- Food Packaging

- BPA-free Coatings Market

BPA-free Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

BPA-free Coatings Market By Material Type (Acrylic-Based Coatings, Polyester-Based Coatings, Others), Application (Can Liners, Bottles, Others), End-use Industry, and Regional Analysis for 2026 - 2033

BPA-free Coatings Market Size and Trends Analysis

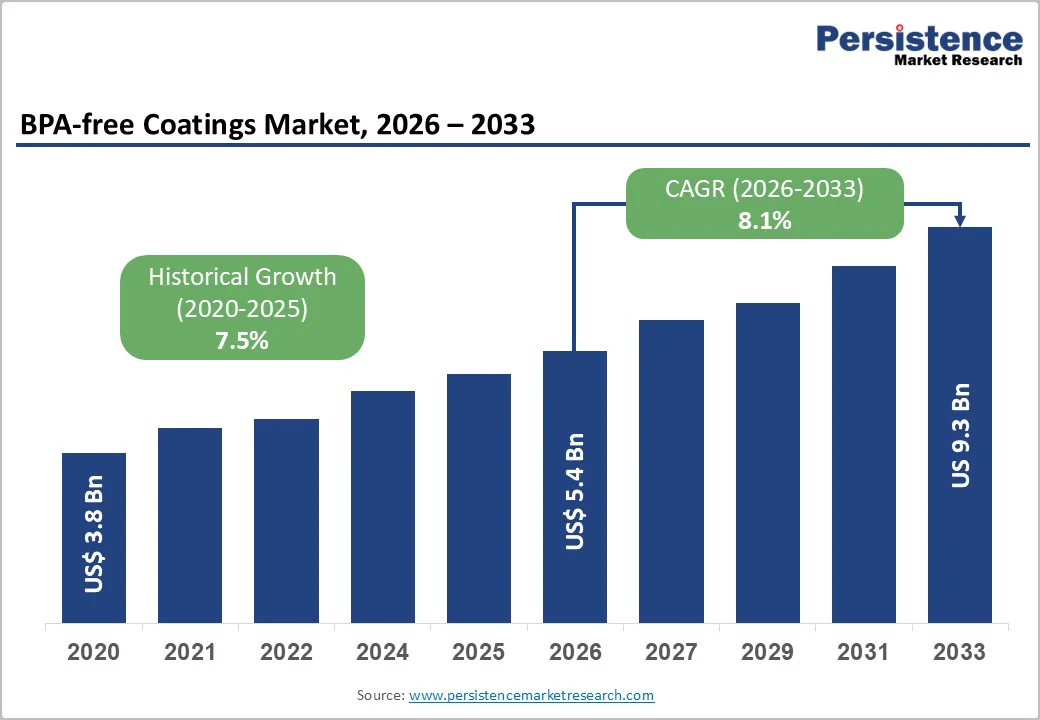

The global BPA-free coatings market size is likely to be valued at US$5.4 billion in 2026 and is expected to reach US$9.3 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033, driven by regulatory restrictions on bisphenol A, accelerated conversion of metal packaging and bottle coatings to non-bisphenol chemistries, and sustained investments by major coatings manufacturers in BPA-NI technologies and regional production capacity.

Consumer safety concerns and brand risk mitigation continue to reinforce adoption across food & beverage and healthcare end-uses.

