- Medical Devices

- Air Fluidized Therapy Beds Market

Air Fluidized Therapy Beds Market Size, Share, and Growth Forecast, 2026 - 2033

Air Fluidized Therapy Beds Market by Application (Pressure Ulcers, Burns, Postoperative Recovery, Others), Product Type (Standard Therapy Beds, Low Air Loss Beds, Combination Therapy Beds), End-User (Hospitals, Long-Term Care Facilities, Home Care Settings), and Regional Analysis for 2026-2033

Air Fluidized Therapy Beds Market Share and Trends Analysis

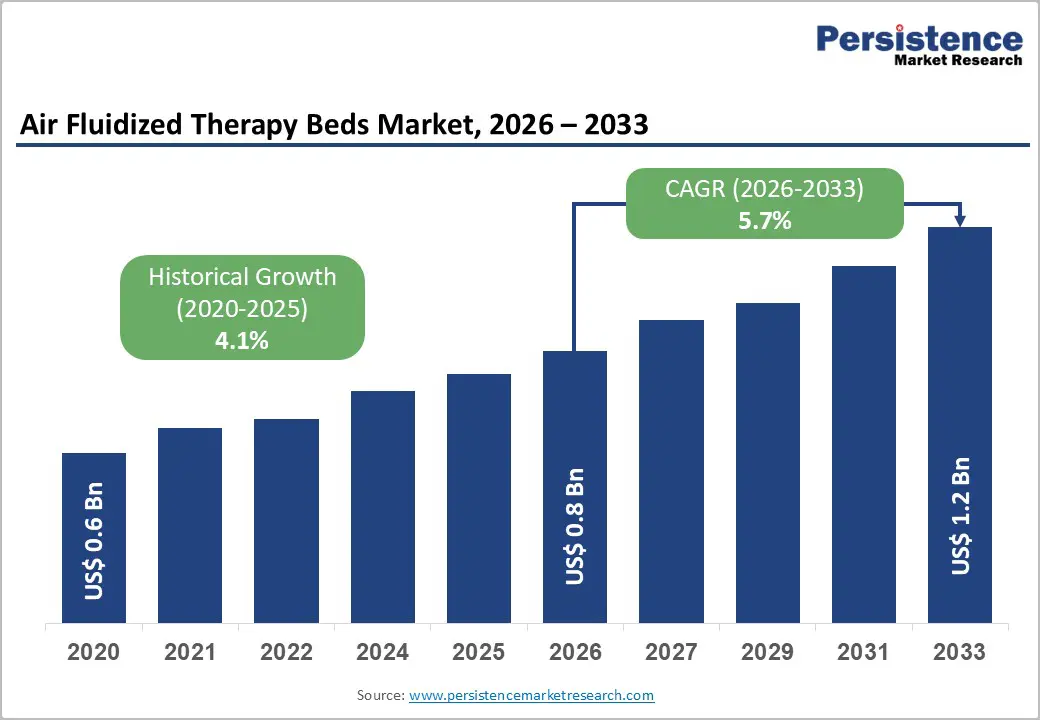

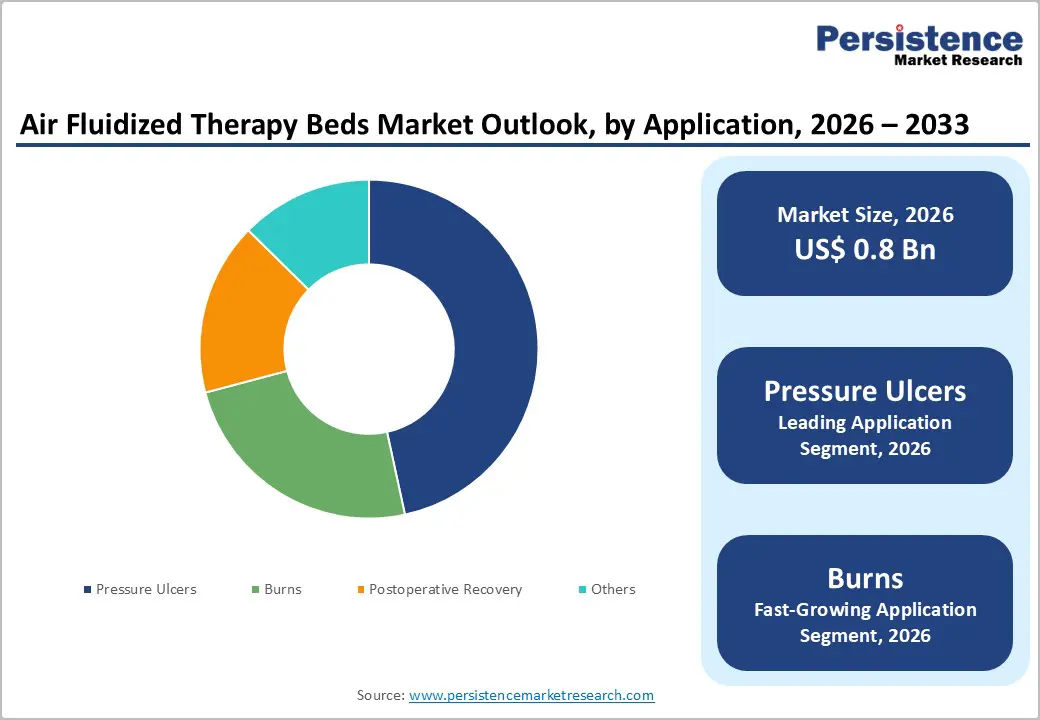

The global air fluidized therapy beds market size is likely to be valued at US$ 0.8 billion in 2026, and is projected to reach US$ 1.2 billion by 2033, growing at a CAGR of 5.7% during the forecast period 2026−2033.

Growth is primarily driven by the rising global incidence of pressure ulcers and chronic wounds, an aging population requiring advanced wound management, and