- Automotive Components & Materials

- Fuel and Lube Trucks Market

Fuel and Lube Trucks Market Size, Share, and Growth Forecast, 2025 - 2032

Fuel and Lube Trucks Market By Truck Type (Fuel Tank Trucks, Lube Service Trucks, Others), Capacity (Below 10,000 Kg, 10,000 Kg to 15,000 Kg, Others), Application (Construction & Infrastructure, Transportation & Logistics, Others), and Regional Analysis for 2025 - 2032

Fuel and Lube Trucks Market Share and Trends Analysis

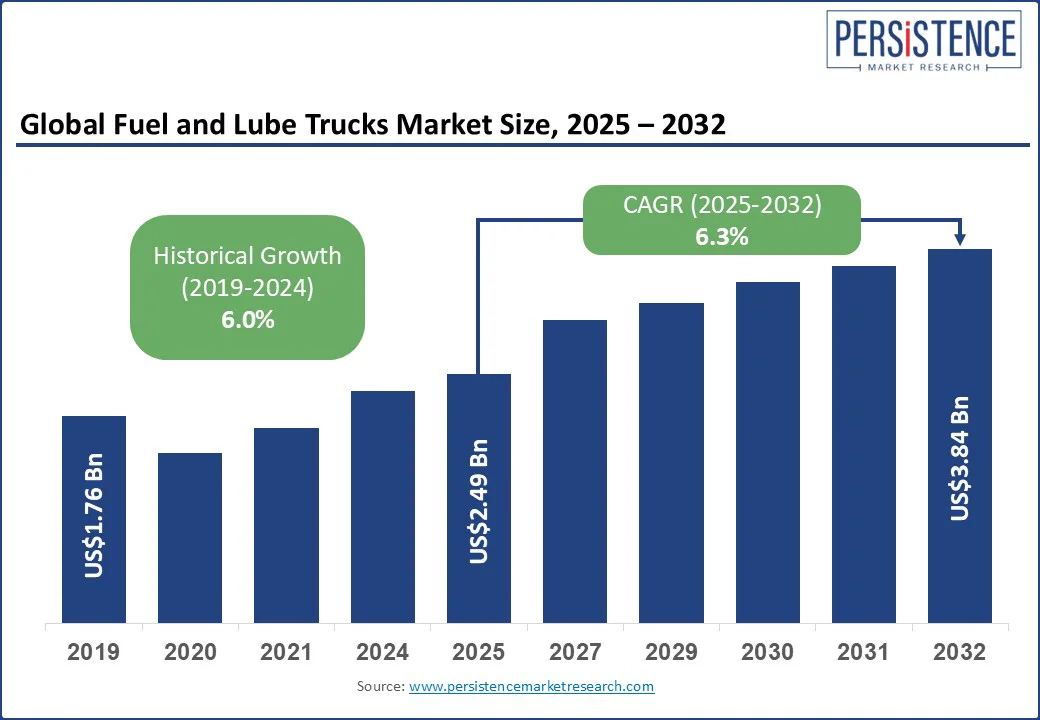

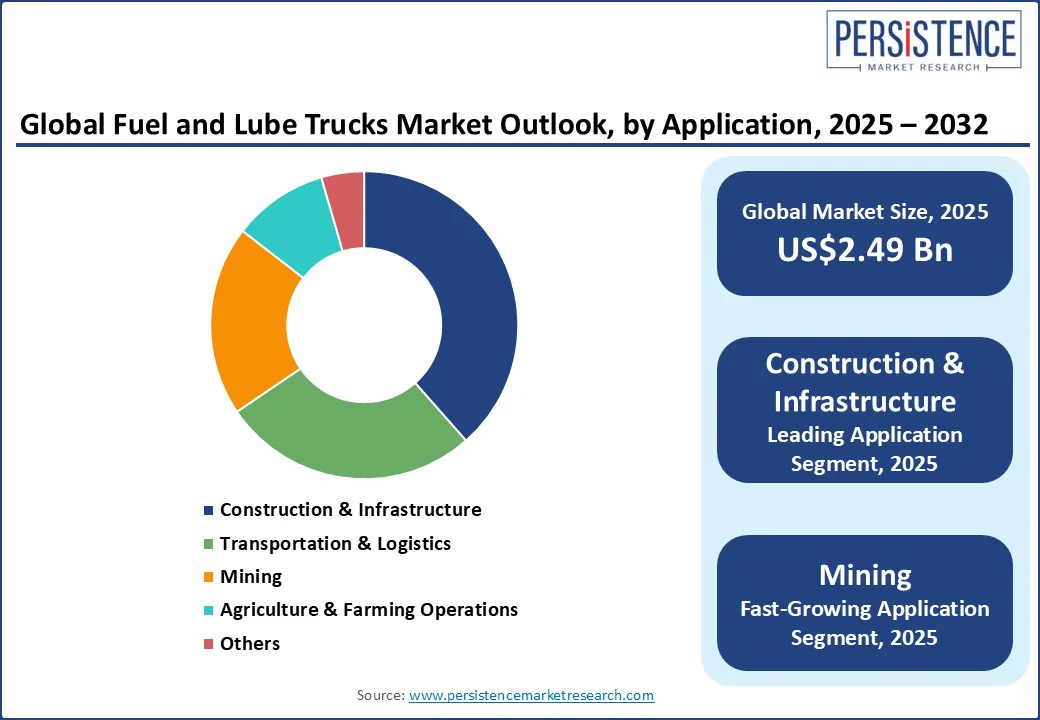

The global fuel and lube trucks market size is projected to rise from US$ 2.49 Bn in 2025 to US$ 3.84 Bn by 2032. It is anticipated to witness a CAGR of 6.3% during the forecast period from 2025 to 2032.

Fuel diversification from liquefied natural gas (LNG) and biofuels to electric medium- and heavy-duty trucks is driving market growth by prompting equipment upgrades, tank retrofits, and development of hybrid fuel and lube truck service fleets.

Fuel and lube trucks are specialized service vehicles for on-site delivery of diesel, lubricants, LNG, and alternative fuels. Essential for minimizing downtime and maximizing productivity in core sectors such as mining, construction, and agriculture, modern mobile fuel delivery and lube service trucks integrate safety compliance and multi-compartment tanks for mixed-fuel runs. These trucks are increasingly equipped with IoT-enabled fuel management systems integrated with asset telematics.

The demand for these trucks is fueled by rapid infrastructure growth, rising on-site fleet servicing needs, and evolving safety and Agreement concerning the International Carriage of Dangerous Goods by Road (ADR) regulations of the UN Economic Commission for Europe (UNECE). Multi-fuel mobile refueling, predictive lubrication scheduling, and refueling-as-a-service contracts are shaping competitive strategies, while green refueling hubs combining diesel, LNG, biofuels, and EV charging equipment are opening new opportunities.

Key Industry Highlights

- Leading Application Segment: The construction & infrastructure segment is expected to hold the largest market share in 2025 at approximately 38.5%, driven by rapid global urbanization and large-scale infrastructure projects that require efficient on-site fueling and lubrication.

- Dominant Truck Type Segment: Fuel tank trucks are expected to dominate the truck type segment in 2025 with a projected revenue share of approximately 60.2%, driven by their critical role in the safe and efficient delivery of fuel to operational sites in the mining, construction, and agriculture sectors.

