- Electric Mobility

- EV Charging Equipment Market

EV Charging Equipment Market Size, Share, and Growth Forecast 2026 - 2033

EV Charging Equipment Market by Connector Type (Type 1, Type 2, GB/T), Charging Type (Level 1, Level 2, DC Fast Charging), Power Output (Up to 3 kW, 3 kW - 22 kW), End-user (Residential, Commercial), and Regional Analysis, 2026 - 2033

EV Charging Equipment Market Size and Trends Analysis

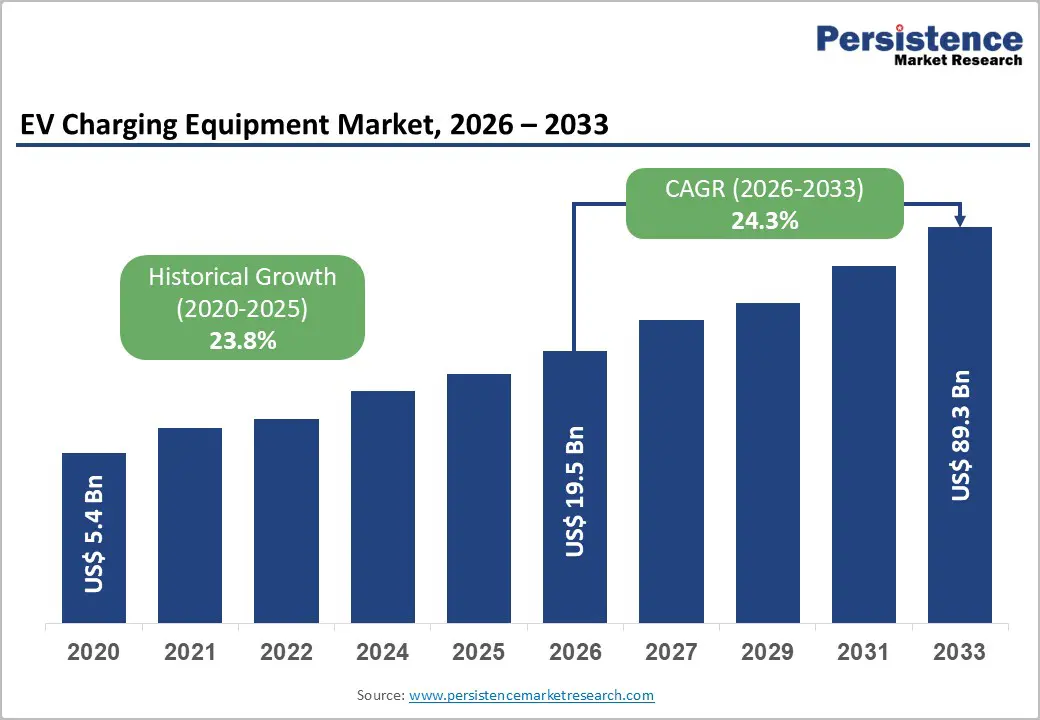

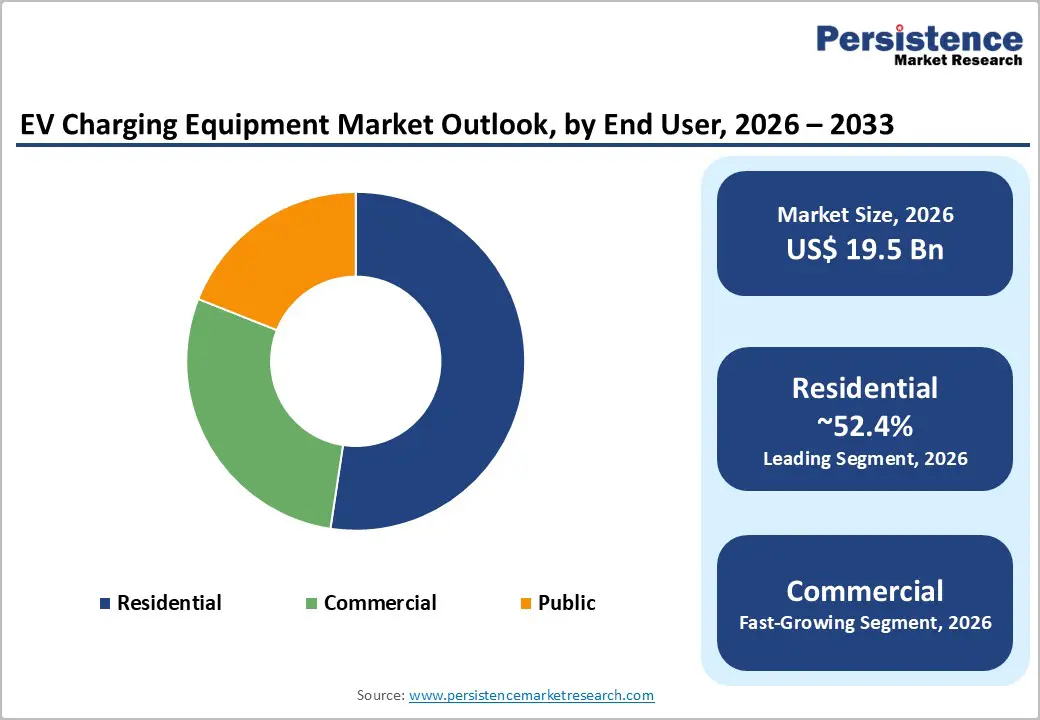

The global EV charging equipment market size is likely to be valued at US$19.5 billion in 2026 and is expected to reach US$89.3 billion by 2033, growing at a CAGR of 24.3% during the forecast period from 2026 to 2033, driven by the rising Electric Vehicle (EV) sales, supported by favorable policy incentives and stringent emission targets across key regions.

