- Display Technologies

- Free Standing Display Units Market

Free Standing Display Units Market Size, Share, and Growth Forecast, 2026 - 2033

Free Standing Display Units Market by Material (Plastic, Cardboard, Others), Product Type (Full-Floor Displays, Pallet Displays, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Free Standing Display Units Market Size and Trends Analysis

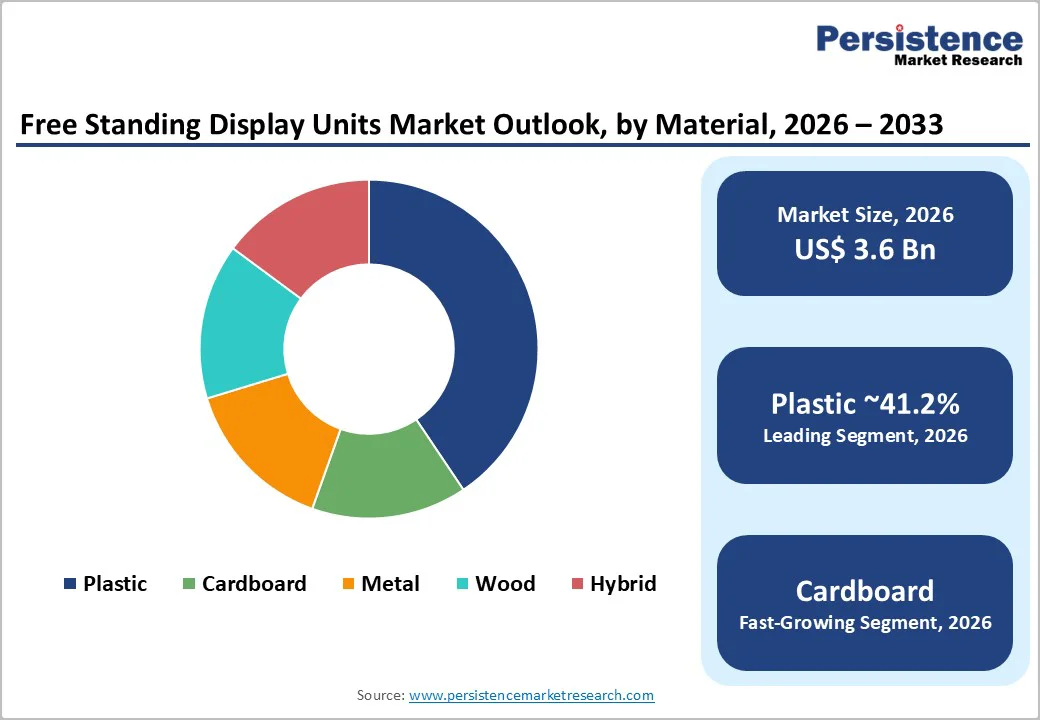

The global free standing display units market size is likely to be valued at US$3.6 billion in 2026 and is expected to reach US$5.4 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033, driven by sustained retailer focus on in-store conversion and impulse purchasing, continuous material and process innovations that improve cost efficiency, and increasing adoption of sustainable and digitally enabled display solutions.

These factors are driving higher per-store merchandising investments across grocery, pharmacy, convenience, and specialty retail formats. The overall trajectory reflects consistent structural demand for physical point-of-purchase engagement despite the parallel rise of e-commerce.

