- Renewable Energy

- Fuel Station Market

Fuel Station Market Size, Share, and Growth Forecast, 2025 - 2032

Fuel Station Market By Fuel Type (Gasoline/Petrol, Diesel, Others), Ownership (Company-Operated, Dealer/Branded-Dealer), Service Format, End-User and Regional Analysis for 2025 - 2032

Fuel Station Market Size and Trends Analysis

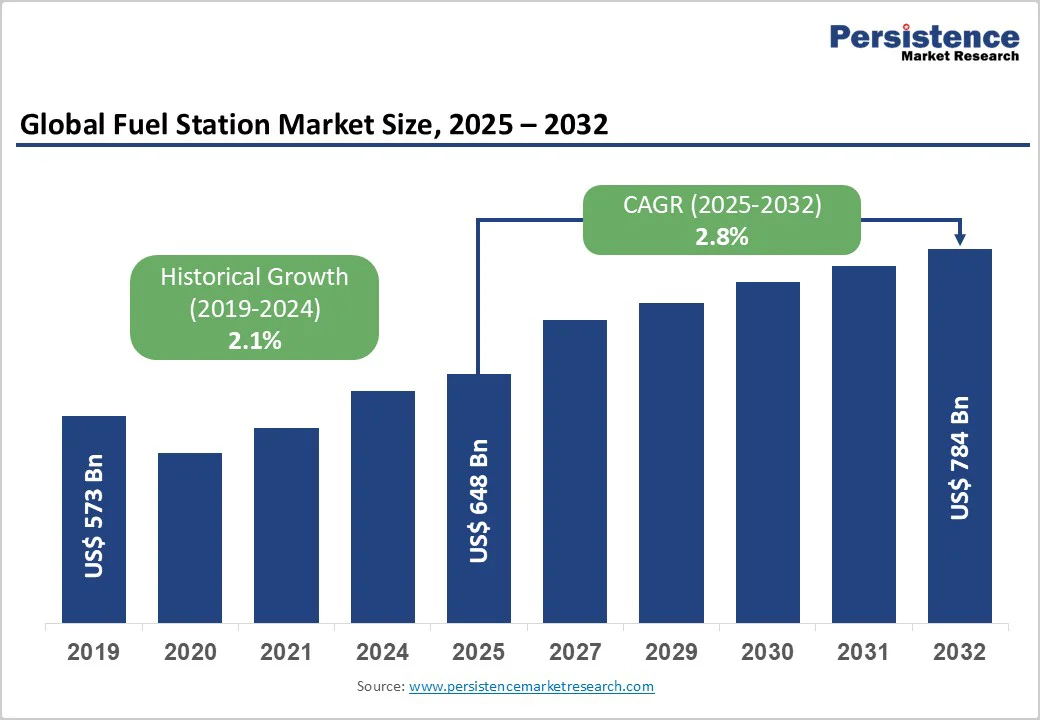

The global fuel station market is likely to be valued at around US$648 billion in 2025 and is expected to reach around US$784 billion by 2032-35, growing at a CAGR of 2.8% during 2025 - 2032.

Key growth factors include rising vehicle fleets and freight activity in developing economies, stable consumer fuel demand in major transport regions, and the ongoing modernization of stations into multi-service hubs, all of which are supporting steady market expansion. Parallel investments in EV fast-charging, CNG, and biofuel integration are reshaping station infrastructure, adding a new growth vector beyond traditional fuels.

