- Processed Food

- Fruit and Vegetable Pulp Market

Fruit and Vegetable Pulp Market Size, Share, and Growth Forecast, 2025 - 2032

Fruit and Vegetable Pulp Market By Product Form (Frozen Pulp, Aseptic Pulp, Others), Pulp Type (Fruit Pulps, Vegetable Pulps), Application, End-user, and Regional Analysis for 2025 - 2032

Fruit and Vegetable Pulp Market Size and Trends Analysis

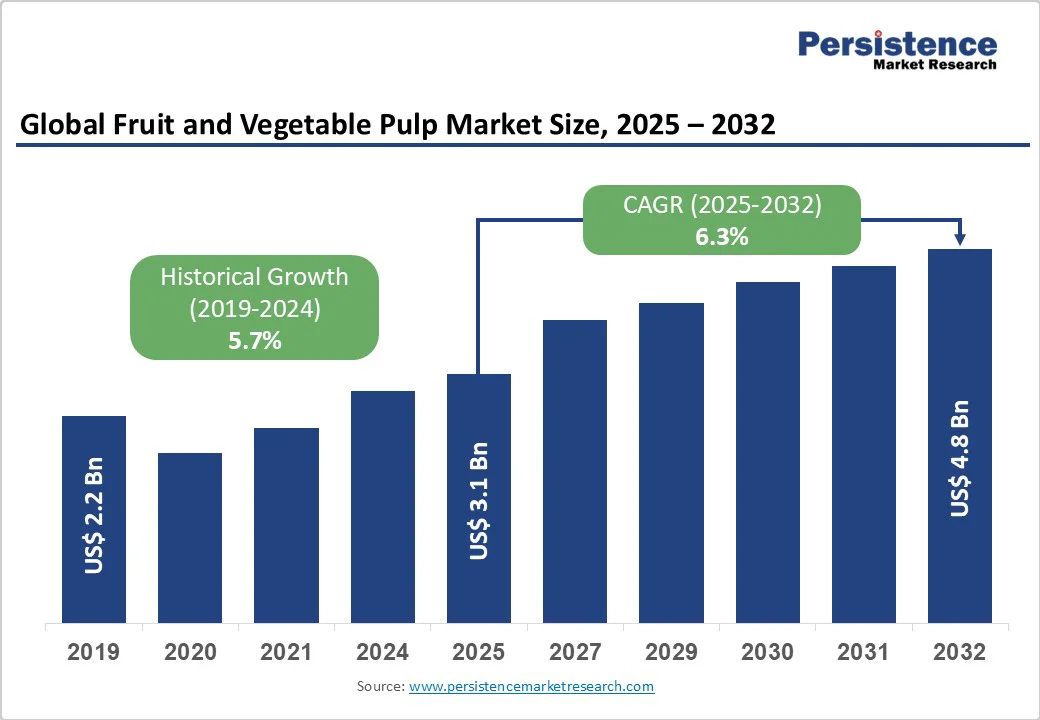

The global fruit and vegetable pulp market is expected to reach US$3.1 billion in 2025. It is expected to reach US$4.8 billion by 2032, growing at a CAGR of 6.3% during the forecast period from 2025 to 2032, driven by the increasing adoption of natural, clean-label, and functional ingredients across food and beverage applications.

Rising health awareness, the surge in ready-to-drink beverages, and advances in aseptic processing and cold-chain technology are fueling consumption. Asia Pacific leads production with abundant raw materials and low costs, while North America and Europe drive demand for premium and functional pulp products.

