- Beverages

- Fruit Juice and Vegetable Juice Market

Fruit Juice and Vegetable Juice Market Size, Share, and Growth Forecast, 2025 - 2032

Fruit Juice and Vegetable Juice Market by Nature (Conventional, Organic), Packaging Material (Tetra Pak Cartons, PET Bottles, Glass Bottles, Cans, Pouches, Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience/Grocery Stores, Online Retail Stores, Others), and Regional Analysis for 2025 - 2032

Fruit Juice and Vegetable Juice Market Size and Trends Analysis

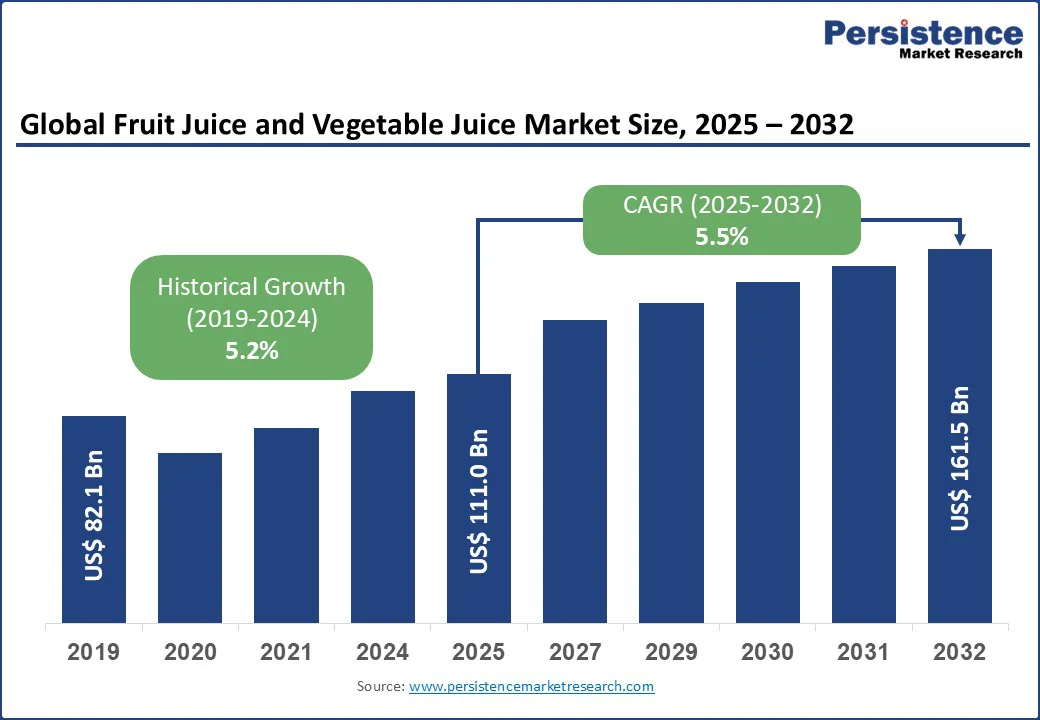

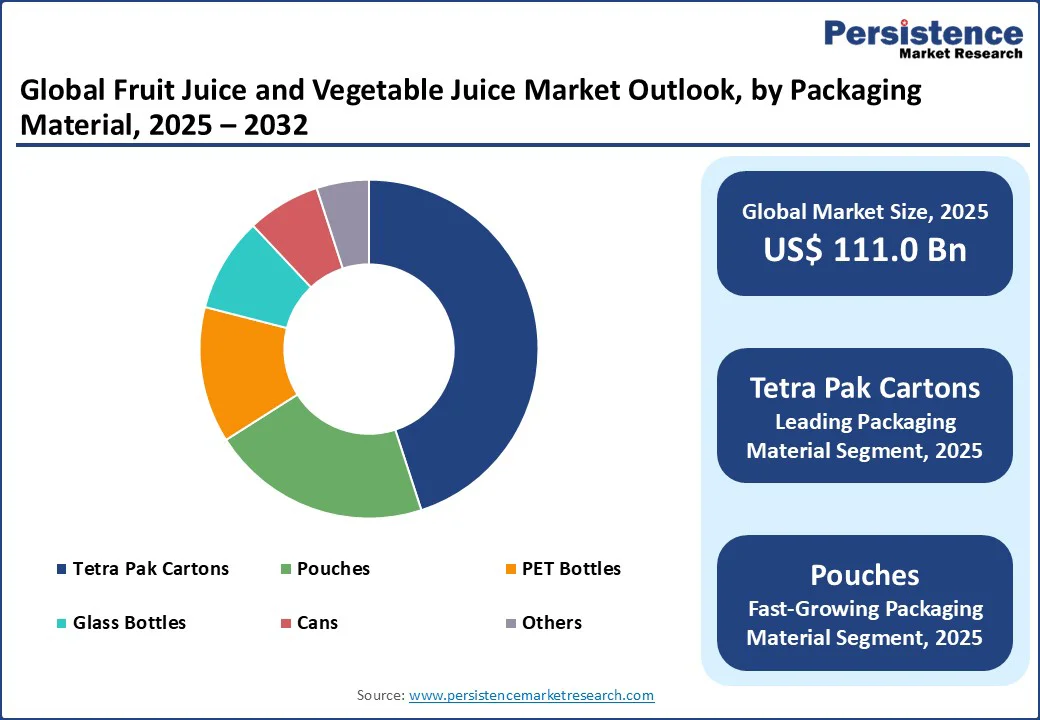