Key Industry Highlights

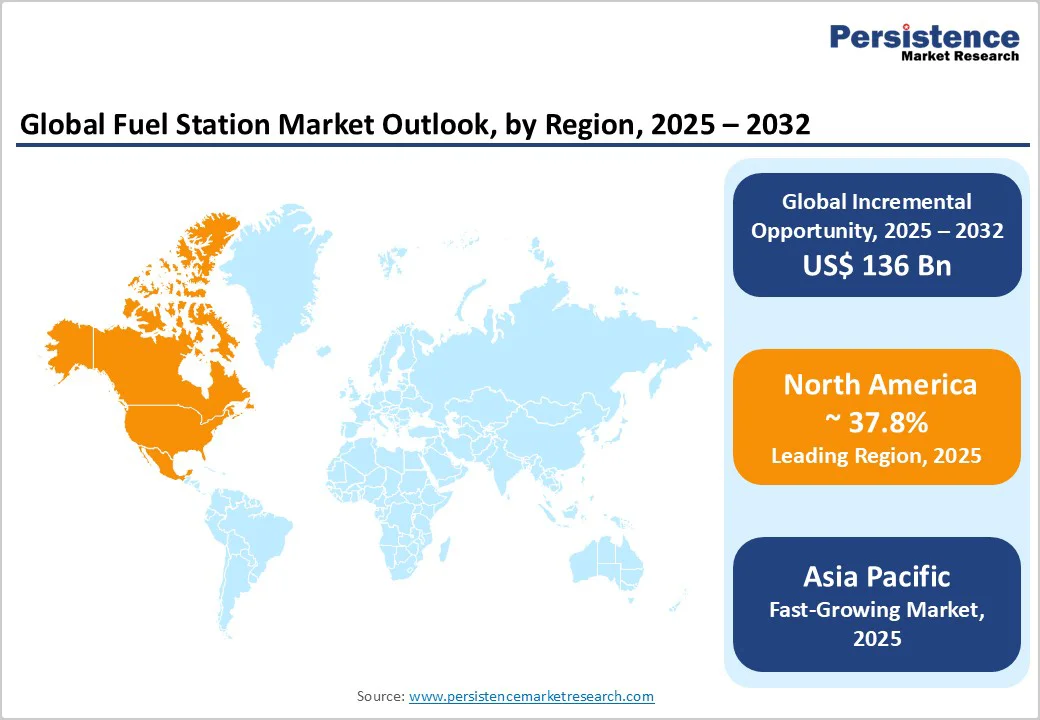

- Leading Region: North America dominates the global market, accounting for over 37.8% of total market value in 2025, supported by more than 121,000 operational fuel stations, strong convenience retail margins, and extensive highway infrastructure.

- Fastest-growing Region: Asia Pacific, driven by surging vehicle ownership, infrastructure expansion in China and India, and rapid adoption of CNG, biofuels, and EV-charging solutions.

- Investment Plans: Major oil and energy companies are investing heavily in EV-charging and smart forecourt modernization, with projects such as Shell-Duke Energy’s fast-charging corridors in the U.S. and Sinopec’s 20,000 integrated fuel-and-charging sites in China planned by 2030.

