- Energy Storage Solutions

- Renewable Aviation Fuel Market

Renewable Aviation Fuel Market Size, Share, and Growth Forecast, 2025 - 2032

Renewable Aviation Fuel Market By Fuel Type (Biofuels, Synthetic Fuels), Feedstock (Used Cooking Oil (UCO) & Waste Fats, Others), Technology (Hydroprocessed Esters & Fatty Acids (HEFA-SPK), Others), and Regional Analysis for 2025 - 2032

Renewable Aviation Fuel Market Share and Trends Analysis

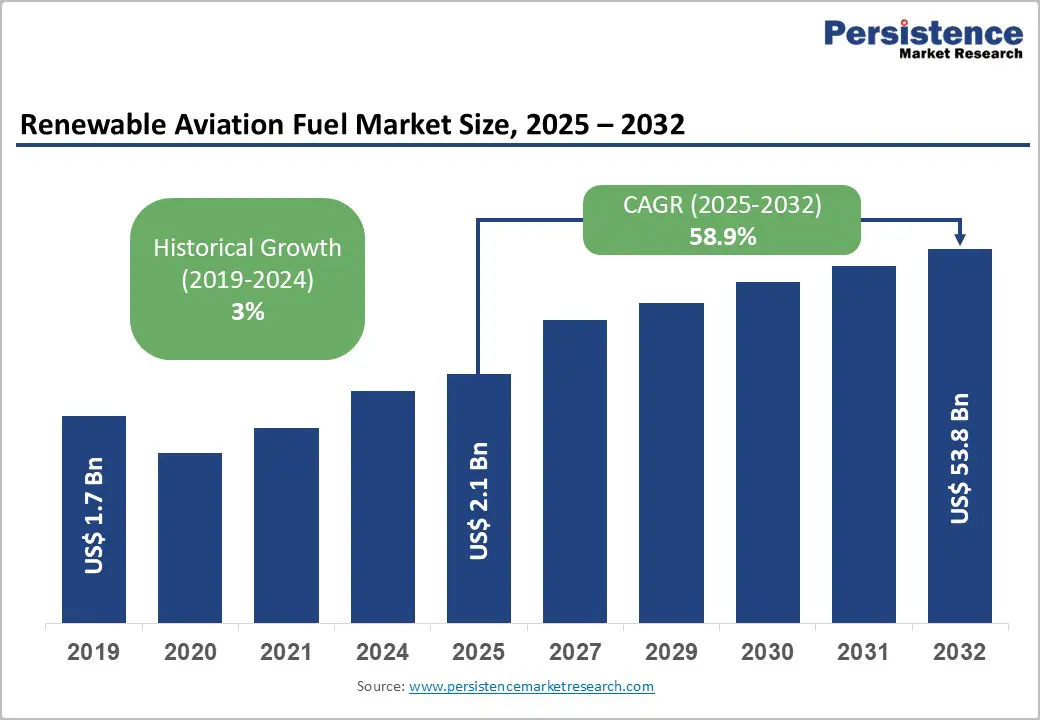

The global renewable aviation fuel market size is likely to be valued at US$2.1 Billion in 2025, and is estimated to reach US$53.8 Billion by 2032, growing at a CAGR of 58.9% during the forecast period 2025 - 2032, driven by national emissions mandates, aggressive decarbonization targets, and surging airline demand for sustainable solutions.

This growth is driven by blending quotas, expanding SAF infrastructure, and new feedstock options. Airlines are increasingly adopting SAF to reduce carbon risks, motivated by regulatory penalties and voluntary offset programs. The shift toward renewable aviation fuels reflects rising policy pressure, technological progress, and new market entrants.

Key Industry Highlights

- Leading Fuel Type: Biofuels are the market share leader, accounting for approximately 78% of global revenue in 2025, backed by mature HEFA-SPK and ATJ-SPK technologies.

- Fastest-growing Fuel Type: Synthetic fuels are the fastest-growing segment as PtL attracts significant infrastructure investment.

- Dominant Feedstock: Used cooking oil and waste fats represent 43% of the feedstock supply in 2025, but feedstock diversification is being accelerated due to supply constraints.

