- Power Generation, Transmission, & Distribution

- Heat Shrink Tube Market

Heat Shrink Tube Market Size, Share, and Growth Forecast, 2025 - 2032

Heat Shrink Tube Market By Material Type (Polyolefin, PVC, Others), Voltage Class (Low Voltage, Medium Voltage), End-user Industry, and Regional Analysis for 2025 - 2032

Heat Shrink Tube Market Size and Trends Analysis

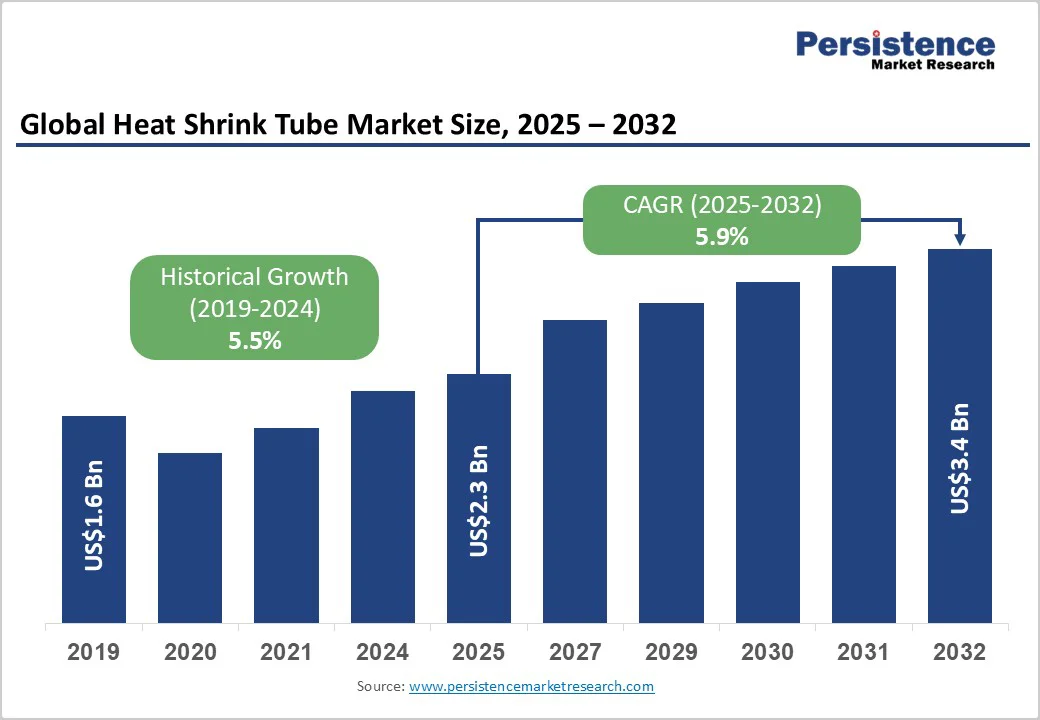

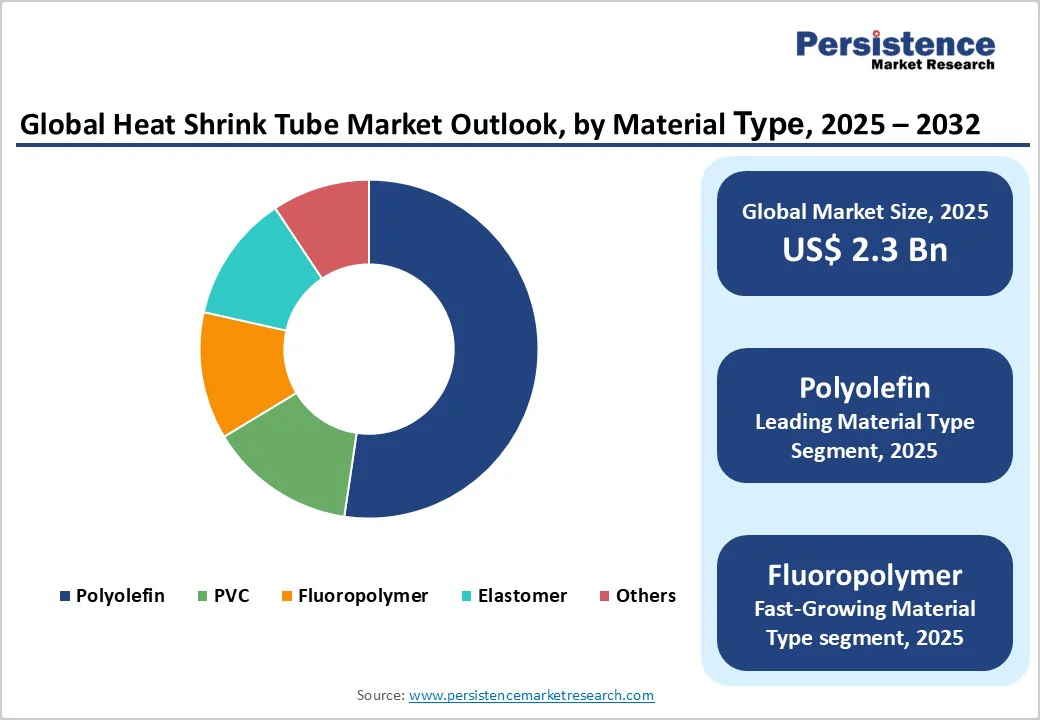

The global heat shrink tube market size was valued at US$2.3 billion in 2025 and is projected to reach US$3.4 billion by 2032, growing at a CAGR of 5.9% between 2025 and 2032, driven by the increasing need for reliable insulation and mechanical protection across electrical, automotive, and telecommunications systems. Heat shrink tubing demand is rising due to vehicle electrification, grid modernization, and polymer innovations. Flame-retardant, eco-friendly materials boost adoption and align with safety and sustainability standards.

Key Industry Highlights

- Leading Region: Asia Pacific accounted for over 40.5% of global revenue in 2025, supported by large-scale electronics, automotive, and power infrastructure industries in China, Japan, and India.

- Fastest-growing Region: Asia Pacific, driven by EV proliferation, telecom expansion, and renewable-energy investments.

- Investment Plans: Significant R&D and capacity expansion investments observed in 2024–2025, including HellermannTyton’s German facility upgrade and WOER’s Shenzhen plant expansion to meet surging insulation demand across EV and aerospace applications.

- Dominant Material Type: Polyolefin held over 56.3% share in 2025 due to its cost-effectiveness, flexibility, and broad applicability in electrical and automotive systems.