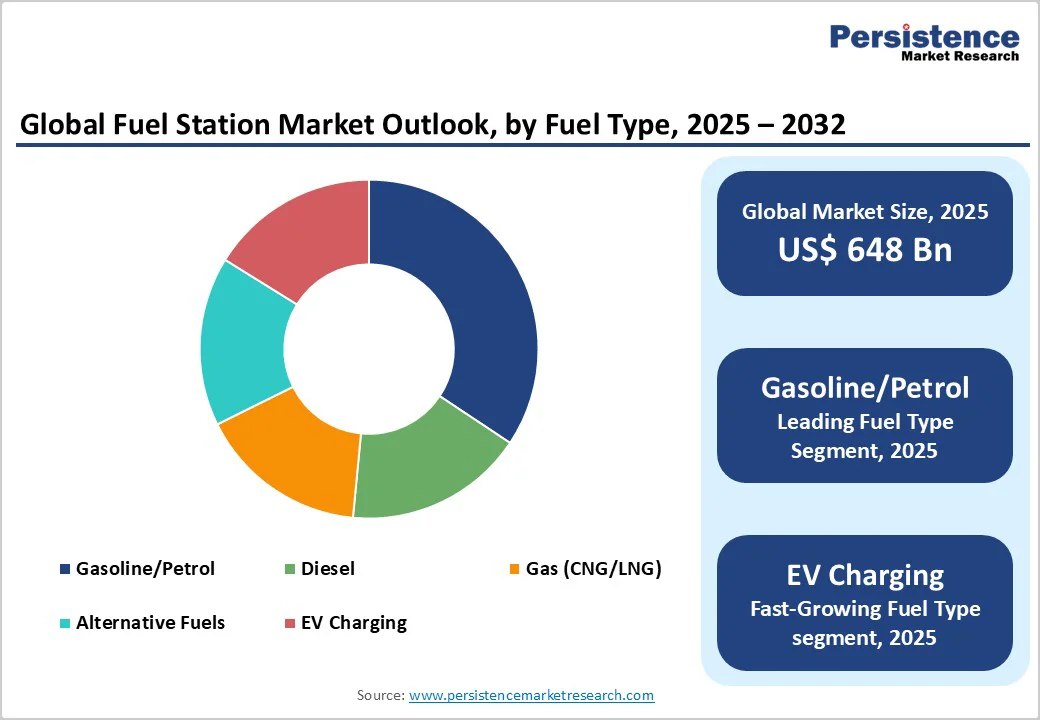

- Dominant Fuel Type: Gasoline remains the leading fuel type, contributing around 34% of total global market revenue in 2025. Its dominance is driven by widespread passenger-vehicle ownership

- Leading Service Format: Convenience-integrated stations represent the leading service format, generating over 55% of site EBITDA through non-fuel transactions, including retail, foodservice, and digital engagement.

| Key Insights | Details |

|---|---|

| Fuel Station Market Size (2025E) | US$648 Bn |

| Market Value Forecast (2032F) | US$784 Bn |

| Projected Growth (CAGR 2025 to 2032) | 2.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Steady demand from vehicle fleets and road transport growth

Global road transport continues to anchor the retail fuel market. Expanding vehicle ownership in emerging economies, particularly across Asia-Pacific, sustains fuel throughput. The United States alone hosts over 121,000 fuel stations, while China’s network surpasses 100,000, ensuring stable infrastructure revenue.

This entrenched base of operating sites secures predictable low-single-digit growth even as electrification rises. Core gasoline and diesel demand remains resilient, maintaining the backbone of station revenue streams through 2032.

Diversification into non-fuel revenue streams

Fuel retailers are increasingly generating revenue through convenience retailing, foodservice, and car wash facilities. These additions can account for over 40-60% of forecourt EBITDA in mature markets.

Stations are evolving into mobility and lifestyle hubs, where customer dwell times and spend-per-visit rise significantly. Capital investments are flowing into store fit-outs, refrigeration, POS, and digital loyalty platforms, creating measurable growth for associated service and equipment providers.

Infrastructure transition toward multi-energy offerings

Oil majors and large network operators are incorporating EV fast-charging, hydrogen, RNG, and CNG into their forecourts. This transition is evident in large-scale partnerships and acquisitions, transforming traditional stations into multi-energy hubs. Such diversification creates a new revenue layer, per-kilowatt-hour sales, grid services, and customer retention via charging-linked loyalty programs, driving long-term CAPEX in high-power equipment and grid connectivity.

Declining liquid fuel demand due to EV adoption

As electric vehicle penetration accelerates across Europe, China, and North America, gasoline and diesel throughput per site faces gradual erosion. Regions where EVs represent over 20-30% of new vehicle sales are already observing annual volume declines of 1-3% at traditional forecourts. Operators without diversification into EV charging or retail formats risk declining margins and asset underutilization within the decade.

High CAPEX and regulatory hurdles in site upgrades

Modernizing existing stations, including installing EV chargers, hydrogen pumps, or underground tank replacements, entails heavy upfront investment. Urban locations often face zoning, environmental, and grid-connection challenges. When permitting and grid upgrades add 20-30% to project costs, rollout pace slows. Many independents defer conversions unless supported by government subsidies or joint-venture financing models.