increasing adoption of air fluidized therapy in intensive care and long-term care settings. Technological advancements enabling precise temperature and pressure regulation are improving clinical outcomes and expanding market penetration across acute and sub-acute care environments. Favorable reimbursement frameworks in North America and Europe are accelerating adoption, while emerging economies in the Asia Pacific present significant untapped demand corridors fueled by healthcare infrastructure development and rising medical tourism.

Key Industry Highlights

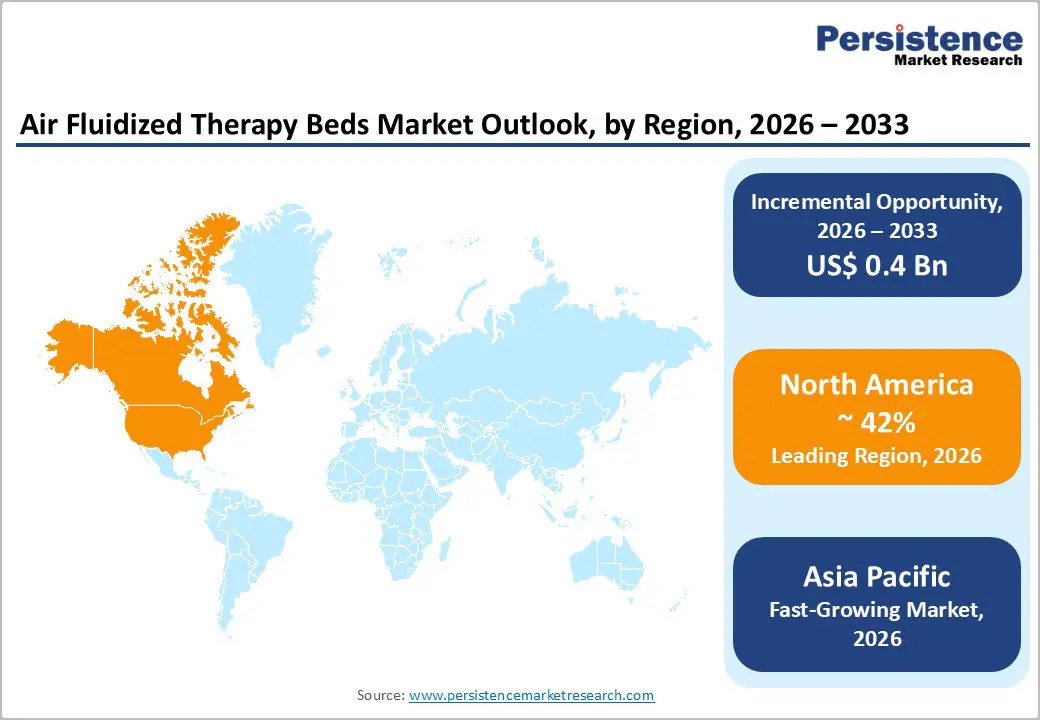

- Dominant Region: North America is expected to command about 42% market share in 2026, supported by high per-capita healthcare expenditure and a robust healthcare infrastructure.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market from 2026 to 2033, on account of increasing healthcare investments and improving medical infrastructure.