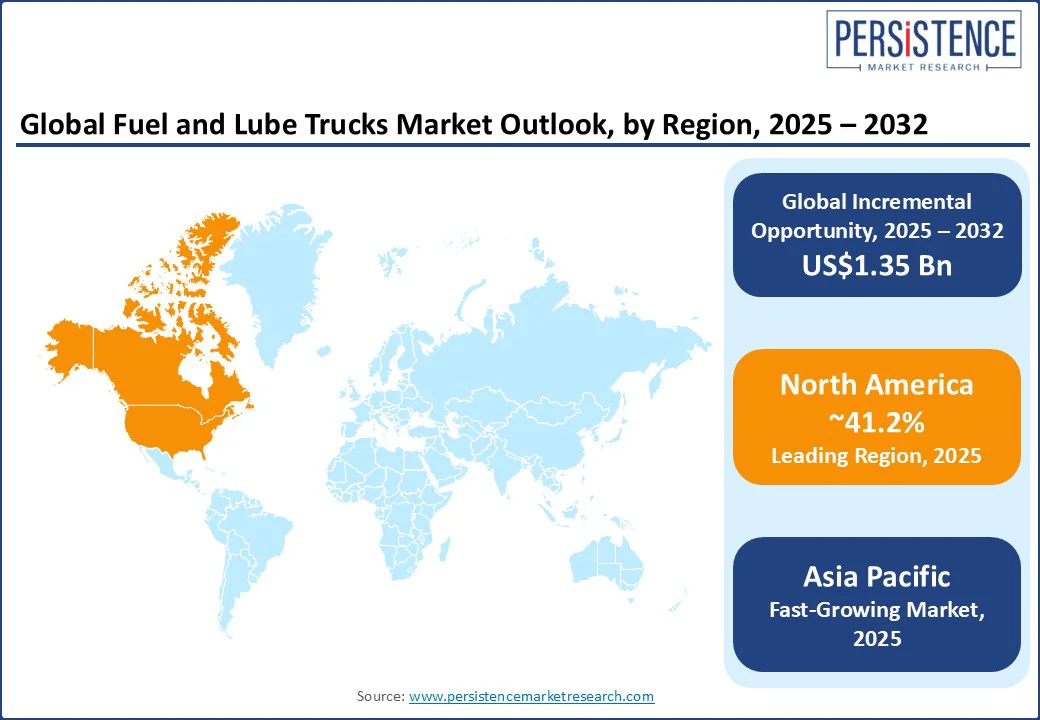

- Dominant Region: North America is projected to lead the market in 2025 with a 41.2% share, driven by large-scale infrastructure investments, advanced fleet automation, and strong sustainability initiatives.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by rapid urbanization, industrialization, and large-scale infrastructure development in China, India, and Southeast Asia.

|

Global Market Attribute |

Key Insights |

|

Fuel and Lube Trucks Market Size (2025E) |

US$2.49 Bn |

|

Market Value Forecast (2032F) |

US$3.84 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.0% |

Market Dynamics

Driver - Continued Dependence on Heavy Equipment to Boost Market Growth

A key driver of the market, especially in the lube service and fuel tank truck segments, is the ongoing reliance of critical industries such as construction and mining on uninterrupted heavy equipment operations. The surge in construction and mining activities globally is the core growth catalyst for the fuel and lube trucks market.

According to a 2024 research report the global construction spending is projected to jump from US$ 13 Tn in 2023 to a massive US$ 22 Tn by 2040. Furthermore, as large-scale infrastructure projects expand into remote and underdeveloped regions, companies are turning to on-site fuel delivery and mobile lubrication solutions to minimize downtime for bulldozers, haul trucks, and other high-value assets. This shift is attracting investments in mobile refueling and fleet lubrication systems that can operate in challenging terrains while meeting stringent safety and compliance standards.

Restraint - Rising Compliance Costs to Dampen Market Outlook

One of the most significant factors limiting market growth is the mounting burden of regulatory compliance. Stricter emissions standards, hazardous goods transport regulations, and safety certifications are prompting manufacturers and fleet operators to invest heavily in advanced tank designs, enhanced filtration, secondary containment systems, and emissions control technologies.

For example, the U.S. Environmental Protection Agency (EPA) regulates equipment manufacturers in the trucking industry by mandating manufacturers to undergo rigorous testing to ensure their products meet the emissions requirements. These standards substantially raise production and operational costs, disproportionately affecting small and mid-sized manufacturers while giving larger original equipment manufacturers (OEMs) a competitive edge.

Even as regulatory pressures contribute to higher unit costs in the sector, sustainability-focused mandates continue to increase operational complexity and capital expenditure, slowing the pace of innovation and limiting flexibility for a large portion of market participants.

Opportunity - Establishment of Integrated Multi-Energy Refueling Hubs to Present a High-Value Growth Avenue

The rise and expansion of integrated multi-energy refueling hubs, which are facilities capable of supplying diesel, LNG, biofuels, electricity, hydrogen, and hydrotreated vegetable oil (HVO) from a single location, has emerged as probably the most exciting opportunity in the fuel and lube trucks market. A prime example is Aegis Energy’s US$122 Mn investments in the U.K. to develop a network of green refueling hubs along key logistics routes, offering heavy goods vehicles access to multiple fuel types, rapid EV charging, and hydrogen.

