- HVAC

- Heat Pump Market

Heat Pump Market Size, Share, and Growth Forecast 2025 - 2032

Heat Pump Market Analysis By Technology (Air Sources, Water, Source, Geothermal), Capacity (Upto 10kW, 10-20 kW, Above 20kW), Refrigerant (R410A, R744, R290, R-1234yf), Application and Regional Analysis 2025 - 2032

Heat Pump Market Share and Trends Analysis

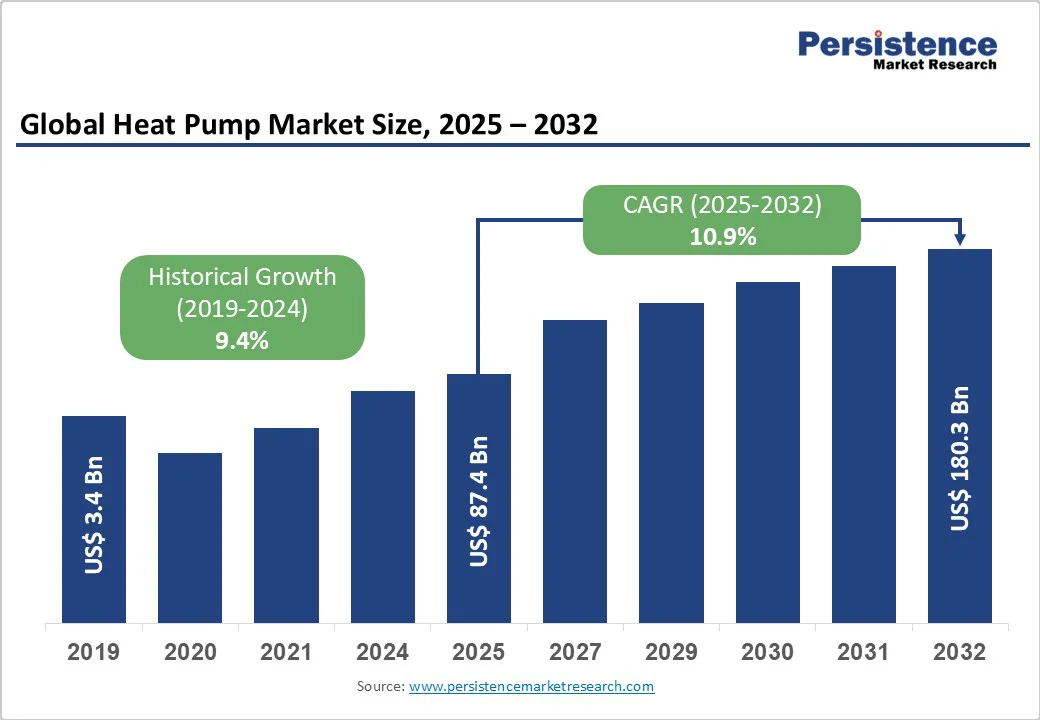

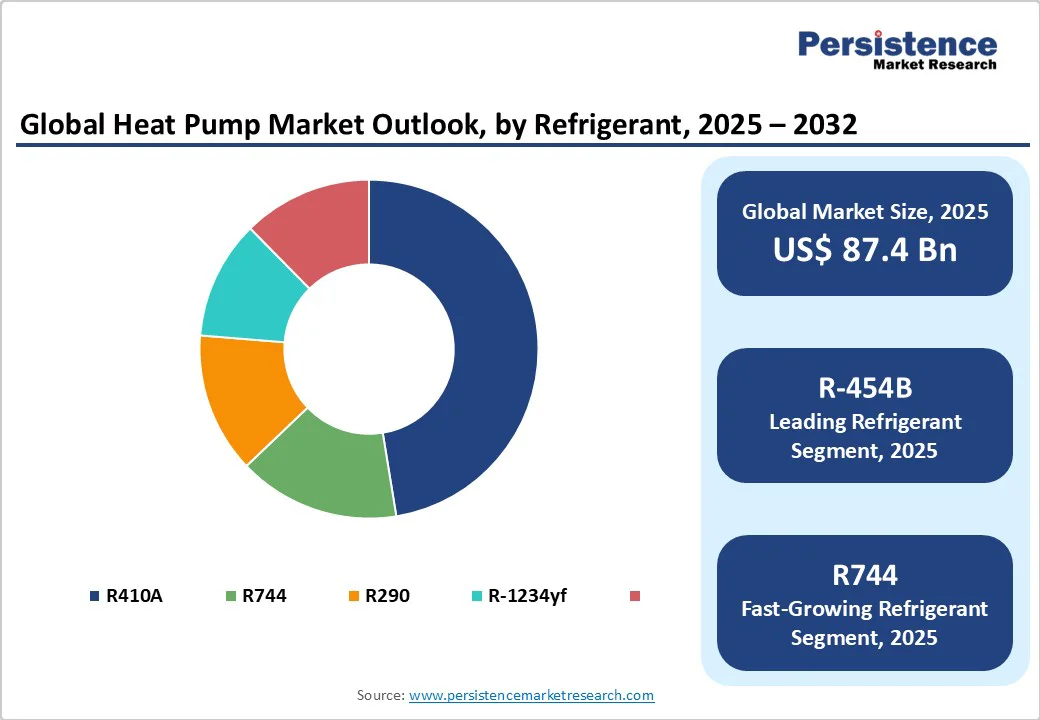

The global heat pump market size is likely to be valued at US$87.4 Bn in 2025 and is projected to reach US$180.3 Bn by 2032, growing at a CAGR of 10.9% between 2025 and 2032.

