- Automotive Components & Materials

- Automotive Gearbox Valves Market

Automotive Gearbox Valves Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Gearbox Valves Market by Valve Type (Solenoid Valve, EGR Valve, Thermostat Valve, Fuel System Valve, Tire Valve, Brake Valve, A/C Valve), by Gearbox Type (Manual Transmission, Automatic Transmission, Automated Manual Transmission, Continuously Variable Transmission, Dual-Clutch Transmission, Hydrostatic Transmission, Electric Drive Gearboxes), by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), by Function (Hydraulic Actuated Valves, Electro-Hydraulic Valves, Electromagnetic Valves, Pneumatic Valves, Electronic Smart Valves), by Sales Channel (OEM, Aftermarket), by Regional Analysis, 2026-2033

Automotive Gearbox Valves Market Size and Trend Analysis

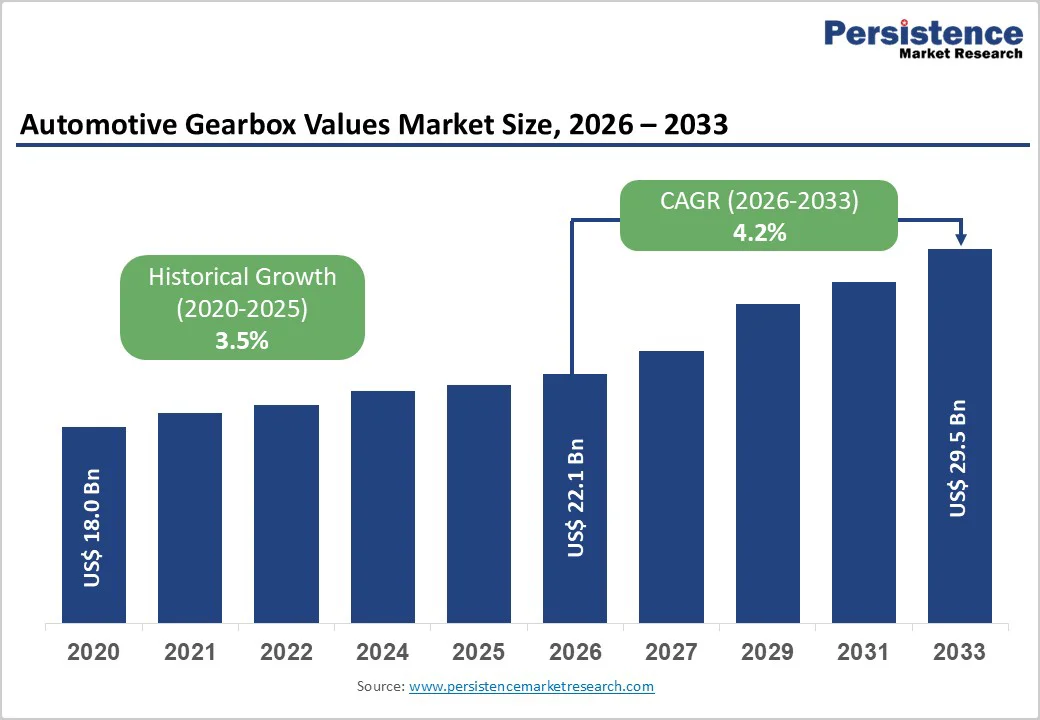

The global Automotive Gearbox Valves market size is expected to be valued at US$ 22.1 billion in 2026 and projected to reach US$ 29.5 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

Market growth is driven by the convergence of advanced automated transmission systems, accelerating electrification of vehicle powertrains, and tightening global emission regulations. Increasing adoption of electronically controlled solenoid valves enables precise shift control and efficiency gains. At the same time, hybrid and electric vehicles require specialized thermal and smart valve solutions to optimize powertrain performance and meet stringent fuel economy and emission standards.