Key Industry Highlights

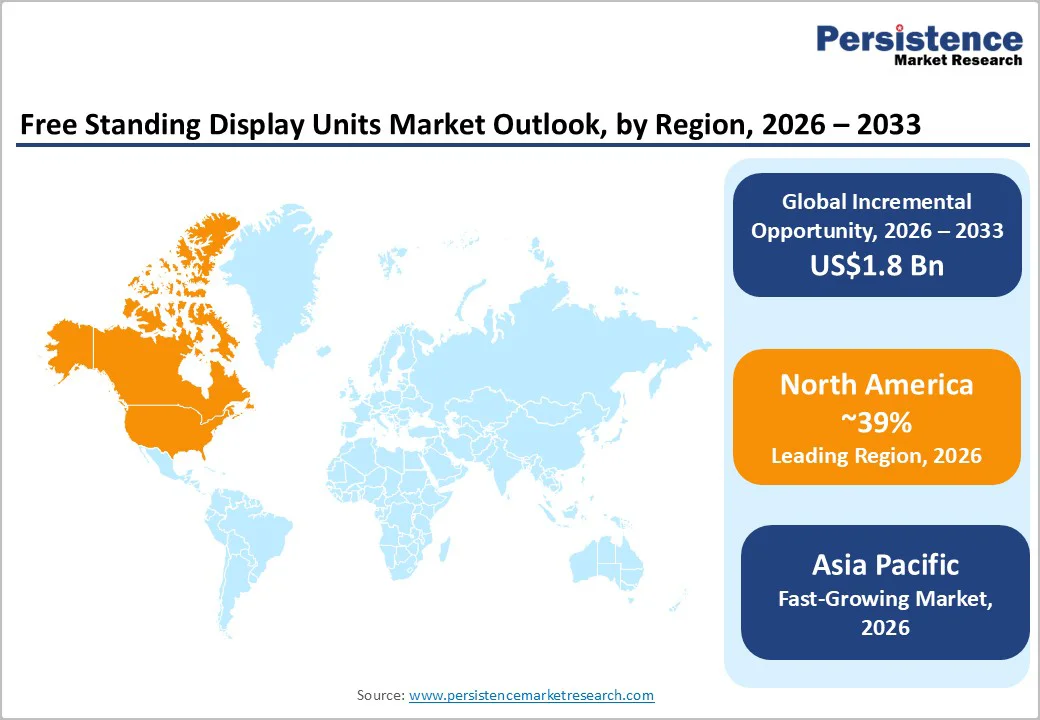

- Leading Region: North America is expected to lead the global free-standing display units (FSDU) market, with an estimated 39% share, supported by the dominance of large-format retail chains, centralized merchandising programs, and higher per-store display deployments across the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing regional market, driven by rapid retail modernization in China, India, and ASEAN economies, along with rising brand investments in in-store visibility.

- Investment Plans: Manufacturers and brand owners are prioritizing investments in sustainable materials, modular reusable display systems, and digitally enabled FSDUs, with an estimated 30-35% of new display program budgets allocated toward recyclable corrugated structures, hybrid materials, and smart display features.

- Dominant Material: Plastic displays are expected to dominate, with approximately 41.2% market share, owing to their durability, moisture resistance, and suitability for multi-cycle promotional use in high-traffic retail environments.

- Leading End-use Industry: The food and beverages segment is estimated to remain the largest segment, accounting for roughly 30.8% of market share, driven by impulse purchasing behavior and frequent promotional turnover in grocery and convenience retail formats.

| Key Insights | Details |

|---|---|

| Free Standing Display Units Market Size (2026E) | US$3.6 Bn |

| Market Value Forecast (2033F) | US$5.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - In-store Decision Density and Retail Merchandising ROI

A substantial proportion of consumer purchasing decisions continues to occur within physical retail environments. Industry surveys indicate that approximately 70-76% of purchase decisions are made in-store, underscoring the importance of effective point-of-purchase visibility. Free-standing display units directly influence impulse buying behavior by positioning products in high-traffic areas, including aisles, end caps, and promotional zones.

Retail pilots and brand campaigns consistently report double-digit percentage sales uplifts for new product launches supported by prominent floor-standing displays. As a result, brands allocate recurring budgets toward FSDU deployment and replacement cycles. This steady demand for campaign-driven displays contributes to the market’s sustained mid-single-digit growth trajectory and reinforces FSDUs as a measurable return-on-investment merchandising tool.

Material Innovation, Sustainability Mandates, and Cost Substitution

Procurement strategies increasingly favor fiber-based corrugated and hybrid composite materials due to their lower lifecycle costs and compliance with retailer sustainability requirements. Corrugated displays offer recyclability, lightweight handling, and cost advantages, making them suitable for high-volume promotional rollouts.

