- Oil & Gas

- Jet Fuel Market

Jet Fuel Market Size, Share, and Growth Forecast, 2025 - 2032

Jet Fuel Market By Fuel Type (Conventional Aviation Fuel, Sustainable Aviation Fuel (SAF)), Application (Commercial Aviation, Military Aviation, General Aviation), End-user (Airlines, Air Cargo Carriers, Private Jet Operators, Armed Forces), and Regional Analysis for 2025 - 2032

Jet Fuel Market Share and Trends Analysis

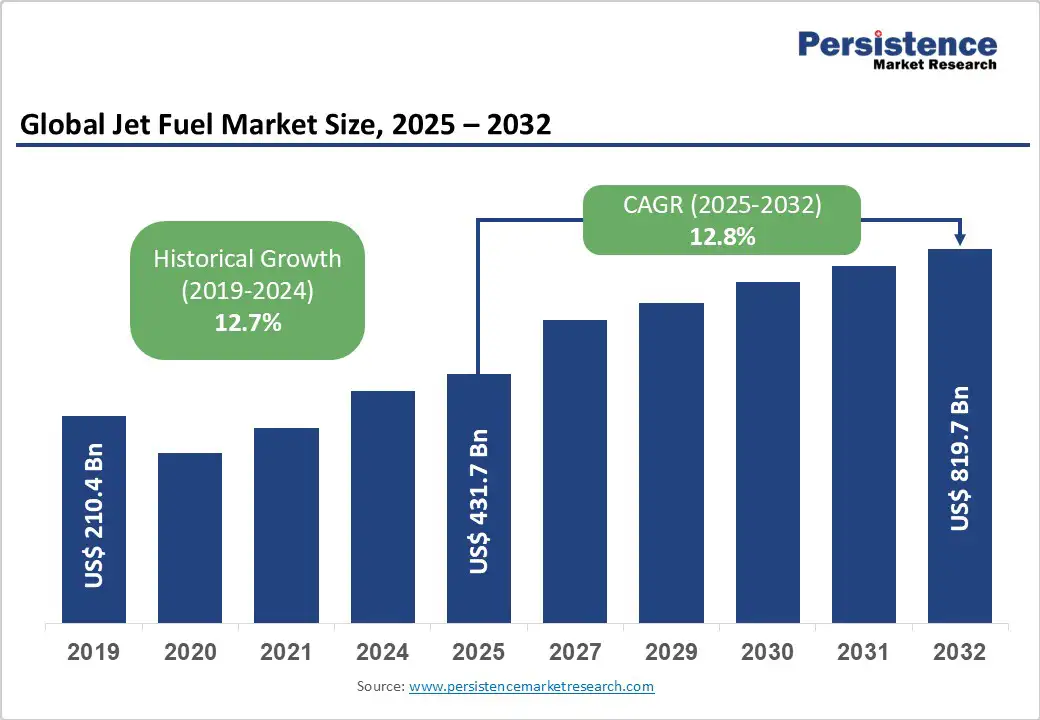

The global jet fuel market size is likely to be valued at US$431.7 Billion in 2025, and is estimated to reach US$819.7 Billion by 2032, growing at a CAGR of 12.8% during the forecast period 2025 - 2032, driven by rising air travel demand, the expansion of commercial airlines, especially in developing economies, and increasing investments in airport infrastructure.

The perceptible shift toward sustainable aviation fuels (SAF) is opening lucrative avenues, with SAF poised for substantial technological and market adoption advances.