Key Industry Highlights

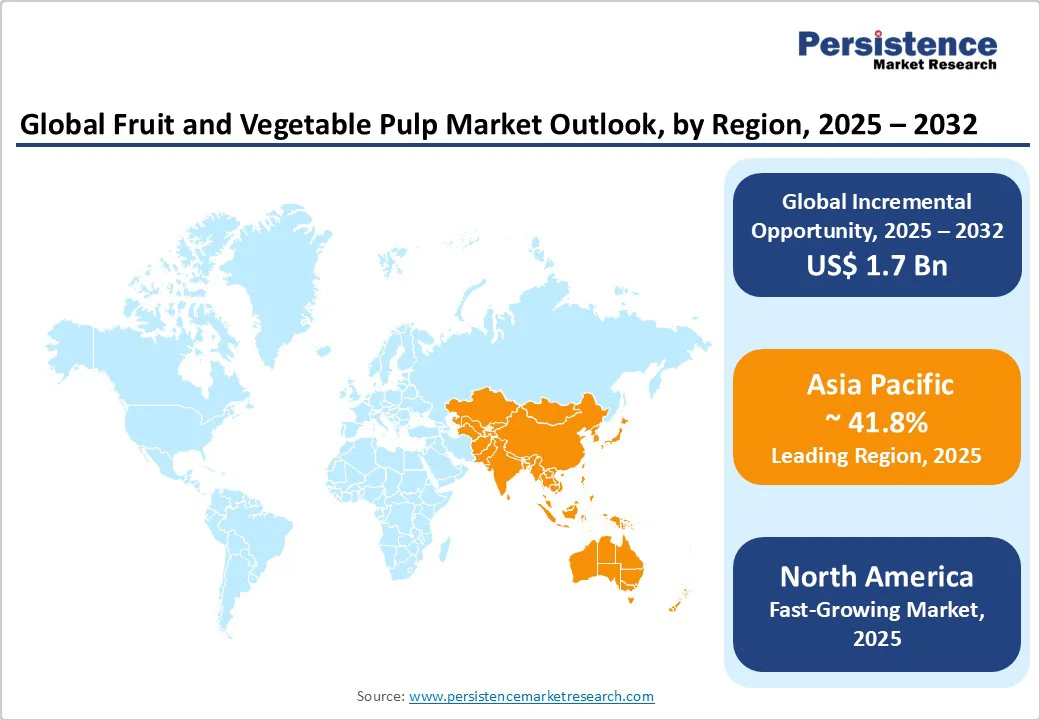

- Leading Region: Asia Pacific remains the largest producer and exporter of fruit and vegetable pulps, accounting for approximately 41.8% of global market volume in 2025, driven by countries such as India, Thailand, and China.

- Fastest-Growing Region: North America is the fastest-growing region, fueled by rising demand for clean-label beverages, functional foods, and aseptic pulp products.

- Investment Plans: Major processors are expanding aseptic pulp production lines and upgrading IQF freezing technologies, with investment volumes exceeding US$200 million globally over the next five years, targeting export growth and premium product development.

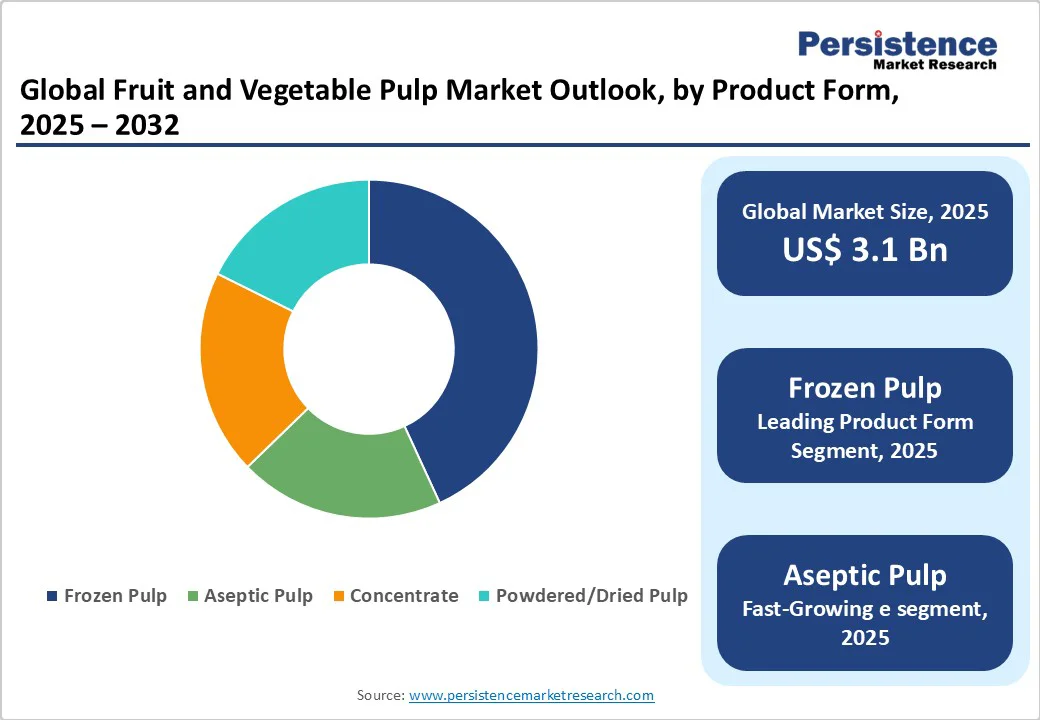

- Dominant Product Form: Frozen pulps continue to dominate, accounting for 43.9% of global trade volume and are widely used in bakery fillings, jams, desserts, and foodservice applications due to their minimal processing and nutrient preservation.

