- Industrial Machinery

- Hydraulic Gear Pumps Market

Hydraulic Gear Pumps Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Hydraulic Gear Pumps Market by Product Type (External Gear Pump and Internal Gear Pump), Operating Pressure (Up to 15 bar, 15-50 bar, 50-150 bar, 150-250 bar, 250-300 bar, and More than 300 bar), End-user (Semiconductors, Mining Equipment, Automotive, Processing Industry, and Others), Regional Analysis from 2025 to 2032

Hydraulic Gear Pumps Market Size and Share Analysis

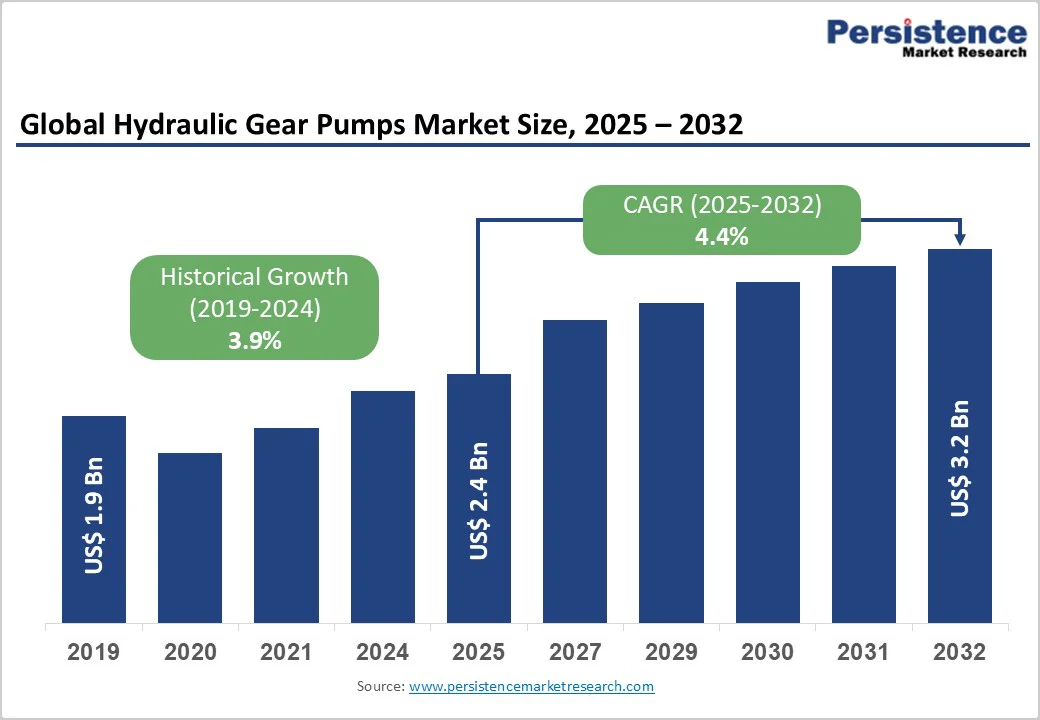

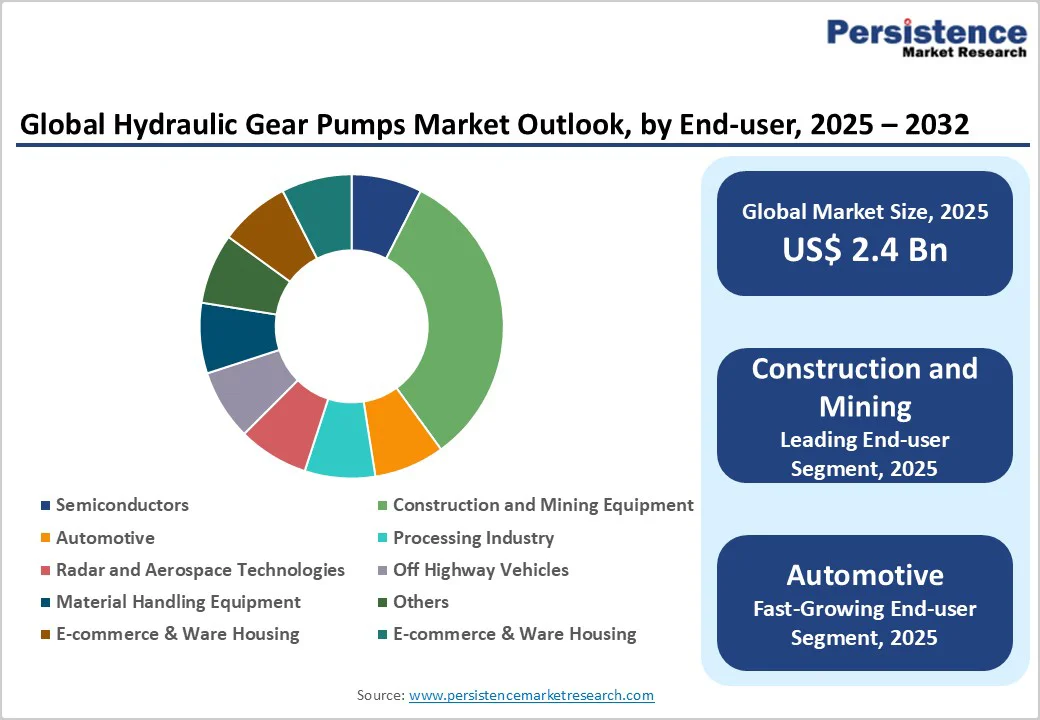

The global hydraulic gear pumps market size is valued at US$2.4 billion in 2025 and is projected to reach US$3.2 billion, growing at a CAGR of 4.4% between 2025 and 2032.

Robust global infrastructure development and accelerating mechanization across construction, mining, and agricultural sectors are driving the growth of the hydraulic gear pumps market.