Key Industry Highlights

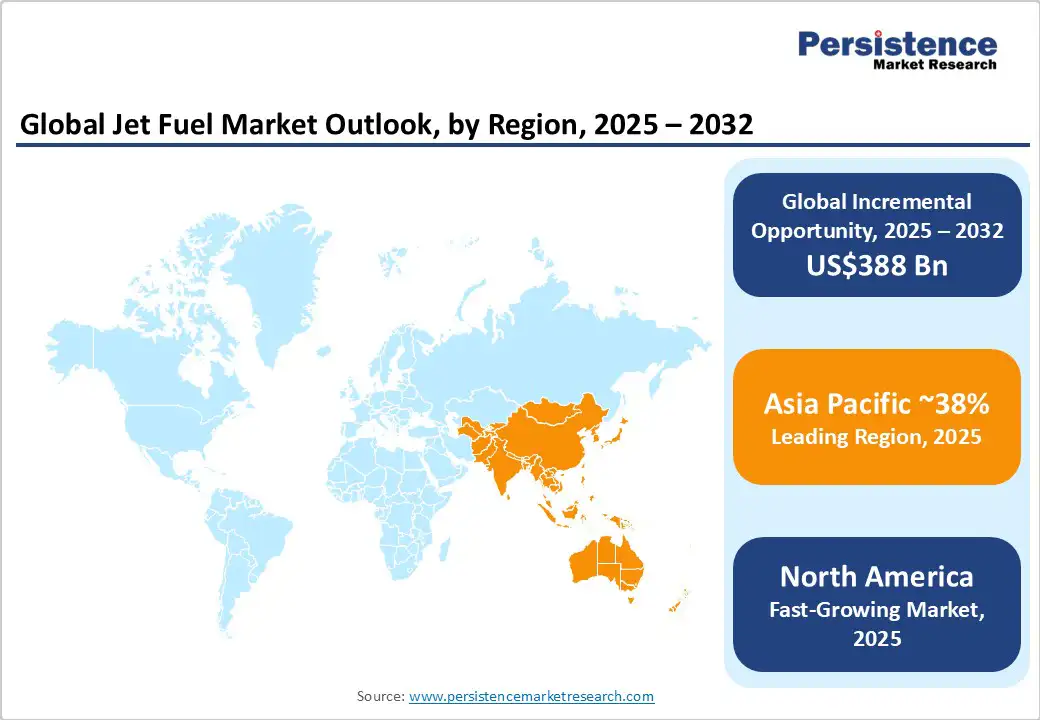

- Dominating Region: Asia Pacific dominates the market with a 38% share in 2025, driven by increasing air passenger traffic and infrastructure investments.

- Fastest-Growing Fuel Type: Sustainable aviation fuel (SAF) is the fastest-growing segment, propelled by regulatory support and airline commitments.

- Leading Fuel Type: Conventional jet fuel retains the largest current market share at approximately 95% in 2025, maintaining volume dominance despite gradual SAF penetration.

- Fastest-growing region: North America is anticipated to grow at the highest CAGR through 2032.

- Key development: In September 2025, Delta Air Lines partnered with Dutch startup Maeve Aerospace to help develop the MAEVE Jet, a hybrid-electric regional aircraft designed to deliver up to 40% fuel and emissions reduction compared with jets using conventional jet fuel, with reductions possible using SAF.

| Key Insights | Details |

|---|---|

| Jet Fuel Market Size (2025E) | US$431.7 Bn |

| Market Value Forecast (2032F) | US$819.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 12.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 12.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Air Travel and Cargo Traffic

Global passenger air traffic is expanding rapidly, with the International Air Transport Association (IATA) forecasting a 3.8% annual increase leading to over 4 billion additional journeys by 2043 compared to 2023. This growth is driven by improving connectivity, affordable pricing, and rising disposable incomes across Asia Pacific, the Middle East, and developing regions.

Concurrent growth in air cargo, fueled by booming e-commerce and pharmaceutical logistics, is significantly raising jet fuel consumption. Airlines are expanding fleets and flight frequencies to accommodate this surge, directly increasing fuel demand. For example, North American airlines recorded a 203.4% increase in traffic by May 2022 relative to 2021, demonstrating strong recovery momentum and a fuel consumption uptick.

The drive toward reducing the carbon footprint of the aviation industry is accelerating sustainable fuel adoption. SAF production technologies such as hydrothermal liquefaction and ethanol-to-jet (ETJ) fuel conversion are gaining traction, supported by key industry partnerships and government incentives.

SAF can reduce carbon emissions by up to 80% compared to conventional jet fuel, aligning with international regulations such as CORSIA under the International Civil Aviation Organization (ICAO) and the Fit for 55 initiative of the European Union (EU).

Companies such as Honeywell and Microsoft are innovating to scale low-cost, low-carbon jet fuels. Increasing airline commitments and regulatory support create considerable growth opportunities, positioning SAF as the fastest-growing fuel type segment.

Volatility in Crude Oil Prices Impacting Aviation Fuel Costs

The jet fuel market growth is highly sensitive to Brent crude oil price fluctuations; as jet fuel is derived from crude oil. Geopolitical events, supply cuts by major oil producers such as members of the Organization of the Petroleum Exporting Countries (OPEC), and uneven global economic recoveries induce price volatility.