Forecourt electrification and high-power charging infrastructure

The transition to electric mobility is generating a multi-billion-dollar opportunity in station equipment and installation services. The gas-station equipment market alone is estimated near US$ 50.5 billion in 2025, underscoring the scale of retrofit activity. Stations that position themselves as EV fast-charging hubs can achieve higher per-customer margins, combining charging revenue with retail spend.

Expansion in emerging markets and alternative fuels

Asia-Pacific and Latin America still experience vehicle-fleet growth and underdeveloped station density, creating significant white spaces for new deployments. Government incentives promoting CNG, RNG, and biofuels further boost investment attractiveness. Well-timed entry into these markets can add low-to-mid single-digit revenue growth annually for forecourt operators, particularly those integrating low-carbon fuels with traditional offerings.

Category-wise Analysis

Fuel Type Insights

Gasoline continues to dominate the global fuel-station market, contributing to 34% of total revenue. Its dominance is underpinned by the sheer scale of passenger-vehicle ownership in the United States, Europe, and India, where petrol vehicles make up nearly 65-70% of the active fleet.

The segment remains a critical profit driver for major oil companies and independent operators, providing stable throughput even in regions where electric vehicle adoption is accelerating. For example, Shell and ExxonMobil continue to generate robust margins from premium gasoline offerings such as Shell V-Power and Mobil Synergy, both of which leverage fuel-additive branding to maintain pricing power.

In India, Indian Oil Corporation and Bharat Petroleum are expanding their retail footprints, targeting over 30,000 active petrol forecourts to serve growing urban demand.

The EV charging category, and high-power EV chargers, is the fastest-expanding segment within the fuel station market. Developed economies such as the United Kingdom, Germany, and the Netherlands are witnessing double-digit annual growth in EV charger deployment, particularly high-power chargers (HPCs) capable of delivering 150-350 kW.

Major forecourt operators are rapidly adapting: BP Pulse has already installed over 29,000 charging points globally, while TotalEnergies aims to deploy 150,000 EV chargers by 2030 under its “multi-energy” roadmap. In Asia, China Petroleum & Chemical Corporation (Sinopec) operates hybrid stations combining fuel, CNG, and EV charging bays, positioning itself as a mobility-energy provider.

Service Format Insights

Convenience-integrated stations represent the largest service format, capturing a growing share of 55% through retail, foodservice, and digital engagement. In mature markets, 40-60% of site EBITDA now comes from non-fuel transactions, reflecting a structural shift toward consumer-centric mobility hubs.

Companies such as Alimentation Couche-Tard (Circle K), BP, and EG Group have built extensive networks combining branded fuel dispensing with coffee bars, quick-serve food counters, and grocery outlets. For example, Shell Select and BP Connect stores in Europe report consistent revenue growth from food and beverage sales, outpacing traditional fuel margins.

Similarly, Indian Oil’s “XtraCare” stations and HPCL’s Club HP outlets in India are incorporating co-branded cafés, Wi-Fi zones, and digital payment kiosks to attract younger, tech-savvy consumers. This retail-integrated model not only stabilizes profitability amid volatile fuel prices but also creates strong brand stickiness.

Operators are increasingly investing in automated checkout systems, loyalty apps, and energy-efficient store design, which enhance customer retention and operational efficiency.

The multi-energy hub model, encompassing EV fast-charging, CNG, biofuel, and hydrogen refueling, is experiencing the highest growth trajectory in both developed and emerging markets. These hybrid forecourts exemplify the transition toward low-carbon mobility infrastructure, blending traditional and renewable energy delivery.

Governments across Europe and Asia are channeling funds into highway electrification and hydrogen corridor programs. For instance, the EU’s Alternative Fuels Infrastructure Regulation (AFIR) mandates installation of HPC chargers every 60 km along major routes, while India’s National Hydrogen Mission promotes co-located hydrogen dispensers within existing stations.