The global fruit juice and vegetable juice market size is likely to be valued at US$ 111.0 Bn in 2025, and it is expected to reach US$ 161.5 Bn by 2032, growing at a CAGR of 5.5% during the forecast period from 2025 to 2032.

Key Industry Highlights:

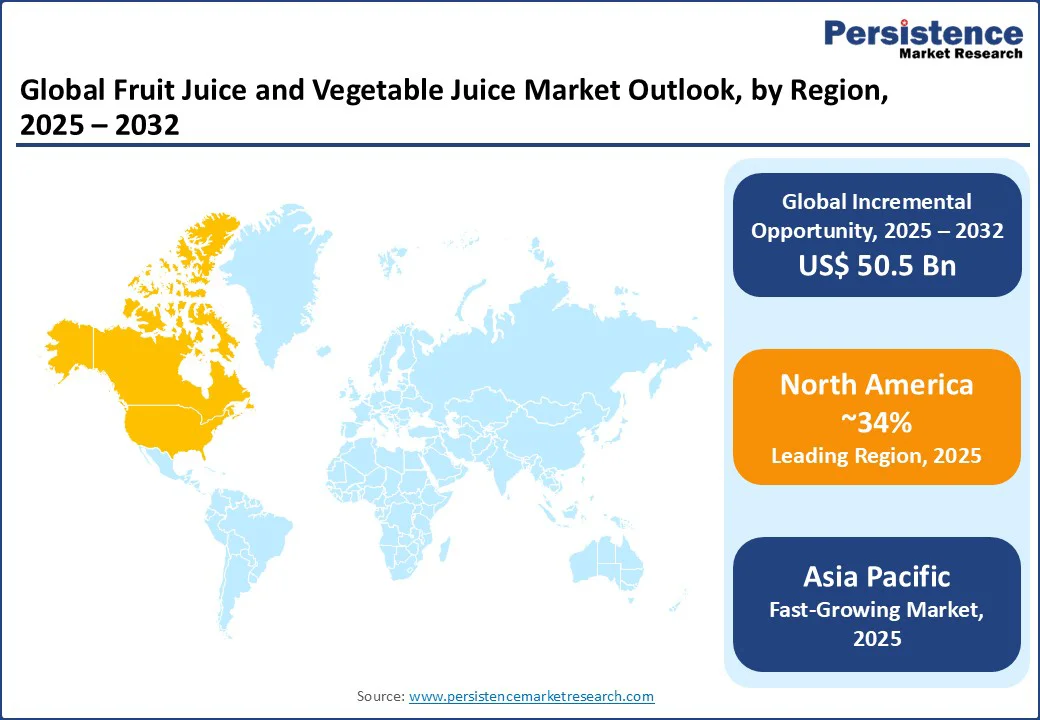

- Leading Region: North America is expected to account for a 34% share in 2025, driven by high consumer demand for health-oriented beverages, advanced retail infrastructure, and the presence of major players such as Coca-Cola and PepsiCo in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising disposable incomes, increasing health awareness, and growing demand for premium and organic juices in countries such as China and India.