Crude oil constitutes around 30-40% of airline operational costs, making fuel price surges impactful on ticket pricing, profitability, and demand. For instance, Saudi Arabia's recent production cuts, aimed to balance supply amid a fragile global economy, have increased fuel costs.

Price spikes constrain air travel affordability, especially in price-sensitive regions such as Asia Pacific and Africa, restricting market growth and prompting airlines to reconsider network expansions or investments.

Fuel supply is also highly vulnerable to geopolitical tensions, natural disasters, labor actions, and refinery constraints that disrupt production, distribution, or transportation. These interruptions not only increase fuel costs through scarcity but also affect airline operational efficiency and budgeting certainty.

The specialized feedstock requirements and nascent production infrastructure for SAF exacerbate supply fragility. Limited SAF availability slows adoption despite growing demand, slowing sustainability progress and weakening investor confidence. Persistent supply chain risks complicate infrastructure investments and long-term strategic planning for fuel producers and airlines alike.

Emergence of SAF as a Market Disruptor

SAF represents a transformative opportunity to capitalize on global decarbonization mandates and airline sustainability commitments. Government incentives such as the tax credits extended in the U.S. and the EU are improving the production capacity and cost competitiveness of SAF.

The global SAF market is projected to grow at an exceptionally high CAGR, with projected volumes surpassing 6.4 billion gallons. This expansion is expected to spur investment in feedstock cultivation, supply chain development, and refining capacity. For investors and fuel producers, accelerating SAF innovation and commercialization can generate strong returns by capturing emerging market share and aligning with regulatory frameworks.

Asia Pacific’s rapid economic growth, expanding middle class, and rising air travel are driving demand for sustainable aviation fuels. Government investments in airport infrastructure and supportive policies in China, India, Japan, and ASEAN nations are boosting regional fuel production and distribution.

Advancements in catalytic refining, hydrothermal liquefaction, and waste-to-fuel technologies are enabling cleaner, more efficient fuels, enhancing performance, lowering emissions, and improving cost competitiveness across the aviation sector.

Category-wise Analysis

Fuel Type Insights

Conventional jet fuel, also known as aviation turbine fuel (ATF), continues to dominate, holding about 95% of the market revenue share in 2025. This predominance is driven by its widespread use in commercial airliners, military aviation, and cargo fleets, supported by well-established supply chains and refueling infrastructure worldwide.

While the COVID-19 pandemic caused significant, albeit temporary, disruptions in air travel and fuel demand, the sector is recovering rapidly. Industry forecasts suggest a full rebound to pre-pandemic fuel consumption levels by the mid-2020s, fueled by renewed passenger confidence, airline fleet expansions, and growing cargo operations.

Sustainable aviation fuel (SAF) is poised to emerge as the fastest-growing fuel segment, with a robust CAGR projected through 2032. Government policies incentivizing low-carbon technologies, such as the U.S. Renewable Fuel Standard and the European Union’s RED II framework, are pivotal in accelerating SAF adoption.

Airlines in North America and Europe are committing to ambitious emissions reduction targets, integrating SAF blends into their fuel mix to offset carbon footprints. This evolving dynamic results in a dual-market structure where conventional jet fuel retains near-term volume dominance, while SAF represents a rapidly expanding opportunity, attracting substantial investments in feedstock development, production capacity, and distribution infrastructure.

Application Insights

The commercial aviation sector is projected to lead fuel consumption with an estimated 78% market share in 2025. Growth drivers include expanding airline fleets, increasing passenger traffic, particularly across fast-growing regions such as Asia Pacific and the Middle East, and diversification of route networks, including the rising prominence of long-haul and ultra-long-haul flights.

Besides this, evolving tourism trends, such as sports tourism and experiential travel, are further stimulating demand. The sector’s reliance on consistent, high-volume jet fuel underscores its critical role as the linchpin of the aviation fuel market.

Military aviation remains a significant and stable fuel consumer segment, expected to register a steady CAGR from 2025 to 2032. This growth is underpinned by ongoing defense budget allocations in key regions such as the U.S. and Europe and expanding deployment of advanced aircraft requiring reliable fuel supplies.