TotalEnergies’ Source network, a joint venture with SSE in the UK, is developing 3,000 ultra-fast chargers by 2030, converting legacy fuel sites into fully electrified hubs. Likewise, Shell Recharge sites in the Netherlands and BP Pulse hubs in Germany demonstrate scalable hybrid energy layouts combining fast charging with convenience retail and rest areas.

Regional Insights

North America Fuel Station Market Trends-Modernization, Multi-Fuel Integration, and Electrification Transition

North America, led by the United States, represents 37.8% of share of the global fuel-station market, supported by an extensive network of over 121,000 operational sites. The region’s vast highway infrastructure, freight corridors, and commuter population sustain robust baseline demand. Non-fuel revenues, especially from convenience retail, food services, and digital payment solutions, contribute significantly to station profitability.

The United States continues to outperform in both site density and per-station revenue, driven by the growth of e-commerce logistics and last-mile delivery fleets that are fueling diesel and fleet-charging demand. Canada, meanwhile, has emerged as a leader in Compressed Natural Gas (CNG) and Renewable Natural Gas (RNG) adoption, particularly within municipal and heavy-duty transport fleets.

In terms of regulation, federal tax credits for EV infrastructure, such as those under the U.S. Inflation Reduction Act (IRA), and state-level clean-fuel standards continue to attract investment into high-power charging networks.

Investment trends reveal modernization across the retail network, including forecourt automation, contactless payment systems, and multi-fuel site layouts. Large-scale collaborations between oil majors and utilities underscore the region’s long-term pivot toward electrification.

For example, in June 2025, Shell USA partnered with Duke Energy to co-develop a network of fast-charging corridors across key freight routes, integrating smart energy management systems. Similarly, BP expanded its Pulse charging network across major metropolitan areas in North America, enhancing the integration of EV-charging infrastructure into existing forecourt designs.

Europe Fuel Station Market Trends -HPC Expansion, Public-Private Partnerships, and Low-Carbon Mobility

Europe hosts one of the world’s most technologically advanced and dense fuel-station networks, with Germany, France, the U.K., and Spain serving as primary contributors. The regional market is undergoing a rapid shift toward zero-emission mobility, underpinned by public tenders and private investments aimed at installing high-power chargers (HPC) across strategic routes.

Germany’s Deutschlandnetz initiative granted contracts for over 1,100 HPC stations to TotalEnergies in 2024, signaling significant public commitment to decarbonization. In the U.K., joint ventures are reshaping the retail landscape; for instance, TotalEnergies and SSE Renewables’ “Source” partnership plans to deploy up to 3,000 HPC sites by 2030, focusing on motorway corridors and urban hubs.

The region’s growth is driven by stringent EU CO2 and emission regulations, which accelerate fleet electrification, government tenders that support nationwide HPC rollouts, and a growing consumer preference for low-carbon mobility solutions. Investment patterns in Europe favor public-private partnerships and joint ventures between energy utilities and oil majors.

A notable example includes BP’s collaboration with Iberdrola in 2025, aimed at expanding a network of 11,000 HPC chargers across Spain and Portugal by 2030. Similarly, Shell Recharge has been scaling its European network, with a focus on integrating renewable energy sourcing. These efforts demonstrate commercial viability while establishing scalable models for future HPC expansion across the continent.

Asia Pacific Fuel Station Market Trends -Infrastructure Growth, Green-Fuel Adoption, and EV Network Acceleration

Asia Pacific stands out as the fastest-growing regional market, propelled by rapid urbanization, surging vehicle ownership, and significant investments in transport infrastructure. China and India together account for the highest number of fuel stations globally, reflecting their vast automotive markets and expanding middle-class base.

China’s network is maturing yet remains dynamic, with EV integration and smart-charging infrastructure expanding under national programs. India continues to grow its network, driven by petrol and diesel demand, though it is simultaneously scaling biofuel blending and CNG corridor initiatives.