- Leading Voltage Class: Low Voltage (≤1 kV) represented more than 60.5% of total demand in 2025, supported by rapid residential electrification and consumer-electronics wiring applications.

| Key Insights | Details |

|---|---|

|

Heat Shrink Tube Market Size (2025E) |

US$2.3 Bn |

|

Market Value Forecast (2032F) |

US$3.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Electrification of Vehicles and Expansion of Automotive Wiring Systems

The accelerating shift toward electric and hybrid vehicles is substantially increasing wiring complexity and thermal exposure within automotive platforms. A typical EV contains over 4 km of wiring harnesses, demanding high-performance insulation capable of withstanding voltage surges and temperature extremes. According to the International Energy Agency (IEA), electric car sales surpassed 14 million units in 2024, representing 18% of global vehicle sales. Heat-shrink tubes, particularly cross-linked polyolefin and fluoropolymer types, are widely used to protect connectors, joints, and terminals. This automotive electrification trend is expected to account for over 25% of new demand for heat shrink tubing by 2032.

Rapid Expansion of Power and Telecommunication Infrastructure

Global investments in transmission and broadband networks continue to rise. The International Telecommunication Union (ITU) estimates that 5.5 billion people will be online by 2024, up from 3.8 billion in 2019, stimulating demand for fiber-optic and copper connectivity solutions requiring durable cable protection. Power-grid modernization initiatives in North America and the Asia Pacific are also fueling the installation of high-voltage systems and underground cabling, where heat-shrink tubing provides moisture sealing, corrosion resistance, and insulation reliability. These infrastructure upgrades collectively represent a multi-billion-dollar opportunity for heat shrink tube manufacturers through 2032.