- Leading Pulp Type: Fruit pulps account for roughly 66% of the total market revenue, led by mango, banana, apple, and citrus varieties, serving key beverage, confectionery, and dessert segments globally.

| Key Insights | Details |

|---|---|

|

Fruit and Vegetable Pulp Market Size (2025E) |

US$3.1 Bn |

|

Market Value Forecast (2032F) |

US$4.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Natural and Clean-Label Ingredients

The global shift toward healthy and minimally processed foods has led to a strong preference for pulps as natural flavoring, coloring, and texturizing agents in beverages, bakery products, and dairy alternatives. According to major food ingredient associations, over 70% of new beverage product launches in 2024 emphasized “natural” or “no artificial additive” claims. This trend directly fuels pulp consumption, as processors replace synthetic concentrates with real fruit or vegetable bases. Clean-label reformulations have increased pulp utilization per product batch by nearly 15%, driving sustained demand growth across both B2B and foodservice channels.

Technological Advancements in Processing and Preservation

Innovations in aseptic packaging, individual quick freezing (IQF), and high-pressure pasteurization have revolutionized the pulp production process. These technologies ensure longer shelf life without compromising nutritional quality or flavor. Modern aseptic lines extend pulp shelf stability up to 18 months, improving supply reliability for beverage manufacturers and reducing post-harvest losses by 20–25%. Enhanced logistics and cold-chain integration allow producers in tropical regions to supply distant markets year-round, thereby supporting steady global trade and minimizing the traditional impact of seasonal supply cycles.

Growth of Convenience and Functional Beverage Segments

Rising consumption of ready-to-consume smoothies, energy drinks, and functional shots has intensified the industrial use of pulps as texture-enhancing and fiber-rich bases. In the U.S. alone, the functional beverage market grew by over 8% in 2024, with fruit and vegetable pulps forming a key ingredient base. Similarly, in Europe and Asia, health-driven beverage launches incorporating pulp-based formulations have tripled over the past five years. This sustained demand from beverage co-packers and foodservice chains anchors pulp utilization across the value chain.

Barrier Analysis - Raw Material Seasonality and Price Volatility

Fruit and vegetable pulps depend on seasonal harvests, leading to pronounced supply-side fluctuations. Inconsistent climatic conditions, droughts, and pest infestations often disrupt the availability of key raw materials such as mango, banana, guava, and tomato. Price volatility of up to 30% has been observed during poor harvest cycles, directly impacting processor margins. Limited cold-chain coverage in emerging economies increases waste risks, underscoring the need for contract farming and improved storage infrastructure to stabilize supply.

Compliance and Quality-Control Costs

Stringent food safety and traceability regulations across importing markets—such as the U.S. Food Safety Modernization Act (FSMA) and the EU’s General Food Law—demand continuous quality verification. Achieving certifications such as GFSI, HACCP, or ISO 22000 entails high operational costs, especially for small and medium processors. These compliance costs often range between 5–8% of total production expenses, limiting participation by smaller suppliers in export-oriented trade and reinforcing the market dominance of organized, large-scale processors.

Opportunity Analysis - Expansion of Premium and Functional Pulps

Consumers are increasingly willing to pay a premium for organic, cold-pressed, fiber-enriched, or probiotic-infused pulps. Industry projections suggest that premium pulps could account for 15–20% of market revenues by 2030, representing a segment value exceeding US$1 billion. Producers investing in traceable supply chains and R&D for nutrient-fortified formulations stand to achieve higher margins while capturing the growing health-conscious demographic.

Upcycling and By-Product Valorization

By-products from fruit processing, including peels, seeds, and pomace, are now being utilized to produce pectin, dietary fiber, and natural colorants. Upcycling initiatives reduce environmental footprints and also add incremental revenue streams estimated at 8–10% of total processor income. As investors increasingly emphasize sustainability and waste reduction, producers integrating circular-economy models are likely to build stronger partnerships with multinational food brands.

