- Medical Devices

- Fluid Warmer Devices Market

Fluid Warmer Devices Market Size, Share, Trends, Growth, and Regional Forecast, 2026 to 2033

Fluid Warmer Devices Market by Product Type (Warming Devices, Temperature Probe, Disposable Accessories), by Application (Surgery / Operating Rooms, Neonatal / Infant Care, ICU / Critical Care, Blood & IV Fluid Warming, Others), End-user, and Regional Analysis from 2026 to 2033

Fluid Warmer Devices Market Share and Trends Analysis

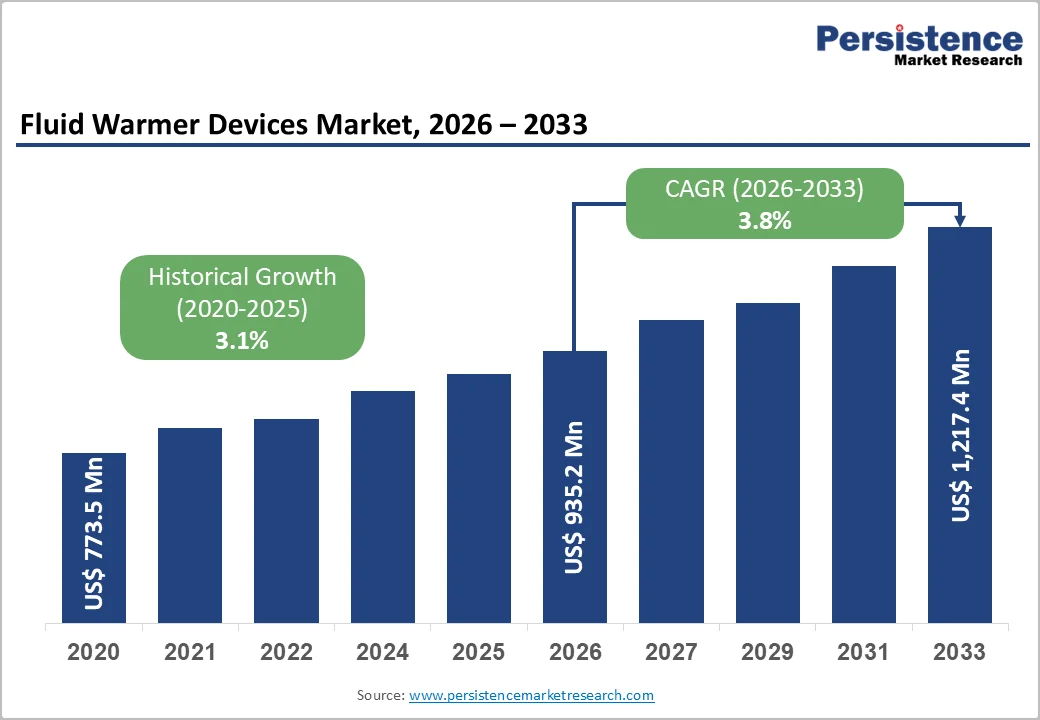

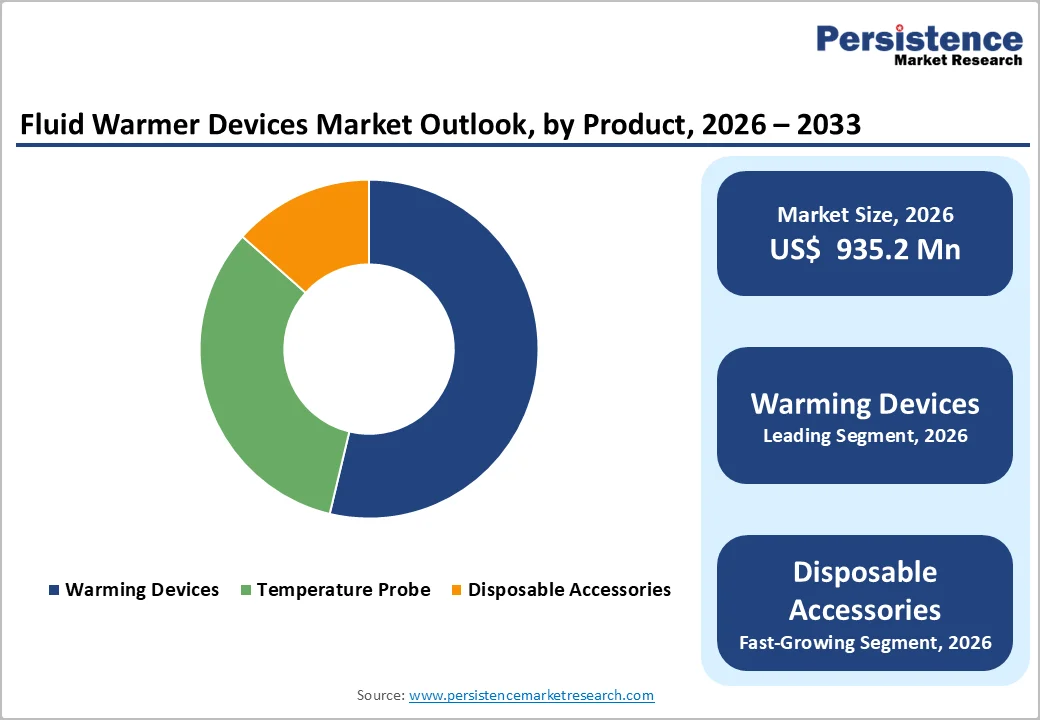

The global fluid warmer devices market size is estimated to grow from US$935.2 million in 2026 to US$1,217.4 million by 2033, growing at a CAGR of 3.8% during the forecast period from 2026 to 2033.

The global market is experiencing a steady growth driven by the prevalence of surgeries, trauma cases, and critical care procedures that require precise thermal management. These devices, including IV, blood, and fluid warmers, help prevent hypothermia and maintain patient stability during fluid transfusions or operations.

Technological advancements such as portable, battery-operated, and smart fluid warmers are boosting adoption across hospitals, surgical centers, and emergency care units. Increasing awareness of perioperative patient safety, rising geriatric population, and expanding healthcare infrastructure in emerging regions further fuel demand.

Key Industry Highlights:

- The increasing number of surgeries globally, including elective and emergency procedures, is a key growth driver.

- ICU and emergency care settings require rapid administration of fluids and blood while maintaining patient temperature.

- Infants and children are highly sensitive to temperature fluctuations. The market is seeing increased demand for neonatal and pediatric fluid warmers in NICUs and pediatric surgical units.

- Warming devices (IV warmers, blood warmers, fluid warmers) are the primary equipment used to maintain fluid temperature during transfusions, surgeries, or critical care.