Key Industry Highlights

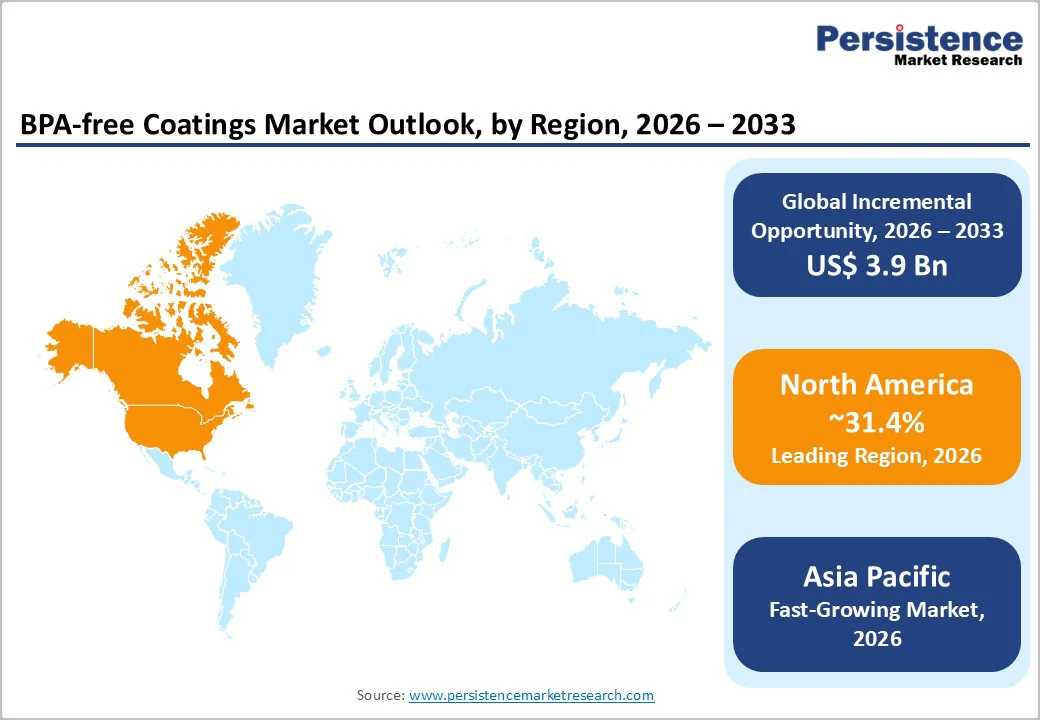

- Leading Region: North America is projected to account for approximately 31.4% of global market share, supported by large-scale beverage and canned food production, strong brand-led BPA substitution commitments, and a mature packaging supply chain ecosystem.

- Fastest-growing Region: Asia Pacific, projected to record the highest growth rate through 2033, driven by expanding packaged food consumption, export-oriented compliance requirements, and increasing local production investments across China, India, and ASEAN markets.

- Investment Plans: Capacity expansion and product validation investments are concentrated in Asia Pacific and Europe, with suppliers allocating capital to localized manufacturing, technical service centers, and qualification labs to support the adoption of BPA-free acrylic and polyester coatings for food-contact and beverage applications.

- Dominant Material Type: Acrylic-based coatings are anticipated to hold approximately 44.8% market share, due to broad regulatory acceptance, compatibility with waterborne formulations, and widespread use across can bodies, closures, and general food-contact applications.