Industrial automation initiatives, particularly in developed economies, coupled with increasing adoption of advanced hydraulic technologies for energy efficiency and reduced environmental impact, are propelling sustained demand.

Key Market Highlights:

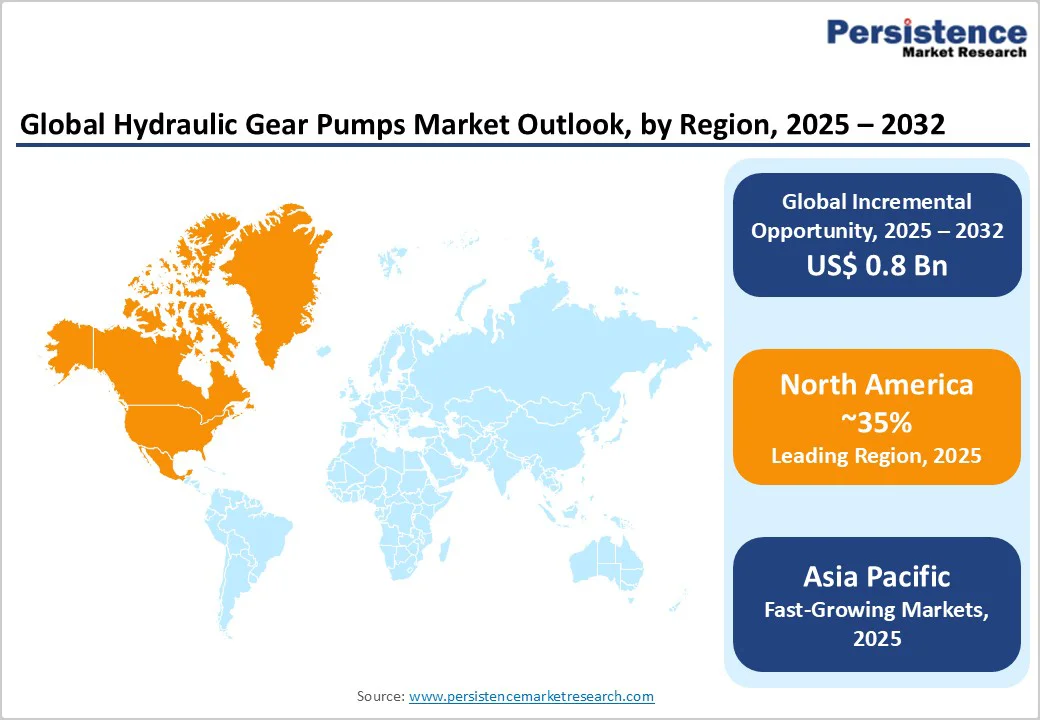

- Leading Region: North America dominates the hydraulic gear pump market, maintaining leadership through advanced industrial infrastructure and a strong presence in construction and oil and gas sectors.

- Fastest Growing Region: Asia Pacific demonstrates the fastest growth trajectory, driven by rapid industrialization, massive infrastructure investments, and accelerating construction equipment demand.

- Dominant Product Type: External gear pumps hold the largest market share, accounting for approximately 58% of the total hydraulic gear pump market, driven by their simple design, cost-effectiveness, high volumetric efficiency, and widespread industrial standardization across construction and manufacturing equipment.

