reinforcing long-term ADAS (advanced driver assistance system) sensor adoption. Safety assessment frameworks increasingly tie higher safety scores to advanced driver assistance performance, pressuring automakers to exceed minimum regulatory requirements. Vision Zero road safety initiatives and urban mobility policies are driving the adoption of collision avoidance and driver monitoring systems. Regulatory focus is also expanding beyond physical safety to include functional safety, cybersecurity, and software reliability, particularly as vehicles move toward semi-autonomous operation. Standards addressing sensor redundancy, fail-operational performance, and secure data handling are increasing the complexity and value of ADAS sensor systems.

Environmental and Functional Limitations

Vision-based sensors such as cameras struggle in low-light, glare, fog, rain, and snow, affecting functions such as lane departure warning, traffic sign recognition, and pedestrian detection. LiDAR performance can degrade in heavy rain, dust, or snow due to signal scattering, while radar systems may face challenges such as multipath interference and reduced resolution in dense urban environments. These environmental constraints can lead to false alerts, delayed responses, or temporary system deactivation, negatively impacting driver confidence in ADAS features. In emerging markets, inconsistent road markings, poor lighting infrastructure, and mixed traffic conditions exacerbate these challenges. OEMs deploy multiple sensors and advanced redundancy architectures to ensure reliability, increasing system complexity and development costs.

Functional limitations also pose critical challenges for widespread ADAS sensor deployment. Sensor fusion systems require precise synchronization, calibration, and real-time data processing to deliver accurate situational awareness, making system integration complex and resource-intensive. Inaccurate calibration or sensor misalignment over time can degrade system performance, increasing maintenance requirements. Functional constraints such as limited detection range, latency issues, and difficulty distinguishing between static and dynamic objects can reduce system effectiveness, especially at higher vehicle speeds. ADAS systems often rely on high-quality maps and software updates, which may not be uniformly available across all regions. These functional challenges raise concerns among regulators and automakers regarding reliability and safety validation.

Technological Convergence and Retrofits

The integration of cameras, radar, LiDAR, ultrasonic sensors, AI algorithms, and sensor fusion software into unified architectures is enhancing perception accuracy while reducing overall system complexity. This convergence allows OEMs to replace multiple standalone systems with centralized ADAS domain controllers, lowering wiring, weight, and energy consumption an important advantage for electric vehicles. Advances in semiconductor technologies, edge AI, and automotive-grade processors are enabling real-time data processing and decision-making. Vehicles increasingly adopt software-defined architectures, and ADAS functionality can be upgraded via over-the-air updates, extending system life and improving performance without additional hardware changes.

Retrofit opportunities represent another high-growth avenue, particularly for the large fleet of vehicles not originally equipped with ADAS features. Fleet operators, logistics companies, and public transportation providers are increasingly adopting aftermarket ADAS sensor kits to enhance safety, reduce accident-related costs, and comply with evolving regulations. Retrofit solutions incorporating cameras, radar, and driver monitoring systems can be installed in existing vehicles with minimal structural modification. These systems are especially attractive for commercial fleets seeking blind spot detection, collision warning, and parking assistance functionalities. The growing insurance incentives and safety compliance requirements support retrofit adoption.

Category-wise Analysis

Application Type Insights

Adaptive cruise control (ACC) is expected to lead the ADAS sensors market, accounting for approximately 24% of revenue in 2026, driven by its growing role in enhancing driving comfort and active safety. ACC systems rely heavily on radar and camera sensors to maintain safe vehicle spacing, automatically adjusting speed in response to surrounding traffic conditions. Increasing regulatory emphasis on collision avoidance and speed management has accelerated ACC integration across passenger and commercial vehicles. Automakers are increasingly positioning adaptive cruise control (ACC) as a core element of broader ADAS packages, especially in mid-range and premium vehicles, to boost safety ratings and enhance consumer appeal. For instance, Bosch supplies radar-based ACC systems integrated across multiple OEM platforms, helping enable smoother traffic flow while meeting advanced safety requirements.