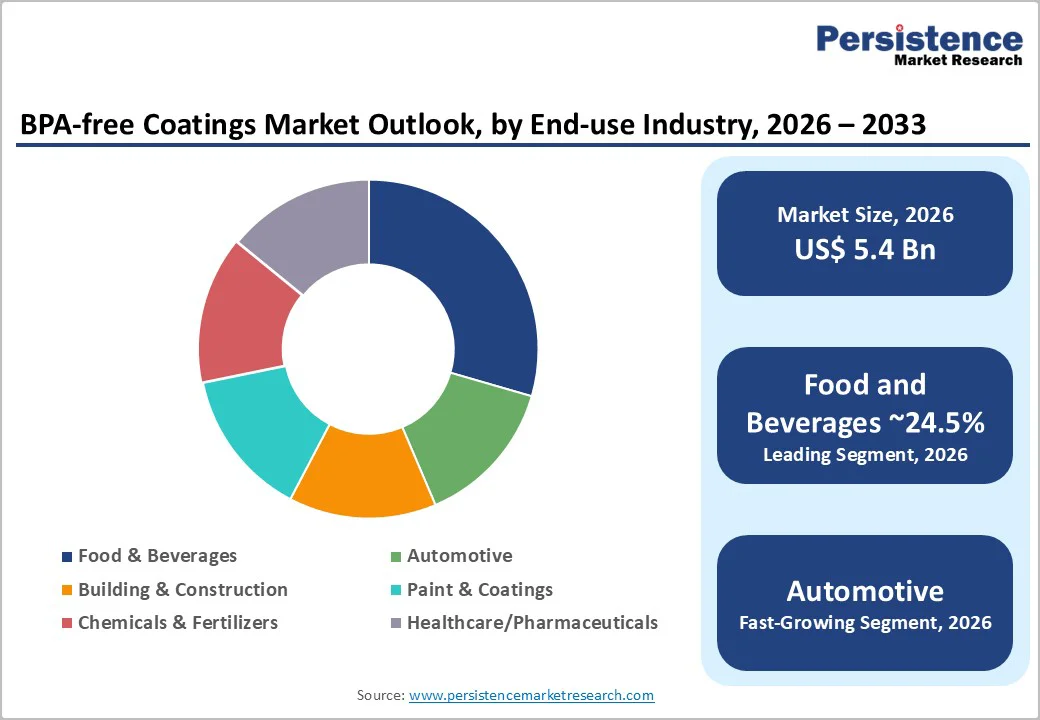

- Leading End-use Industry: Food & beverages are estimated to represent around 24.5% of total demand in 2026, driven by high regulatory exposure, consumer safety expectations, and sustained adoption across canned foods, beverages, and prepared-meal packaging.

| Key Insights | Details |

|---|---|

| BPA-free Coatings Market Size (2026E) | US$5.4 Bn |

| Market Value Forecast (2033F) | US$9.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Tightening and Explicit Bans on BPA in Food-Contact Materials

Regulatory action across key global markets has become the most decisive growth catalyst for BPA-free coatings. In Europe, the introduction of binding restrictions on bisphenol A in food-contact materials has established firm compliance deadlines for coatings, varnishes, and linings used in cans, containers, and closures.

Updated toxicological assessments have significantly lowered acceptable exposure thresholds, effectively accelerating mandatory replacement cycles. This regulatory clarity reduces uncertainty for brand owners and can manufacturers, compelling rapid conversion of product lines and increasing near-term procurement volumes. As a result, BPA-free coatings have shifted from optional substitutes to compliance-critical materials in regulated food-contact applications.

Brand, Retailer, and Consumer Pressure for Safer Packaging

Beyond regulation, commercial pressure from brand owners and retailers has emerged as a powerful driver of adoption. Large food and beverage companies increasingly mandate verified absence of BPA or strict migration limits in packaging materials to protect brand equity and reduce litigation exposure.

Heightened public awareness of chemical safety, combined with media scrutiny of food-contact materials, has made BPA-free claims commercially significant. Suppliers capable of demonstrating validated migration performance, traceability, and compliance documentation are securing long-term supply agreements. This shift has transformed BPA-free coatings from a discretionary sustainability upgrade to a strategic procurement requirement.

Technology Maturation and Supplier Investments

Technological progress has materially improved the performance profile of BPA-free coatings. Advances in acrylic, polyester, and engineered non-bisphenol polymer systems, alongside waterborne and radiation-cured technologies, have narrowed historical gaps in corrosion resistance, shelf-life stability, and processing tolerance.

Large-scale investments in research, pilot testing, and regional manufacturing capacity have lowered qualification risks for converters and brand owners. These improvements have enabled broader replacement of epoxy-based systems across demanding applications, reinforcing confidence in BPA-free solutions as viable long-term alternatives.

Barrier Analysis - Conversion Cost and Supply-Chain Scaling

Transitioning to BPA-free coatings requires comprehensive requalification programs, including line trials, migration testing, and in some cases, equipment or process adjustments. Raw material costs for alternative chemistries remain higher than legacy epoxy-based systems, increasing unit costs during early adoption phases.

In highly price-sensitive packaging categories, these cost pressures can delay conversion decisions, particularly in regions with less stringent regulatory enforcement. Supply-chain scaling also presents challenges, as consistent quality and availability must be ensured across global production networks during transition periods.