Rising Safety and Regulatory Compliance Requirements

Global standards such as UL 224, IEC 60684, and RoHS/REACH have strengthened performance and environmental criteria for electrical insulation products. Manufacturers are compelled to adopt halogen-free, flame-retardant, and low-smoke materials to ensure safety in critical installations. According to the European Chemicals Agency, the usage of halogen-free polymers increased by over 8% annually from 2020 to 2024, reflecting the transition toward sustainable insulation materials. Compliance with such directives broadens export eligibility and also enhances customer confidence in aerospace, rail, and industrial sectors, thereby sustaining long-term demand for certified heat shrink tubing.

Barrier Analysis - Volatility in Raw-Material Prices and Supply Chain Disruptions

Heat-shrink tubes rely heavily on polymers such as polyethylene, fluoropolymers, and polyvinyl chloride. Price volatility linked to crude oil fluctuations and resin shortages can significantly impact manufacturing margins. In 2023, average polyolefin prices increased by nearly 15 % year-on-year, according to the World Bank Commodity Outlook. The industry’s reliance on specific chemical intermediates makes it vulnerable to disruptions in Asia’s petrochemical supply chain, leading to cost escalations and production delays.

Competition from Alternative Insulation Technologies

The expanding use of cold-applied tapes, molded boots, and liquid sealants in cable management applications poses a substitution risk. These solutions often provide faster installation and reduced material waste. The preference among OEMs for lightweight, integrated harness protection systems is encouraging hybrid insulation methods that may limit volume growth for traditional heat shrink tubing in selected low-voltage applications.

Opportunity Analysis - Growth of Renewable Energy Installations

Rising investments in offshore wind infrastructure across Europe and Asia are significantly driving product demand. For instance, large-scale projects such as the U.K.’s Dogger Bank Wind Farm and China’s Jiangsu Offshore Cluster require miles of undersea cabling, where heat-shrink tubes provide moisture sealing and electrical insulation in extreme marine conditions. The transition toward decentralized energy grids and microgrids is another driver, as it involves extensive low-voltage and medium-voltage wiring networks for solar rooftops and community energy systems. This trend is boosting the consumption of flame-retardant and weather-resistant heat shrink materials that ensure long-term performance in outdoor installations.

Miniaturization and Advanced Electronics Manufacturing

The rapid adoption of compact electronics in consumer, aerospace, and medical devices demands ultra-thin yet high-performance insulation. Manufacturers developing fluoropolymer and elastomeric micro-shrink tubing stand to benefit from miniaturization trends. These specialized tubes enable precise insulation of micro-cables and sensors while maintaining flexibility and chemical resistance, an emerging niche with projected double-digit growth through 2032.

Strategic Shift toward Sustainable and Recyclable Materials

With rising emphasis on circular-economy policies, OEMs are exploring recyclable and bio-based heat-shrink materials. Companies investing in polyolefin blends with low carbon footprints or post-consumer recycled inputs can access premium customer segments. Sustainability labeling, particularly under the EU Green Deal, could add a 3–5 % pricing advantage for compliant products over the forecast period.

Category-wise Analysis

Material Type Insights

Polyolefin dominates the heat shrink tubing market, capturing over 56.3% of global share in 2025, due to its versatile performance characteristics. With thermal stability up to 135°C, high dielectric strength, and flexibility, polyolefin tubing is widely used in automotive wiring, consumer electronics, and industrial maintenance. Its uniform shrinkage and rapid recovery ensure reliable sealing around connectors and splices. Dual-wall variants with adhesive inner layers, such as TE Connectivity’s RNF-100 series and HellermannTyton’s HA47 line, enhance waterproofing and corrosion resistance in wire harnesses and low-voltage assemblies. Cross-linked polyolefin tubing is increasingly adopted in solar installations and household wiring for its cost efficiency and RoHS compliance.