Ongoing investments in recycling infrastructure and closed-loop sourcing have improved material availability and reduced long-term cost volatility. Standardized certifications for responsibly sourced materials have also expanded adoption in regions with strict sustainability frameworks. These shifts support both volume growth and selective premium pricing for certified and environmentally compliant display solutions.

Digitization and Modularization of Display Formats

Retailers and consumer brands are increasingly integrating QR codes, near-field communication, sensors, and low-power digital screens into floor-standing displays. Advances in display hardware affordability and cloud-based content management systems have enabled dynamic in-store messaging, real-time campaign updates, and performance measurement.

Digitally enabled FSDUs support new use cases, including interactive promotions, shopper engagement tracking, and inventory visibility. These capabilities justify higher per-unit pricing and shorten replacement cycles in developed retail markets. Modular and reusable designs further enhance long-term value by allowing reconfiguration across multiple campaigns.

Barrier Analysis - Supply Chain and Raw Material Price Volatility

The FSDU market depends heavily on raw materials such as corrugated board, polymer resins, surface coatings, and electronic components. Price fluctuations in pulp, plastics, and semiconductors introduce cost unpredictability, particularly for custom or low-volume display programs.

Historical input cost spikes have led to single-year cost increases of 10% to 30%, compressing margins and delaying purchasing decisions. In response, some brands shift toward reusable retailer-owned fixtures or reduce campaign frequency, limiting short-term demand growth in cost-sensitive markets.

Execution and Compliance Complexity in Multi-Store Rollouts

Large-scale FSDU deployments often face execution challenges at the store level. Audits frequently show that a meaningful share of displays are incorrectly assembled, poorly positioned, or not installed at all. These execution gaps materially reduce campaign effectiveness and weaken ROI justification.

Logistical complexity, including transportation, assembly labor, store-specific placement rules, and local compliance requirements, increases rollout costs. When execution failure rates exceed 20-30%, brands tend to reallocate budgets toward trade promotions or digital advertising, slowing replacement cycles for traditional FSDUs.

Opportunity Analysis - Recyclable Fiber-Based Displays in Regulated Markets

Retailers in North America and Europe are tightening sustainability standards for in-store materials, driven by extended producer responsibility rules, packaging waste directives, and retailer-led ESG scorecards that increasingly influence supplier qualification and promotional access. Transitioning 40-60% of display volume to certified corrugated or post-consumer fiber formats enables suppliers to secure preferred-vendor status and long-term contracts, while also reducing exposure to plastic restrictions, disposal fees, and compliance risk.

Advances in structural corrugated design, mono-material construction, and water-based inks are improving durability and load performance, allowing fiber-based FSDUs to support longer in-store lifecycles and repeated promotional use. If fiber-based FSDUs capture an incremental US$200-350 million in global spending by 2028, manufacturers with certified sourcing, scalable regional production, and transparent sustainability reporting, including lifecycle and carbon disclosures, stand to gain durable, repeat-program revenue streams while strengthening retailer relationships and mitigating regulatory pressure.

Digital FSDUs and Retail-Media Monetization

Sensor-enabled and digital FSDUs support measurable engagement metrics, including dwell time, impressions, and interaction rates, enabling real-time optimization of creative content and placement effectiveness. These displays can be integrated into retail-media networks, functioning as physical extensions of retailers’ broader media ecosystems and allowing brands to attribute in-store performance more precisely to sales uplift.

As retailers seek higher monetization per square foot, digital FSDUs offer a compelling alternative to static fixtures by combining hardware deployment with recurring revenue from content management, analytics, and campaign services. If digital FSDUs achieve 5-10% penetration within modern grocery and convenience networks by 2028, the combined hardware and recurring content services opportunity could reach a meaningful scale, with subscription-based models significantly enhancing supplier margins, stabilizing revenue, and extending customer lifetime value compared to traditional single-use displays.