The private aviation segment, while smaller in volume, is one of the fastest-growing drivers, propelled by increasing discretionary income, rising numbers of private jet owners, and evolving lifestyle preferences. This niche is influencing evolving fuel consumption patterns, as governments and industry players expand focus on green technologies, including sustainable fuel blends and electric propulsion, across all aviation application sub-segments.

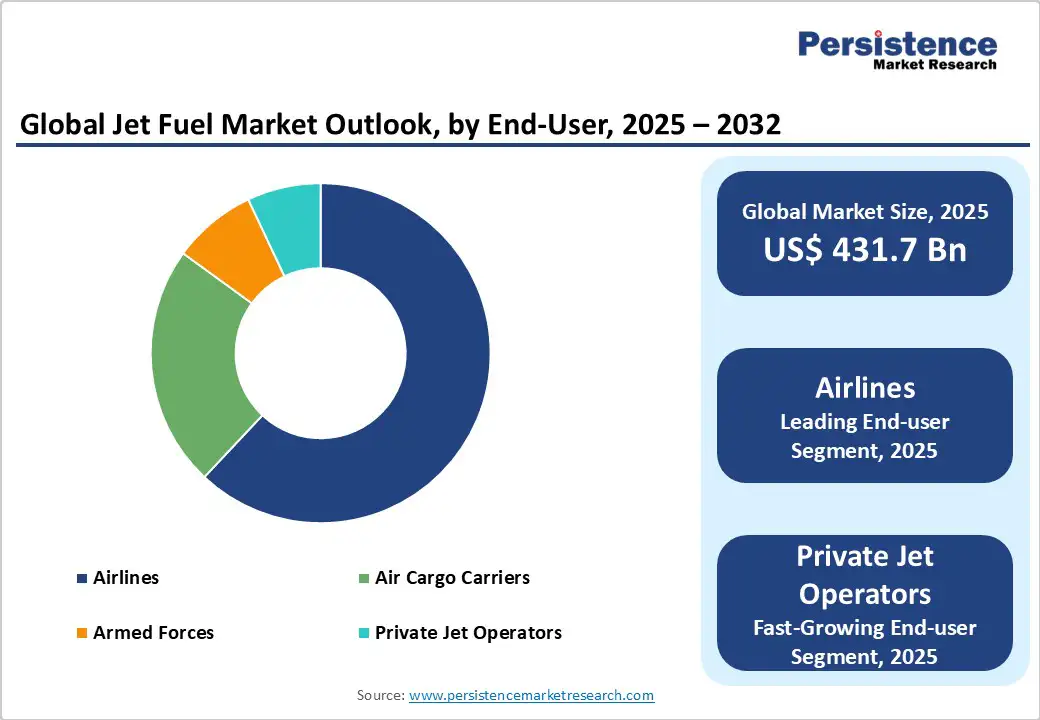

End-user Insights

Airlines will dominate the jet fuel end-user category, capturing an estimated 83% of the market revenue in 2025, driven by their sizeable commercial and cargo fleets. The rapid expansion of e-commerce and global supply chains is increasing freight demand, thereby elevating jet fuel consumption in the cargo sector.

Although smaller in volume, government and military users remain crucial actors, not only ensuring strategic fuel reserves but also frequently serving as testbeds for fuel efficiency and sustainable technology adoption, influencing broader market trends.

Private jet operators represent an emerging and promising growth cluster, projected to achieve a notable CAGR through 2032. Reflecting lifestyle shifts toward personalized travel and segmented market preferences, this segment demands highly reliable yet flexible fuel supply solutions.

Together, these end-user distinctions underscore diverse demand drivers, highlighting the need for tailored fuel formulations, supply chain strategies, and technology deployments aligned to each sub-sector’s operational and regulatory context.

Regional Insights

Asia Pacific Jet Fuel Market Trends

Asia Pacific is set to become the largest regional market, capturing an estimated share of 38% in 2025. The market growth is fueled by rapid urbanization, increasing disposable incomes of an expanding middle class, and government-driven expansions in airport infrastructures across key countries such as China, India, Japan, and members of ASEAN.

Evolving regulatory frameworks within the region are increasingly incentivizing the production and utilization of sustainable aviation fuel, although challenges remain in price competitiveness and infrastructure readiness. The competitive landscape is characterized by emerging domestic producers forming strategic partnerships with global energy majors to scale refining capacity and SAF deployment.