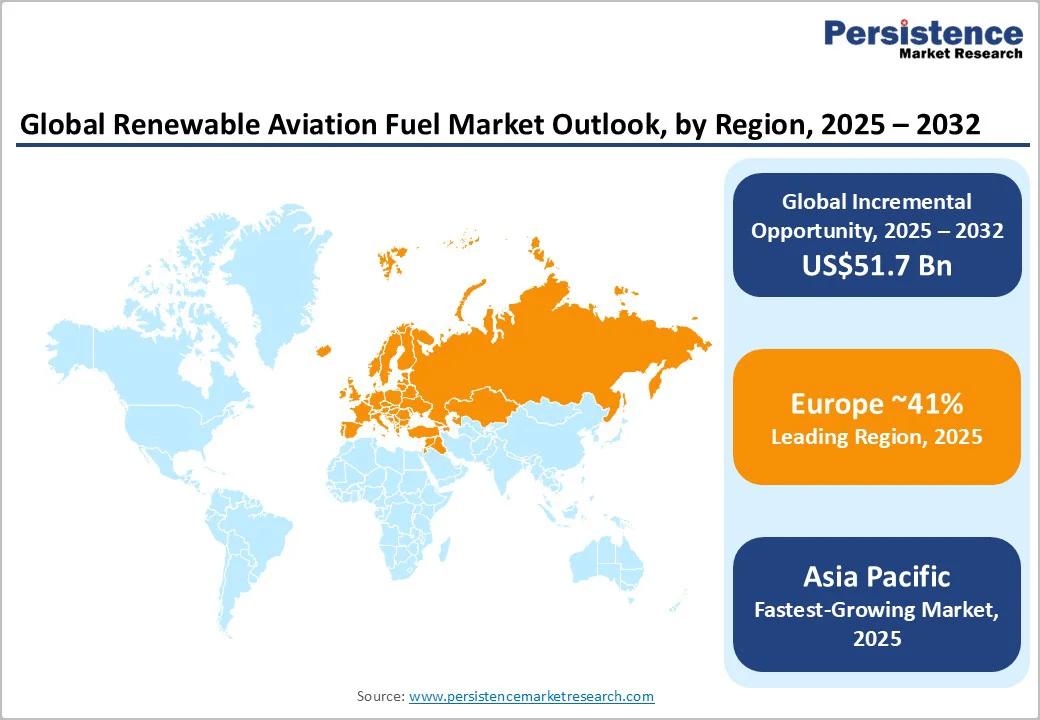

- Dominant Region: Europe dominates with around 41% market share, with Germany and the Nordics leading PtL SAF programs.

- Fastest-growing Regional Market: Asia Pacific is the fastest-growing regional market through 2032, propelled by domestic manufacturing, feedstock reserves, and evolving regulatory standards.

- Competitive Dynamics: Industry consolidation is intensifying, with major firms securing multiyear offtake agreements, investing in vertical integration, and expanding refinery capacity.

- June 2025: NTPC Green Energy and Honeywell India partnered to explore SAF production in India using Honeywell’s eFining technology, aiming to support India’s aviation sector in meeting its long-term environmental and net-zero goals through innovative green hydrogen and carbon capture solutions.

| Key Insights | Details |

|---|---|

| Renewable Aviation Fuel Market Size (2025E) | US$2.1 Bn |

| Market Value Forecast (2032F) | US$53.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 58.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Forward-Thinking Regulatory Innovation to Transform the SAF Market

Policy incentives from governments and supranational bodies are catalyzing investment in renewable aviation fuels. For example, the U.S. Inflation Reduction Act provides a SAF tax credit of US$1.25/gallon plus additional credits for lifecycle GHG reduction, which can cause a marked acceleration of SAF production projects.

Similarly, the European Union (EU)’s ReFuelEU Aviation mandate requires fuel suppliers to blend increasing amounts of SAF, starting at 2% in 2025 and scaling to 70% by 2050. At the global level, the CORSIA program of the International Civil Aviation Organization (ICAO) is imposing global emissions monitoring and supporting international adoption.

These measures are lowering entry barriers, spurring multibillion-dollar investments in new bio-refineries, and encouraging partnerships between airlines, refiners, and feedstock suppliers. They are also driving rapid market scale-up by guaranteeing long-term demand and facilitating financial close for large-scale projects.