Governments are also investing in highway and urban charging networks to reduce range anxiety and support long-distance travel.

Key Industry Highlights:

- Leading Charging Type: Level 2 charging, approximately 33.1% share in 2026, as it provides a practical mix of affordability, easy installation, and sufficient charging speed for daily use.

- Dominant End-user: Residential, nearly 52.4% in 2026, spurred by government incentives and automaker support for home charger installation.

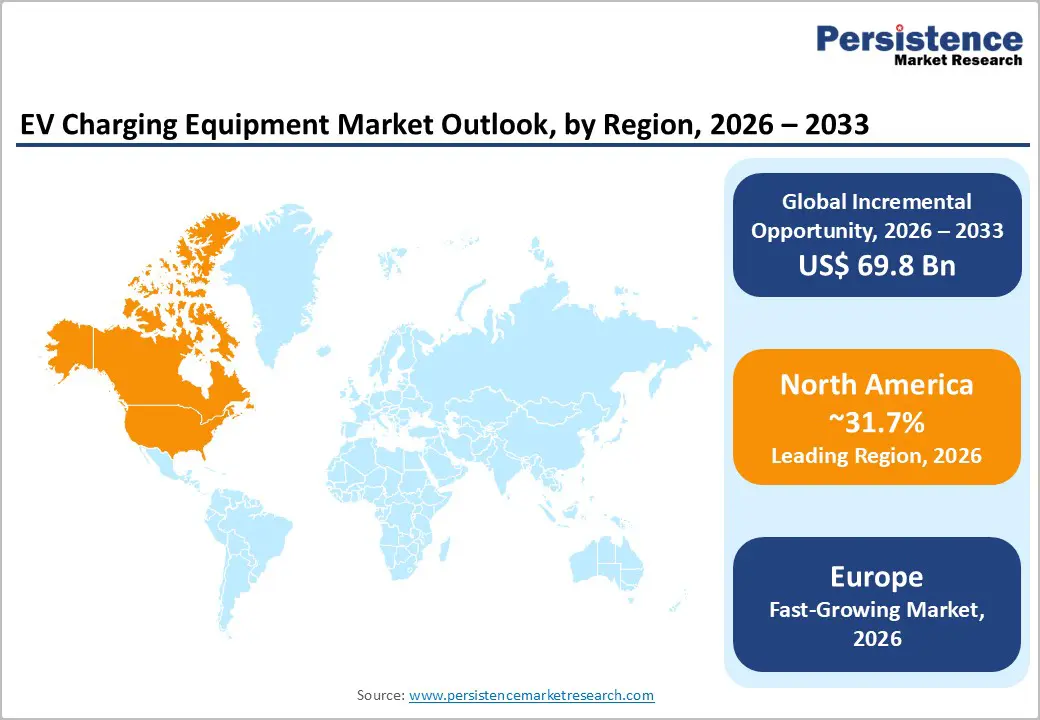

- Leading Region: North America, with about 31.7% share in 2026, backed by increasing federal funding programs and standardized charging frameworks.