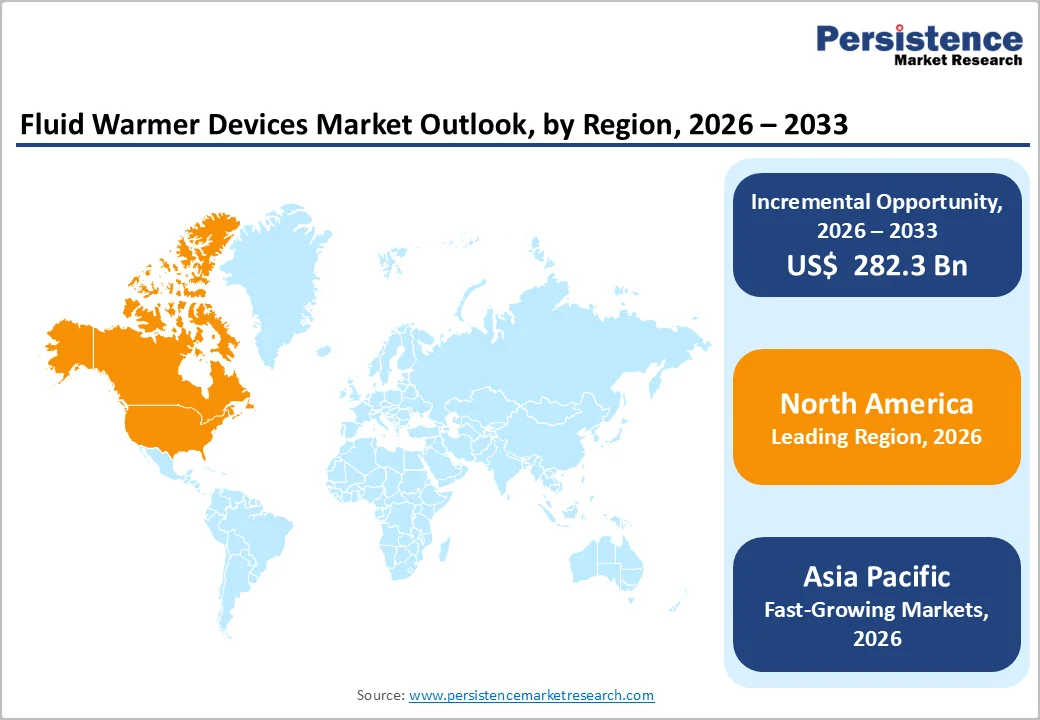

- North America leads due to a large number of surgeries, trauma cases, and ICU admissions, increasing demand for fluid warmers.

| Key Insights | Details |

|---|---|

| Fluid Warmer Devices Market Size (2026E) | US$ 935.2 Mn |

| Market Value Forecast (2033F) | US$1,217.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 3.8% |

| Historical Market Growth (CAGR 2020 to 2024) | 3.1% |

Market Dynamics

Driver - Increasing Neonatal & Pediatric Surgeries

The rising number of neonatal and pediatric surgeries is a significant driver for the fluid warmer devices market. Infants and young children are particularly vulnerable to hypothermia, as their bodies have limited capacity to regulate temperature during surgical procedures or transfusions. Even small fluctuations in body temperature can lead to complications such as delayed recovery, coagulation issues, or increased risk of infection.

To address this, hospitals and neonatal intensive care units (NICUs) are increasingly adopting specialized fluid warmers designed specifically for pediatric and neonatal patients. These devices provide precise temperature control for IV fluids and blood products, ensuring safety and stability. Growing awareness among healthcare professionals about the critical importance of thermal management in young patients is further accelerating market adoption.

Restraints - Recurring Maintenance & Consumable Costs

One of the major restraints on the adoption of fluid warmer devices is the recurring maintenance and consumable costs associated with their operation. Beyond the initial purchase, hospitals and surgical centers must continually invest in disposable sets, tubing, warming cartridges, and specialized fluid lines, which are often single-use and need frequent replacement to maintain hygiene and safety standards.

Additionally, periodic calibration, preventive servicing, and technical inspections are required to ensure accuracy and prevent device malfunctions, adding to operational expenses. For smaller hospitals or clinics with limited budgets, these cumulative costs can be substantial, making it difficult to justify frequent usage or wide-scale deployment. As a result, even when clinical benefits are clear, financial constraints limit adoption and optimal utilization.

Opportunity - Portable & Battery-Operated Warmers

The demand for portable and battery-operated fluid warmers is increasing rapidly due to the critical need for maintaining patient body temperature during pre-hospital care, emergency response, and field medical interventions. Compact, lightweight, and battery-powered devices enable healthcare providers to deliver safe and effective fluid and blood warming in ambulances, disaster zones, and remote locations where conventional power sources are unavailable.

These devices enhance patient survival by preventing hypothermia during transport or emergency procedures. Moreover, their portability allows rapid deployment in trauma care, military operations, and rural healthcare settings, making them a high-growth segment in the fluid warmer devices market.

Category-wise Analysis

By Product Type Insights

Warming Devices lead the fluid warmer market because they are the primary equipment used to maintain patient body temperature during surgeries, blood transfusions, and critical care procedures. Without these devices, temperature probes or disposable accessories cannot function independently, as they are designed to support the main warming systems.

Hospitals, ICUs, and surgical centers invest heavily in high-quality warming devices due to their critical role in preventing hypothermia, reducing complications, and improving patient outcomes. Additionally, technological advancements like portable, smart, and automated warming devices further boost adoption, making warming devices the highest-revenue and most widely used segment in the market.