- Fastest Growing Industry: Automotive represents the fastest-growing end-use segment, amid battery assembly, thermal management, and electrified drivetrain hydraulic requirements across automotive production facilities.

- Key Market Opportunity: Smart hydraulic systems integration with Industry 4.0 manufacturing frameworks creates a significant growth opportunity, with embedded sensors, predictive maintenance capabilities, and real-time monitoring features commanding premium pricing and driving digital transformation adoption across industrial sectors.

| Key Insights | Details |

|---|---|

| Hydraulic Gear Pumps Market Size (2025E) | US$2.4 Bn |

| Market Value Forecast (2032F) | US$3.2 Bn |

| Projected Growth CAGR (2025 - 2032) | 4.4% |

| Historical Market Growth (2019 - 2024) | 3.9% |

Market Dynamics

Drivers - Expanding Construction and Infrastructure Development Propel Market Growth

The booming global construction industry stands as a primary driver of the hydraulic gear pumps market. Hydraulic gear pumps play a vital role in a wide range of construction machinery, including excavators, bulldozers, loaders, cranes, and concrete pumps, by converting mechanical energy into hydraulic power for precise lifting, steering, and movement operations.

As governments and the private sector worldwide increase investments in infrastructure projects such as roads, bridges, residential complexes, and commercial buildings, demand for construction equipment has grown substantially.

According to Oxford Economics, global construction output is expected to reach USD 15.5 trillion by 2030, with Asia Pacific, North America, and Europe accounting for more than 75% of total activity. This surge directly translates into higher consumption of hydraulic gear pumps, as they are integral components in almost every piece of heavy machinery used on construction sites.

The growing adoption of smart and automated construction machinery is further boosting market demand. Equipment manufacturers are increasingly integrating advanced hydraulic gear pumps that deliver improved efficiency, reduced noise, and enhanced load-handling capacity.

The development of energy-efficient and environmentally friendly hydraulic systems aligns with the industry’s shift toward sustainability and reduced carbon emissions. The rising pace of construction activities globally continues to fuel strong growth momentum for the hydraulic gear pumps market.

Agricultural Mechanization and Renewable Energy Expansion Boost Hydraulic Gear Pump Sales

The agricultural sector is experiencing accelerating mechanization through the adoption of advanced farming equipment powered by hydraulic systems, particularly in developing Asian economies, where agrarian modernization is a government priority.

France, as a leading European agricultural producer accounting for over 15% of regional production, received US$2.45 billion in investments to accelerate agricultural and food production innovation. Simultaneously, renewable energy applications, including wind power generation and hydroelectric installations, require high-performance hydraulic systems for turbine controls, lubrication, and pressure management operations.

The U.S. Energy Information Administration forecast that renewable energy sources would generate 16% of total energy by 2023, up from 14% in 2022, underscoring sustained demand for hydraulic pumps across global energy infrastructure development initiatives.

Restraints - Raw Material Price Volatility and Supply Chain Disruption Hamper Market Growth

Hydraulic gear pump manufacturing relies on specialty steel alloys, aluminum, and cast iron, which are subject to significant commodity price fluctuations, directly impacting production costs and manufacturer profit margins. Geopolitical tensions, including international trade disputes and tariff implementations, create supply chain uncertainty affecting component sourcing and manufacturing timelines.

Additionally, regulatory compliance requirements for environmental protection and emissions standards necessitate continuous manufacturing process modifications, increasing operational complexity and capital expenditure requirements for equipment manufacturers seeking compliance certification.

Competition from Alternative Hydraulic Technologies to Limit Market Growth

Emerging pump technologies, including variable-displacement pumps and electric-driven hydraulic systems, directly compete with conventional gear pump designs in certain applications, particularly in efficiency-focused operations where energy consumption is a critical performance metric.

Industrial electrification trends accelerate substitution risks in specific sectors, while noise-reduction requirements drive manufacturers toward alternative pump geometries that offer quieter operation at premium price points.

Opportunity - Smart Hydraulic Systems Integration and Industry 4.0 Adoption Presents Opportunity

Industry 4.0 manufacturing initiatives create substantial market opportunities for advanced hydraulic systems that incorporate embedded sensors, real-time monitoring, and predictive maintenance algorithms. Leading manufacturers, including Bosch Rexroth and Parker Hannifin, increasingly embed IoT-enabled diagnostics, pressure sensors, and flow measurement devices enabling seamless integration into smart manufacturing environments.

Germany's Industrie 4.0 framework actively promotes automation adoption, with Germany Trade & Invest reporting US$35 billion in foreign direct investment in May 2024, specifically targeting advanced manufacturing infrastructure.