Key Market Highlights

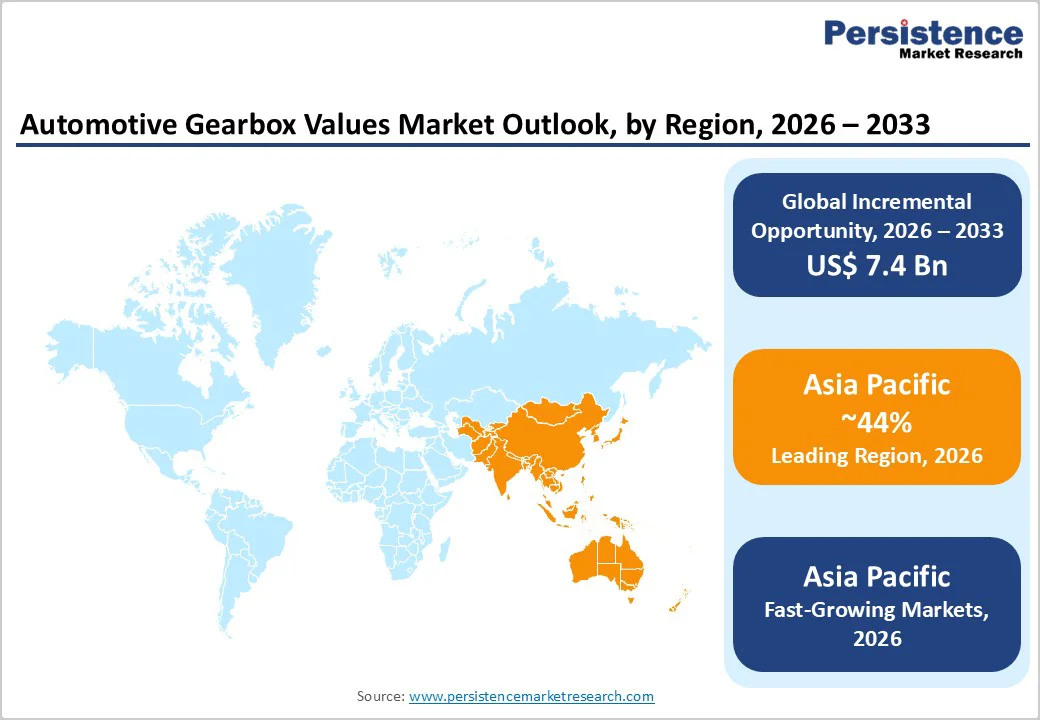

- Leading Region: Asia Pacific leads the Automotive Gearbox Valves market in 2025 with a 44% share, supported by high vehicle production in China, rising ownership in emerging economies, and strong adoption of advanced transmission technologies.

- Fastest Growing Region: Asia Pacific is expected to remain the fastest-growing region at a 4.6% CAGR during 2026–2033, driven by expanding automotive output, electrification mandates, and strengthening manufacturing bases across key Asian countries.

- Dominant Segment: Automatic transmission systems dominate with a 62% market share in 2025, driven by consumer preference for smooth shifting, fuel efficiency, and the growing use of multi-speed automatic platforms.

- Fastest-Growing Segment: Electric-vehicle transmission valve applications are projected to grow at an 8.6% CAGR from 2026 to 2033, driven

- by rising EV penetration and demand for advanced thermal management solutions.

- Key Market Opportunity: AI-enabled adaptive transmission control combined with integrated thermal management systems represents the most significant growth opportunity for gearbox valve manufacturers.

| Global Market Attributes | Key Insights |

|---|---|

| Automotive Gearbox Valves Market Size (2026E) | US$ 22.1 billion |

| Market Value Forecast (2033F) | US$ 29.5 billion |

| Projected Growth CAGR (2026-2033) | 4.2% |

| Historical Market Growth (2020-2025) | 3.5% |

Market Dynamics

Market Growth Drivers

Proliferation of Automatic and Multi-Speed Transmission Technologies in Passenger and Commercial Vehicles

The automotive industry is experiencing a profound transformation toward automatic and advanced multi-speed transmission platforms, with automatic transmissions commanding 58-61% market share across global vehicle production and dual-clutch transmissions (DCTs) projected to grow at 8.6-8.9% CAGR through 2032. The USA automatic gearbox valves market alone is valued at approximately US$ 12.5 billion, driven by rising North American consumer preference for seamless shifting, refined drivability, and improved fuel economy.

In response to regulatory pressure, automotive OEMs, including General Motors, Ford, Volkswagen, BMW, and Mercedes-Benz, are transitioning from 6-speed automatic platforms to 8-speed, 9-speed, and 10-speed configurations, featuring sophisticated solenoid valve assemblies that enable adaptive transmission control strategies and sport mode calibrations. The integration of electronic transmission control units (TCUs) leveraging proportional solenoid valves and pressure regulator valves enables infinitely variable line pressure modulation, clutch pack engagement timing optimization, and dynamic shift scheduling algorithms that adapt to driver inputs, vehicle speed profiles, and engine torque characteristics.

Technological Advancement in Electronically Controlled Valve Systems and IoT-Enabled Predictive Maintenance

The automotive transmission valve industry is undergoing a fundamental technology evolution from traditional mechanical hydraulic controls to sophisticated electronically managed platforms featuring microprocessor-driven algorithms, real-time pressure-sensing feedback loops, and AI-enabled predictive maintenance capabilities. Advanced proportional valve technology, incorporating corrosion-resistant coatings on valve spools, improved solenoid coil design, and temperature-compensated flow control mechanisms, reduces hydraulic leakage risks, extends service life, and improves long-term reliability across diverse operating temperature ranges.