The heat pump industry is experiencing unprecedented growth, driven by increasing global decarbonization initiatives, rising energy costs, and stringent government regulations that promote renewable energy technologies.

Energy efficiency mandates and carbon reduction targets are compelling industries and households to transition from fossil fuel-based heating systems to electric heat pump solutions that deliver superior coefficient of performance (COP) ratings.

Key Market highlights:

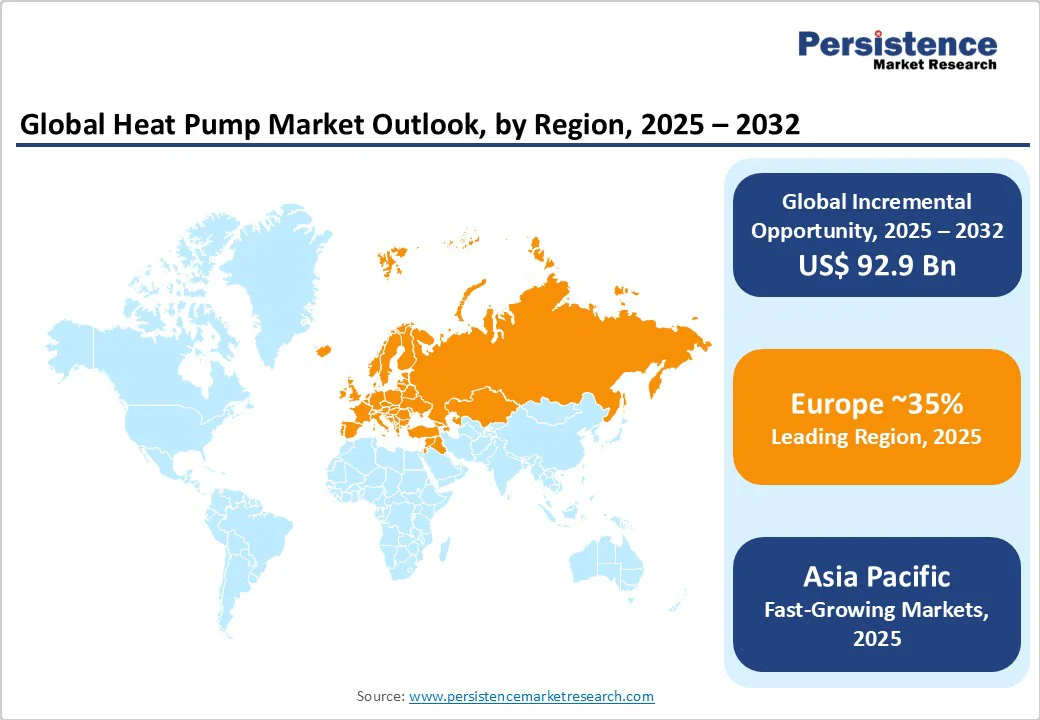

- Leading region: Europe dominates the global heat pump market, boasting the most mature infrastructure, comprehensive policy frameworks, and over 10 million installation targets by 2027 under the REPowerEU initiatives.