This model can enable OEMs and fleet operators to reposition fuel and lube trucks as integral components of a broader energy-as-a-service ecosystem. By leveraging multi-fuel depot solutions, hybrid service fleets, and sustainable on-site refueling systems, stakeholders can secure higher margins, long-term customer loyalty, and a competitive advantage in serving logistics, mining, and infrastructure sectors.

Category-wise Analysis

Application Insights

The construction & infrastructure segment is projected to hold a dominant revenue share of approximately 38.5% in 2025. The leading position of this segment is based on rapid infrastructure development and urbanization, especially in emerging economies. For instance, under the 2019 National Infrastructure Pipeline (NIP), the Government of India planned on spending INR 102 Tn (around US$ 1.4 Tn) on energy, roads, railways, and urban development projects.

These trucks are thus indispensable assets for on-site fueling and lubrication of heavy construction machinery, helping minimize costly downtime and maximize operational efficiency in large-scale projects. Advances in truck technology, including automated dispensing systems, GPS tracking, and IoT-enabled fleet management, will further enhance precision and reduce fuel wastage. The growing adoption of eco-friendly, fuel-efficient trucks to meet strict environmental regulations, coupled with substantial government funding and private investment in infrastructure, is expected to be a key driver of segment growth.

The mining segment is anticipated to grow at the fastest CAGR through 2032, driven by widespread mineral and resource extraction activities requiring reliable on-site fuel and lubrication. Mines are often located in remote areas with limited access to traditional fueling stations, making fuel and lube trucks critical for the continuous operation of heavy-duty machinery such as excavators, haul trucks, and drills.

Technological innovations in ruggedized truck designs and integration of smart monitoring systems can optimize fuel delivery schedules and maintenance, reducing operational costs and environmental impact and creating a highly profitable opportunity in this space.

The rising demand for minerals essential for the energy transition, such as lithium and cobalt, further propels the segment growth. Companies actively operating in mining sectors in regions such as Latin America and Australia are investing in specialized fuel trucks to ensure uninterrupted supply chains.

Truck Type Insights

Fuel tank trucks are slated to lead the truck type segment with a revenue share of about 60.2% in 2025, owing to their central role in safely and efficiently transporting fuel to operational sites across the mining, construction, and agriculture industries. Their large tank capacity, typically ranging from 1,000 to 4,500 gallons, enables the servicing of extensive and diverse equipment fleets in one trip, optimizing operational uptime and reducing refueling delays.

The demand for fuel tank trucks is further heightened by the soaring rate of infrastructure expansion worldwide and increased mechanization of heavy industrial operations, particularly in emerging economies. In addition, advancements in fuel tank safety, spill prevention technologies, and adherence to stricter environmental regulations will further contribute to the segment growth. For example, automated fuel dispensing systems and GPS-enabled truck tracking are improving delivery precision and safety standards globally.

Combination trucks are gaining traction due to their operational efficiency and adaptability, particularly in remote and complex work environments. These trucks minimize the need for multiple vehicles on-site by combining fueling and lubrication tasks, thus reducing logistical costs and equipment downtime. Rapid progress in modular tank designs, automation, and telematics integration enables real-time monitoring and predictive maintenance, attracting sectors emphasizing operational efficiency and cost control. The rising popularity of combination trucks in mining and infrastructure projects with challenging terrains will brighten market prospects for the foreseeable future.

Regional Insights

North America Fuel and Lube Trucks Market Trends

North America is set to command 41.2% of the fuel and lube trucks market share in 2025, primarily backed by robust and ongoing infrastructure development projects across the U.S. and Canada. The U.S. Infrastructure Investment and Jobs Act of 2025 has injected massive capital into transportation and construction projects, bolstering the demand for mobile fueling and lubrication solutions designed to reduce machinery downtime.

Advanced technologies such as automated dispensing systems, IoT-enabled real-time monitoring, and GPS fleet tracking are widely adopted in the region, enhancing operational precision and fuel management efficiency. Moreover, the well-established logistics and mining industries in North America require efficient on-site fueling trucks to sustain productivity in geographically diverse sites, further solidifying the region’s market dominance. Sustainability initiatives pushing for cleaner fuels and more energy-efficient trucks are also stimulating the innovation capacities of market players.