Manufacturers, including HUSCO Automotive, have expanded production capacity for electro-hydraulic solenoid valves supporting shift-by-wire and start-stop transmission systems, with facilities in China and Europe delivering low-hysteresis valve designs with repeatable performance across high-volume OEM applications. Integration of pressure sensor feedback, valve position monitoring, solenoid resistance diagnostics, and onboard vehicle connectivity enables real-time transmission health monitoring, predictive failure alerts, and targeted maintenance scheduling, reducing warranty costs and improving perceived vehicle reliability.

Market Restraints

High Manufacturing Complexity and Capital-Intensive Production Requirements

The design, development, and manufacturing of precision-engineered gearbox valve systems require substantial capital investment in advanced machining equipment, precision casting processes, and sophisticated quality control systems to meet stringent accuracy and reliability standards. Advanced hydraulic valve bodies require laser processing technology, micro-nano manufacturing techniques, and automated production lines incorporating industrial robotics, collectively increasing production costs by 20-30% compared to conventional manufacturing approaches.

These stringent performance requirements create significant barriers to market entry for small and medium-sized automotive suppliers, while large Tier-1 manufacturers, including Continental AG, Bosch, ZF Friedrichshafen, and Magna International, consolidate market share through vertical integration into component manufacturing and proprietary technology development. First-tier suppliers increasingly acquire specialized valve manufacturers to internalize critical component production and reduce supply chain complexity, limiting opportunities for independent valve manufacturers and compressing competitive dynamics.

Shift Toward Electric Vehicle Architectures Utilizing Simplified Single-Speed Transmission Systems

The accelerating electrification of the automotive industry, with battery-electric vehicles (BEVs) projected to comprise 50%+ of new vehicle sales by 2035 across major developed markets, represents a structural market headwind for traditional multi-speed transmission valve systems. Electric vehicles featuring single-speed transmissions eliminate the need for complex hydraulic valve bodies, solenoid shifting mechanisms, and torque converter systems, fundamentally reducing valve system demand and supplier revenue opportunities.

Companies, including Tesla, have pioneered EV propulsion architectures that use single-stage reduction gearboxes, offering superior efficiency, reliability, and cost advantages compared to traditional multi-speed automatics. However, emerging opportunities exist in specialized valve applications for thermal management systems, battery cooling circuits, electronic expansion valves (EXVs) for air conditioning systems, and oil-cooled electric motor thermal control, partially offsetting the decline in demand from traditional transmission valve applications.

Market Opportunities

Integration of AI-Based Predictive Maintenance and Self-Learning Transmission Control Algorithms

Artificial intelligence and machine learning technologies are transforming the architecture of transmission valve systems toward intelligent, adaptive platforms that optimize performance by real-time assessment of driving conditions, driver behavior patterns, and vehicle dynamics. Modern automatic transmissions increasingly integrate AI-powered transmission control algorithms that adjust hydraulic line pressures, shift timing, and torque distribution profiles dynamically to minimize fuel consumption, enhance shift quality, and extend transmission component longevity.

Porsche, Mercedes-Benz, and BMW have deployed advanced DCT platforms incorporating adaptive shift logic that learns driver preferences across accelerating, cruising, and braking scenarios, enabling personalized transmission calibration. Development opportunities exist for valve manufacturers capable of delivering high-speed solenoid actuators with sub-millisecond response times, proportional pressure control, and integrated diagnostic sensor nodes that support real-time transmission health monitoring and predictive maintenance alerts.

Expansion of Dual-Clutch and Continuously Variable Transmission Platforms in Emerging Market Vehicles

The global dual-clutch transmission market is projected to expand at a 9.0% CAGR through 2033, with particular growth in the Asia Pacific and emerging market segments. Continuously Variable Transmissions (CVTs) are similarly expanding with 8.0% CAGR in the same period, driven by increasing adoption in affordable vehicle segments across China, India, Indonesia, and Southeast Asia where fuel efficiency benefits and cost-effectiveness drive consumer demand.

These advanced transmission platforms require sophisticated multi-solenoid valve control systems, proportional pressure regulators, and electronically managed friction element engagement mechanisms, creating substantial demand for valve components. Manufacturers, including Schaeffler, Valeo, and BorgWarner, are leading innovation in DCT valve architecture with proprietary multi-clutch transmission designs incorporating integrated valve bodies, pressure sensors, and electronic actuation systems.