Feedstock Logistics and Supply Chain Instability Pose Critical Cost Barriers

The SAF market confronts significant near-term risks from constrained feedstock supply and complex logistics. Used cooking oil (UCO) and tallow represent the leading feedstock, but geographic unevenness and regulatory hurdles, such as the EU’s RED II anti-fraud frameworks, have created uncertainty for sourcing and certification.

Biofuel producers face volatile pricing, while alternative feedstock sources such as lignocellulosic biomass face slow commercial maturity and high conversion costs. Transport infrastructure limitations, especially cold chain and bulk storage for low-volume feedstock, raise CAPEX and OPEX burdens.

Supply chain risks are further amplified by the limited availability of dedicated bio-refining facilities, often resulting in bottlenecks and sub-scale production runs. These systemic barriers require strategic feedstock diversification and robust traceability frameworks.

PtL and e-Fuels to Unlock Scale and Carbon Mitigation Possibilities

The rapid maturation of power-to-liquids (PtL) technology offers a transformative growth opportunity. PtL enables the production of e-kerosene from captured CO2 and renewable electricity, addressing both feedstock scarcity and carbon emissions. This technology is making notable headway in the renewable aviation fuel market, catalyzed by falling renewable energy costs and expanding hydrogen availability.

The EU is providing heavy funding for PtL innovation through the Horizon Europe initiative, with the first commercial e-fuel plants in Germany and Norway slated to come online by 2026. Airlines aiming for net-zero status are partnering with fuel innovators, providing offtake agreements and joint development capital. PtL’s scalability, grid interconnection, and carbon reduction profile position it as the next major driver of SAF adoption and investment prioritization.

Category-wise Analysis

Fuel Type Insights

Biofuels dominate the renewable aviation fuel market landscape in 2025, capturing approximately 78% of the revenue share. This leadership position reflects the segment's commercial maturity, regulatory certainty, and operational compatibility with existing aviation infrastructure.

Biofuel-derived SAF is produced through well-established conversion pathways, most prominently HEFA-SPK, which converts renewable feedstock into drop-in jet fuel meeting ASTM D7566 specifications. Airlines operating biofuel SAF blends report seamless integration with existing turbine engines without mechanical modifications, reducing transition risks and operational complexity.

Major carriers, including American Airlines, Lufthansa, and Singapore Airlines, have secured multiyear offtake contracts for biofuel SAF, signaling confidence in feedstock availability and supply chain stability. Regulatory frameworks across the U.S., the EU, and Asia Pacific mandate biofuel blending thresholds, guaranteeing sustained demand through 2030.

Synthetic fuels, particularly PtL and e-kerosene, represent the fastest-expanding fuel category through 2032. This segment is accelerating rapidly as renewable energy costs decline and regulatory support intensifies. PtL technology converts renewable electricity and captured CO2 into synthetic kerosene through advanced chemical processes, such as Fischer-Tropsch synthesis, circumventing traditional feedstock constraints.

The EU is investing heavily in PtL infrastructure, with Germany's INERATEC commissioning Europe's largest commercial e-fuel plant, ERA ONE, in 2025, capable of producing 130,000 tons annually. Airlines and corporate aircraft operators are bidding aggressively for e-fuel offtake contracts, viewing PtL as a long-term decarbonization pathway without agricultural land-use constraints.

Feedstock Insights

UCO and waste animal fats dominate, representing 85% of the renewable aviation fuel market revenue share in 2025. The growth of this segment is rooted in the abundant supply from the food industry, established collection and logistics infrastructure, and attractive sustainability metrics.

The EU's ReFuelEU Aviation mandate and advanced biofuel classification provide strong regulatory incentives, with sustainability certification frameworks, such as RSPO and ISCC, ensuring traceability and environmental credibility.

Energy majors such as Neste and World Energy have established long-term contracts with municipal waste treatment facilities, food processing companies, and restaurants, securing feedstock predictability. As a result, UCO-based SAF production is forecast to grow rapidly, driven by expanded collection networks, regulatory compliance investments, and airline demand.