Asia Pacific Fuel and Lube Trucks Market Trends

Asia Pacific is expected to be the fastest-growing regional market for fuel and lube trucks. This rapid growth correlates with accelerated urbanization, industrialization, and expansive infrastructure development, particularly in China, India, and Southeast Asian economies.

The expanding manufacturing sector and large-scale mining operations have increased the demand for highly reliable on-site fueling and lubrication services in the region. Modern ruggedized truck designs customized for remote and challenging terrains, alongside the growing adoption of green and fuel-efficient vehicles, characterize this region’s evolving trucking landscape. Government incentives and industrial investments have encouraged OEMs to expand local production facilities, allowing them to capitalize on the region's much untapped potential. For example, infrastructure mega-projects such as India’s national highways expansion and China's Belt and Road Initiative amplify requirements for mobile fuel truck fleets.

Europe Fuel and Lube Trucks Market Trends

In Europe, the upward movement of the market is supported by stringent environmental regulations of the EU and long-term investments in electrified and efficient transportation infrastructure. Stakeholders in Europe value sustainability above all other considerations. As a result, the regional market will gain from the active promotion of eco-friendly fueling solutions with reduced emissions and the integration of smart monitoring systems, aligning with the European Green Deal targets.

Strong demand for fuel and lube trucks in construction, mining, and urban logistics also fuels the market, with regional players innovating in lightweight and automated fuel dispensing technologies. The EU’s emphasis on regulatory compliance, circular economy principles, and smart fleet solutions is creating niche opportunities in Europe’s fuel and lube trucks market, driving emission reductions and cost-effective fleet management.

Competitive Landscape

The global fuel and lube trucks market landscape is experiencing a material shift, as OEMs and specialist builders attempt to differentiate through service integration, advanced technology, and fuel diversification capabilities. Leaders are moving past standard tanker production to deliver compliance-certified, multi-service solutions, from refueling-as-a-service contracts and IoT-enabled mobile fuel delivery systems to alternative-fuel-ready retrofits.

Strategic alliances between vehicle manufacturers, tank fabricators, and telematics providers are increasingly common, allowing companies to offset rising regulatory and ADR compliance costs while offering integrated fuel management systems as turnkey solutions. Rapidly growing demand for multi-compartment, explosion-proof tanks, and multi-fuel depot compatibility is raising technical entry barriers, strengthening the market position of established brands.

Key Industry Developments

- In January 2025, Sage Oil Vac introduced the compact LV230 and LV430 service lube vans built on a Ford Transit chassis, tailored for tight urban jobsites. Featuring pump-free vacuum technology, ample storage (303-349 cu ft), and no CDL requirement, these vans ensure faster, cleaner fluid transfers, keep fluids warm in cold weather, and improve fuel economy while reducing costs versus traditional lube trucks.

- In January 2025, Stellar Industries made a strong return at World of Concrete by unveiling a mini lube truck, the first since acquiring Elliott Machine Works. Offered in both open and enclosed models for CDL and non-CDL drivers, it came equipped with multiple pumping systems for oil, antifreeze, and grease, ample underbody storage, and fast used-oil removal. This addition broadened Stellar’s service truck portfolio, boosting efficiency and versatility for the construction and concrete sectors.

Companies Covered in Fuel and Lube Trucks Market

- Knapheide Manufacturing Company

- McLellan Industries, Inc.

- Niece Equipment, LP

- Stellar Industries, Inc.

- Heil Trailer International, L.P.

- Taylor Pump & Lift

- Sage Oil Vac, Inc.

- Thunder Creek Equipment, LLC

Frequently Asked Questions

The fuel and lube trucks market is projected to reach US$ 2.49 Bn in 2025.

Rapid infrastructure growth, rising on-site fleet servicing needs, and evolving cargo safety regulations are driving the market.

The market is poised to witness a CAGR of 6.3% from 2025 to 2032.

The rise and expansion of integrated multi-energy refueling hubs and a growing demand for sustainable on-site fueling facilities are key market opportunities.

Knapheide Manufacturing Company, McLellan Industries, Inc., and Niece Equipment, LP are some of the key market players.