Blind spot detection (BSD) is likely to represent the fastest-growing segment in 2026, supported by rising urban traffic density and increasing emphasis on lane-change safety. BSD systems use radar and camera sensors to monitor areas not visible to drivers, issuing alerts during unsafe maneuvers. Growing awareness of side-collision risks and stronger safety rating incentives are encouraging OEMs to integrate BSD even in compact and mid-segment vehicles. Advancements in short-range radar and cost-efficient sensor modules have improved system accuracy while reducing implementation complexity. BSD is especially valuable in congested urban settings, where frequent lane changes and mixed traffic significantly increase accident risk. For example, Continental provides compact radar-based BSD solutions that are widely adopted by automakers to strengthen side-impact avoidance and overall driving safety.

Vehicle Insights

Passenger cars are projected to lead the market, capturing around 73% of the revenue share in 2026, supported by high consumer demand for safety, comfort, and convenience features. Urbanization, increasing traffic congestion, and heightened safety awareness have pushed automakers to integrate ADAS sensors as standard or bundled features in passenger vehicles, including compact and mid-size models. Camera, radar, and ultrasonic sensors are widely deployed to support applications such as lane assistance, adaptive cruise control, and parking assistance. Regulatory safety frameworks and consumer rating programs encourage OEMs to expand ADAS adoption in passenger vehicles to secure higher safety ratings and strengthen brand differentiation. For example, Toyota integrates a comprehensive suite of ADAS sensors across its passenger car lineup to improve occupant protection and comply with evolving safety standards.

Commercial vehicles are likely to be the fastest-growing vehicle segment in 2026, driven by increasing logistics activity and safety-focused fleet modernization. Fleet operators are prioritizing ADAS technologies to reduce accident risks, minimize downtime, and lower insurance costs. Sensors supporting blind spot detection, collision warning, and parking assistance are particularly critical for large vehicles operating in dense traffic and loading environments. Growth in e-commerce and last-mile delivery services is accelerating the adoption of ADAS sensors in light and heavy commercial vehicles. Growing regulatory pressure to enhance road safety for trucks and buses is pushing OEMs and fleet operators to invest in advanced sensing technologies. For example, ZF Friedrichshafen offers integrated ADAS sensor systems specifically designed to improve commercial vehicle safety and fleet operational efficiency.

Regional Insights

North America ADAS Sensors Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by strict safety regulations, high consumer awareness, and rapid adoption of advanced vehicle technologies. Regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) are mandating safety features, including automatic emergency braking, lane departure warning, and forward collision warning, which significantly increases the demand for cameras, radar, and ultrasonic sensors. The region also benefits from strong penetration of premium and electric vehicles, where ADAS features are positioned as standard offerings rather than optional upgrades. Rising concerns over road fatalities, coupled with insurance incentives for ADAS-equipped vehicles, support market expansion.

Technological innovation and close collaboration between OEMs and suppliers are shaping current market trends in North America. Automakers are increasingly deploying AI-driven sensor fusion to enhance detection accuracy and system robustness in complex driving scenarios. For example, Mobileye plays a significant role in the region by supplying vision-based ADAS solutions to multiple North American automakers, enabling functions such as lane keeping, collision avoidance, and driver monitoring. The growing emphasis on software-defined vehicles, cybersecurity compliance, and over-the-air updates is driving the ongoing evolution of the regional ADAS sensors market.

Europe ADAS Sensors Market Trends

Europe is likely to be a significant market for ADAS sensors in 2026, due to widespread adoption of advanced driver assistance technologies. European safety assessment programs such as Euro NCAP incentivize automakers to integrate more sophisticated sensor suites, including radar, cameras, LiDAR, and ultrasonic sensors, to achieve higher safety ratings. Governments and transportation authorities are also promoting initiatives such as Vision Zero, aimed at eliminating road fatalities and serious injuries, which reinforces the requirement for vehicles equipped with features such as automatic emergency braking, lane-keeping assist, and blind spot monitoring. Consumers in Europe are increasingly prioritizing safety and connectivity when purchasing vehicles, making ADAS an integral part of the value proposition.

Technological innovation and collaboration among OEMs and suppliers are key trends shaping the European ADAS sensors landscape. Companies are focusing on sensor fusion, the integration of data from multiple sensor types, to improve environmental perception and reduce false positives. For example, Valeo has developed integrated ADAS sensor platforms combining radar and camera technologies tailored for European driving conditions, enabling efficient lane detection, adaptive cruise control, and pedestrian recognition across varied terrains. With increasing demand for semi-autonomous features and electric vehicles, automakers are also adopting scalable sensor solutions that can support evolving automation levels.