These digital integration capabilities enable manufacturers to optimize operational efficiency, reduce maintenance costs through predictive failure detection, and improve uptime performance across industrial applications, generating premium pricing opportunities for technologically advanced hydraulic gear pump solutions.

Electric Vehicle Manufacturing and Aerospace Defense Expansion

Electric vehicle production expansion is driving demand for hydraulic systems in battery assembly, thermal management, and manufacturing automation applications, with emerging opportunities across ASEAN regions where vehicle production is rapidly growing.

The aerospace and defense sectors require specialized, high-performance hydraulic pumps for aircraft landing gear systems, flight control mechanisms, and military equipment, commanding premium pricing and sustained demand through defense budget allocations.

France's aerospace sector benefits from significant investment in aircraft systems, creating specialized demand for tailored hydraulic solutions. The convergence of electrification trends and aerospace modernization creates differentiated market segments where hydraulic gear pump manufacturers can command pricing premiums while developing specialized product variants addressing unique application requirements.

Category-wise Insights

Product Type Analysis

External gear pumps represent the dominant product segment, commanding approximately 58% market share within the hydraulic gear pump market. These pumps feature straightforward design configurations with two meshing external gears housed within a pump body, delivering exceptional volumetric efficiency ranging from 85-95% depending on operating pressure and viscosity conditions.

External gear pump design simplicity facilitates cost-effective manufacturing, wide availability of replacement components, and established service infrastructure across global markets.

Their proven reliability across diverse industrial applications, combined with robust performance across pressure ranges from 15 bar to 300 bar operating conditions, supports market leadership positioning. Industries ranging from construction equipment to agricultural machinery standardly specify external gear pumps due to established interchangeability standards and extensive historical performance documentation.

End-User Analysis

Mining equipment sectors represent the largest end-use segment, capturing approximately 35% market share through sustained demand for hydraulic systems powering heavy construction machinery and underground mining operations.

Construction equipment manufacturers, including excavators, loaders, and cranes, collectively represent the largest hydraulic pump consumer segment globally, with each major equipment platform incorporating multiple hydraulic systems across lift mechanisms, implement controls, and steering functions.

Mining operations require robust hydraulic systems capable of withstanding harsh operating environments, vibration, and contaminated fluids characteristic of underground extraction. Global construction activity expansion, particularly across Asia Pacific infrastructure projects and emerging market infrastructure development, drives sustained capital equipment investment and pump replacement demand across these end-use industries.

Operating Pressure Analysis

The 50-150 bar operating pressure range represents the dominant pressure segment, accounting for approximately 42% of the share across industrial hydraulic pump applications. This pressure classification encompasses standard industrial machinery, construction equipment, and general-purpose hydraulic systems where 100 bar nominal operating pressure represents the industry standard for volumetric pump sizing and component selection.

Pumps operating within this pressure band deliver an optimal balance between performance capability, component reliability, and manufacturing cost efficiency, supporting widespread adoption across diverse industrial sectors.

Applications ranging from loader bucket control systems to agricultural equipment hydraulic functions typically specify pumps rated for continuous operation at 50-150 bar, with peak pressure ratings extended to 180-210 bar for emergency load conditions, making this pressure classification the foundation of modern hydraulic system design practices.

Regional Insights

North America Hydraulic Gear Pumps Trends

North America maintains market leadership positioning through advanced industrial infrastructure, a strong presence of construction, automotive, and oil and gas sectors. The region's thriving construction industry, encompassing residential, commercial, and industrial development, drives continuous demand for excavators, loaders, cranes, and bulldozers dependent upon hydraulic systems.

The U.S. oil and gas industry, particularly in upstream and downstream operations, represents a critical pump consumer segment that requires specialized equipment for drilling, fluid handling, and pressure management applications.

The region's well-established regulatory framework, encouraging energy-efficient and sustainable solutions, promotes the adoption of advanced hydraulic technologies with enhanced performance characteristics.

Leading manufacturers, including Eaton Corporation Plc, Parker Hannifin Corp, and Roper Pump Company, maintain extensive research and development operations and manufacturing facilities across North America, driving continuous product innovation and supporting strong regional market presence through established distribution networks and technical service infrastructure.

Europe Hydraulic Gear Pumps Trends

Europe represents a mature, sophisticated market with substantial demand from construction, mining, agriculture, and automotive manufacturing sectors. Germany leads European market activity, capturing 52.7% of total European sold production value in 2023, according to Eurostat data, reflecting the country's industrial heritage and manufacturing leadership.