The Chinese automotive market, commanding approximately 40% market share of Asia Pacific gearbox valve demand, is experiencing rapid DCT and CVT adoption, supported by local transmission manufacturers, including Geely, Great Wall Motors, and BYD, seeking to differentiate products through advanced transmission technologies. Suppliers capable of delivering scalable valve platforms supporting diverse transmission architectures and achieving significant cost reductions through advanced manufacturing processes are positioned to capture substantial market opportunities across emerging market vehicle segments.

Category-wise Insights

Valve Type Analysis

Solenoid valves dominate the automotive gearbox valves market with around 48% share in 2025, reflecting their central role in modern transmission control. These valves regulate hydraulic pressure, manage gear shifts, and control clutch engagement across automatic, DCT, and CVT systems. Their integration with transmission control modules enables rapid, electronically driven response to driving conditions, supporting smooth shifting, torque optimization, and fuel efficiency. Technological progress in proportional solenoid valves has further enhanced performance by enabling continuous pressure control rather than simple on–off operation. This capability is critical for eliminating shift shock and improving drivability. Demand growth is supported by rising adoption of multi-speed automatic and hybrid transmissions, positioning solenoid valves as a core enabler of next-generation powertrain architectures.

Gearbox Type Analysis

Automatic transmission systems account for approximately 62% of market demand in 2025, driven by strong consumer preference for driving comfort, reduced fatigue, and refined shift quality. These systems rely heavily on integrated valve bodies containing multiple solenoids and pressure control valves that coordinate seamless gear changes and torque converter operation. The transition toward higher-gear-count platforms, including 8-speed and higher configurations, has increased system complexity and valve content per transmission. Automatic transmissions are particularly dominant in Asia Pacific and North America, where urban driving conditions favor ease of use. Continued penetration in emerging markets, coupled with replacement demand as older platforms are phased out, sustains steady growth for valve suppliers aligned with advanced automatic transmission designs.

Vehicle Type Analysis

Passenger cars account for nearly 68% of gearbox valve demand in 2025, supported by the world’s large and aging passenger vehicle fleet and ongoing upgrades in transmission technology. This segment places strong emphasis on smooth shifting, low noise, and fuel efficiency, driving demand for precision solenoid and electro-hydraulic valve systems. Innovation introduced in premium and luxury passenger vehicles often sets performance benchmarks that later diffuse into mass-market models, accelerating overall valve adoption. Rising penetration of automatic and hybrid powertrains in mid-size sedans and SUVs further strengthens demand. While electrification introduces new design requirements, passenger cars remain the primary volume driver for gearbox valves due to their scale, replacement cycles, and ongoing technology refinement.

Function Analysis

Electro-hydraulic valves lead the functional segmentation with about 54% market share in 2025, reflecting their importance in linking electronic control logic with hydraulic actuation. These valves combine solenoid-driven inputs with precise fluid flow regulation to enable adaptive transmission behavior under varying load and speed conditions. Their ability to support proportional pressure modulation is essential for advanced shift strategies and efficiency optimization. Increasing integration of sensors and diagnostic features within electro-hydraulic valve assemblies allows real-time monitoring and early fault detection, improving transmission reliability. As transmissions become more software-driven and performance-sensitive, electro-hydraulic valves remain critical components for balancing electronic intelligence with robust mechanical power delivery.

Sales Channel Analysis

OEM sales dominate the automotive gearbox valves market, with roughly a 76% share in 2025, reflecting the deep integration of valve suppliers into vehicle and transmission manufacturing supply chains. Direct supply to OEMs enables early-stage collaboration on transmission design, calibration, and validation, ensuring optimal valve performance for specific powertrain architectures. Long-term contracts and high-volume production provide suppliers with revenue stability and scale advantages. OEM channels also benefit from growing content per vehicle as transmissions become more complex and electronically controlled. While aftermarket demand provides supplementary growth, OEM sales remain the primary driver due to ongoing new-vehicle production, platform upgrades, and increasing adoption of advanced automatic and electrified transmissions.

Regional Insights

North America Automotive Gearbox Valves Market Trends and Insights

North America accounts for roughly 29% of the global automotive gearbox valves market in 2025, supported by a large and aging vehicle fleet and high penetration of automatic transmissions. The United States drives regional demand due to strong consumer preference for automatic drivetrains in passenger cars, SUVs, and light trucks, where comfort and drivability are key purchase criteria. The region demonstrates advanced adoption of electronically controlled valve systems, proportional pressure control, and integrated diagnostics to enhance shift quality and reduce warranty risks.