- Fast-growing Region: Europe, owing to strict emission regulations and mandatory highway charging networks.

- Latest Charging Platform: In May 2026, ABB E-mobility launched the OM X-Series megawatt-scale charging platform designed for logistics hubs, transit depots, and heavy-duty EV corridors. The new liquid-cooled charging architecture can expand from 800 kW to over 10 MW across more than 100 charging points.

DRO Analysis

Driver - Increasing Adoption of Electric Vehicles Worldwide

The steady rise in EV adoption is driving a greater need for reliable charging infrastructure. Governments are backing this shift with superior policy support and transparent deployment targets. For instance, the International Energy Agency reported that global EV sales crossed 14 million units in 2023, and continued growth in 2025 is pushing utilities and private firms to extend charging networks quickly.

In India, the Ministry of Heavy Industries expanded the FAME-II scheme and sanctioned over 6,000 public charging stations across highways and cities. Automakers are also contributing by investing in charging ecosystems. Tata Motors has partnered with multiple charge point operators to improve access for its EV customers. This rising vehicle base is creating consistent demand for both AC and DC charging equipment.

Shift toward Low-Emission Mobility to Push Infrastructure Investments

The rising focus on clean mobility is pushing governments and corporations to invest in EV charging systems. Several countries have introduced strict emission targets that require parallel development of charging infrastructure. The European Commission, under its AFIR regulation, mandates fast chargers every 60 km on major highways. This is compelling the need for the speedy deployment of high-capacity charging equipment.

Corporations are also accelerating investments in EV infrastructure. Amazon, for example, is deploying EV chargers across its delivery hubs to support the transition of its logistics fleet to electric vehicles. At the same time, energy companies are increasingly combining renewable energy sources with charging networks to lower overall lifecycle emissions. This growing alignment between government policies and corporate sustainability initiatives is driving long-term demand for advanced and scalable EV charging solutions.

Restraint - High Operating Costs and Long Payback Periods

One key challenge is the difficulty in achieving stable returns for charge point operators. Setting up fast-charging stations requires high upfront investment in grid upgrades, hardware, and land. In various regions, electricity tariffs for commercial users remain high, which increases operating costs.

A report by the U.S. Department of Energy showed that demand charges can account for a large share of total electricity bills for fast-charging stations, especially when utilization is low. This creates uneven revenue streams. In India, operators have raised concerns about state-level tariff differences, which are affecting pricing models. Companies such as ChargePoint have also shifted focus toward software subscriptions to offset hardware margins. These financial pressures slow network expansion in less-dense areas.

Opportunity - Emergence of Ultra-Fast and Liquid-Cooled Charging Systems

The industry is moving toward high-power charging systems that reduce waiting time and improve efficiency. Liquid-cooled cables and modular designs are enabling chargers above 350 kW, especially for heavy-duty vehicles. Companies such as ABB E-mobility and Siemens are actively developing such systems for highways and fleet corridors.

In 2025, pilot projects in Europe demonstrated megawatt charging systems for electric trucks under initiatives supported by the European Union. These systems reduce heat losses and allow continuous high-power delivery. As charging time approaches refueling time, adoption barriers decrease, creating new growth potential for advanced EV charging equipment.

Corporate Electrification Goals to Open New Avenues

Large companies are setting clear decarbonization targets, which is creating demand for private and semi-public charging infrastructure. Several firms are electrifying their fleets and need dedicated charging setups. For instance, IKEA has committed to using only zero-emission delivery vehicles in various cities, leading to investments in depot charging systems.

The U.S. Environmental Protection Agency has also supported fleet electrification programs that include funding for charging infrastructure. This trend is creating opportunities for equipment suppliers to deliver customized solutions for logistics hubs, warehouses, and office campuses.

Category-wise Analysis

Charging Type Insights

The level 2 charging segment is estimated to dominate in 2026, with a share of about 33.1%. Level 2 chargers provide a practical balance between charging speed and installation cost. They are widely used in homes, workplaces, and public parking areas. They do not require major grid upgrades. The U.S. Department of Energy states that Level 2 chargers can add 25-30 miles of range per hour, which is sufficient for daily use. This makes them suitable for overnight home charging and long-duration parking at offices. Automakers such as Ford Motor Company and General Motors bundle Level 2 home chargers with EV purchases, which further supports adoption.