Renewable electricity and green hydrogen are emerging as the fastest-growing feedstocks, owing to PtL technology adoption and accelerating renewable energy deployment. This segment is transitioning from pilot projects to commercial-scale manufacturing, with an anticipated CAGR of 54% through 2032.

PtL feedstock economics are improving dramatically due to a decline in solar PV costs in favorable geographies and increasing price competitiveness in wind power. Green hydrogen, produced via water electrolysis powered by renewables, is the intermediate energy carrier for PtL synthesis.

Current hydrogen production costs are declining, as electrolyzer manufacturing scales and renewable electricity contracts mature. The aviation sector's net-zero commitments are accelerating PtL feedstock development, with the ICAO's CORSIA program and voluntary corporate pledges creating demand certainty.

Technology Insights

HEFA-SPK technology commands 68% of the SAF market revenue share in 2025, attributable to its commercial maturity and long operational history, existing refinery compatibility, modest capital requirements, and ASTM D7566 approval for up to 50% jet fuel blending. The HEFA process involves hydrogenation of fatty acid esters and triglycerides to produce saturated hydrocarbons, followed by isomerization and distillation to meet jet fuel specifications.

HEFA technology is deployed widely across commercial-scale facilities worldwide, generating massive volumes of SAF globally. Capital intensity for HEFA plants is also significantly lower than alternative conversion pathways, making it an attractive investment option for SAF market players. Airlines favor HEFA-SPK due to regulatory certainty and minimal engine modification requirements, further promoting this segment.

FT-SPK represents the fastest-growing segment through 2032. FT-SPK converts synthesis gas (syngas), a mixture of carbon monoxide and hydrogen derived from biomass, waste, captured CO2, or coal, into synthetic paraffinic kerosene via the Fischer-Tropsch catalytic process. FT-SPK's competitive advantages include feedstock flexibility, process scalability, and superior lifecycle carbon reduction when powered by sustainable feedstock.

FT-SPK's modular design also enables deployment in waste-abundant regions, decoupling SAF production from geographically concentrated feedstock sources. Technology maturation is progressing rapidly, with the technical versatility and scalability of FT-SPK serving as a cornerstone of long-term, high-volume SAF production.

Regional Insights

North America Renewable Aviation Fuel Market Trends

North America is driven by strong regulatory incentives such as the Inflation Reduction Act's tax credits, extensive aviation infrastructure, and robust capital markets, attracting significant venture and equity investment. The U.S. dominates regional capacity, with major production hubs in the Gulf Coast, California, and the Midwest, supported by significant investments from key producers such as World Energy, Gevo, and Neste targeting substantial capacity expansion.

Leading airlines have committed to large SAF purchases, backed by streamlined U.S. regulatory approvals and government initiatives aimed at scaling production. Canada and Mexico are emerging players, leveraging biomass and agricultural feedstock to support SAF development.

The regional market growth is characterized by policy stability, increasing airline demand for sustainable fuels, ongoing technological innovations in PtL and Fischer-Tropsch processes, and secure feedstock supply from agricultural and waste streams. The regulatory framework includes the U.S. Environmental Protection Agency (EPA)’s Renewable Fuel Standard and state-level incentives, complemented by ICAO’s emissions monitoring programs.

The market is moderately consolidated among established firms, with new entrants advancing innovative pathways such as alcohol-to-jet and carbon capture fuels, while investments from major energy companies increase, underscoring strong sector confidence and growth potential.

Europe Renewable Aviation Fuel Market Trends

Europe leads the renewable aviation fuel market in 2025, holding 41% of revenue and acting as the main hub for innovation and policy leadership driven by ambitious climate commitments and a comprehensive regulatory framework, including ReFuelEU Aviation and Fit for 55. Germany is the regional production leader with strong support for PtL technology, advanced renewable electricity infrastructure, and active SAF procurement by carriers such as Lufthansa.

The Netherlands is a key SAF producer, leveraging Rotterdam’s logistics and established supply chains, while the U.K., France, Spain, Italy, and Scandinavian countries are rapidly expanding production capacities and technology adoption.

Europe’s regulatory environment is the most rigorous globally, emphasizing lifecycle emissions assessments, anti-fraud measures, and sustainability traceability, with additional support from EU funding programs such as Horizon Europe.