Fluoropolymer tubing, including PTFE, FEP, PVDF, and ETFE, is projected to register the highest CAGR through 2032, driven by applications in aerospace, medical, and semiconductor markets. These materials offer superior chemical resistance, UV stability, low friction, and excellent dielectric performance. Aerospace wiring leverages fluoropolymer tubing for resistance to jet fuel and hydraulic fluids, supplied by companies such as Zeus Industrial Products and Sumitomo Electric. In medical devices, FEP and PTFE microtubing are used for catheter sheathing, endoscope insulation, and microsensor protection due to their biocompatibility and transparency. Semiconductor manufacturing relies on fluoropolymer tubing for high-purity fluid transfer lines that withstand acids and plasma cleaning. The combination of performance reliability and specialized applications positions polyolefin and fluoropolymer tubing as the backbone of global heat shrink markets.

Voltage Class Insights

The low-voltage segment led the global heat shrink tubing market in 2025, accounting for over 60.5% of the market share, driven by strong demand in consumer electronics, residential wiring, and automotive circuits. These tubes play a vital role in protecting splices, connectors, and terminals from abrasion, moisture, and short circuits. Rapid urbanization and electrification in developing regions have fueled widespread adoption of household wiring and small appliances. Initiatives such as India’s “Saubhagya Scheme” and China’s rural electrification programs have further boosted demand for cost-effective electrical accessories. Leading manufacturers, including WOER Heat-Shrinkable Material Co. Ltd. and Changyuan Group, dominate this segment by supplying bulk polyolefin tubing, ensuring scalability and consistent volume growth.

The high-voltage segment is emerging as the fastest-growing category, propelled by renewable energy expansion, smart grid deployment, and utility modernization. Heat shrink tubing is essential for cable joints, terminations, and busbar insulation in high-voltage applications. Cross-linked fluoropolymer and elastomeric tubing offer superior dielectric strength and thermal endurance, making them suitable for substations, wind farms, and underground installations.

Products such as Shawcor’s DSG-Canusa HV series offer long-term resistance to weather and mechanical stress. The shift from overhead to underground cabling in Europe and Asia, alongside projects such as the U.S. Grid Resilience and Innovation Partnership (GRIP) and China’s Ultra-High-Voltage network, is accelerating demand for specialized high-voltage tubing. These developments are driving robust growth and expanding opportunities in the segment.

Regional Insights

Asia Pacific Heat Shrink Tube Market Trends - EV Expansion and Electronics Manufacturing Leadership

Asia Pacific accounts for over 40.5% of global revenue in 2025 and is the fastest-growing region. China, Japan, India, and ASEAN nations lead both production and consumption due to their extensive electronics, automotive, and energy infrastructure sectors. China’s rapid adoption of electric vehicles, expected to account for over 60% of new car sales by 2030, has significantly increased demand for heat-resistant insulation products for battery systems and high-voltage connectors. India’s expanding power distribution grid and telecom growth under the Digital India initiative are further stimulating the market.

Government-backed policies promoting local manufacturing and polymer technology parks are helping regional suppliers achieve cost efficiencies and supply-chain resilience. The presence of major resin producers in China and South Korea, such as LG Chem and Sinopec, supports consistent availability of raw materials. Recent industry developments include Changyuan Group’s 2025 launch of high-transparency fluoropolymer tubing for the medical and aerospace sectors, and WOER’s expansion of its Shenzhen facility to scale up production for export markets. Continuous investments in 6G testing infrastructure, renewable microgrids, and electric mobility systems are expected to sustain long-term demand across the region.

North America Heat Shrink Tube Market Trends - Regulatory Compliance and Sustainable Material Innovation

North America is driven primarily by the U.S., which maintains a strong presence in the automotive, aerospace, and renewable energy industries. Stringent regulatory standards such as those from Underwriters Laboratories (UL) and the National Electrical Code (NEC) ensure consistent product quality, electrical insulation integrity, and fire safety compliance. The implementation of the Inflation Reduction Act (2022) has significantly boosted investments in electric vehicle manufacturing and renewable energy infrastructure, directly increasing the demand for reliable cable-protection materials.