- Dominant Nature: Conventional juices command nearly 77% share due to their affordability, widespread availability, and established consumer base.

- Leading Packaging Material: Tetra Pak Cartons likely to account for 45% revenue in 2025 arre driven by their cost-effectiveness, eco-friendly properties, and widespread use in retail.

- Leading Distribution Channel: Supermarkets/Hypermarkets, contributing approximately 52% of market revenue, due to their extensive reach, product variety, and consumer preference for one-stop shopping.

| Key Insights | Details |

|---|---|

| Market Size (2025E) | US$ 111.0 Bn |

| Market Value Forecast (2032F) | US$ 161.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

The fruit juice and vegetable juice market growth is driven by increasing consumer demand for healthy and natural beverages, rising awareness of nutritional benefits, and innovations in packaging and product formulations.

Market Dynamics

Driver- Increasing health awareness and demand for functional beverages

The rising health consciousness among consumers is a major driver propelling growth in the global fruit and vegetable juice market. With increasing awareness of the role in wellness, consumers are gravitating toward natural, minimally processed beverages rich in nutrients as alternatives to sugary sodas. Fruit and vegetable juices are being positioned as functional beverages, offering benefits such as improved digestion, enhanced immunity, weight management, and cardiovascular support.

For instance, Ocean Spray has introduced its Immunity line flavors, such as Cranberry Blueberry Acai and Orange Mango, packed with vitamins C and E and zinc, with no added sugar, positioning them as immunity-supportive options. The company also launched a Zero Sugar Juice Drink made with real fruit juice and stevia, offering bold flavor with zero added sugar.

Tropicana unveiled its Special Start range featuring blood orange, pink grapefruit, and pineapple pressed juices, along with enhanced Multivit Boost variants such as Mixed Berries and Smooth Orange, delivered with 100% daily value of vitamin C and essential B and E vitamins. These launches reflect consumer demand for beverages that go beyond hydration serving a preventive health function.

As lifestyles shift post-pandemic, with heightened emphasis on immunity and balanced nutrition, juice brands are responding with low-sugar variants, fortified formulations, and clean-label positioning. Functional fruit and vegetable juices are increasingly central to wellness routines, especially among urban and younger demographics who seek both convenience and health benefits.

Restraint- High Production and Raw Material Costs

High costs of production and raw materials represents a significant restraint on the market growth. The industry relies heavily on the consistent availability of fresh fruits and vegetables, which are subject to seasonal fluctuations, climate change impacts, and supply chain disruptions. Unpredictable weather conditions, such as droughts, floods, and hurricanes, often lead to reduced crop yields, driving up the prices of key raw materials such as oranges, apples, cranberries, and tomatoes.

For instance, global orange juice supplies have been severely impacted in recent years due to citrus greening disease in Florida and adverse weather in Brazil, leading to historically high orange juice prices.

In addition to raw material volatility, production costs are rising due to the need for advanced processing technologies, cold-press extraction, pasteurization, and packaging innovations. Sustainable packaging, such as biodegradable cartons or recyclable PET bottles, further adds to expenses.

Energy, labor, and logistics costs also contribute to elevated overall expenditures. These higher costs are often passed on to consumers, making premium juice products less accessible in price-sensitive markets, thereby limiting widespread adoption and market expansion.

Opportunity- Growth in Organic and Sustainable Juice Products

The growing demand for organic and sustainable juice products presents a significant opportunity in the global fruit and vegetable juice market. Consumers are becoming more health-conscious and environmentally aware, seeking products that not only deliver nutritional benefits but also align with their values of sustainability and ethical sourcing.

Organic juices, free from synthetic pesticides, fertilizers, and genetically modified organisms, are increasingly perceived as healthier and safer alternatives. This is particularly appealing to millennials and Gen Z consumers, who are more inclined toward clean-label and plant-based lifestyles.

Sustainability is also playing a vital role in shaping consumer preferences. Eco-friendly packaging, such as recyclable PET bottles, biodegradable cartons, and refillable pouches, is gaining traction as companies attempt to reduce their carbon footprint and meet global sustainability goals.