The region’s competitive market is more fragmented than North America’s, featuring multiple regional producers and strategic airline-producer alliances that consolidate demand. Strong government and institutional investments underscore Europe’s leading role in driving demand growth and infrastructure development for sustainable aviation fuels.

Asia Pacific Renewable Aviation Fuel Market Trends

Asia Pacific represents the fastest-growing regional market for renewable aviation fuel, driven by rapidly expanding aviation demand, abundant feedstock resources, emerging policy support, and manufacturing cost advantages. China is establishing regional dominance through state-backed investments in SAF conversion capacity, agricultural waste utilization, and airport blending programs, while major carriers implement supply contracts.

Japan leads in technology innovation and efficiency, with carriers pioneering SAF adoption and technology conglomerates advancing advanced conversion methods, though domestic feedstock supply requires regional imports. India is an emerging frontier with rapidly expanding aviation demand and agricultural feedstock potential, supported by government biofuel initiatives and strategic partnerships with global producers.

Southeast Asian countries position themselves as feedstock hubs with significant used cooking oil and palm oil resources, while carriers commit to SAF adoption despite slower infrastructure development due to capital constraints.

South Korea and Australasia are developing niche roles focused on technology innovation and renewable energy-driven e-fuel production. The regulatory environment remains heterogeneous across the region, lacking unified frameworks comparable to Europe, though policy convergence is gaining momentum.

Competitive Landscape

The global renewable aviation fuel market structure is moderately consolidated with several key players dominating, such as Neste Oyj, World Energy, LanzaTech, Gevo, and SkyNRG.

These companies leverage their technological expertise, long-term feedstock agreements, and airline partnerships to maintain competitive advantages. While mature technologies such as HEFA-SPK drive most current production, emerging processes such as Fischer-Tropsch and Power-to-Liquids are gaining traction, encouraging technological diversification and innovation.

The industry is witnessing strategic partnerships between airlines and producers, aligning long-term supply and demand to reduce investment risks.

Although barriers such as high capital costs and feedstock supply constraints exist, regulatory support and demand for sustainable fuels are fostering market growth. The competitive landscape is expected to evolve with consolidation among mid-tier firms, regional specialization, and technology-driven disruptions, creating a dynamic yet progressively mature market environment.

Key Industry Developments

- In November 2025, Masdar and Tadweer partnered to build Abu Dhabi’s first commercial waste-to-SAF plant, converting 500,000 tons of waste using green hydrogen. The project supports UAE decarbonization goals, aims to make Abu Dhabi a SAF hub, and enhances waste management via AI-driven systems.

- In November 2025, In November 2025, Rolls-Royce led a U.K. government-backed initiative to enhance SAF performance through advanced engine and fuel system technologies. The project aims to boost SAF efficiency, cut aviation emissions, and support national sustainability goals, highlighting technology partnerships’ role in accelerating SAF adoption.

- In November 2025, Sky Renewables partnered with Australian farmers to trial SAF production from sugar beet, aiming to diversify feedstocks and assess viability for renewable jet fuel. The initiative supports aviation decarbonization and highlights alternative crops in Australia’s sustainable fuel strategy.

Companies Covered in Renewable Aviation Fuel Market

- Neste Oyj

- World Energy LLC

- LanzaTech Global, Inc.

- Gevo, Inc.

- SkyNRG B.V.

- TotalEnergies SE

- Fulcrum BioEnergy, Inc.

- Honeywell International Inc.

- Shell plc

- BASF SE

- Velocys plc

- Red Rock Biofuels LLC

- Aemetis, Inc.

- Renewable Energy Group, Inc.

- BP plc

Frequently Asked Questions

The global renewable aviation fuel market is projected to reach US$2.1 Billion in 2025.

National emissions mandates, aggressive corporate decarbonization targets, and surging airline demand for sustainable solutions are driving the aviation fuel market.

The aviation fuel market is poised to witness a CAGR of 58.9% from 2025 to 2032.

The implementation of blending quotas, escalating investment in sustainable aviation fuel infrastructure, and emerging feedstock alternatives are key market opportunities.

Neste Oyj, World Energy LLC, and LanzaTech Global are some of the key players in the aviation fuel market.