Export-Led Growth from Emerging Economies

Asia Pacific and Latin America are evolving into key global suppliers due to their favorable climates and lower production costs. Countries, including India, Thailand, and Mexico, have scaled up aseptic pulp exports to meet growing global demand. Export-driven expansions could raise regional revenue shares by 10–15% during the forecast period, aided by government incentives for food processing and improved port logistics.

Category-wise Analysis

Product Form Insights

In 2025, frozen pulps dominate global trade, comprising about 43.9% of total volume. Their long shelf life, ease of storage, and minimal processing make them ideal for bakery fillings, jams, desserts, ice cream, and institutional foodservice. Freezing preserves natural flavor, color, and nutrients, ensuring consistent quality. Frozen tomato pulp is particularly popular in sauces and ready-to-eat meals across Italy and the U.S. Bulk buyers, including bakery manufacturers and QSR chains, value frozen pulps for maintaining uniform texture and sweetness after thawing. Advances in individual quick freezing (IQF) technology have improved handling efficiency and minimized product wastage.

Aseptic pulps are emerging as the fastest-growing segment, offering ambient storage for up to 18 months without refrigeration due to heat treatment and sterilized packaging. This format provides logistical advantages, especially for exporters targeting regions with limited cold-chain infrastructure. Aseptic pulps are increasingly used in beverages, smoothies, baby foods, and dairy alternatives, where consistent quality and microbiological safety are critical. Beverage formulators rely on aseptic pulps for year-round uniformity, while tomato and carrot pulps find new applications in plant-based soups and sauces. Leading companies such as Döhler GmbH, Capricorn Food Products India Ltd., and SVZ International B.V. have invested heavily in aseptic processing to meet growing global demand.

Pulp Type Insights

In 2025, fruit pulps led the global market, accounting for around 66% of total revenue. Popular varieties —mango, banana, apple, guava, pineapple, and citrus —are key ingredients in beverages, jams, confectionery, and frozen desserts, valued for their natural sweetness, color, and flavor. Mango pulp dominates exports, with India supplying over 40% to the Middle East and Europe. Apple and pear pulps from China and Poland are crucial for baby foods and applesauce, while tropical pulps from Thailand, the Philippines, and Mexico drive juice and dessert production. Major beverage brands such as PepsiCo, Coca-Cola, and ITC Foods depend on steady pulp sourcing for consistent quality.

Vegetable pulps, including tomato, carrot, pumpkin, beetroot, spinach, and mixed vegetable blends, are gaining prominence due to rising demand for plant-based, low-sugar, and functional nutrition products. These pulps are increasingly used in soups, smoothies, sauces, baby foods, and ready-to-drink nutritional beverages. Brands such as Suja Life, Naked Juice, and Daily Harvest are introducing mixed-vegetable pulp smoothies blended with spinach, kale, and beetroot to appeal to health-conscious consumers. The growing popularity of flexitarian and vegan diets is driving applications in dairy alternatives and functional snacks. Vegetable pulps are being incorporated into probiotic- or fiber-fortified beverages, offering both nutritional benefits and visual appeal, further expanding their role in the wellness-focused food and beverage sector.

Regional Insights

Asia Pacific Fruit and Vegetable Pulp Market Trends - Production Powerhouse and Export Expansion

Asia Pacific continues to lead the global fruit and vegetable pulp market, accounting for an estimated 41.8% of total demand in 2025. The region benefits from diverse tropical and subtropical crops, high fruit yields, and well-developed export infrastructure. India, Thailand, the Philippines, and China dominate production, supported by favorable climates, cost-competitive labor, and government initiatives promoting agro-industrial growth. India leads mango and guava pulp exports, accounting for nearly 40% of global shipments, while Thailand and the Philippines are key producers of pineapple and banana pulp.

Rising domestic consumption of processed foods, ready-to-drink beverages, and convenience-focused fruit blends further drives market expansion. Programs such as India’s Production Linked Incentive (PLI) Scheme for Food Processing and Thailand’s Bio-Circular-Green (BCG) Economy Strategy have accelerated investments in pulp extraction and packaging technologies. Industry partnerships, such as Döhler Group’s 2024 collaboration with China Huiyuan Juice Group, and increased adherence to Codex Alimentarius and ISO 22000 standards reinforce APAC’s position as a major hub for both the production and export of fruit and vegetable pulps.