Regulatory pressure from fuel-economy standards is accelerating the transition from legacy 6-speed systems to higher-gear-count automatic platforms, increasing valve complexity per transmission. Market growth is also supported by steady aftermarket replacement demand and early adoption of electric and hybrid vehicles, which require specialized thermal management and cooling valve solutions. Overall, North America shows stable, technology-led growth driven by system upgrades and electrification.

Europe Automotive Gearbox Valves Market Trends and Insights

Europe represents a technologically advanced and regulation-driven market for automotive gearbox valves, characterized by a strong emphasis on efficiency, emissions reduction, and drivetrain innovation. Demand is concentrated in major automotive manufacturing economies, where advanced transmission systems are widely deployed across both premium and mass-market vehicles. Europe has been an early adopter of dual-clutch and continuously variable transmissions, driving sustained demand for precision valve control and proportional pressure management technologies.

Compliance with stringent emission and fuel-efficiency regulations under EU frameworks continues to shape transmission design and valve-system requirements. The region also leads in integrating diagnostics and electronic control into transmission valve architectures to optimize performance and lifecycle reliability. Growth is further supported by increasing electrification, which requires dedicated thermal management valve systems for hybrid and electric vehicles. Europe is expected to maintain steady expansion through ongoing regulatory tightening and continuous refinement of powertrain technology.

Asia Pacific Automotive Gearbox Valves Market Trends and Insights

Asia Pacific dominates the global automotive gearbox valves market with approximately 44% share in 2025, reflecting its role as the world’s largest vehicle production and consumption region. High manufacturing volumes, expanding middle-class vehicle ownership, and rapid technology diffusion support strong regional demand. China remains the primary growth engine, driven by large-scale adoption of advanced automatic, dual-clutch, and electrified transmissions aligned with national electrification policies.

Japan contributes through leadership in continuously variable and hybrid transmission technologies, emphasizing efficiency and durability. India represents a fast-growing market as automatic transmissions gain acceptance in mid-size and compact vehicles. Across the region, increasing electrification and hybridization are accelerating demand for electronic smart valves and thermal management solutions. Asia Pacific is forecast to remain the fastest-growing region due to scale advantages, cost-efficient manufacturing, and accelerating adoption of advanced powertrain technologies.

Competitive Landscape

Market Structure Analysis

The automotive gearbox valves market is moderately consolidated, with a limited number of large, global suppliers accounting for a majority of total revenues, while smaller regional and specialized manufacturers remain active in niche applications and aftermarket segments. Market structure is shaped by high entry barriers related to precision engineering, regulatory compliance, and long OEM qualification cycles, which favor established suppliers. Competitive positioning increasingly depends on vertical integration across transmission design, valve manufacturing, and electronic control systems to enhance cost efficiency and influence system architecture.

Leading participants prioritize geographic expansion into high-growth automotive markets through localized production and joint ventures to improve supply responsiveness. Technology differentiation is a core strategy, focused on proportional valve systems, software-driven control, and embedded diagnostics supporting predictive maintenance. Selective mergers and acquisitions are used to consolidate capabilities and fill technology gaps. Emerging service-oriented models centered on software, diagnostics, and lifecycle support are gradually complementing traditional component supply strategies.

Key Market Developments

October 2025: BORG Automotive Newman is set to launch over 3,100 Lucas-branded spare parts for engines, chassis, and transmissions across Europe starting Q1 2026. After securing exclusive rights following the brand's market absence, these OEM-compliant components will be integrated into TecDoc catalogs in 2025.

August 2025: HPL has launched the Supreme Intelligent ATS series, an automatic transfer switch for seamless power. It features inbuilt/panel-mounted controllers, controlling over 45.

Companies Covered in Automotive Gearbox Valves Market

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aisin Seiki Co. Ltd.

- Eaton Corporation PLC

- Hitachi Ltd

- Magna International Inc.

- Johnson Electric Group

- Delphi Technologies PLC

- Valeo SA

- BorgWarner Inc.

- Schaeffler AG

Frequently Asked Questions

The global Automotive Gearbox Valves market is expected to reach US$ 22.1 billion in 2026.

Key drivers include rising adoption of automatic transmissions, stricter fuel efficiency regulations, growth of electronically controlled valves, and increasing electrification of vehicle powertrains.

Asia Pacific leads the market in 2025 with about 44% share.

Advanced intelligent valve systems with AI-based control and thermal management for hybrid and electric vehicles represent the main growth opportunity.

The market is dominated by global leaders including Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, Aisin Seiki, Eaton Corporation, Hitachi Ltd, and Magna International.