Performance Parity and Formulation Complexity

Achieving full functional parity with traditional epoxy systems remains technically demanding. Early-generation BPA-NI coatings occasionally exhibited limitations under aggressive food chemistries, high-temperature sterilization, or extended shelf-life conditions.

Addressing these issues requires complex formulation work, multi-disciplinary testing, and prolonged validation cycles. These technical hurdles can extend qualification timelines and increase the risk of reformulation costs if performance gaps emerge after commercialization. For brand owners, this translates into cautious adoption strategies and phased rollouts rather than immediate system-wide conversion.

Opportunity Analysis - Can Coatings and Beverage-End Replacement

BPA-free can linings and beverage-end coatings represent one of the fastest-moving and most clearly defined opportunities in the coatings market. Regulatory pressure and high consumer visibility have made these applications top priorities for conversion.

Beverage-end coatings, in particular, account for a significant share of near-term replacement demand, creating a sizable addressable market for suppliers with certified, fast-qualifying solutions. Manufacturers that offer strong technical support, rapid testing, and scalable supply are well-positioned to gain share as conversion accelerates across global beverage packaging networks.

Asia Pacific Manufacturing Scale and Export Orientation

Asia Pacific represents the largest growth opportunity due to its manufacturing scale, rising packaged food consumption, and export-driven packaging industries. Localized production of BPA-free coatings reduces logistics costs and shortens qualification timelines for regional converters serving both domestic and export markets.

As packaging produced in Asia increasingly supplies markets with strict chemical regulations, demand for compliant coatings continues to rise. Suppliers with established production and technical infrastructure in the region are positioned to benefit from sustained volume growth and cost-efficient expansion.

Category-wise Analysis

Material Type Insights

Acrylic-based coatings are anticipated to hold the leading position, accounting for approximately 44.8% of the total demand. Their dominance reflects strong adaptability across both metal and plastic substrates, favorable regulatory acceptance, and compatibility with waterborne and low-solvent formulation platforms.

Acrylic systems are extensively used in can bodies, external packaging surfaces, closures, and general food-contact applications where low migration, optical clarity, and stable processing behavior are essential.

Ongoing improvements in binder purity, molecular weight control, and extractables management have strengthened the performance of acrylic coatings under pasteurization and short-to-medium shelf-life conditions. For example, waterborne acrylic systems are widely adopted for beverage can exteriors and food container glass coatings, where regulatory compliance and aesthetic consistency are critical.

Their relatively straightforward reformulation and qualification pathways also make acrylics a preferred first-line replacement during epoxy-to-BPA-free transitions, particularly for brand owners seeking rapid regulatory compliance with minimal production disruption.

Polyester-based coatings are likely to be the fastest-growing material segment due to their ability to replicate many functional attributes of epoxy systems while eliminating bisphenol content.

These coatings offer enhanced chemical resistance, thermal stability, and adhesion, making them suitable for demanding food-contact applications that involve aggressive contents or high-temperature sterilization. As a result, polyester systems are increasingly used in beverage ends, food can interiors, and high-acidity product packaging, where simpler acrylic formulations may face performance limitations.

Recent product innovations and successful commercial pilots have expanded confidence in polyester-based solutions across global canmaking operations. For instance, polyester coatings are gaining traction in carbonated beverage cans and ready-to-eat food containers, where resistance to carbonation pressure and acidic formulations is critical.

As validation data accumulates and supply chains mature, polyester coatings are expected to capture incremental share from legacy epoxy formulations, particularly in technically demanding and high-risk packaging environments.

End-use Industry Insights

Food and beverage applications are estimated to account for approximately 24.5% of the market share. High regulatory exposure, strict food-contact safety requirements, and elevated consumer sensitivity to packaging materials drive early and sustained adoption in this category.

Demand spans canned foods, beverage cans, bottle interiors, closures, and ready-meal containers, with particularly strong uptake in categories with long shelf lives or that undergo thermal processing.

Large branded manufacturers dominate procurement and typically require multi-site approvals, validated migration testing, and consistent global supply, favoring suppliers with established regulatory documentation and scalable production.