- Leading & Fastest-growing End-User: Hospitals are likely to lead the revenue share in 2026 at approximately 75%, while home care settings are expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Leading & Fastest-growing Application: Pressure ulcer are set to hold around 48% revenue share in 2026, with burns likely to grow the fastest during the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

| Air Fluidized Therapy Beds Market Size (2026E) | US$ 0.8 Bn |

| Market Value Forecast (2033F) | US$ 1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Pressure Ulcers and Chronic Wounds

Pressure ulcers are affecting more than one in ten adult hospital patients, according to the World Health Organization (WHO). These injuries are representing a major yet preventable patient safety challenge and often signal declining clinical status. Global incidence has exceeded about 2.47 million cases in 2021, more than double the level recorded in 1990. Prevalence is rising sharply in high Socio-Demographic Index (SDI) regions and aging populations. This pattern is strengthening the need for advanced therapeutic support surfaces that are addressing sustained pressure and impaired tissue perfusion.

Air fluidized therapy beds are addressing this clinical requirement by redistributing body weight across a layer of silicone-coated beads. The system is lowering interface pressure below capillary closing pressure, a key threshold associated with pressure injury formation. Clinicians are validating these beds because the technology directly targets the primary mechanical driver of tissue damage. Hospitals are integrating these systems into structured wound management programs to improve recovery outcomes and reduce complications among immobile patients. The technology is also supporting long-duration immobility management in critical and chronic care environments.

Technological Advancements in Fluidized Bed Design and Connectivity

Manufacturers are integrating Internet of Things (IoT) sensors into next generation air fluidized therapy beds to improve clinical monitoring and operational efficiency. These systems are delivering real time pressure mapping and automated temperature control. Smart algorithms are adjusting fluidization levels based on patient movement and physiological requirements. Integrated weight detection is ensuring accurate support distribution across the therapy surface. Beds are also connecting with electronic health records (EHRs), which allows seamless data exchange with hospital information systems. Care teams are accessing patient metrics easily, enabling faster decisions in high acuity settings. Remote monitoring capabilities are allowing clinicians to adjust parameters proactively and reduce the risk of pressure injury progression.

Regulatory support is also accelerating technological adoption. The U.S. Food and Drug Administration (FDA) is approving innovative therapeutic surface devices through the De Novo classification pathway, which is shortening product development cycles and improving market entry timelines. As a result, manufacturers are increasing investment in research and development to strengthen product differentiation and clinical performance. Advanced engineering features are enabling improved outcomes for complex wound cases, enabling premium product positioning. Healthcare providers are justifying investments in these technologies through reduced complications and faster patient recovery.

Regulatory Complexity and Reimbursement Limitations

Manufacturers are encountering regulatory complexity across major healthcare markets. In the United States, the FDA requires 510(k) clearance for therapeutic support surface devices, which involves extensive clinical testing and detailed technical documentation. European markets require Conformité Européenne (CE) marking, which enforces strict safety and performance verification. These regulatory procedures are extending product approval timelines and increasing compliance costs. Companies are allocating significant resources to audits, design modifications, and certification processes to satisfy diverse regional standards. While governments are enforcing these frameworks to protect patient safety, the requirements are slowing technology deployment and limiting participation by smaller manufacturers.

Reimbursement policies are also restricting broader adoption. For instance, the Centers for Medicare and Medicaid Services (CMS) in the U.S. are covering air fluidized therapy beds only for severe clinical cases such as Stage III or Stage IV pressure ulcers that have not responded to prior treatment. Healthcare providers must submit detailed clinical evidence to confirm patient eligibility. This requirement is narrowing access and discouraging routine deployment across hospital systems. European healthcare systems are applying different reimbursement criteria across member states, which is creating uncertainty for procurement teams. Emerging markets are presenting an additional constraint as formal reimbursement structures are often absent. Healthcare facilities are also hesitating to invest in specialized therapy beds without predictable financial support in these countries, limiting market expansion.