Asia Pacific ADAS Sensors Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the ADAS sensors market in 2026, driven by automotive manufacturers integrating advanced safety systems to meet stringent regional safety regulations and rising consumer demand for smarter vehicles. Countries such as China and India are driving this growth through substantial vehicle production volumes and strong adoption of electrified and connected mobility solutions. China is driving demand for radar, camera, and LiDAR technologies. Regulatory emphasis on vehicle safety standards across Asia Pacific nations is compelling OEMs to equip new models with features such as adaptive cruise control, lane-keeping assist, and automatic emergency braking, increasing sensor uptake.

Technological innovation and strategic collaborations are key trends shaping the Asia Pacific ADAS sensors landscape, with regional players and suppliers investing in next-generation sensor solutions tailored for local requirements. For example, RoboSense, a leading Chinese LiDAR developer, has been actively advancing high-performance LiDAR sensors designed for integration into ADAS and autonomous driving systems, supporting improved perception capabilities across varying environmental conditions. This type of innovation is helping to reduce barriers such as cost and reliability, enabling wider adoption of LiDAR-enhanced ADAS in electric vehicles and higher-level driver assistance applications.

Competitive Landscape

The global ADAS sensors market exhibits a moderately fragmented structure, driven by a mix of established automotive component suppliers and emerging technology innovators competing on technology, integration capability, and geographic reach. Leveraging decades of automotive expertise and extensive R&D investments to advance radar, camera, LiDAR, and sensor-fusion solutions for adaptive cruise control, collision avoidance, and lane assistance systems. Larger players benefit from deep relationships with automakers, robust manufacturing capacity, and the ability to tailor sensor stacks for diverse vehicle segments, from economy models to premium electric and autonomous platforms.

Key industry leaders, including Mobileye, Valeo, Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, and Magna International Inc., collectively command a substantial share of the market. Competition among these players centers on continuous innovation, strategic partnerships, mergers and acquisitions, and co-development initiatives with OEMs, all of which accelerate improvements in sensor accuracy, reliability, and cost efficiency. For example, Mobileye has reinforced its market position by deploying advanced camera-based ADAS platforms and EyeQ processing chips across numerous vehicle programs, highlighting the growing role of proprietary software and perception algorithms in differentiating solutions.

Key Industry Developments:

- In October 2025, Aptiv launched its next-generation Gen 8 radar technology for ADAS, advancing automotive sensing capabilities. The radar portfolio supported AI- and machine learning–based ADAS functions, enabling reliable hands-free driving in complex urban environments while remaining cost-efficient. The Gen 8 lineup featured front-facing and corner radar units with enhanced 4D perception, a wider field of view, and improved object classification in varied weather and lighting conditions. It also supported Aptiv’s new PULSE Sensor, which fused radar and camera data to improve near-field perception and replace multiple ultrasonic sensors, reducing system complexity for automakers.

- In September 2025, Qualcomm and Valeo expanded their long-standing partnership to accelerate the transition to software-defined vehicles. They delivered scalable, safety-focused ADAS and automated driving solutions by combining Qualcomm’s Snapdragon Ride™ SoCs and ADAS/AD software with Valeo’s sensors, ECUs, parking algorithms, and system integration expertise. The pre-integrated platform shortened implementation time for automakers and supported configurations ranging from entry-level systems to high-performance centralized computing, enabling the integration of ADAS and infotainment on a single SoC.

Companies Covered in ADAS Sensors Market

- BorgWarner

- Continental

- Gentex

- HELLA

- Magna

- Mobileye

- Renesas Electronics

- Bosch

- VALEO

- Friedrichshafen

Frequently Asked Questions

The global ADAS sensors market is projected to reach US$43.6 billion in 2026.

Stringent vehicle safety regulations, rising demand for advanced driver assistance features, and growing adoption of electric and autonomous vehicles.

The ADAS sensors market is expected to grow at a CAGR of 12.2% from 2026 to 2033.

Technological convergence, AI-based sensor fusion, retrofitting existing vehicles, and expanding adoption in electric and autonomous vehicles.

BorgWarner, Continental, Gentex, HELLA, Magna, Mobileye, Renesas Electronics, and Bosch are the leading players.