Category-wise Analysis

Material Insights

Plastic displays are anticipated to dominate the FSDU market with an estimated 41.2% share, supported by their durability, moisture resistance, and multi-cycle reusability. These displays are widely used in convenience stores, beverage aisles, and outdoor or semi-outdoor retail environments, where exposure to humidity, temperature variation, and frequent handling is common. Injection-molded and thermoformed plastics enable consistent quality at scale, while integrated shelving, hooks, and LED lighting enhance product visibility for categories such as carbonated drinks, snacks, and personal care items. Their long service life makes them suitable for brand-owned or retailer-owned display programs that run across multiple promotional periods.

Cardboard and corrugated displays are anticipated to be the fastest-growing material segment, driven by cost efficiency, recyclability, and fast production cycles. Lightweight construction allows easy transportation and rapid in-store setup, supporting short-term promotions and seasonal campaigns. Advances in high-resolution digital printing, die-cut engineering, and surface coatings have significantly improved structural strength and visual appeal, narrowing the performance gap with plastic alternatives. These displays are increasingly adopted for FMCG product launches, snack foods, confectionery, and limited-time offers, particularly in supermarkets and hypermarkets where sustainability compliance and quick campaign turnover are prioritized.

End-use Industry Insights

The food and beverages sector is estimated to lead FSDU adoption with approximately 30.8% market share, reflecting the category’s strong reliance on impulse purchasing and high promotional intensity. Floor-standing displays are commonly deployed for snacks, beverages, confectionery, and ready-to-eat products, especially during seasonal promotions and new product introductions. Frequent campaign rotation and high SKU velocity support steady demand for both corrugated single-use displays and durable plastic units in high-traffic retail zones such as store entrances and aisle intersections.

The cosmetics and personal care segment is likely to be the fastest-growing end-use segment, expanding at roughly 7% CAGR, driven by premiumization and experiential merchandising trends. Brands increasingly use FSDUs with integrated lighting, mirrors, testers, and digital screens to enhance consumer engagement and brand differentiation. These displays are particularly prominent in drugstores, beauty specialty retailers, and premium supermarkets, where visual impact directly influences trial and conversion. Higher design complexity and material quality elevate average unit value, contributing to above-average revenue growth within this segment.

Regional Insights

North America Free Standing Display Units Market Trends - Retail Media Monetization and Sustainable Smart Displays in U.S.-Led Big-Box Retail

North America is projected to remain the largest regional market, accounting for approximately 39% of global FSDU demand, with the U.S. driving most consumption due to its highly developed big-box, grocery, and specialty retail ecosystem. Large retailers such as Walmart, Target, Costco, and Kroger rely on centralized procurement models and standardized display programs to support high-volume deployment of floor-standing and pallet-based units. Growth is increasingly influenced by retail media monetization, in which brands invest in high-impact displays that serve as in-store advertising assets. Companies such as PepsiCo and Procter & Gamble have expanded the use of branded, reusable plastic and hybrid displays with integrated signage and lighting to improve campaign ROI across multi-store rollouts.

Sustainability initiatives are also reshaping material selection. Major retailers, including Walmart and CVS Health, have introduced supplier sustainability scorecards and packaging waste reduction targets, encouraging a shift toward recyclable corrugated and reusable modular display systems. At the same time, adoption of digitally enabled FSDUs, including QR codes, NFC tags, and embedded screens, has increased, particularly in electronics, personal care, and health categories. U.S.-based display manufacturers such as FFP, Great Northern Corporation, and Creative Displays Now have expanded digital printing and smart-display capabilities, reinforcing North America’s leadership in innovation-driven retail merchandising.

Europe Free Standing Display Units Market Trends - Regulation-Driven Shift toward Fiber-Based and Modular Displays across European Retail

Europe is a significant market for free-standing display units, with Germany, the U.K., France, and Spain serving as core demand centers. The region’s FSDU market is strongly shaped by regulatory frameworks focused on recyclability, waste reduction, and extended producer responsibility (EPR). EU directives on packaging waste and national-level enforcement have accelerated the adoption of fiber-based, mono-material, and reusable display formats, particularly in grocery and drugstore retail. Retailers such as Tesco, Carrefour, Aldi, and Lidl increasingly specify corrugated or paper-based displays that meet recycling and lifecycle assessment requirements.