Infection Prevention Concerns and Evolving Decontamination Standards

The air fluidized therapy beds market growth is facing rising pressure from infection prevention and decontamination requirements. Silicone microsphere media are delivering effective pressure redistribution but can accumulate microbial contaminants over time. The bead matrix can trap pathogens such as multi drug resistant organisms (MDROs), including Clostridioides difficile, Methicillin-resistant Staphylococcus aureus (MRSA), and carbapenem resistant Enterobacteriaceae (CRE). These risks are affecting immunocompromised patients and individuals with open wounds most severely. Hospitals are strengthening inspection routines and environmental monitoring to reduce contamination risks associated with porous therapeutic surfaces.

Public health authorities are tightening infection control standards for clinical environments. The U.S. CDC and the European Centre for Disease Prevention and Control (ECDC) are issuing stricter environmental cleaning guidance for healthcare equipment. Regulators are applying closer scrutiny to particulate based surfaces used in therapeutic beds. Hospitals are shortening bead replacement cycles and are validating sanitation procedures more rigorously, while facilities with limited infection control resources are prioritizing equipment that is easier to sanitize. These actions are increasing operational workloads for clinical staff and facility management teams.

Technological Advancements & Continuous Research and Development

Technological progress is creating strategic opportunities in the air fluidized therapy bed market. Manufacturers are increasing research and development investment to introduce systems with integrated sensors that monitor patient parameters in real time. These smart beds are enabling remote oversight from centralized nursing stations, which improves clinical responsiveness and operational efficiency. Advanced materials are strengthening structural durability and patient comfort during extended immobilization. Such capabilities are addressing performance gaps in conventional therapeutic surfaces and are supporting precision driven wound care management. Healthcare providers are adopting these technologies to tailor treatment protocols, improve monitoring accuracy, and optimize resource utilization in high acuity care settings.

Next-generation designs are incorporating artificial intelligence (AI)-based predictive adjustments that respond to patient movement patterns and shifting pressure distribution. This functionality is generating detailed clinical analytics that allow care teams to refine treatment strategies and track recovery progression more effectively. Patients are experiencing fewer complications and shorter healing periods as a result. Manufacturers are differentiating products through intuitive interfaces and modular architectures that adapt to varied clinical environments. Hospitals are prioritizing systems with validated outcome improvements to meet regulatory expectations and strengthen care quality. Companies that align innovation with clinical evidence can establish long-term partnerships with healthcare providers and strengthen their competitive positioning.

Home Care and Ambulatory Settings Adoption

The shift toward home based healthcare delivery is expanding opportunities for air fluidized therapy beds. The COVID-19 pandemic has accelerated patient preference for treatment outside hospital settings. Rental and leasing models are enabling access without major upfront expenditure. In the United States, Medicare Part B is supporting rental coverage for patients with severe wound conditions, which is opening structured entry into home care channels. Families are gaining access to advanced therapeutic support surfaces, while caregivers are managing treatment more confidently in residential environments. Manufacturers are responding by designing systems that align with the clinical and logistical requirements of home healthcare services.

Companies are introducing compact and portable bed systems suited for domestic use. Lightweight frames are improving mobility during repositioning or relocation within homes. Energy efficient mechanisms are lowering electricity demand, which reduces operational costs. Simplified user interfaces are guiding non-professional caregivers through routine operation and maintenance tasks. Remote monitoring applications are allowing clinicians to track patient progress and adjust therapy parameters without requiring hospital visits. This approach is reducing readmission risk and supporting independent living among aging populations. Manufacturers are strengthening market presence through maintenance services and partnerships with medical equipment rental networks that expand distribution across home care ecosystems.

Category-wise Analysis

Application Insights

Pressure ulcer treatment is anticipated to dominate in 2026 by holding an estimated 48% of the air fluidized therapy beds market revenue share. Strong clinical evidence is supporting the effectiveness of these beds in treating Stage III and Stage IV pressure injuries. Guidance from the Wound, Ostomy and Continence Nurses Society (WOCN) is reinforcing their role in advanced wound management. Hospitals are upgrading therapeutic support surfaces for high risk patients as part of institutional care protocols.