Italy ranks second with 35.0% market share, demonstrating strength in specialized hydraulic equipment production. The region prioritizes environmental sustainability through stringent emissions standards, driving adoption of energy-efficient hydraulic systems aligned with European Green Deal sustainability objectives and industrial decarbonization targets.

France's aerospace sector investment and Spain's manufacturing expansion create specialized opportunities for tailored hydraulic solutions across diverse end-user industries. Industry 4.0 integration, particularly evident across Germany's manufacturing ecosystem, accelerates the adoption of smart hydraulic pumps with embedded sensors and predictive maintenance capabilities, supporting premium product positioning for technologically advanced manufacturers.

Asia Pacific Hydraulic Gear Pumps Trends

Asia Pacific emerges as the fastest-growing regional market, driven by rapid industrialization, urbanization, and massive infrastructure investment commitments. China dominates regional activity with 37.9% market share, leveraging its substantial manufacturing capacity and industrial base centered on construction, mining, and petrochemical operations.

The nation's construction sector demonstrates sustained expansion, supported by government infrastructure modernization initiatives, including high-speed rail development, urban transit systems, and industrial facility expansion.

India's infrastructure development initiatives, including the Pradhan Mantri Awas Yojana (Housing for All) program, drive construction equipment demand, while agricultural mechanization represents accelerating growth opportunities across rural farming regions.

ASEAN countries including Indonesia, Thailand, and Vietnam demonstrate emerging market potential through vehicle production expansion, with global vehicle production reaching approximately 91.7 million units in 2019, supporting sustained demand for automotive hydraulic systems incorporating multiple pump specifications.

Regional manufacturers increasingly invest in localized production capacity, reducing reliance on imports while capturing growing market share through competitive pricing and accelerated product delivery.

Competitive Landscape

The hydraulic gear pump market exhibits moderate consolidation characteristics with global market leaders controlling significant but not dominant shares across diverse end-market segments. Leading manufacturers including Bosch Rexroth AG, Parker Hannifin Corp, and Eaton Corporation Plc compete through comprehensive product portfolios, advanced technology integration, and established global distribution infrastructure.

Differentiation strategies emphasize energy efficiency improvements, noise reduction capabilities, and digital integration features supporting Industry 4.0 adoption. Niche competitors target specialized applications including aerospace, pharmaceuticals, and renewable energy sectors, commanding premium pricing through specialized engineering expertise and application-specific certifications.

Key Market Developments:

- In June 2024, Shimadzu Corporation launches environment-friendly MLP2 Series high-pressure gear pump succeeding SGP2 Series, increasing rated pressure from 24.5 MPa to 25 MPa while eliminating plating processes to improve durability.

- In February 2024, Bosch Rexroth introduces external gear pump series equipped with digital monitoring interfaces enabling seamless Industry 4.0 integration for real-time performance tracking and predictive maintenance capabilities.

- In April 2024, CASAPPA S.p.A. launches aluminum gear pump series tailored for electric vehicles and hybrid machinery supporting automotive electrification trends in industrial equipment.

Companies Covered in Hydraulic Gear Pumps Market

- Eaton Corporation Plc

- Parker Hannifin Corp

- Bucher Hydraulics GmbH,

- KYB Corporation

- Bosch Rexroth AG

- CASAPPA S.p.A.

- Dynamatic Technologies Ltd.

- Linde Hydraulics GmbH & Co. KG

- Roper Pump Company

- Kawasaki Heavy Industries Ltd.

Frequently Asked Questions

The global hydraulic gear pump market was valued at US$ 2.4 billion in 2025 and is projected to reach US$ 3.2 billion by 2032, representing a CAGR of 4.4% during the forecast period.

Primary demand drivers include global infrastructure expansion, accelerating agricultural mechanization across emerging markets, expanding oil and gas operations, renewable energy infrastructure development, and industrial automation adoption supporting Industry 4.0 manufacturing initiatives requiring advanced hydraulic power transmission systems.

External gear pumps command the dominant market segment with approximately 58% market share, driven by straightforward design architecture, high volumetric efficiency ranging from 85-95%, cost-effective manufacturing characteristics, and widespread industrial standardization.

North America maintains market leadership through advanced industrial infrastructure, strong construction and oil and gas sector presence.

Smart hydraulic systems integration with embedded sensors, predictive maintenance algorithms, and real-time monitoring capabilities aligned with Industry 4.0 manufacturing frameworks represents the highest-growth opportunity segment.

Market leaders include Bosch Rexroth AG (Germany), Parker Hannifin Corp (United States), Eaton Corporation Plc (United States), alongside regional specialists including CASAPPA S.p.A. (Italy) and Bucher Hydraulics (Switzerland) serving diverse industrial segments.