- Fastest Growing Region: Asia Pacific demonstrates the highest growth potential with 48% market share and 11.0% CAGR, driven by China's decarbonization commitments and industrial electrification.

- Dominant Technology Segment: Air source technology commands approximately 80% market share through superior accessibility, installation flexibility, and cost-effectiveness across residential and commercial applications.

- Fastest Growing Refrigerant Segment: R454B refrigerant achieves 16.7% CAGR as the fastest-growing segment, driven by 466 GWP rating and environmental compliance advantages over traditional refrigerants.

- Key Market Opportunity: Smart technology integration and IoT connectivity enable demand response services, predictive maintenance, and renewable energy optimization, creating new revenue streams and operational efficiencies.

| Key Insights | Details |

|---|---|

| Heat Pump Market Size (2025E) | US$87.4 Billion |

| Market Value Forecast (2032F) | US$180.3 Billion |

| Projected Growth CAGR(2025-2032) | 10.9% |

| Historical Market Growth (2019-2024) | 9.4% |

Market Dynamics

Drivers - Government Regulations and Decarbonization Initiatives Drive Market Expansion

Government regulations and policy frameworks are serving as primary catalysts for the global growth of the heat pump market. The European Union's REPowerEU plan aims to install 10 million heat pumps by 2027, while the United States Inflation Reduction Act provides 30% tax credits up to $2,000 for qualified heat pump installations.

Germany's BEG subsidies cover up to 70% of installation costs for residential buildings, with maximum subsidies reaching €21,000 for air-to-water heat pumps. The Kigali Amendment to the Montreal Protocol mandates an 80-85% phase-down of high-GWP hydrofluorocarbons over the next two decades, creating regulatory pressure for low-GWP alternatives, such as heat pumps.

Building codes in numerous jurisdictions now require or incentivize the installation of heat pumps, with countries such as Norway, Denmark, and the Netherlands implementing bans on gas and oil boilers in new constructions.

Rising Energy Costs and Energy Efficiency Requirements Fuel Adoption

Escalating energy costs and stringent energy efficiency standards are driving the adoption of heat pumps across residential, commercial, and industrial sectors. Traditional heating systems face increasing operational costs as natural gas and oil prices fluctuate. At the same time, heat pumps deliver coefficient of performance (COP) ratings exceeding 4.0, making them 300-400% more efficient than conventional electric resistance heating.

The International Energy Agency reports that heat pump sales rose by 15% overall in the United States in 2025, with a 30% jump in the second half of the year. Industrial applications are particularly driving demand, as manufacturers seek process heating solutions that can deliver temperatures exceeding 100°C while reducing operational costs by 20-30% compared to fossil fuel boilers.

Smart heat pump integration with IoT and automation systems enables 25% of new installations to feature remote control and energy monitoring capabilities, optimizing energy consumption and operational efficiency.

Market Restraint- High Initial Installation Costs Limit Market Penetration

The relatively high upfront investment required for heat pump systems represents a significant barrier to widespread adoption, particularly in price-sensitive markets and developing economies. Cold climate air source heat pumps typically cost $15,000 to $ 25,000 for residential installations, which is significantly higher than the cost of conventional gas or electric heating systems.

High-efficiency cold-climate heat pumps command premium pricing over minimum-efficiency models. At the same time, system compatibility requirements often necessitate additional infrastructure investments, including electrical panel upgrades, ductwork modifications, and hydronic system retrofits.

Limited production capacity and supply chain constraints have led to price volatility, particularly for advanced refrigerants like R454B, where demand has exceeded manufacturing expectations. Installation complexity requires specialized technician training, creating additional labor costs and limiting contractor availability in certain regions.

Cold Climate Performance Limitations and Infrastructure Challenges

Heat pump performance degradation in extremely cold climates continues to restrict market penetration in northern regions, despite technological improvements in cold climate air source heat pump (CCASHP) designs. Systems experience reduced efficiency and heating capacity at ambient temperatures below -15°C to -20°C, necessitating the use of backup heating elements that increase energy consumption and operational costs.

Grid modernization requirements to support electrification present infrastructure challenges, particularly in regions with aging electrical distribution systems that are inadequate for widespread heat pump adoption.