For example, multinational beverage and canned food producers increasingly specify BPA-free linings as a baseline requirement across global packaging platforms, reinforcing steady, contract-driven demand and long-term supplier relationships within this segment.

Automotive is the fastest-growing end-use segment for BPA-free coatings, driven by rising demand for non-toxic, high-performance materials in interior and functional components.

Growth is supported by vehicle electrification, increased use of mixed substrates, and stricter material restrictions related to passenger safety and environmental compliance. BPA-free coatings are being evaluated for interior metal parts, battery-adjacent components, and corrosion-resistant functional coatings, where chemical stability and low emission profiles are required.

Although qualification cycles in the automotive sector are lengthy, successful approvals provide access to long-term, high-value supply contracts. As OEMs increasingly align interior material specifications with broader sustainability and chemical-restriction frameworks, BPA-free coatings are positioned to gain sustained traction in automotive platforms, particularly in electric and next-generation vehicle architectures.

Regional Insights

North America BPA-free Coatings Market Trends - Brand-Led Adoption Supported by Integrated Supply Chains

North America is projected to account for roughly 31.4% of market share, with the U.S. as the primary contributor, supported by large-scale manufacturing of beverages, canned foods, and processed foods. Major canmakers and brand owners operate integrated supply chains across the U.S., Mexico, and Canada, enabling faster formulation changes and qualification cycles.

While federal regulatory positions on bisphenol A differ from Europe’s precautionary framework, state-level actions, including restrictions on BPA use in food-contact materials for infant and child products, have created indirect pressure for broader substitution across packaging portfolios.

Brand-led initiatives have played a decisive role in accelerating adoption. Large beverage and food companies, including The Coca-Cola Company, PepsiCo, and Campbell Soup Company, have publicly committed to reducing or eliminating BPA-containing linings across significant portions of their packaging, prompting upstream suppliers to expand the use of acrylic- and polyester-based alternatives.

Packaging suppliers such as Ball Corporation and Crown Holdings have invested in reformulating internal can coatings to meet customer specifications, reinforcing North America’s role as an early commercialization market.

The region also benefits from strong technical infrastructure, with coating suppliers maintaining application laboratories and pilot lines in the U.S. to support rapid testing and regulatory documentation. These capabilities have enabled faster deployment of BPA-free solutions in beverage cans, aerosol containers, and specialty food packaging. Continued innovation activity and long-term supply agreements support stable growth, even as regulatory drivers remain largely market-led rather than federally mandated.

Europe BPA-free Coatings Market Trends - Regulation-Driven Mandatory Substitution across Food Contact Applications

Europe is the most regulation-driven market for BPA-free coatings, with binding restrictions on bisphenol A creating mandatory replacement demand across food-contact applications.

Revisions to BPA exposure limits by the European Food Safety Authority, followed by concrete policy actions, have accelerated substitution across metal packaging, closures, and food containers. This clear regulatory framework has reduced uncertainty for manufacturers, supporting continued capital investment and long-term formulation development.

Germany leads the region in both innovation and manufacturing capacity, supported by a strong base of chemical producers and packaging technology providers. Companies such as BASF and Altana (ACTEGA) have expanded their BPA-free coating portfolios to align with European food-contact compliance requirements.

The U.K., France, and Spain exhibit high adoption rates due to their large packaged food industries and export-oriented production, where compliance with EU standards is essential for cross-border trade.

Regulatory harmonization across the European Union has accelerated qualification timelines and cross-country approvals, enabling coating suppliers to scale solutions more efficiently.

As a result, Europe often serves as a reference market for BPA-free coating performance and compliance, with formulations validated in Europe later adapted for deployment in other regions. This position strengthens Europe’s influence on global product standards and supplier roadmaps, despite comparatively slower volume growth than the Asia Pacific.

Asia Pacific BPA-free Coatings Market Trends - Export-Driven Growth and Rapid Manufacturing Scale-Up

Asia Pacific is the fastest-growing regional market for BPA-free coatings, driven by expanding packaged food and beverage consumption, rapid urbanization, and the presence of large can and bottle manufacturing bases.