Reimbursement policies are also strengthening adoption. Programs such as Medicare in the United States and comparable European healthcare schemes are covering air fluidized therapy beds for severe pressure ulcer treatment, which is sustaining consistent procurement across hospital systems.

Burn care is likely to emerge as the fastest-growing application area for the 2026-2033 forecast period. Air fluidized beds lay down a stable therapeutic surface that reduces shear forces and friction, which supports tissue protection during burn recovery. The system is also maintaining controlled temperature conditions that assist wound healing. Specialized burn treatment centers are expanding across North America and the Asia Pacific region, which is increasing equipment demand.

Rising occupational and domestic burn injuries are also contributing to higher utilization. Major hospitals in the United States and Europe are upgrading therapeutic bed infrastructure within burn units, which is strengthening unit sales and accelerating segment growth.

End-User Insights

Hospitals are poised to command an approximate 75% of the air fluidized therapy beds market share in 2026, given their central role in bolstering critical care environments such as intensive care units (ICUs), burn treatment centers, and postoperative recovery wards. Advanced therapeutic surfaces are reducing pressure injury risk and improving wound healing outcomes among high acuity patients. Rising hospital admissions are strengthening procurement as healthcare providers expand infrastructure to manage patient volume and complexity. Investment in specialized support surfaces is also helping institutions meet clinical quality standards and patient safety requirements.

Home care settings are expected to chart the highest growth trajectory between 2026 and 2033. Expansion of home healthcare services is aligning with patient preference for treatment within familiar residential environments. Air fluidized therapy beds designed for home use are delivering therapeutic functions such as pressure redistribution and wound stabilization comparable to hospital grade systems. Simplified operation is enabling family caregivers to manage therapy effectively. This model is gaining traction among households managing chronic illness and mobility limitations. Demand is also likely to surge as aging populations prioritize independent living and shorter hospital stays.

Regional Insights

North America Air Fluidized Therapy Beds Market Trends

North America is predicted to account for about 42% of the air fluidized therapy beds market value in 2026, on the back of strong healthcare expenditure that is enabling hospitals to invest in advanced therapeutic equipment. Well-developed clinical infrastructure is supporting reliable distribution, installation, and servicing networks. Healthcare providers are showing high awareness of specialized wound care technologies, which is accelerating adoption across acute care facilities.

Major manufacturers are operating in the region, which is strengthening product innovation and clinical validation cycles. Hospitals are integrating air fluidized therapy beds into treatment protocols for high risk patients as chronic disease prevalence and population aging increase the need for pressure injury prevention systems.

Regulatory and reimbursement frameworks are reinforcing market stability. The CMS are providing additional support in terms of reimbursement for severe pressure ulcer treatment, which is encouraging procurement among healthcare institutions. Academic research centers are collaborating with manufacturers to refine product design and improve therapeutic outcomes. As patient complexity rises, hospitals and long term care facilities are prioritizing technologies that reduce complications and improve recovery efficiency. These factors will have sustained regional leadership while international manufacturers pursue partnerships to access the mature North America healthcare market.

Europe Air Fluidized Therapy Beds Market Trends

Europe represents a vital market for air fluidized therapy beds due to its well-established and robust public healthcare systems and structured wound management programs. Hospitals are integrating advanced therapeutic surfaces into routine care to manage complex pressure injuries. Countries such as Germany, France, and the United Kingdom are leading regional demand through extensive hospital networks and standardized treatment protocols. Healthcare providers are upgrading equipment to comply with clinical guidelines that prioritize patient safety and treatment efficiency.

Rising prevalence of chronic diseases and pressure ulcers is increasing demand for specialized pressure redistribution systems. Rapid growth of the geriatric population across Europe is also strengthening the need for preventive wound care technologies.

Government initiatives are supporting healthcare infrastructure upgrades and higher treatment standards across both public and private facilities. Regulatory oversight from institutions such as the European Medicines Agency (EMA) is facilitating approval pathways for innovative therapeutic devices. Hospitals are collaborating with manufacturers to deploy systems tailored for high risk clinical units. Budget constraints are encouraging procurement teams to select cost efficient solutions that deliver measurable clinical outcomes.