Limited consumer awareness and education about heat pump technology, maintenance requirements, and long-term benefits hinder adoption rates in markets where traditional heating methods are predominant. Skilled technician shortages for installation, commissioning, and maintenance services create bottlenecks in market expansion, particularly in rapidly growing segments.

Market Opportunities

Smart Technology Integration and IoT Connectivity Present Growth Potential

The integration of smart technologies and Internet of Things (IoT) capabilities in heat pump systems represents a transformative growth opportunity for market participants. Connected heat pumps enable advanced demand response services, allowing systems to optimize electricity consumption based on real-time pricing signals and grid conditions. PreHEAT heat pump controllers demonstrate energy cost reductions through model predictive control (MPC) algorithms.

Predictive maintenance capabilities, utilizing advanced data analytics and grey box modeling, can reduce operational costs and extend system lifespans. Integrating these capabilities with renewable energy systems, such as solar photovoltaic and energy storage, maximizes self-consumption rates and enhances grid independence.

Smart heat pump technologies enable participation in aggregator-based services for electricity markets, creating revenue streams for building owners through flexibility provision and grid stabilization services. The development of hybrid renewable energy applications, combining heat pumps with solar thermal systems, geothermal energy, and biomass, creates comprehensive energy solutions for both residential and industrial applications.

Industrial Decarbonization and High-Temperature Applications Drive Market Expansion

Industrial sector decarbonization initiatives present substantial growth opportunities for high-temperature heat pump systems capable of delivering process heating above 100°C for manufacturing applications. The heavy-duty heat pump market is projected to grow from USD 3.5 billion in 2025 to USD 5.4 billion by 2035 at a 4.3% CAGR, driven by industrial electrification and clean energy mandates.

High-temperature heat Pump Market applications in food processing, chemical manufacturing, and metal treatment require specialized systems operating at temperatures exceeding 150°C, creating opportunities for technology providers developing ammonia and CO2-based natural refrigerant solutions.

District heating applications represent significant expansion potential, particularly in Northern Europe and East Asia, where existing hydronic infrastructure can be retrofitted with heat pump systems. The convergence of the Personal Cooling Device Market and the Portable Air Conditioner Market with heat pump technology creates opportunities for integrated heating and cooling solutions in residential and commercial applications. Meanwhile, the growth of the Hydrofluoroolefin Market supports the adoption of next-generation refrigerants in advanced heat pump systems.

Category-wise Insights

Technology Analysis

Air Source technology dominates the global heat pump market, accounting for nearly 80% of the share in 2025, and establishing its position as the leading segment due to its superior accessibility, installation flexibility, and cost-effectiveness compared to alternative technologies. Air source heat pumps extract thermal energy from ambient air using advanced inverter-driven compressor technology and variable refrigerant flow systems, enabling efficient operation across diverse climate conditions.

The water source heat pump segment is emerging as the fastest-growing category, fueled by expanding adoption in district heating, commercial buildings, and industrial energy recovery projects. Water source systems achieve superior efficiency and reliability by stabilizing the water temperature, thereby minimizing energy consumption. Their increasing integration into sustainable building designs, green infrastructure initiatives, and hybrid geothermal-water systems is accelerating global deployment.

Capacity Analysis

Up to 10 kW capacity systems command the largest market share at approximately 45%, serving primarily residential applications where smaller heating loads and space constraints require compact, efficient solutions. This segment addresses the core residential market, including single-family homes, apartments, and townhouses, where heating and cooling demands typically range from 3 to 8 kW, depending on building size and insulation characteristics. The 10-20 kW segment serves both residential and commercial applications, providing versatile solutions for medium-sized buildings, office spaces, and small commercial establishments with moderate heating loads.

Above 20 kW systems target industrial and large commercial applications that require higher heating capacities for process heating, as well as large office buildings, hotels, and manufacturing facilities. Demand across all capacity segments is expected to grow significantly as continuous advancements in compressor and heat exchanger technology enhance performance and reliability. The segment's dominance reflects the concentration of residential heating demand globally, supported by government rebates and tax credits that specifically target residential energy-efficient system installations.