Japan leads in hydrogen-fuel and hybrid technologies, supported by long-standing government programs such as the Basic Hydrogen Strategy, while ASEAN countries, including Indonesia, Thailand, and Malaysia, are piloting electrification projects and increasing private participation in retail energy distribution.

Regulations vary significantly across markets, some prioritize EV infrastructure expansion, while others focus on biofuel mandates and local-content rules guiding foreign investment. For example, India’s 2025 Green Mobility Mission incentivizes EV-charging infrastructure at petrol stations, whereas Indonesia’s Ministry of Energy and Mineral Resources continues to promote B40 biodiesel adoption through subsidies and tax exemptions.

Investment activity across Asia Pacific is intensifying, especially in green-fuel deployment and EV-ready infrastructure. In April 2025, Sinopec launched a joint venture with State Grid Corporation of China to build 20,000 integrated fuel and charging stations by 2030, combining traditional refueling, EV-charging, and retail convenience formats.

Competitive Landscape

The global fuel-station market remains moderately concentrated, with state-owned and integrated oil companies controlling significant national shares, while independent dealer networks dominate regional site counts. Leading international players such as Shell, BP, TotalEnergies, ExxonMobil, and Sinopec continue to shape the competitive dynamics through cross-regional investments, technology adoption, and branding strategies.

Convenience retail specialists, including Alimentation Couche-Tard (Circle K), are expanding their presence by focusing on customer-experience differentiation, loyalty ecosystems, and quick-service food offerings. Meanwhile, oil majors are diversifying into electric mobility and alternative fuels to balance short-term fuel profitability with long-term sustainability goals.

Key strategic developments reinforce this transition. In May 2025, Shell announced the completion of 1,000 public fast chargers across Europe, integrating renewable power sources. BP Pulse partnered with Uber in February 2025 to expand fast-charging hubs for ride-share fleets in key U.S. cities. These initiatives highlight the industry’s strategic shift toward electrification, retail innovation, and digital engagement, marking a decisive move beyond conventional refueling operations.

Key Industry Developments

- In July 2024, TotalEnergies and SSE launched a joint venture “Source” to build up to 3,000 ultra-fast chargers across the U.K. and Ireland. This model integrates utility expertise with oil-major retail networks, setting a benchmark for corridor electrification.

- In January 2024, TotalEnergies acquired 200 Wenea ultra-fast charging stations in Spain, expanding its charging network and consolidating its position in Europe’s EV infrastructure market.

- In April 2025, Source opened its first branded HPC hub in Edinburgh, signaling operational rollout from planned tender to active network.

Companies Covered in Fuel Station Market

- Shell plc

- BP plc

- TotalEnergies SE

- ExxonMobil Corporation

- Chevron Corporation

- Sinopec Group

- PetroChina Company Limited

- Saudi Aramco

- Indian Oil Corporation Limited

- Bharat Petroleum Corporation Limited (BPCL)

- Hindustan Petroleum Corporation Limited (HPCL)

- ENEOS Holdings, Inc.

- PTT Public Company Limited

- Repsol S.A.

- Eni S.p.A.

- Phillips 66

- Marathon Petroleum Corporation

- Valero Energy Corporation

- Petronas

- Couche-Tard Inc. (Circle K)

Frequently Asked Questions

The global fuel station market is valued at US$648 billion in 2025.

By 2032, the market is projected to reach US$784 billion, registering a compound annual growth rate (CAGR) of 2.8% between 2025 and 2032.

Key trends include the integration of EV-charging infrastructure, growth in non-fuel revenue streams (foodservice and retail), automation and digital payments, and the emergence of multi-energy hubs offering hydrogen, CNG, and renewable fuels alongside traditional fuels.

Gasoline/Petrol remains the dominant fuel type, contributing over one-third of global revenue due to widespread passenger vehicle ownership in the U.S., Europe, and India.

The global market is expected to expand at a CAGR of 2.8% from 2025 to 2032.

Major companies include Shell plc, BP plc, TotalEnergies SE, ExxonMobil Corporation and Sinopec Group.