North America Fruit and Vegetable Pulp Market Trends - Clean-Label Growth and Traceable Supply Networks

North America is the fastest-growing and most lucrative value market, with the U.S. leading consumption through its large beverage and convenience-food industries. The region’s emphasis on clean-label, traceable, and functional ingredients aligns perfectly with pulp applications. Strict regulatory frameworks such as FSMA ensure high product quality, favoring established suppliers with certified facilities.

Investments in aseptic processing and traceability technology are rising across the U.S. and Canada, ensuring a consistent supply to beverage manufacturers. The presence of major health-drink brands and expanding smoothie chains continues to anchor regional pulp imports. Mexico’s role as both a processor and exporter strengthens the region’s integrated supply network.

Europe Fruit and Vegetable Pulp Market Trends - Premium, Organic, and Sustainable Sourcing

Europe remains a premium-oriented market, emphasizing organic sourcing, traceability, and origin labeling. Germany, France, Spain, and the U.K. are leading importers and processors of both fruit and vegetable pulps. The region’s stringent food safety regulations, under the European Food Safety Authority (EFSA), drive investments in advanced preservation and traceability systems.

Demand for organic and fair-trade pulps has accelerated, particularly in Western Europe, where consumers favor authenticity and transparency. Processing clusters in Germany and the Netherlands serve as innovation hubs for fruit preparations. Consolidation among mid-sized ingredient firms and partnerships with global beverage brands are reshaping the competitive landscape toward premium, sustainable sourcing.

Competitive Landscape

The global fruit and vegetable pulp market is moderately fragmented, characterized by a mix of multinational ingredient manufacturers and regional processors. Large companies account for an estimated 40–45% of the global market share, while numerous small-scale processors operate domestically or within niche export markets.

Value-added segments such as organic and aseptic pulps are comparatively consolidated due to the high capital requirements for advanced processing equipment. Leading players focus on product differentiation, supply-chain integration, and sustainability. Strategies include developing organic and fortified pulp variants, establishing contract farming models, and investing in energy-efficient, zero-waste processing plants. Thematic priorities center around innovation, traceability, and market diversification to capture long-term brand partnerships with beverage and dairy manufacturers.

Key Industry Developments

- In March 2025, Döhler GmbH expanded its fruit ingredient portfolio with new aseptic pulp product systems aimed at beverage and dairy manufacturers. The expansion reinforced its leadership in the natural ingredient segment and increased processing capacity across Europe and Asia.

- In September 2024, AGRANA Beteiligungs-AG announced significant investments in its fruit preparation and pulp production facilities in Austria and India. The initiative strengthened its position in the value-added fruit ingredient sector and enhanced vertical integration from farm to processing.

- In 2025, multiple Indian and Thai processors commissioned new aseptic packing lines to target export markets, supported by government incentives for food processing. These developments are expected to improve export competitiveness and address global supply gaps in premium pulp formats.

Companies Covered in Fruit and Vegetable Pulp Market

- Döhler GmbH

- AGRANA Beteiligungs-AG

- SunOpta Inc.

- Iprona AG

- Allanasons Ltd.

- Keventer Group

- Ingredion Incorporated

- Jain Irrigation Systems Ltd.

- SVZ International B.V.

- Capricorn Food Products India Ltd.

- Tate & Lyle PLC

- Kerry Group PLC

- Mother Dairy Fruit & Vegetable Pvt Ltd.

- Conagra Brands Inc.

- Sunimpex International Foods

- Parle Agro Pvt Ltd.

- Del Monte Foods, Inc.

- Heinz India Pvt Ltd.

- Natco Foods Ltd.

- Future Consumer Ltd.

Frequently Asked Questions

The fruit and vegetable pulp market size is estimated at US$3.1 Billion in 2025.

The fruit and vegetable pulp market size is projected to reach US$4.8 Billion by 2032, reflecting steady growth.

Key trends include the rising demand for clean-label and natural ingredients in beverages and snacks and the rapid adoption of aseptic pulp formats for shelf-stable applications.

Frozen fruit pulps are the leading segment, accounting for approximately 43.9% of the total global trade, widely used in bakery, jam, dessert, and foodservice applications.

The fruit and vegetable pulp market is projected to grow at a CAGR of 6.3% between 2025 and 2032, driven by the rising demand for functional beverages, plant-based formulations, and premium fruit pulps.

Major companies include Döhler GmbH, AGRANA Beteiligungs-AG, SunOpta Inc., Allanasons Ltd., and Keventer Group.