As demographic pressure increases, healthcare providers are prioritizing technologies that reduce complications and improve care efficiency. Manufacturers are strengthening market presence through localized service networks, clinical training programs, and long term hospital partnerships.

Asia Pacific Air Fluidized Therapy Beds Market Trends

Asia Pacific is well-positioned to emerge as the fastest-growing market for air fluidized therapy beds during the 2026-2033 forecast period. Governments across the region are increasing healthcare expenditure to modernize medical systems and expand treatment capacity. New hospital construction and equipment upgrades are strengthening clinical infrastructure. China and India have been raising healthcare budgets for several years to improve care quality and expand access to advanced medical technologies.

Urbanization and changing dietary patterns are increasing the prevalence of chronic conditions, which is raising the risk of pressure injuries among vulnerable populations. Professional training programs and clinical awareness campaigns are also strengthening understanding of advanced wound care technologies among healthcare providers.

Healthcare facilities in the region are expanding to meet the needs of large and aging populations. Hospitals are integrating air fluidized therapy beds into treatment protocols for patients with limited mobility and complex wounds. Local manufacturers are adapting product design to regional climate conditions and patient characteristics, which improves usability and clinical acceptance. Governments are collaborating with medical equipment suppliers to equip public hospitals with advanced therapeutic surfaces.

As regional economies strengthen, manufacturers are localizing production to reduce import dependence and accelerate distribution. These factors are positioning Asia Pacific as a major growth center for advanced wound care technologies.

Competitive Landscape

The global air fluidized therapy beds market is moderately consolidated, with leading manufacturers such as Arjo AB, Baxter International, Stryker Corporation, Invacare Corporation, and Sizewise holding a combined share of about 55% to 60%. These companies are shaping industry dynamics through product development initiatives, strategic partnerships, and mergers and acquisitions. Their scale, distribution networks, and clinical expertise are allowing them to respond quickly to rising demand for advanced therapeutic support surfaces across hospitals and specialized care facilities.

Competitive intensity is encouraging manufacturers to invest in research and development to introduce beds with enhanced clinical functionality. Product differentiation is focusing on features such as integrated sensors, simplified user interfaces, and improved patient monitoring capabilities. These innovations are helping healthcare providers manage complex wound cases more effectively while improving operational efficiency. Market leaders are aligning technological development with clinical requirements, which is strengthening product credibility and accelerating adoption across modern wound care programs.

Key Industry Developments

- In February 2026, Aurora Manufacturing unveiled the HydroAire 3000 air fluidized therapy bed that uses silicone coated microspheres fluidized by air to create a flotation surface that redistributes pressure and supports tissue regeneration. It is indicated for severe wounds such as Stage III and Stage IV pressure ulcers, burns, and complex surgical wounds, helping reduce interface pressure and improve healing outcomes.

- In August 2025, engineers at the University of California, Los Angeles (UCLA) designed an alternating-pressure mattress that redistributes pressure locally across the bed surface using embedded sensors and mechanical actuators. The system adjusts support based on real-time patient data such as weight and body position, enabling more precise pressure control than conventional air chamber mattresses. The prototype also improves airflow and reduces fluid buildup, while replaceable sensor-embedded foam components simplify cleaning and maintenance.

Companies Covered in Air Fluidized Therapy Beds Market

- Arjo AB

- Baxter International / Hill-Rom

- Stryker Corporation

- Sizewise

- Invacare Corporation

- Joerns Healthcare

- Medline Industries

- Drive DeVilbiss Healthcare

- Winncare Group

- Huntleigh Healthcare

- Apex Medical Corporation

- Karman Healthcare

- Blue Chip Medical Products

- Umano Medical

Frequently Asked Questions

The global air fluidized therapy beds market is projected to reach US$ 0.8 billion in 2026.

The market is driven by rising pressure ulcer incidence from aging populations and chronic conditions.

The market is poised to witness a CAGR of 5.9% from 2026 to 2033.

Home healthcare expansion and smart sensor integrations are producing prime growth avenues for market players.

Arjo AB, Baxter International, Stryker Corporation, Invacare Corporation, and Sizewise are some of the key players in the market.