The region’s growth is further reinforced by export-driven compliance requirements, as producers supplying Europe and North America must align with BPA-free standards regardless of local regulations. This dynamic has accelerated voluntary adoption across key manufacturing hubs.

China leads in production scale, with extensive canmaking and metal packaging capacity serving both domestic consumption and export markets. Major packaging suppliers operating in China have increasingly introduced BPA-free coating lines to meet international customer specifications.

Japan, by contrast, leads in specialty coating technology, supported by long-standing expertise in food safety, material science, and high-precision manufacturing. Japanese coating suppliers have played an important role in advancing polyester and hybrid BPA-free systems suitable for demanding applications.

India and ASEAN countries represent the fastest-growing demand centers, supported by rising packaged food consumption, expanding beverage markets, and investments in local can manufacturing. Multinational coating suppliers have increased regional production and technical support to reduce costs and accelerate customer qualification.

These localized investments improve supply reliability and shorten approval cycles, positioning Asia Pacific as a central pillar of long-term volume growth and global capacity expansion for BPA-free coatings.

Competitive Landscape

The global BPA-free coatings market exhibits a moderately consolidated structure. Global coatings manufacturers dominate high-volume, regulated applications, while regional specialists and toll formulators serve localized demand.

Market concentration is highest in can liners due to long qualification cycles and regulatory barriers, whereas niche applications remain more fragmented. Competitive differentiation centers on regulatory compliance, technical support capabilities, and regional manufacturing presence.

Recent strategic activity has focused on regional capacity expansion, BPA-NI product launches, and the development of epoxy-equivalent performance coatings. Investments in Asia-based production lines, expanded beverage-end coating portfolios, and enhanced technical service capabilities illustrate supplier efforts to secure early-mover advantages and support accelerated customer conversions.

Leading companies emphasize innovation-driven differentiation, localized production, and conversion support services. Portfolio breadth, regulatory documentation, and collaborative qualification models are key competitive tools used to secure long-term contracts with global brand owners.

Key Industry Developments

- In February 2025, PPG Industries launched the PPG Hoba Pro 2848 non-BPA internal coating for aluminum bottles at Paris Packaging Week, earning recognition at the 2025 ADF Innovation Awards and expanding its BPA-free portfolio into aluminum beverage and liquid packaging.

- In 2025, AkzoNobel Packaging Coatings introduced Accelshield 700, a BPA-non-intent internal coating for beverage can ends compliant with FDA and EU food contact regulations, enabling can manufacturers to transition away from traditional bisphenol-based systems.

Companies Covered in BPA-free Coatings Market

- PPG Industries

- AkzoNobel

- The Sherwin-Williams Company

- BASF

- ALTANA (ACTEGA)

- Allnex

- Kansai Paint

- Toyochem (Toyo Ink Group)

- Valspar

- Axalta Coating Systems

- Hempel

- Nippon Paint

- Jotun

- Berger Paints

- Siegwerk

- Sun Chemical

- DSM Coating Resins

- Covestro

- Eastman Chemical Company

- Arkema

Frequently Asked Questions

The global BPA-free coatings market is estimated to be valued at US$5.4 billion in 2026.

By 2033, the BPA-free coatings market is projected to reach US$9.3 billion.

Key trends include accelerated regulatory-driven replacement of BPA-based can linings, increased adoption of acrylic and polyester-based chemistries, expansion of waterborne and low-migration formulations, and rising supplier investment in regional production and qualification capabilities, particularly in Asia Pacific.

Acrylic-based coatings are the leading material segment, accounting for approximately 44.8% of total market demand, due to their regulatory acceptance, versatility across substrates, and compatibility with food-contact requirements.

The BPA-free coatings market is expected to grow at a CAGR of 8.1% between 2026 and 2033.

Major players with strong BPA-free product portfolios include PPG Industries, AkzoNobel, The Sherwin-Williams Company, BASF, and ALTANA (ACTEGA).