Brand owners have responded by redesigning merchandising strategies. For example, Unilever and Nestlé have publicly committed to reducing virgin plastic use across in-store promotional materials, leading to higher demand for corrugated, molded fiber, and hybrid displays in European campaigns. Investment is also concentrated in modular and premium experiential formats, especially in cosmetics and electronics, where brands deploy reusable display structures with interchangeable graphic panels to comply with sustainability goals while maintaining visual differentiation. European display specialists such as DS Smith, Smurfit Kappa, and STI Group continue to expand sustainable design and rapid customization capabilities, reinforcing Europe’s position as a leader in regulation-driven innovation.

Asia Pacific Free Standing Display Units Market Trends - Manufacturing Scale and Modern Trade Expansion Fueling Asia-Pacific FSDU Growth

Asia Pacific is the fastest-growing regional market, supported by rapid urbanization, retail infrastructure development, and rising middle-class consumption across multiple economies. China plays a dual role as both the largest manufacturing hub and a major consumption market, with domestic retailers and global brands leveraging cost-efficient production of plastic, metal, and hybrid FSDUs. Chinese manufacturers supply large volumes of promotional displays for multinational FMCG brands operating across the Asia Pacific, benefiting from integrated supply chains and scalable production capacity.

In India and ASEAN markets, growth is primarily demand-driven, fueled by the expansion of organized retail, supermarkets, and modern trade formats. Retailers such as Reliance Retail, DMart, Lotus’s, and Big C have increased the use of floor-standing and pallet displays to improve product visibility and drive impulse purchases. International brands, including Coca-Cola, L’Oréal, and Samsung, are investing more heavily in localized display designs tailored to smaller store formats and high footfall conditions. As brand competition intensifies, spending on visually differentiated and semi-permanent FSDUs continues to rise, positioning Asia Pacific as a long-term growth engine for both global and regional display manufacturers.

Competitive Landscape

The global free standing display units market is moderately consolidated at the material supplier level and highly fragmented at the fabrication and regional execution level. Large packaging and substrate suppliers control a significant upstream share, while numerous regional players compete in customization, speed, and local execution. Leading players prioritize sustainability certification, digital integration, and vertical integration across design, manufacturing, logistics, and in-store execution. Competitive differentiation increasingly depends on analytics capability, execution reliability, and scalable certified supply chains.

Key Industry Developments

- In May 2025, WestRock launched EcoShow, a modular and fully recyclable display system designed for quick assembly and sustainability compliance, positioning it to meet increasing retailer demand for eco-friendly merchandising solutions.

- In January 2025, Avery Dennison announced a strategic partnership with Seiko Epson to co-develop advanced digital point-of-purchase display solutions, aiming to enable retailers to deploy customized, data-driven in-store displays that enhance consumer engagement.

Companies Covered in Free Standing Display Units Market

- Smurfit Kappa

- DS Smith

- WestRock

- International Paper

- Sonoco Products Company

- Georgia-Pacific

- FFP Packaging Solutions

- Creative Displays Now

- Great Northern Corporation

- STI Group

- BDS Marketing

- HL Display

- Rapid Displays

- Pratt Industries

- Packaging Corporation of America

- Miller Zell

- Felbro Displays

- Tilsner Carton Company

- Peak Design Displays

Frequently Asked Questions

The global free standing display units market is estimated to be valued at US$3.6 billion in 2026.

By 2033, the free standing display units market is projected to reach US$5.4 billion.

Key trends include rising adoption of recyclable and fiber-based displays, increased use of modular and reusable structures, integration of digital and interactive elements, and growing alignment with retailer sustainability and waste-reduction mandates.

The food and beverages end-use segment leads the free standing display units market with approximately 30.8% share, driven by impulse purchase behavior and frequent promotional cycles in grocery and convenience retail.

The market is expected to grow at a CAGR of 5.9% between 2026 and 2033.

Major players with strong portfolios include Smurfit Kappa, DS Smith, WestRock, Sonoco Products Company, and International Paper.