DC fast charging is expected to remain in second place as EV use expands beyond cities. These chargers can deliver 80% charge in under 30 minutes, making them ideal for highways and commercial fleets. The Federal Highway Administration is funding corridor-based charging networks under the NEVI program to ensure chargers are installed every 50 miles on key highways. In 2025, multiple states reported deploying high-power charging stations under this program. Companies such as Tesla are also opening their fast-charging networks to other brands, increasing accessibility and utilization.

End-user Insights

The residential segment is expected to lead with nearly 52.4% of the share in 2026, as most EV owners prefer charging at home. It is cost-effective and more convenient than public charging. The International Energy Agency notes that a large share of EV charging occurs at private residences worldwide. In markets such as the U.S. and Europe, governments provide subsidies for home charger installation. For example, the U.K.’s EV chargepoint grant supports the deployment of home chargers. This trend reduces dependency on public infrastructure and supports steady demand for residential charging equipment.

The commercial segment is expected to rank second in 2026 as businesses electrify fleets and install chargers for employees and customers. Logistics companies, ride-hailing services, and retail chains are investing in charging stations. Amazon has already deployed EV charging hubs to support its delivery fleet. The U.S. Environmental Protection Agency has also supported fleet electrification programs that include charging infrastructure. Workplaces are installing chargers to attract employees with EVs, increasing utilization rates during working hours.

Regional Insights

North America EV Charging Equipment Market Trends

In 2026, North America is predicted to dominate with approximately 31.7% of the share in 2026, owing to structured funding programs and private sector participation. The U.S. government has allocated billions under the Bipartisan Infrastructure Law for EV charging networks. The U.S. Department of Transportation oversees the rollout of national charging corridors. Private players such as ChargePoint and EVgo are also expanding their networks at a steady pace. This blend of policy and private investment is propelling large-scale deployment.

U.S. EV Charging Equipment Market Trends

The U.S. market is in an unmistakably strong growth phase, propelled by private investment more than federal policy. As of February 2026, the country has over 326,000 publicly accessible Level 2 and DC fast charging ports. It has added more than 18,000 new DC fast-charging ports in 2025, representing nearly 30% year-over-year growth, the largest single-year expansion in U.S. history. The Federal Highway Administration's pause of the NEVI program captured most industry headlines in 2025, yet the program and its funding would have only accounted for about 2 to 3% of the total new DCFC ports opened that year. Charge point operators were moving full steam ahead regardless.

The power output of new chargers is rising sharply. In Q1 2026, high-power chargers of 250 kW or more accounted for 55% of new non-Tesla deployments. The total average reached 67%, up from 62% at the end of 2025. Tesla is also ramping up deployment of 500 kW V4 Superchargers. A key structural shift is happening at the operator level. In 2025, Rivian, Mercedes-Benz HPC, Walmart, and bp pulse expanded their portfolios. These are companies whose primary business is not charging, but many have plans to open thousands of stations in North America by 2030.

Europe EV Charging Equipment Market Trends

Europe is anticipated to be the fastest-growing market over the forecast period. This is due to regulatory mandates and coordinated infrastructure planning. The Renewable Energy Directive III (RED III) requires member states to establish a marketplace where charge point operators can earn credits for supplying renewable electricity to EVs. Fossil fuel suppliers must buy these credits to offset emissions. This gives Charge Point Operators (CPOs) an entirely new revenue stream, improving their return on investment. The Alternative Fuels Infrastructure Regulation (AFIR) mandates fast-charging coverage along key transport corridors, de-risking large-scale projects for investors.

U.K. EV Charging Equipment Market Trends

The U.K. is building a large network, but the quality gap between what exists and what is required is the defining tension of its market at present. The number of public EV chargers in the country grew from 102,771 at the end of 2024 to 116,052 by the end of 2025, a 13% increase. As of April 2026, the network has reached 120,388 chargers at 46,333 locations. A milestone was crossed quietly in early 2026.