By End-user Insights

Hospitals hold the largest share of the fluid warmer devices market because they are the primary centers for surgery, critical care, and emergency interventions, where maintaining patient body temperature is crucial. Operating rooms, ICUs, and trauma units require reliable and continuous fluid warming to prevent hypothermia, ensure safe transfusions, and improve surgical outcomes.

Hospitals have the infrastructure, trained staff, and budgets to invest in high-quality, advanced warming devices, unlike clinics or home care settings, which use these devices less frequently. The high patient volume and diverse clinical applications make hospitals the dominant end-user segment driving market demand and revenue.

Regional Insights

North America Fluid Warmer Devices Trends

North America leads the fluid warmer devices market, driven by advanced healthcare infrastructure, high surgical volumes, and strong patient-safety protocols. Hospitals and surgical centers in the U.S. are increasingly adopting smart, portable, and automated fluid warmers to prevent perioperative hypothermia and improve outcomes.

The region benefits from regulatory support, including FDA approvals, which help ensure device safety and encourage hospital adoption. Additionally, rising geriatric populations and growing awareness of critical care best practices boost demand. In the U.S., high healthcare spending enables investment in premium devices, while continuous technological innovation and integration with monitoring systems further strengthen North America’s dominance in the market.

Asia Pacific Fluid Warmer Devices Market Trends

The Asia Pacific fluid warmer devices market is emerging rapidly due to expanding healthcare infrastructure, increasing surgical procedures, and rising awareness of patient safety. Countries like India, China, and Japan are witnessing growing adoption of portable, cost-effective, and technologically advanced warming devices in hospitals, surgical centers, and emergency care units.

The rising prevalence of trauma cases, critical care demand, and neonatal surgeries further drives market growth. Government initiatives to modernize healthcare facilities, coupled with increasing private healthcare investments, are creating opportunities for both international and regional manufacturers. Affordability and accessibility remain key factors shaping the market in this region.

Competitive Landscape

The fluid warmer devices market is highly competitive, driven by continuous innovation and technological advancements. Companies compete on product performance, accuracy, safety features, and usability, offering portable, smart, and automated warming solutions.

Differentiation also comes through disposable accessories, integration with hospital monitoring systems, and enhanced user training. Price, regulatory compliance, and after-sales support influence purchasing decisions.

Key Industry Developments:

- In August 2025, North Texas’s QinFlow launched an advanced blood and IV fluid warming device for ICUs and operating rooms. The Plano- and Israel-based company introduced the Warrior AC Station, which delivered warm blood and IV fluids “in seconds.” This innovation addressed a critical need in hospital ORs and ICUs, where blood was typically stored at temperatures as low as 36 degrees.

Companies Covered in Fluid Warmer Devices Market

- 3M Company

- Smiths Medical (ICU Medical)

- Stryker Corporation

- Baxter International Inc.

- GE Healthcare

- Belmont Medical Technologies

- Biegler GmbH

- Barkey GmbH & Co. KG

- Vyaire Medical, Inc.

- Enthermics Medical Systems

- The 37Company

- Emit Corporation

- MEQU A/S

- Keewell Medical Technology Co., Ltd.

- Stihler Electronic GmbH

- Becton, Dickinson and Company (BD)

- Others

Frequently Asked Questions

The global fluid warmer devices market is projected to be valued at US$935.2 Mn in 2026.

The global fluid warmer devices market is driven by the rising incidence of trauma, accidents, and surgical procedures that require rapid warming of blood and IV fluids to prevent hypothermia. Growing adoption of advanced perioperative care standards, especially in emergency rooms, ICUs, and operating rooms, is boosting device demand.

The global fluid warmer devices market is poised to witness a CAGR of 3.8% between 2026 and 2033.

Rising chronic illness and home-care shift create opportunities for compact, user-friendly warmers.

3M, Smiths Medical (ICU Medical), Stryker Corporation, Baxter International Inc., Becton, Dickinson and Company (BD), and others.