Investment focus is strong on supply chain integration and capacity building to sustain rising air travel demand, making Asia Pacific a critical focal point for aggressive market expansion and sustainability initiatives.

North America Jet Fuel Market Trends

North America is anticipated to be the fastest-growing region, led by the U.S., through 2032. Key contributing factors include a mature yet expanding domestic and international aviation network, driven by the proliferation of low-cost carriers and high-frequency air routes.

The sizable military aviation presence further adds to demand volumes. The regulatory landscape further supports sustainable fuel adoption with incentives such as tax credits for renewable fuel blending and federal research grants underpinning innovation in low-carbon fuel technologies.

North America’s market concentration is moderate, prominently featuring major oil and energy players, including Shell, Chevron, and BP. Investment trends reveal a strong focus on renewable fuel production, refining process innovations, and strategic alliances to stabilize fuel availability while mitigating cost volatility. These factors position North America as both a market growth leader and a hub for sustainable aviation fuel development initiatives.

Europe Jet Fuel Market Trends

Europe commands roughly one-fifth of the jet fuel market share, anchored by established aviation hubs in Germany, the U.K., France, and Spain.

The regional market benefits from a highly harmonized regulatory framework driven by the European Union, especially through directives such as Fit for 55 and the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). These policies accelerate the adoption of sustainable aviation fuels and alternative energy sources, compelling airlines and fuel suppliers to innovate rapidly.

Though growth here is steadier and slightly more constrained compared to emerging markets due to market maturity and rigorous environmental targets, Europe is a leader in technological innovation and infrastructure modernization. Investments prominently emphasize SAF production capacity expansion, green port logistics upgrades, and fostering public-private collaboration models to advance clean aviation.

The regional competitive landscape features a mix of integrated energy companies, traditional refiners, and emerging biofuel producers, reinforcing Europe’s role as an innovation nexus within the aviation fuel domain.

Competitive Landscape

The global jet fuel market landscape depicts a concentrated picture, with key players such as Royal Dutch Shell, TotalEnergies, Chevron Corporation, and BP Plc collectively controlling a significant market share. These companies leverage vast refining capacities, global distribution networks, and robust R&D investments, giving them a competitive advantage.

The market exhibits a mix of consolidation and fragmentation, with large multinational oil majors dominating, supported by smaller regional players and emerging sustainable fuel producers. Competitive positioning emphasizes innovation in fuel types, strategic partnerships, and geographic reach to capture growth in emerging markets.

Key Industry Developments

- In September 2025, Oneworld alliance airlines, led by American and Alaska Airlines, partnered with Breakthrough Energy Ventures to launch a US$150 million fund aimed at advancing scalable, low-carbon sustainable aviation fuel technologies and infrastructure to reduce emissions and production costs.

- In September 2025, a £2 Billion (approximately US$2.6 Billion) sustainable aviation fuel plant in Teesside, backed by Saudi investment, advanced its development plans. The facility aims to produce low-carbon jet fuel, support U.K. climate goals, create jobs, and strengthen domestic SAF supply.

- In August 2025, Indian Oil Corporation (IOC) announced plans to launch India’s first commercial-scale sustainable aviation fuel (SAF) plant at its Panipat refinery in December 2025. With an annual capacity of 35,000 tons, the facility will convert used cooking oil into low-carbon jet fuel, reducing import dependence and lifecycle emissions.

Companies Covered in Jet Fuel Market

- Shell plc

- TotalEnergies SE

- Chevron Corporation

- BP Plc

- ExxonMobil Corporation

- Phillips 66

- Neste Corporation

- Honeywell International Inc.

- Valero Energy Corporation

- LanzaTech

- Shell Aviation

- Sasol Limited

- Air BP

- Repsol SA

- World Energy

Frequently Asked Questions

The jet fuel market is projected to reach US$431.7 Billion in 2025.

Rising air travel demand and increasing investments in airport infrastructure are driving the jet fuel market.

The jet fuel market is poised to witness a CAGR of 12.8% from 2025 to 2032.

Key market opportunities include the shift toward sustainable aviation fuels (SAF) and the expansion of commercial airlines, particularly in developing economies.

Royal Dutch Shell, TotalEnergies, and Chevron Corporation are some of the key players in the jet fuel market.