For instance, in 2024, Nestlé partnered with Tetra Pak to develop fully recyclable juice cartons in Europe, aligning with the EU’s circular economy initiatives. Similarly, PepsiCo and Coca-Cola have expanded their portfolios to include organic and low-sugar juices under brands such as Tropicana and Simply.

As the need for transparency, traceability, and eco-conscious choice continues to rise, brands investing in organic farming, ethical sourcing, and sustainable packaging are well-positioned to capture a rapidly expanding consumer base and strengthen long-term market growth.

Category-wise Analysis

Nature Insights

Conventional juices dominate, expected to account for approximately 65% share in 2025. Their dominance stems from their affordability, widespread availability, and established consumer base, particularly in developing regions.

Conventional juices, offered by major players such as Coca-Cola and PepsiCo, benefit from economies of scale, enabling competitive pricing and broad distribution. Their versatility in flavors and accessibility across retail channels make them a preferred choice for mass-market consumers.

The organic juices segment is the fastest-growing, driven by increasing consumer awareness of health, sustainability, and environmental concerns. Organic juices, such as those offered by Lakewood Organic Juices and Bolthouse Farms, appeal to premium consumers willing to pay a higher price for certified organic products. The segment is fueled by rising demand in North America and Europe, where health-conscious lifestyles are prevalent.

Packaging Material Insights

Tetra Pak Cartons led, holding a 45% share in 2025. Their dominance is driven by their cost-effectiveness, lightweight design, and eco-friendly properties, making them ideal for large-scale distribution. Companies such as Tropicana and Dole utilize Tetra Pak cartons for their durability and ability to preserve juice quality without refrigeration, appealing to both retailers and consumers.

The pouches segment is the fastest-growing, driven by their convenience, portability, and appeal to younger consumers, particularly in urban areas. Pouches, often used for single-serve and on-the-go consumption, are gaining popularity in the Asia Pacific and North America, with brands such as Welch’s introducing innovative pouch designs to capture market share.

Distribution Channel Insights

Supermarkets/Hypermarkets account for a major share, likely to account for 52% revenue share in 2025. Their dominance is driven by their extensive reach, diverse product offerings, and consumer preference for one-stop shopping. Major retailers such as Walmart and Tesco stock a wide range of juice brands, making them a preferred channel for both conventional and organic juices.

The online retail stores segment is the fastest-growing, fueled by the rise of e-commerce and changing consumer shopping habits. The convenience of online platforms, coupled with subscription models and targeted marketing by brands such as Nestlé and Keurig Dr Pepper, is driving rapid adoption, particularly in urban markets in the Asia Pacific and North America.

Regional Insights

North America Fruit Juice and Vegetable Juice Market Trends

North America is projected to hold a dominant 34% share of the global fruit and vegetable juice market in 2025, supported by high consumer demand for health-oriented beverages and a well-established retail ecosystem.

Consumers in the U.S. and Canada are increasingly prioritizing healthier lifestyles, driving a shift away from sugary carbonated drinks toward natural juices, organic blends, and functional beverages enriched with vitamins, minerals, and probiotics. This trend has been reinforced by post-pandemic health awareness, with immunity-boosting and low-sugar juice products gaining strong traction.

The region’s advanced retail infrastructure, comprising supermarkets, hypermarkets, convenience stores, and rapidly expanding e-commerce channels, further supports wide product accessibility. Online platforms such as Amazon Fresh, Walmart, and Instacart have significantly boosted juice sales by catering to digital-savvy consumers seeking convenience.

Additionally, the presence of major global players such as Coca-Cola, PepsiCo, Keurig Dr Pepper, and Ocean Spray provides continuous innovation and large-scale distribution networks. For instance, Coca-Cola’s Simply and PepsiCo’s Tropicana brands dominate with new product launches tailored to health-conscious consumers.

Overall, North America’s strong purchasing power, preference for premium products, and concentration of leading beverage companies solidify its role as the sector’s most influential region.

Europe Fruit Juice and Vegetable Juice Market Trends

Europe is a significant player in the fruit juice and vegetable juice market, supported by strong regulatory frameworks and consumer demand for sustainable products. Leading countries, including Germany, France, and the UK, drive market growth through high consumption of organic and functional juices. Germany, the largest market in Europe, benefits from a strong organic food culture, with brands such as Nestlé and Del Monte reporting a 10% increase in organic juice sales.