Growth in 5G network deployment has also accelerated the adoption of heat shrink tubing for fiber-optic cable shielding and connection sealing. Key U.S. suppliers such as TE Connectivity and 3M are investing heavily in advanced polymer composites and recyclable insulation materials, strengthening the region’s competitive position. Venture-backed startups, including those developing bio-based and halogen-free tubing, are further diversifying the market landscape, signaling a growing emphasis on sustainability and high-performance innovation.

Europe Heat Shrink Tube Market Trends - Eco-Friendly Transition and Advanced Polymer Development

Europe continues to demonstrate steady growth supported by strict environmental policies, high-quality manufacturing standards, and widespread adoption of electric and hybrid vehicles. Germany remains the largest market, benefiting from its robust automotive OEM network and expanding renewable energy infrastructure. The U.K. and France are driving further growth through grid-modernization projects and renewable integration efforts. EU directives such as RoHS III and REACH encourage the use of halogen-free and recyclable materials, fostering a shift toward eco-friendly product lines.

European R&D initiatives are focused on developing lightweight, high-efficiency polymers that comply with EN 45545-2 fire-safety standards, particularly for rail and public transport applications. Major manufacturers such as Tyco Electronics, Sumitomo Electric Europe, and HellermannTyton have localized production facilities in Germany and the Netherlands to optimize logistics and ensure compliance with sustainability norms. Recent developments include the 2024 expansion of HellermannTyton’s German plant for high-performance tubing production and Sumitomo Electric’s collaboration with local energy utilities to enhance insulation technologies for renewable power distribution networks.

Competitive Landscape

The global heat shrink tube market is moderately consolidated, with the top five players accounting for roughly 55% of total revenue. Key participants maintain vertically integrated operations encompassing polymer compounding, extrusion, and finished-tube manufacturing. Price competition remains moderate due to product differentiation through certifications, adhesive linings, and high-performance material formulations.

Dominant players prioritize innovation in material science, sustainability compliance, and regional capacity expansion. Cost-optimization through lean manufacturing, coupled with custom-engineered solutions for OEMs, remains a central differentiator.

Key Industry Developments

- In April 2025, Junkosha Inc. unveiled its latest etched PTFE liner developments for peelable heat-shrink tubing, aiming to meet stringent requirements from medical-device OEMs and advance its specialty micro-tubing portfolio.

- In April 2025, E.NEXT introduced the new “TERMO PRO” series adhesive-lined heat-shrink tubing, expanding its portfolio for industrial and electrical installation applications in harsh environments.

Companies Covered in Heat Shrink Tube Market

- TE Connectivity Ltd.

- 3M Company

- Sumitomo Electric Industries Ltd.

- HellermannTyton Group plc

- Changyuan Group Ltd.

- Alpha Wire Company

- WOER Heat-Shrinkable Material Co. Ltd.

- DSG-Canusa (Groupe Thermoplast)

- Shawcor Ltd.

- Qualtek Electronics Corp.

- Zeus Industrial Products Inc.

- Panduit Corp.

- Techflex Inc.

- Insultab Inc.

- Molex LLC

- Shrinkflex Heatshrink Tubing

- Taiyo Cable Tech Co. Ltd.

- Nexus Components Ltd.

- Sumadhura Polymers Pvt. Ltd.

- FITT Spa

Frequently Asked Questions

The global heat shrink tubing market size is anticipated to hit US$2.3 Billion in 2025.

By 2032, the global heat shrink tube market is forecast to reach US$3.4 Billion.

The heat shrink tube market is expected to expand at a CAGR of 5.9% from 2025 to 2032.

Key trends include the rising adoption of halogen-free and recyclable tubing, increased use in EV wiring harnesses, miniaturization in electronics, and advancements in cross-linked fluoropolymer materials for high-temperature and chemical-resistant applications.

By material type, polyolefin dominates the market with over 56.3% share in 2025 due to its cost-effectiveness, flexibility, and broad industrial applicability. The low voltage (≤1 kV) category also leads by voltage class, accounting for more than 60.5% of the overall demand.