Refrigerant Analysis

R410A maintains a leading position in the heat pump refrigerant market, although its dominance is declining due to environmental regulations targeting high-global-warming-potential (GWP) substances. R454B emerges as the fastest-growing segment with an impressive 16.7% CAGR, driven by its low Global Warming Potential (GWP) of 466 compared to R410A's GWP of 2,088. R454B refrigerant offers 78% lower CO2 emissions than R410A and 31% lower than R32, making it an environmentally preferred alternative for air conditioning systems, heat pumps, and chillers.

Industrial applications of R410A heat pumps are prevalent across the food processing, pharmaceutical, and manufacturing sectors, where precise temperature control is crucial for process efficiency and regulatory compliance. The R454B segment benefits from nearly identical performance to R410A with no need for equipment redesign, enabling straightforward retrofitting and new installations. R32 and R290 natural refrigerants are gaining traction in specific applications, while R744 (CO2) systems are finding adoption in commercial and industrial applications that require high-temperature operation and environmental sustainability.

Application Analysis

Residential applications dominate the heat pump market, with an approximate 72% share, reflecting substantial global demand for domestic heating, cooling, and hot water solutions. The residential segment encompasses single-family homes, multi-family housing, apartments, and condominiums where heat pumps replace traditional gas furnaces, oil boilers, and electric resistance heating systems. Rising energy costs and increasing consumer awareness of energy efficiency drive residential adoption, with heat pumps offering cost-effective, sustainable solutions for year-round comfort control.

Government incentives and rebates specifically target residential installations, with programs like the US federal tax credits providing 30% cost offsets up to $2,000. Smart home integration and remote monitoring capabilities enhance consumer appeal, while improved cold climate performance expands market penetration in northern regions. The segment benefits from retrofitting opportunities in existing buildings and the mandatory adoption of energy-efficient solutions in new construction under building energy codes, creating sustained demand growth across both mature and emerging markets.

Regional Insights

North America Heat Pump Trends Insights

North America represents a rapidly evolving heat pump market driven by federal and state-level decarbonization policies, with the United States demonstrating 15% overall sales growth in 2025 and a 30% surge in the second half of the year.

The Inflation Reduction Act provides substantial financial incentives, including 30% tax credits up to $2,000 for air source heat pumps and 100% rebates up to $8,000 for low-to-moderate income households, creating unprecedented market accessibility.

Cold climate heat pump technology advancement enables deployment in northern regions previously served by gas or oil furnaces, with manufacturers such as Rheem completing the DOE Cold Climate Heat Pump Challenge at -22.9°F (-30.5°C). State-level policies, including building electrification mandates in California, New York, and Washington, accelerate adoption, while utility rebate programs offer additional financial incentives.

Canada's heat pump market focuses on cold climate applications and renewable energy integration to meet federal net-zero by 2050 commitments. The Canadian federal government offers the Greener Homes Grant program, providing up to CAD $5,000 for heat pump installations, complemented by provincial incentives in British Columbia, Ontario, and Quebec.

Manufacturing investments by companies like Daikin include California production commitments to produce one million heat pumps by 2030, supporting domestic supply chain development. The region's green building codes and LEED certification requirements increasingly favor heat pump installations in commercial and institutional projects.

Europe Heat Pump Trends Insights

Europe leads global heat pump adoption with the most mature market infrastructure and aggressive policy frameworks supporting decarbonization targets. The European Union's REPowerEU plan targets 10 million heat pump installations by 2027 as part of energy independence and climate strategies, while the European Green Deal establishes comprehensive regulatory frameworks promoting electrification.

Germany dominates European installations with BEG subsidy programs covering up to 70% of installation costs and maximum grants reaching €21,000 for air-to-water systems, contributing to over 500,000 new installations expected in 2025. Nordic countries demonstrate the highest heat pump penetration rates globally, with Sweden achieving approximately 437 heat pumps per 1,000 households and Norway implementing comprehensive fossil fuel heating bans.

France, Netherlands, and United Kingdom implement similar decarbonization policies, including fossil fuel boiler phase-out schedules and building emission standards requiring heat pump installations in new construction and major renovations.

Daikin strategic acquisitions including BKF Klima in Denmark and Kylslaget in Sweden demonstrate industry consolidation and service network expansion across Scandinavian markets. Air-to-water heat pump systems dominate European installations due to compatibility with existing radiator and hydronic heating infrastructure, while hybrid systems combining heat pumps with gas boilers gain popularity in Italy and other transitional markets.