The European Union’s stringent regulations on food safety and sustainability encourage manufacturers to adopt eco-friendly packaging, such as Tetra Pak cartons and glass bottles. The region’s focus on reducing sugar content in beverages, driven by policies such as the UK’s sugar tax, has spurred innovation in low-sugar and vegetable-based juices. Companies such as Innocent Drinks and Tropicana are investing in R&D to develop healthier formulations, ensuring Europe’s steady growth in the global market.

Asia Pacific Fruit Juice and Vegetable Juice Market Trends

Asia Pacific is emerging as the fastest-growing region in the global fruit and vegetable juice market, fueled by rising disposable incomes, increasing health awareness, and a surging appetite for premium and organic beverages.

Consumers in countries such as China, India, and Japan are shifting away from traditional carbonated soft drinks toward natural juices that offer nutritional and functional benefits. The growing middle-class population, particularly in urban centers, is driving demand for healthier and more convenient beverage options, aligning with broader lifestyle changes and wellness trends.

The rapid adoption of organic juices and clean-label products reflects the rising consumer preference for transparency and food safety. For instance, cold-pressed juices and low-sugar blends are gaining popularity among younger demographics who are highly influenced by global health trends and digital marketing campaigns.

Additionally, the expansion of modern retail infrastructure, including supermarkets, hypermarkets, and online platforms such as Flipkart, JD.com, and Alibaba’s Tmall, is improving access to a wide variety of juice products across the region.

Global beverage giants such as Coca-Cola and PepsiCo, along with regional players such as Dabur and ITC in India, are capitalizing on this demand by launching locally tailored products. This strong growth trajectory positions the Asia Pacific as a key driver of future market expansion.

Competitive Landscape

The global fruit juice and vegetable juice market is highly competitive, characterized by a blend of established multinational leaders and fast-growing regional players.

In North America and Europe, companies such as Coca-Cola Company, PepsiCo Inc., Nestlé S.A., Kraft Heinz Company, and Keurig Dr Pepper hold strong positions through extensive R&D, large-scale production facilities, and robust distribution networks that span supermarkets, convenience stores, and online retail platforms.

In Asia Pacific, regional firms such as Huiyuan Juice and Kagome Co. Ltd. are prominent by offering affordable, culturally relevant, and locally sourced juice products tailored to diverse consumer preferences.

Competition is increasingly driven by innovation in organic, low-sugar, and functional juices, along with the adoption of eco-friendly and sustainable packaging solutions such as PET bottles, pouches, and Tetra Pak cartons. Companies are also leveraging digital-first marketing strategies, including influencer-driven campaigns and e-commerce partnerships, to target health-conscious and younger demographics.

Strategic acquisitions, such as Coca-Cola’s investment in regional organic juice brands, further strengthen market positioning. While global leaders consolidate their dominance, regional and niche brands focus on affordability, natural formulations, and local flavors, ensuring a dynamic, fragmented, and innovation-led market landscape.

Key Developments:

- In April 2025, Coca-Cola Company reported a 2% increase in Q1 2025 beverage sales, led by strong growth in India, China, and Brazil, despite a slight revenue dip to $11.1 billion.

- In March 2025, Fresh Del Monte Produce Inc. acquired a majority stake in Ugandan avocado-oil producer Avolio, expanding into the specialty oils sector.

Companies Covered in Fruit Juice and Vegetable Juice Market

- Coca-Cola Company

- PepsiCo Inc.

- Fresh Del Monte Produce Inc.

- Dole Packaged Foods LLC

- Welch’s

- Ocean Spray Cranberries Inc.

- Nestlé S.A.

- Keurig Dr Pepper

- Kraft Heinz Company

- Bolthouse Farms Inc.

- Tropicana Brands Group

- Del Monte Foods Corporation

- Others

Frequently Asked Questions

The global fruit juice and vegetable juice market is projected to reach US$ 111.0 Bn in 2025.

The increasing demand for health-focused and functional beverages is a key driver.

The Fruit Juice and Vegetable Juice market is poised to witness a CAGR of 5.5% from 2025 to 2032.

Advancements in organic and sustainable juice products are a key opportunity.

Coca-Cola, PepsiCo, Nestlé, Tropicana, and Welch’s are key players.