According to the U.K. Department for Transport's official January 2026 statistics release, the DfT confirmed that the number of public EV chargers has exceeded the number of petrol fuel pumps in the country. EV sales are also rising every year. New EV registrations reached 473,348 in 2025, making up 23.4% of all new car sales. However, structural challenges remain. Industry voices have pointed out that the U.K.'s energy cost for charging is higher than all countries in the EU, which raises running costs for both operators and drivers.

Germany EV Charging Equipment Market Trends

Germany's public charging network now comprises more than 200,000 charging points with an installed capacity of over nine gigawatts. Crucially, the expansion of charging infrastructure is outpacing the growth of the vehicle fleet. The country’s government published its Masterplan Ladeinfrastruktur 2030, one of Europe's most detailed national charging blueprints.

The plan guarantees fast-charging coverage every 60 km on TEN-T (Trans-European Transport Network) routes through the Deutschlandnetz initiative. It aims to effectively de-risk high-power projects for private investors. It also targets one million fully accessible and operational charge points nationwide by 2030.

Asia Pacific EV Charging Equipment Market Trends

Asia Pacific is seeing significant growth, backed by constant government intervention, especially in China and India. China leads in charger deployment through state-backed companies and urban planning. The National Development and Reform Commission has supported large-scale charging infrastructure rollout. High EV adoption in cities is pushing demand for both public and private chargers.

Japan EV Charging Equipment Market Trends

Japan’s growth is steady but focused on improving charger reliability and novel technologies. The Ministry of Economy, Trade and Industry is supporting upgrades of aging CHAdeMO chargers and promoting ultra-fast charging systems. Automakers are also exploring battery swapping and smart charging solutions. This focus on quality over quantity is shaping the market.

India EV Charging Equipment Market Trends

India is gradually broadening its EV charging infrastructure with superior government backing. The Ministry of Heavy Industries has sanctioned thousands of public charging stations under the FAME scheme. Oil marketing companies such as Indian Oil Corporation are installing charging stations at fuel stations along highways. Urban centers, including Delhi and Mumbai, are also seeing increased deployment of public chargers. This steady rollout is supporting early-stage EV adoption.

Competitive Landscape

The global EV charging equipment market is highly fragmented, although consolidation is gradually increasing in the fast-charging and network management segments. Leading players include Tesla, ABB, ChargePoint, Siemens, Wallbox, Blink Charging, EVBox, Delta Electronics and China-based firms such as TELD and Star Charge. Tesla has emerged as one of the strongest competitive forces globally due to its Supercharger reliability, proprietary software ecosystem, and growing influence of the North American Charging Standard (NACS).

Competition is intense in DC fast charging, where uptime, charging speed, and expandability are becoming key differentiators. ABB, Alpitronic, Tritium, Siemens, and SK Signet are investing heavily in ultra-fast chargers above 350 kW, liquid-cooled cables, and megawatt charging systems for electric trucks and fleets. Oil majors such as Shell and BP have also acquired charging companies to diversify beyond fossil fuels.

Key Industry Developments:

- In March 2026, Electreon acquired U.S.-based InductEV to strengthen its wireless EV charging portfolio. The acquisition combined Electreon’s dynamic wireless charging technology with InductEV’s high-power stationary charging systems for transit buses and heavy-duty electric trucks.

- In March 2026, CATL accelerated the expansion of its battery swap infrastructure ecosystem in China, announcing plans to build more than 3,000 battery swap stations by the end of 2026. The expansion was supported by new battery-swappable EV models from GAC Aion and BAIC Arcfox.

- In September 2025, Exponent Energy launched its P4 EV charging station in India, capable of fully charging EVs in approximately 15 minutes. The compact charging solution was designed specifically for dense urban deployments and included advanced thermal management and retractable cable systems.

Companies Covered in EV Charging Equipment Market

- Tesla

- ABB

- Siemens

- Schneider Electric

- Electrify America

- Blink Charging

- EVBox

- Wallbox

- Others

Frequently Asked Questions

The global EV charging equipment market is projected to be valued at US$19.5 billion in 2026.

The EV charging equipment market is expected to reach US$89.3 billion by 2033.

Key market trends include the shift toward ultra-fast charging systems and the integration of smart energy management software.

The residential segment is projected to lead with nearly 52.4% of the share in 2026, as most EV users prefer overnight home charging.

The EV charging equipment market is expected to grow at a CAGR of 24.3% from 2026 to 2033.

Tesla, ABB, Siemens, and Schneider Electric are a few key market players.