Asia Pacific Heat Pump Trends

Asia Pacific emerges as the fastest-growing heat pump region with over 49% share in 2025, driven by rapid urbanization and industrial development. China leads regional growth with a positive CAGR, supported by national carbon neutrality by 2060 commitments and comprehensive decarbonization mandates across residential and industrial sectors.

Japan is likely to demonstrate a leading CAGR through 2035 with advanced technology adoption, including the Ene-Farm program, integrating heat pumps with hydrogen energy systems, and government Green Innovation Fund subsidies for industrial applications. South Korea focuses on semiconductor and chemical sector applications through the Korean New Deal and Green Growth Strategy policies incentivize industrial electrification.

India represents a major emerging opportunity with heat pump market growth at 10.44% CAGR from 2021-2024 and projected expansion to USD 4.17 billion by 2030. Manufacturing advantages and cost competitiveness position the Asia Pacific as a global heat pump production hub, with companies such as Midea Group and regional manufacturers expanding capacity to serve domestic and export markets. The Hydrofluoroolefin Market growth supports advanced refrigerant adoption across the region.

Competitive Landscape

The global heat pump market demonstrates moderate concentration, with a mix of multinational corporations and regional players competing across technology, capacity, and geography. Leading suppliers hold strong positions through comprehensive product portfolios, wide distribution networks, and advanced technological capabilities, while mid-sized firms and niche innovators cater to specialized applications and regional demand. Differences in pricing strategies, product efficiency, and compliance with evolving energy regulations shape competition.

Market players adopt varied strategies to strengthen their positions, ranging from distribution expansion into underserved markets to expertise in low-GWP refrigerants and premium product lines. Strategic acquisitions and partnerships are reshaping competitive dynamics by expanding manufacturing bases and enhancing product offerings.

At the same time, digital disruption from new entrants leveraging online configurators, financing solutions, and predictive maintenance platforms is challenging traditional dealer-driven models. Hybrid go-to-market approaches are becoming increasingly popular, combining consultancy-driven services with digital sales channels to offer standardized and small-scale commercial solutions.

Key Market Developments:

- In March 2025, Daikin shares an optimistic outlook projecting 250% heat pump market growth by 2030 at ISH 2025, presenting Daikin Altherma 4 generation and CO2 VRV systems designed for European decarbonization targets.

- In January 2024, Carrier Global Corporation completed a €12 billion acquisition of Viessmann Climate Solutions, expanding its portfolio with advanced energy-efficient heat pump technologies and positioning for rapid European market growth.

- In April 2025, Daikin acquired the Swedish heat pump service company Kylslaget, strengthening its nationwide residential heating service network and expanding technician coverage to over 95% of Swedish households, with more than 7,000 annual maintenance services.

Companies Covered in Heat Pump Market

- Carrier

- Daikin Industries, Ltd

- Robert Bosch GmbH

- Lennox International

- Johnson Controls, Inc.

- Midea Group

- Hitachi, Ltd.

- Ingersoll Rand Plc.

- Rheem Manufacturing Company

- HAIER (GENERAL ELECTRIC)

- Panasonic Holdings Corporation

- Danfoss

- Fujitsu

- LG Electronics, Inc

- Samsung

Frequently Asked Questions

The global heat pump market is projected to reach US$ 180.3 billion by 2032, growing from US$ 87.4 billion in 2025 at a CAGR of 10.9% during the forecast period.

Key demand drivers include government decarbonization initiatives, rising energy costs, energy efficiency regulations, and technological advancements in cold climate performance and smart integration.

Air source technology leads the market with approximately 80% share, driven by installation flexibility, cost-effectiveness, and government incentives for residential and commercial applications.

Europe dominates the market due to its mature policy frameworks, aggressive decarbonization targets, and subsidies such as Germany’s BEG program, which covers up to 70% of installation costs.

Industrial decarbonization through high-temperature heat pumps presents significant opportunities, particularly for process heating above 100°C in manufacturing applications and district heating networks.

Key players include Daikin Industries, Ltd., Carrier, Robert Bosch GmbH, Midea Group, Panasonic Holdings Corporation, and LG Electronics, Inc., competing through innovation and strategic acquisitions.